13 min read

—

AI and machine learning offer the AI-first insurers a competitive edge over their rivals. Here is an overview of the latest advancements in the AI insurance space and their real-world applications.

2020 was a rough patch for most insurance companies.

The global pandemic imposed over $55 billion in losses—a figure second only to the impact of Hurricane Katrina.

However, this year once again reinforced the importance of technology, especially cloud computing and artificial intelligence (AI), for the sector.

Here are the numbers—

Over 76% of insurance executives report that the stakes for innovation have never been higher.

In 2021, over 40% of CIOs plan to increase their spending on AI use cases and pilot projects.

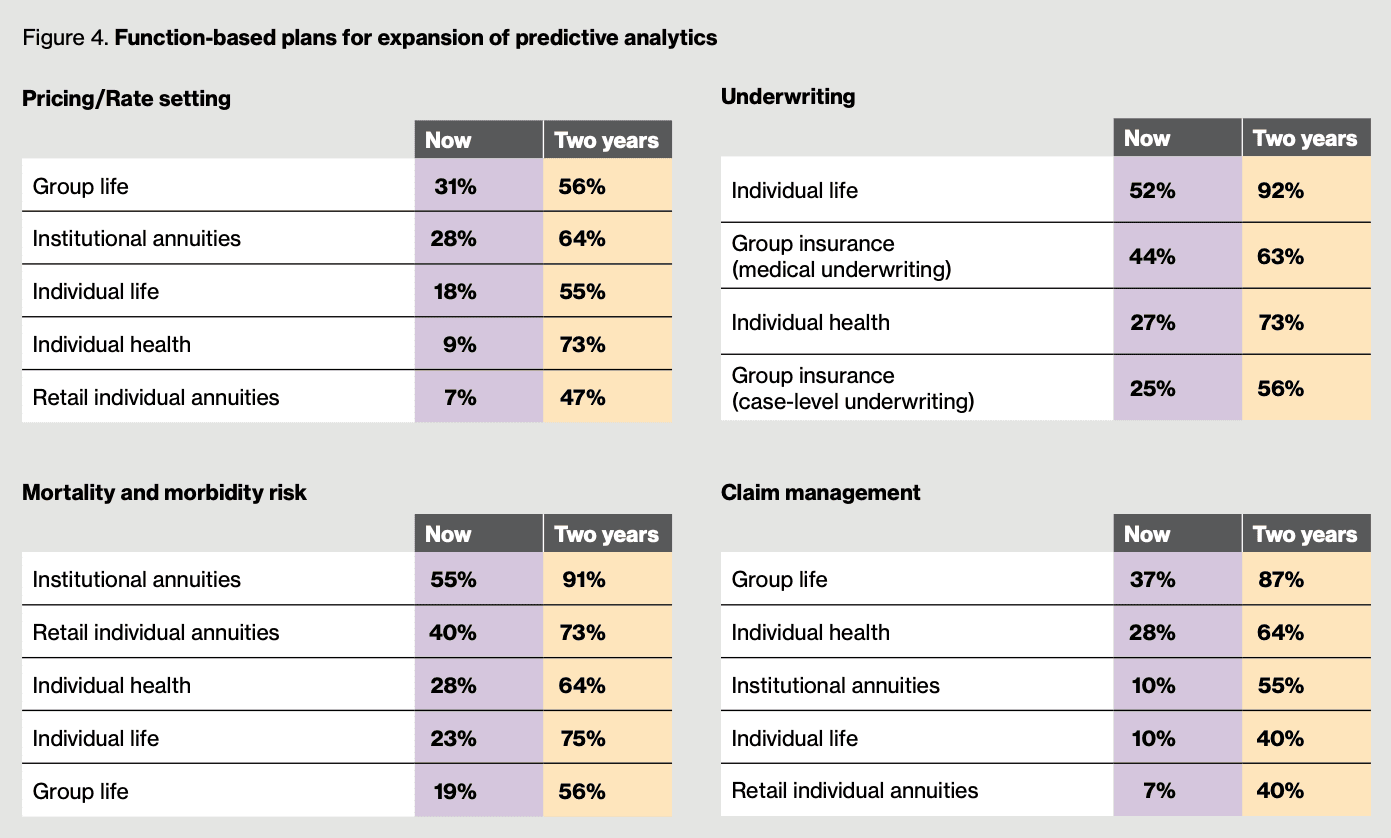

A 2019 survey of life insurers by Willis Towers Watson notes that over half of respondents expect to use predictive analytics for underwriting by shortly or after 2020.

What does it mean?

Investments in artificial intelligence (and umbrella technologies such as machine learning, deep learning, predictive analytics, and big data analytics) rank particularly high on decision-makers agendas.

And for a good reason—

They clearly pay off.

Ultimately, McKinsey estimates that across functions and use cases AI investments can drive up to a whopping $1.1 trillion in potential annual value for the insurance industry.

So, what are those billion dollars deep pockets of value for insurance companies?

Let's have a look.

AI for document processing

Give your insurance team AI agents that actually work

Get started today

1. Streamlined Claims Processing

Intelligent automation drives the best ROI for repetitive, standardized, and attention-demanding workflows. Claims management is a great example of such.

Here's why—

Largely paper-based and rarely end-to-end digitized, the claims management process can eat up to 50%-80% of premiums’ revenues.

Being primarily manual, claims processing is also prone to errors and inefficiencies, which further drive up the insurers’ operating costs.

