Knowledge work automation

19 min read

—

M&A due diligence is the structured investigation a buyer conducts before committing to an acquisition. The methodology has been well understood for decades: the seller populates a virtual data room, the buyer's team reviews the contents, a due diligence questionnaire is exchanged, and material risks surface before the sale and purchase agreement is signed. In practice, this process has become significantly harder to execute well, not because the methodology is flawed, but because the volume of material now involved routinely exceeds what deal teams can process within typical deal timelines.

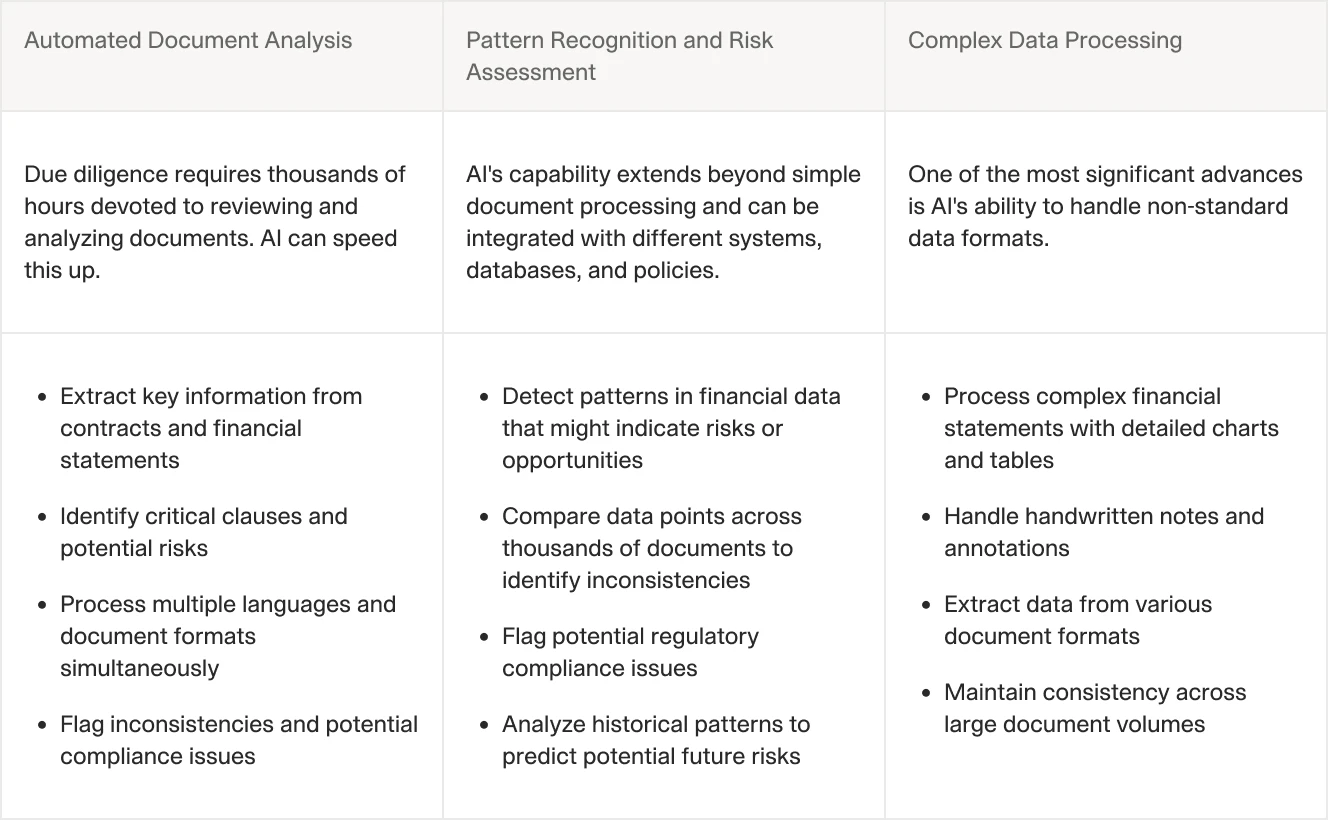

A mid-market acquisition today generates 5,000 to 12,000 data room documents. The due diligence questionnaire, which arrives in whatever format the seller's counsel prefers, typically contains 200 to 400 structured questions spread across 8 to 15 workstream sections. The window to complete the review is usually 30 to 90 days. Between 70% and 90% of M&A transactions fail to deliver the value projected at signing, and inadequate due diligence is among the most consistently cited contributing factors, a finding that Deloitte's annual M&A Trends research has consistently documented across successive years of deal activity. The failures are rarely about missing the obvious. A material fraud is difficult to hide from a determined financial team. What derails deals is subtler: customer concentration that looked manageable in summary data but proved fragile in the underlying contracts; a transfer pricing arrangement carrying forward unresolved tax exposure; a cybersecurity posture that appeared compliant on paper but had never been independently verified. These issues live in the detail, and getting to the detail is, above all, a resourcing problem.