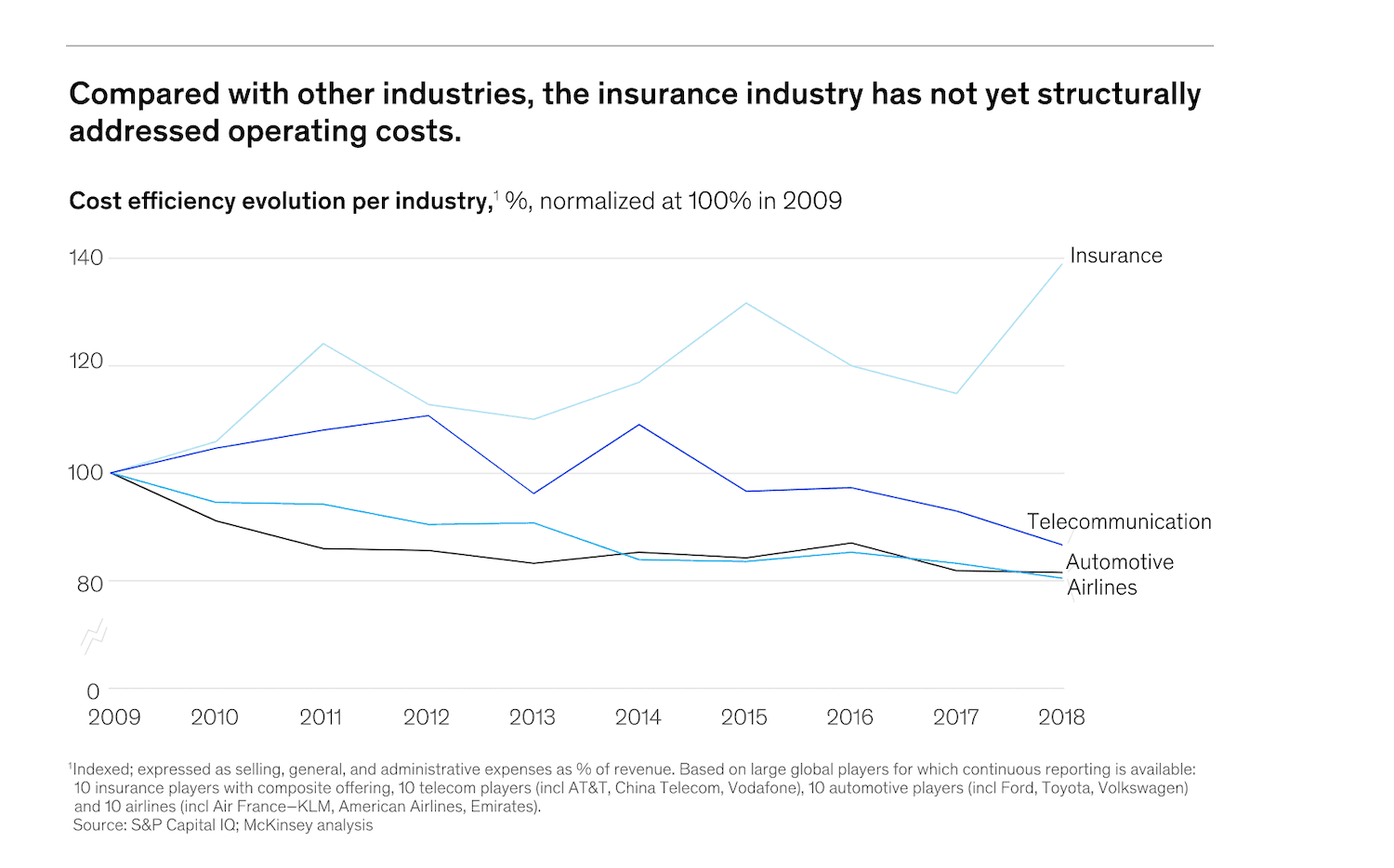

As McKinsey stated at the beginning of 2019, larger insurance carriers haven’t quite addressed the costs of services delivery:

Soundly, in 2021 many insurance companies put plans for achieving greater operational efficiency with the help of emerging technologies including:

AI (machine learning and deep learning)

RPA (robotic process automation)

IoT (internet of things).

In particular, the increase in connectivity—telematics and onboard computers in cars, smart home assistants, fitness trackers, healthcare wearables, and other types of IoT devices—now allows insurers to automatically collect more comprehensive data from customers.

They can then infuse it into their underwriting and claims management tasks to make both faster, more agnostic, and less error-prone.

More data equals better decision-making and reduced risks.

Yet at the same time, larger data volumes require more advanced (and secure) means for processing it.

That’s where artificial intelligence algorithms come to the fore.

Machine learning algorithms can effectively scan all the incoming data, interpret it instead of insurance agents, and provide faster settlement to end-users.

The best part?

With sufficient training data, machine learning and deep learning algorithms can self-improve over time without explicit programming, meaning that your teams gain access to even more accurate and complex insights.