This guide covers M&A due diligence from first principles: what it is and when it happens, the seven workstreams that matter and what each is trying to establish, how the process unfolds from data room access through SPA negotiation, what a comprehensive checklist looks like by workstream, where the DDQ bottleneck sits and why it is structurally underserved, and how AI agents are now being used to process DDQs at a scale and speed that changes what deal teams can realistically cover within a fixed timeline. The final sections address specific red flags that recur across transactions and the most common program-level mistakes.

AI for document processing

Run M&A due diligence without drowning in documents

Get started today

What is M&A due diligence?

M&A due diligence is the process by which a prospective buyer investigates a target company before completing an acquisition. It is conducted after the non-disclosure agreement has been signed and the letter of intent or heads of terms agreed, but before the definitive sale and purchase agreement is executed. In PE-backed transactions, buyers also review the target fund's limited partnership agreement to understand carry structures and assignment restrictions that may affect deal structure. The purpose is to verify that the business is what it appears to be in the information memorandum and initial financial materials, to identify risk factors that are not visible in summary data, and to determine whether the agreed price remains appropriate in light of what the investigation reveals.

Due diligence is almost always buyer-initiated, though sellers increasingly conduct vendor due diligence on themselves before approaching acquirers, both to accelerate the process and to control how information is presented. On the buy side, the scope of diligence is typically set by the deal team with input from legal counsel, financial advisors, and specialist workstream leads. In larger transactions, the buyer will engage external advisors across multiple workstreams simultaneously. In smaller deals, a leaner team covers more ground internally.

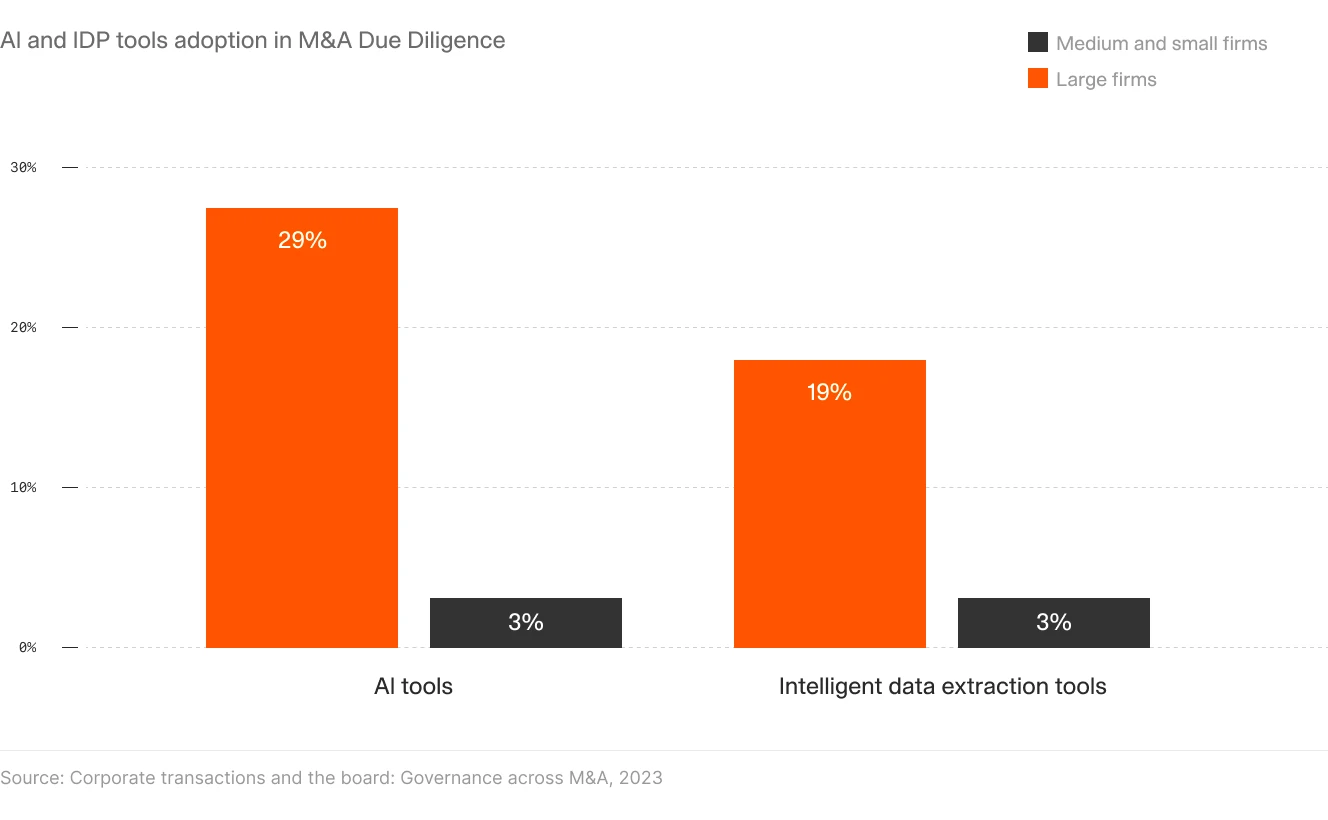

AI adoption in M&A due diligence has accelerated faster than in most adjacent professional services — driven by the compressible timeline of a competitive deal process and the growing volume of cross-border transactions.

The central questions due diligence is designed to answer are: Is the business what it appears to be? What are the actual risk factors, including those not disclosed or not yet visible in the data room? And does the price make sense given what the investigation has now established? The answers to these questions determine whether the deal proceeds at the agreed price, proceeds with conditions or price adjustments, or does not proceed at all.

The 7 types of M&A due diligence

M&A due diligence is structured across multiple parallel workstreams, each investigating a distinct dimension of business risk. In most transactions, all seven are conducted to some degree, with scope and depth calibrated to the size and nature of the deal.

Financial due diligence. Financial diligence examines the quality and sustainability of reported earnings. The core deliverable is a quality of earnings analysis: a restatement of EBITDA that separates recurring earnings from one-time items, normalizations, and accounting treatments that inflate reported profitability. This workstream also reviews the working capital position and its historical range (working capital manipulation in the months before a sale is a common pre-close tactic), debt and contingent liabilities that may not appear on the face of the balance sheet, and revenue recognition policies that may recognize revenue earlier or on different terms than a buyer would apply. The output is typically an adjusted earnings figure that forms the basis for the acquisition multiple.

A modern M&A data room aggregates financial, legal, HR, regulatory, and commercial documents — each category requiring specialist review, and all competing for analyst time in a compressed deal timeline.