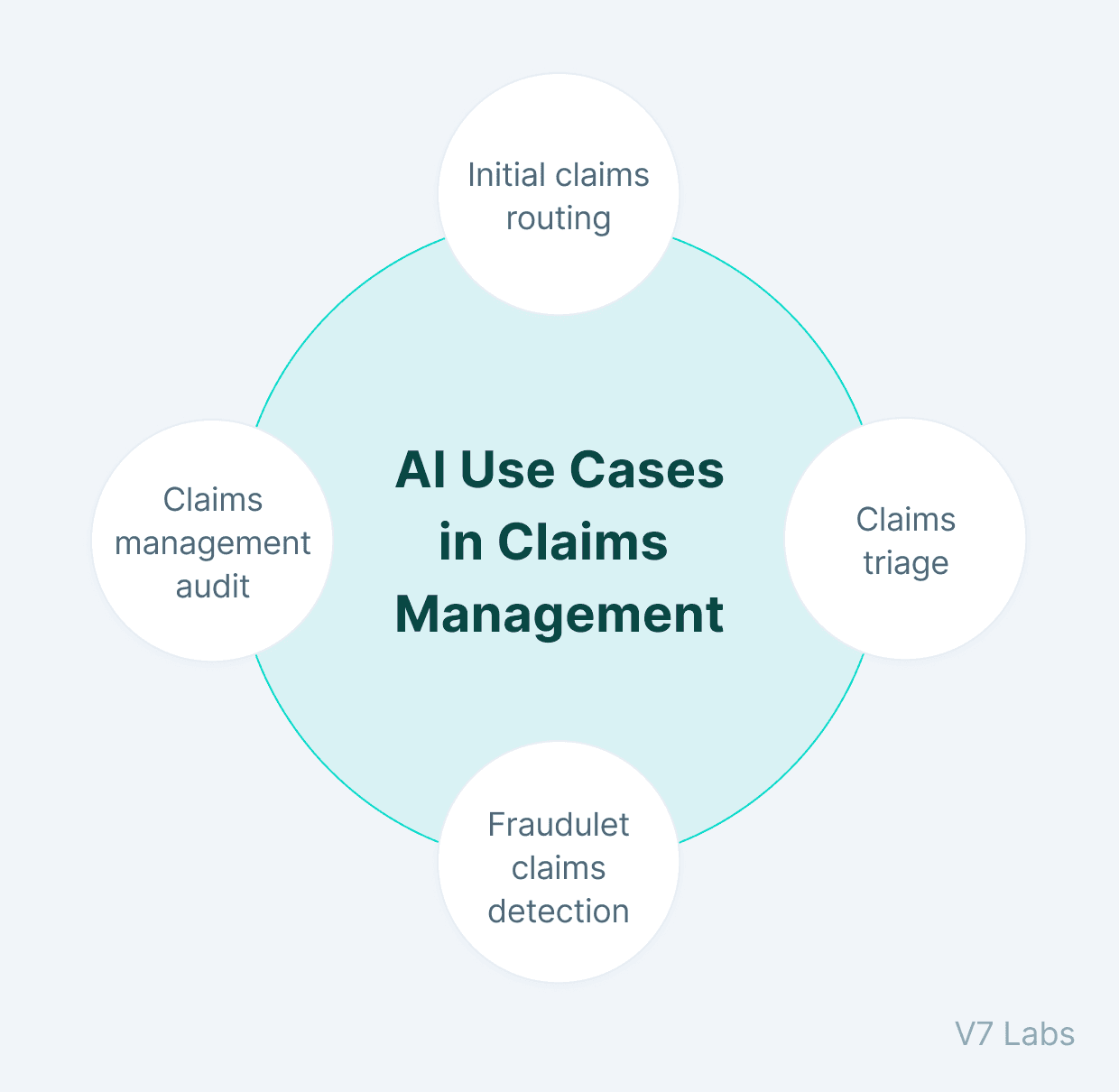

Some of the popular AI use cases in claims management include:

Initial claims routing

Claims triage

Fraudulent claims detection

Claims management audit

Just have a look at Fukoku Mutual Life—a Japanese life insurer that incorporated an AI-backed app for medical claims processing.

Fukoku Mutual Life—Leveraging AI for handling claims data

Based on Watson IBM, the app can automatically access all medical files, related to the case, mine them for relevant information, and auto-calculate accurate pay-outs, based on all the collected insights. The pay-out is forwarded to a human agent who approves and releases it.

The results?

Post-adoption, the staff’s productivity improved by 30% and the pay-out accuracy rates also shifted positively.

Fukou Mutural Life is not an odd case—each year more and more insurance providers consider implementing AI solutions for their claims processes.

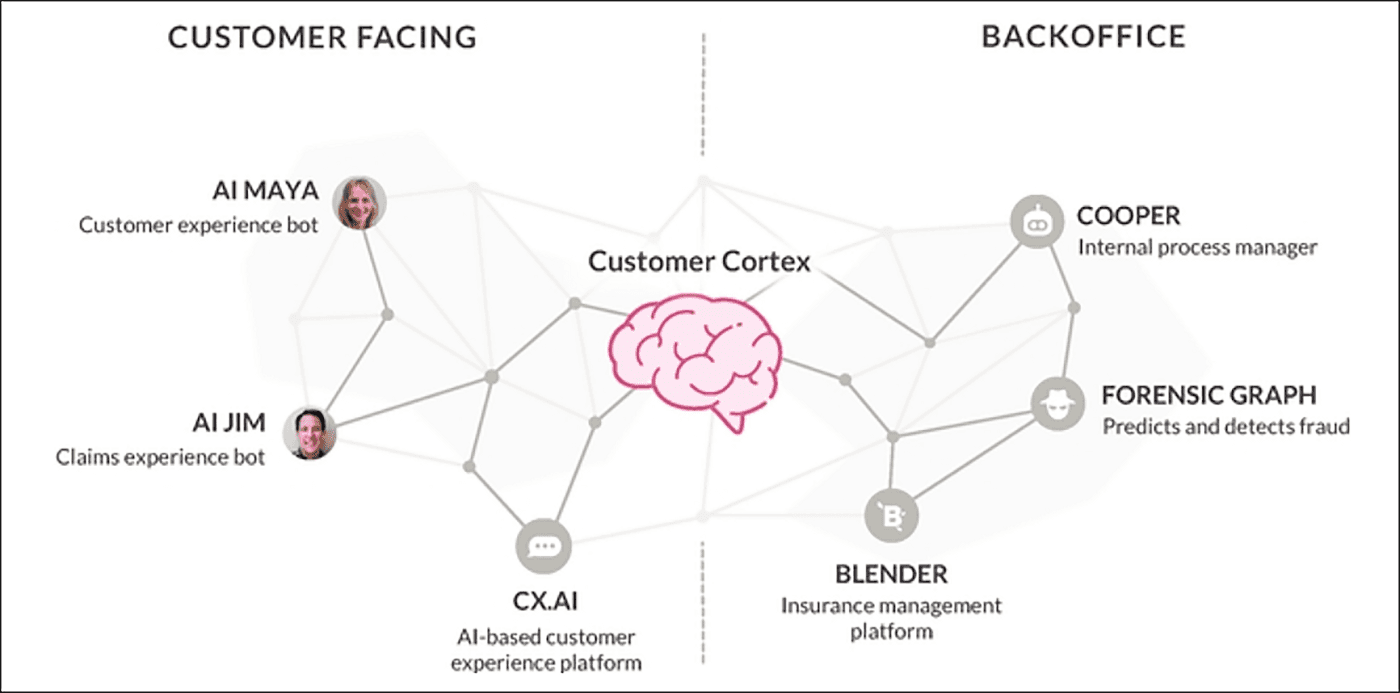

Lemonade—Using AI chatbots to compete with giant insurance companies

Lemonade, an InsureTech startup, valued at $3.9 billion during the IPO in 2020, is another strong example of AI in insurance.

The startup relies on a host of big data analytics and machine learning models to power an array of end-to-end insurance tasks.

Doing so has allowed them to undercut bigger players in terms of price, customer acquisition speed, and overall customer experience and customer engagement. A fully digital and deadpan simple insurance purchase process has made Lemonade a top insurer for younger consumers.

For example, Jim—the AI claims experience bot, can handle the entire claims process without a hitch. In 2019, Jim dealt with 20,000 claims and other customer queries and paid out over $2.5 million with no human involvement.

The morale?

The implementation of AI solutions such as AI-enabled bots can well across various business lines—chatbots can help to improve customer service, collect and analyze personal data, or process claims all while decreasing the workflow in business operations and reducing costs.

2. Accelerated Claims Adjudication

Insurance providers and customers both want fast cycle time.

Artificial intelligence plans to bring up that speed by taking over some of the labor-heavy and oftentimes downright dangerous inspection tasks.

Why does it matter?

Just consider this—

In the US, property insurance rate adjusters get injured 4X times more often than construction workers! Pretty crazy, huh?

AI systems, paired with supporting hardware for data collection, can make evidence gathering and appraisal sessions a lot safer and faster.

For example—

Property adjusters use drones that are equipped with computer vision technology in order to assess roof damage more efficiently and provide an estimation of repair costs to the owner. They can also do the same for inspecting industrial equipment (for example oil pipes), fields and crops, or an early eye view of an area and assets, affected by the natural disaster.

AI-based claims management systems can effectively process:

Geospatial data (GIS) data, collected by satellites

HD video or imagery, shot by a drone

IoT data sets, including temperature, pressure, object position, and more

All of these data sources can provide a wholesome picture of the on-site assets.

Plus, such datasets can be more accurately appraised with ML/DL algorithms, rather than the human eye alone.

Let's have a look at the company that used Ai and machine learning to master this process in the auto insurance sector.

Tokio Marine—Implementing advanced image recognition to estimate repair costs

Auto-insurer Tokio Marine recently deployed an AI-based computer vision system for examining and appraising damaged vehicles.

The average cycle time for auto accident claims in Japan is 2-3 weeks.

Tokio Marine expects to significantly shorten the processing time by relying on AI-churned estimates for repairs, paint, and blend operations produced based on the damage images.

Other insurers such as Allstate, MetLife, and Esurance among others, also accept vehicle photos as part of the claims submission process. However—

Not all of them are leveraging image recognition to speed up the appraisal process and improve customer satisfaction by proving faster, more accurate settlements.