Legal due diligence. Legal diligence reviews the contractual and structural foundations of the business. This includes the corporate structure and ownership documentation, the material commercial contracts (customer agreements, supplier agreements, partnership arrangements), intellectual property ownership and assignment, employment and compensation agreements, and the history of litigation, regulatory action, or claims. The central question in legal diligence is not just what obligations the business has accepted but whether those obligations transfer cleanly to the buyer on a change of control. Many commercial agreements contain change-of-control provisions that require counterparty consent or trigger termination rights. Identifying these before signing is critical. V7 Go's AI legal due diligence agent can accelerate the extraction of key contract terms at scale across hundreds of agreements.

Tax due diligence. Tax diligence reviews the target's tax position across all jurisdictions in which it operates. This includes reviewing filed returns for the last three to five years, identifying any open audits or disputes with tax authorities, assessing deferred tax liabilities that may crystallize post-acquisition, reviewing transfer pricing arrangements for compliance and exposure, and understanding whether any tax losses are available to the combined entity and under what conditions they can be utilized. Tax exposure discovered post-close is among the most expensive due diligence misses, because it is typically structural and difficult to unwind.

Commercial due diligence. Commercial diligence evaluates the market position and revenue quality of the business. The primary concern is customer concentration: a business that generates 60% of its revenue from three customers that have short-term, terminable contracts represents a fundamentally different risk profile than its aggregate revenue figure suggests. Commercial diligence also reviews the quality of the pipeline, competitive dynamics (who is the business actually competing against and why does it win or lose?), churn and retention data for subscription or recurring-revenue businesses, and the degree to which the financial projections in the information memorandum are supported by identifiable demand rather than management optimism.

Operational due diligence. Operational diligence examines how the business actually runs on a day-to-day basis. This covers the management team and organizational structure, key supplier and vendor relationships and whether any create single-point-of-failure risk, operational processes and their scalability, and any dependencies on specific individuals, systems, or third parties whose loss or disruption would materially impair the business. Operational diligence often surfaces integration planning considerations: the parts of the target's operations that are most compatible with the acquirer's existing structure, and the parts that require the most post-close work.

Technology and cybersecurity due diligence. Technology diligence has grown substantially in scope and importance as software and data have become material business assets across all sectors. This workstream reviews the technology stack and its architecture, assesses technical debt (the accumulated cost of past shortcuts in software development that will require remediation), evaluates data practices and compliance with applicable data protection regulation, reviews cybersecurity policies and their implementation (not just whether policies exist but whether they are actually followed), and examines whether any prior incidents have occurred. For technology companies, IP ownership verification is a major component: verifying that all code and data assets are owned by the legal entity being acquired, that open-source licensing obligations are understood, and that all contributors have signed appropriate IP assignment agreements.

HR and people due diligence. People diligence evaluates the human capital dimension of the acquisition. This includes reviewing the retention agreements in place for key personnel, compensation structures and how they compare to market, non-compete and non-solicitation arrangements, equity and incentive schemes and how they are affected by the acquisition event, and cultural compatibility between the two organizations. In many acquisitions, particularly of professional services, technology, or knowledge-intensive businesses, the people are the primary asset. Key-person risk (where one or two individuals represent a disproportionate share of the business's capability or relationships) is among the most material factors in post-close value retention, and it is frequently underweighted in financial and legal-focused diligence programs.

How the M&A due diligence process works

The M&A due diligence process follows a broadly consistent structure across deal sizes and types, though the resources deployed, timeline, and level of external advisor involvement vary significantly.

Phase 1: NDA and initial information request. Once a target has been identified and preliminary valuation discussions have advanced to the point of mutual intent, the buyer signs a non-disclosure agreement and receives an initial information package (typically the information memorandum and a set of preliminary financial data). This phase may involve a preliminary or confirmatory due diligence scope, in which the buyer conducts enough high-level review to decide whether to proceed to full diligence and, if so, at what price range.