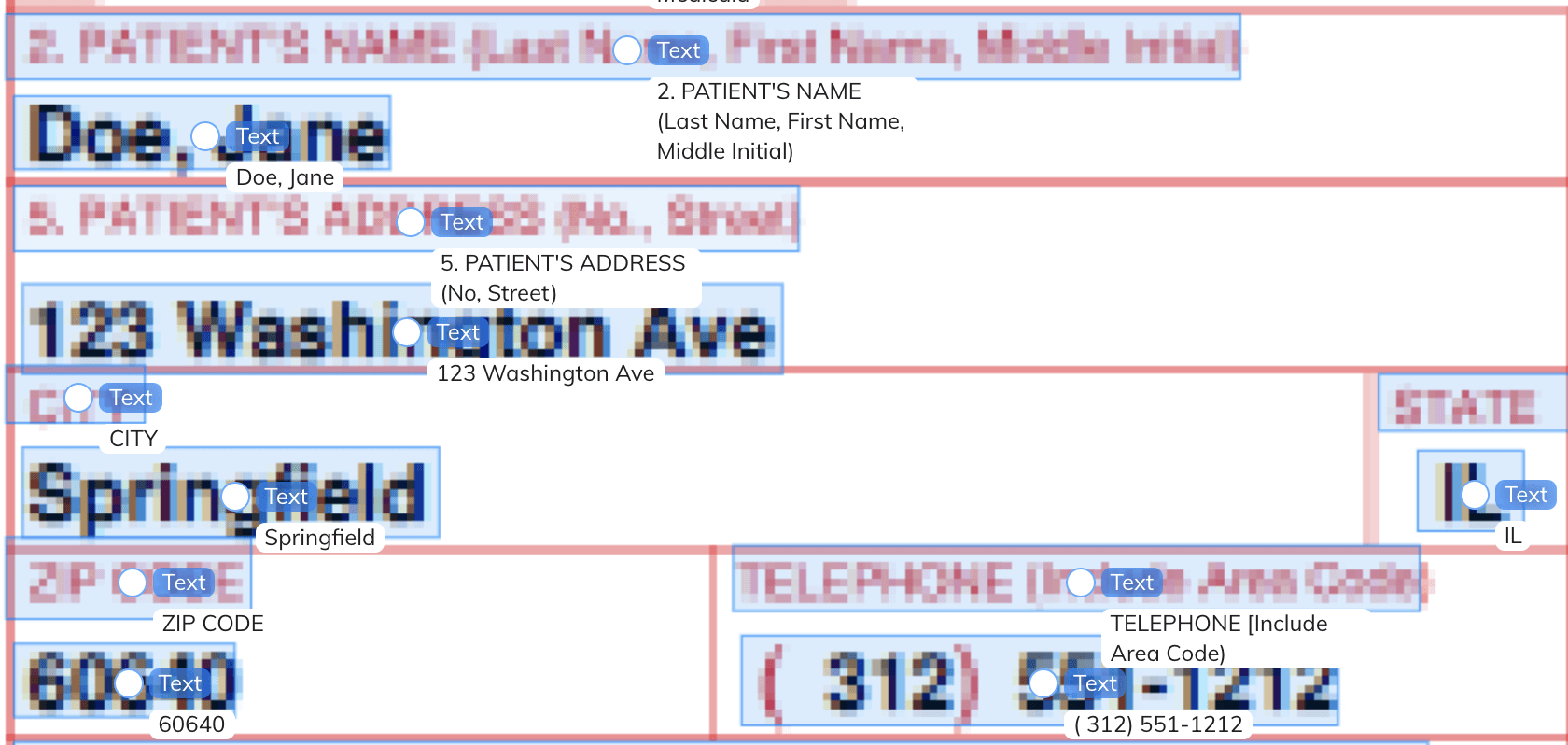

3. Rapid Document Digitization with OCR

OCR stands for optical character recognition—a tech-enabled process of recognizing hand-written digits and texts.

Since legacy insurers still largely rely on paper-based forms and print documents, OCR can be a major game-changer for improving operational efficiencies.

V7's built in Text Scanner on a low resolution insurance document

Instead of manually re-typing information, insurance agents can be empowered with automated systems, accurately capturing and reconciling data from paper-based forms, and augmenting it with inputs from other sources.

When paired with computer vision, OCR technology can accurately render every pixel and translate it to a respective digital input. Then validate the submission against other entries in the database.

Such an increased state of automation can drive up to 80% in cost savings for individual processes.

In addition, OCR applications can be deployed to improve new customer onboarding and the KYC process.

All the necessary data can be extracted from ID photos and added to the customer profile in mere seconds, rather than days. This way insurers can digitally onboard customers through web portals and mobile apps, akin to Lemonade, and majorly reduce the onboarding costs, while increasing the speed and customer satisfaction factors.

Given that the pandemic has added a new premium on performance for insurers, streamlined customer acquisition isn’t an area you’d want to skim on.

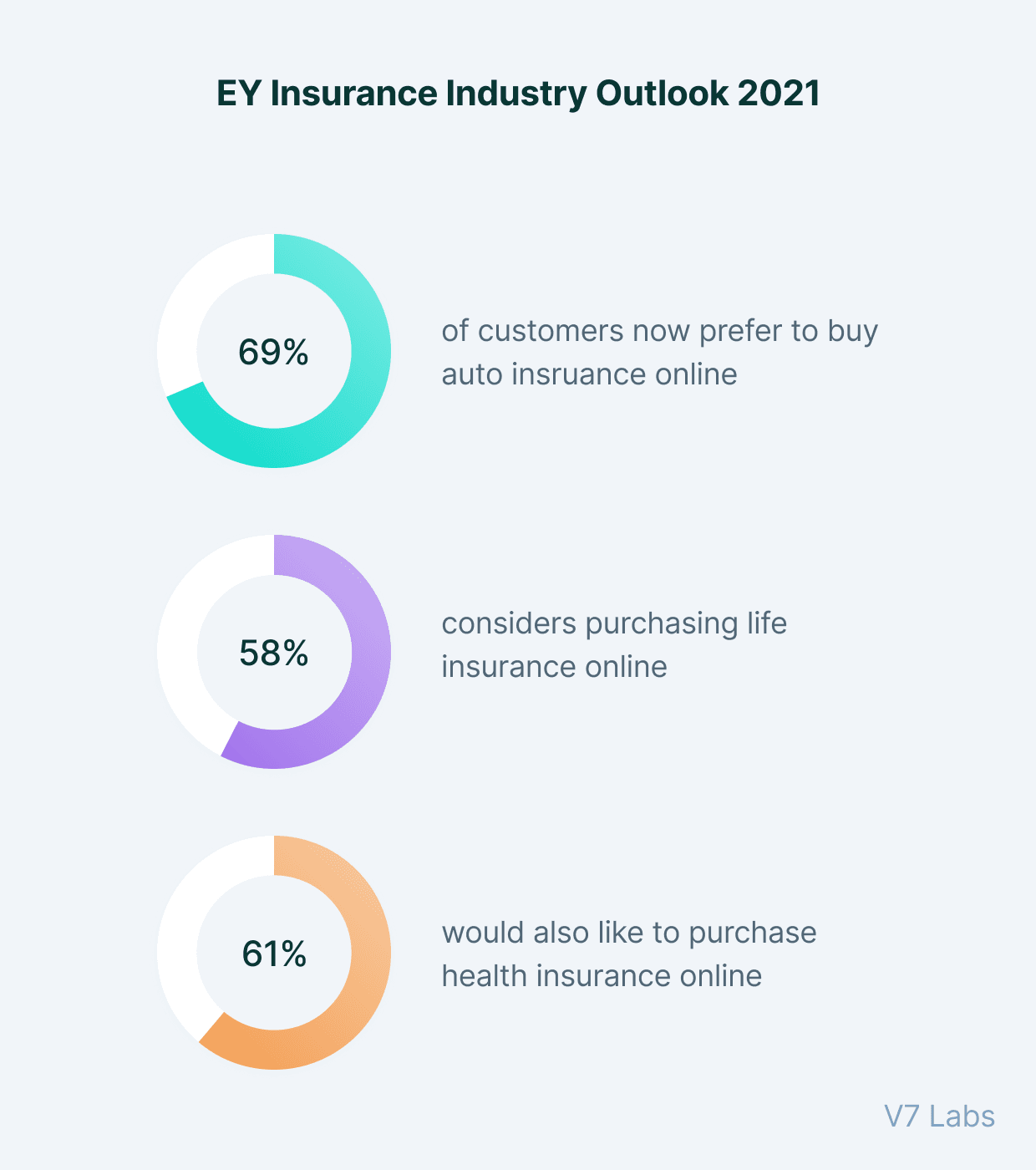

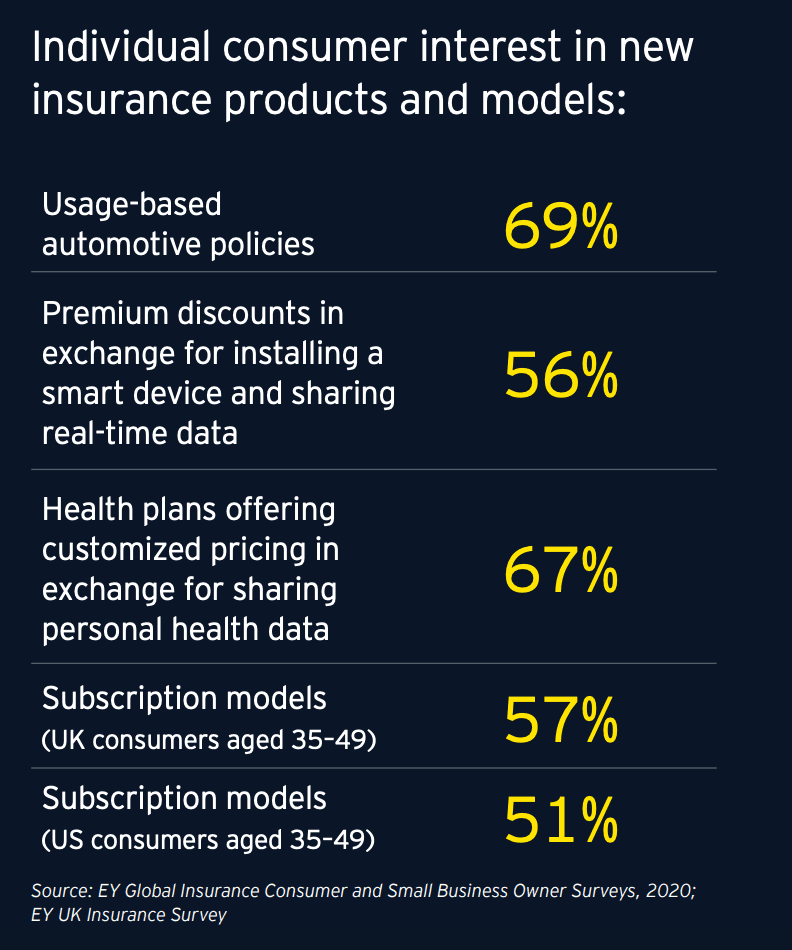

EY Insurance Industry Outlook 2021 reports that:

69% of customers now prefer to buy auto insurance online

61% would also like to purchase health insurance online

58% considers purchasing life insurance online

The numbers don't lie, and companies that take them seriously are the ones staying ahead of the curve.

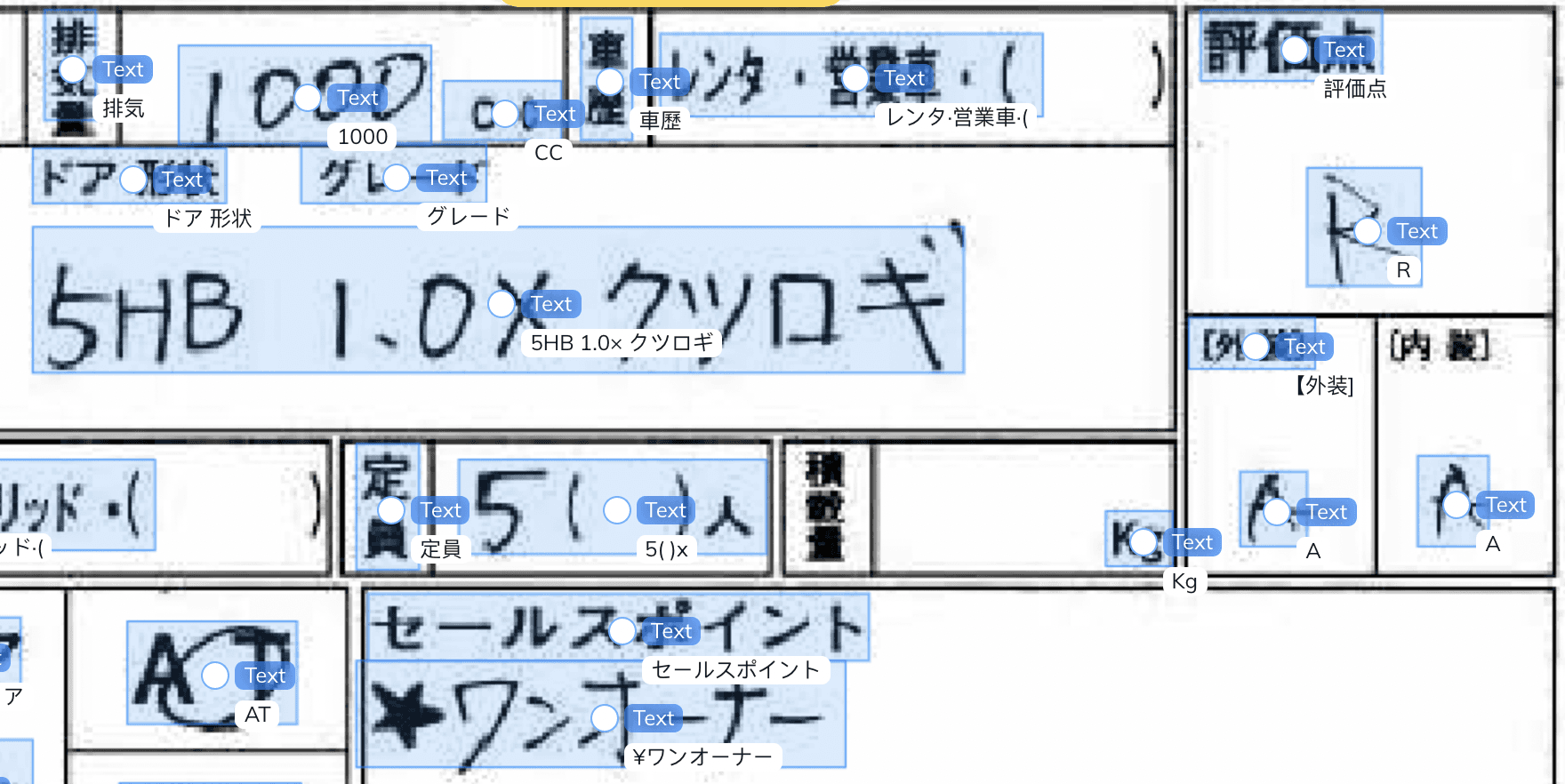

AXA CZ/SK—Leveraging deep learning to improve data ecosystems

AXA CZ/SK recently ran a POC pilot of a deep learning-powered platform for extracting data from incoming unstructured scanned documents.

The AI application auto-classified all incoming documents, extracted hand-printed field values, and submitted the data for further analysis with a 96% accuracy rate.

When scaled successfully, such an OCR system can save hundreds of hours in productive agents’ time and drive measurable operational savings.

4. Faster and More Accurate Underwriting

When it comes to the underwriting process, rule-based evaluation, and risk engines no longer suffice to provide accurate estimates. Especially as insurance scenarios get more complex (e.g. usage-based insurance pricing for shared assets) and fraud levels more elaborate.

Granted the rise in connectivity across all sectors enables digitally mature insurers to devise better ways for doing appraisals.

Computer vision technology, paired with IoT data, can help insurers carefully record the asset state at the time of underwriting and keep making adjustments in near real-time.

For example—

By connecting a GIS data stream to your analytics system, your company can not just eliminate in-person property inspections, but also monitor the property state over time to adjust the policy price.

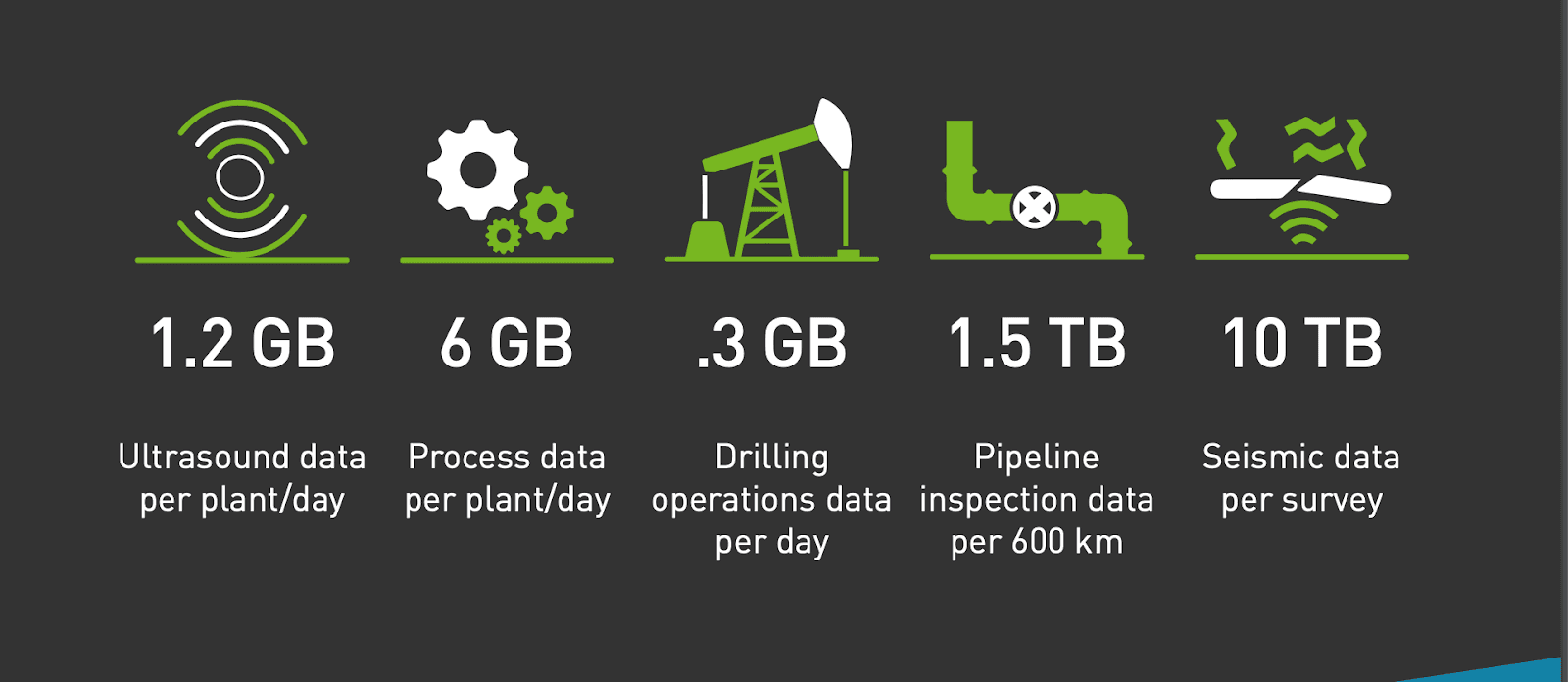

More elaborate scenarios can be used to appraise industrial infrastructure for damage and operational mishaps. For instance, the Oil and Gas industry now produces terabytes of operational data daily:

Insurance companies can connect the above data to predictive analytics systems to anticipate levels of degradation, perform automatic defect inspections, predict potential failure rates and other operational risks, and adjust the premiums accordingly.

Case in point: One global reinsurer built a machine learning algorithm for effectively predicting the likelihood of flooding in the area, using historical and geospatial data and inputs from digitized documents.

Such a setup has allowed them to:

Model a potential market with 83% accuracy

Reduce throughput time in underwriting by 10X

Improved case acceptance by 25%

5. Insurance Fraud Detection and Prevention

American insurance companies lose over $40 billion annually to fraudsters—and that’s without accounting for health insurance fraud.

Fraudulent claims are truly a plague.

The figures are clearly staggering, but understandable given the fact that most still rely on outdated rule-based systems, incapable of detecting elaborate fraud schemes.

AI-powered fraud detection systems address the shortcomings of earlier applications, plus help augment human analysts’ judgments by supplying them with valuable intel.

Inherently, machine learning and deep learning systems are well capable of identifying recurring patterns. Such ability makes such algorithms strong contenders for capturing out-of-the-ordinary behaviors within the systems or amongst individual customers.

For example—

An algorithm pre-trained on employees’ computer- and network-using data can monitor their behavior during the workday. Once it detects a certain degree of deviation from the standard ways of working (e.g. multiple unauthorized access requests), such a security system can flag the user and alert the security team for further investigation.

AI fraud detection applications can be employed to run rapid, automatic background checks during the customer onboarding stage to carefully calculate the risks associated with individuals or businesses.

Anadolu Sigorta—AI in insurance for fraud detection

Turkish insurer, Anadolu Sigorta, recently tested a predictive fraud detection system from Friss.

The company was originally spending over two weeks manually reviewing every submitted claim for signs of fraud. Given that they were processing over 25,000 to 30,000 monthly, the costs of processing were rather high.

After switching to a predictive system, the insurance company gained the capabilities to identify fraud in real-time. They realized a 210% ROI in just one year and attributed over $5.7 million in saved fraud detection and prevention costs to the new AI system.

6. Winning Insurance Customers with Competitive Premiums for Drivers

Connected vehicles now produce, store, and transmit terabytes of valuable data that insurance carriers can use to offer more competitive prices or pivot to new business models as per consumer demands:

Some of the emerging AI use cases for auto insurance include:

Predictive cost analytics for claims: Leverage machine learning techniques and data science to estimate the average claims cost per different customer segments. Adjust premiums respectively and manage your cash flow better.

Driver performance monitoring: By analyzing behavioral data from the connected car systems (in-car and external cameras, telematics, and ADAS systems), you can learn more about individual drivers’ behaviors and delight them with personalized rates and product lines.

Real-time accident support. Insurer carriers can deliver superior service levels to drivers by receiving automatic access to the crash data and providing a rapid semi-automated response. For example, an AI chatbot can prompt the driver on the best actions for recovery, automatically notify the medical team if needed or call a two truck service.

Such real-time connectivity can be especially crucial for saving lives. Per OECD, 44% of car crash fatalities could have been prevented if emergency medical services had had real-time information on the type and severity of their injuries.

SARA Assicurazioni and Automobile Club—AI for car accidents insurance

SARA Assicurazioni and Automobile Club Italia are enticing drivers to install ADAS systems in exchange for a 20% insurance premium discount.

ADAS systems not just reduce the chances of injury-causing collisions, but also help drivers adopt safer driving habits.

A recent study notes that ADAS systems can reduce:

the rate of personal injury liability claim by 4-25%,

the liability claim rate for property damage caused by traffic accidents by 7%-22%

Ant Financial—AI technology for the new generation of insurance carriers

One of China’s so-called “supper apps”—a company offering an ecosystem of connected digital product offerings and services, ranging from social networking to banking services—uses even more data points to create highly detailed customer profiles.

The AI algorithms assign each customer with Auto Insurance Points, similar to credit scoring. Apart from regular factors such as driving experience, age, and car model, the system also takes into account the “lifestyle factors” to build a comprehensive risk profile for the customer..

These include the policy holder’s credit history, spending habits, profession, etc. Using the input, the application assigns a custom score and provides hyper-personalized insurance pricing, services, and overall customer experience.

The Future of AI In Insurance Industry

The insurance industry is under heavy pressure post-pandemic.

Neither artificial intelligence (AI) nor other related technologies are a “silver bullet” solution to all the underlying stressors. However—

The AI insurance use cases described in this post hold strong potential for improving operational efficiency, containing costs, and enabling insurance companies to pivot to digital-first customer experience and technology-enhanced product lines.

Read next:

27+ Most Popular Computer Vision Applications and Use Cases

65+ Best Free Datasets for Machine Learning

What is Data Labeling and How to Do It Efficiently [Tutorial]

The Complete Guide to CVAT—Pros & Cons

Annotating With Bounding Boxes: Quality Best Practices

And if you are interested to learn more about AI applications across other industries, check out:

Tomas is an entrepreneur, designer, and technology blogger from Lithuania. He developed a readership of over 1 million on his personal blog and writes for the Huffington Post and Forbes.