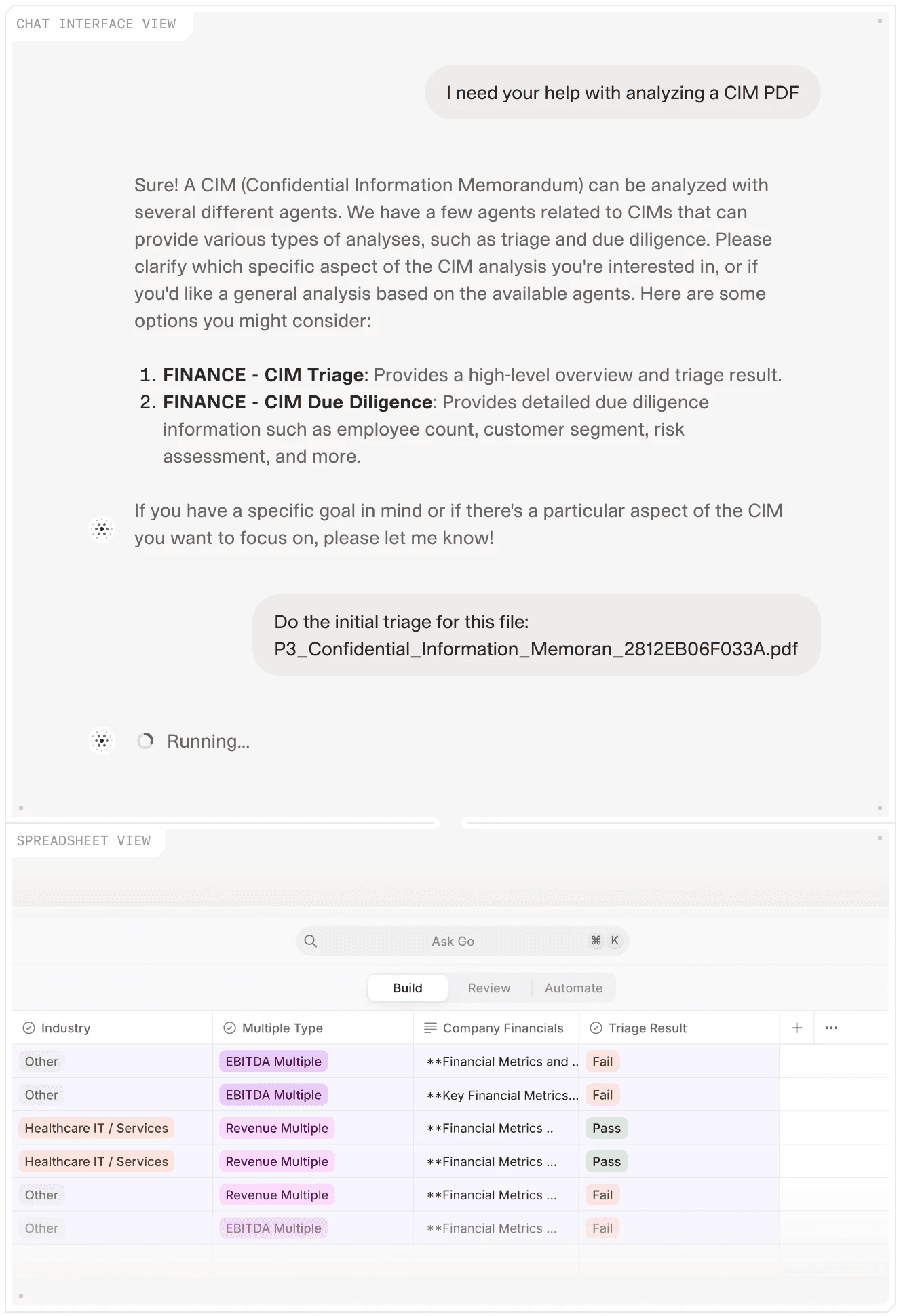

Phase 2: Data room access and structured review. After signing the letter of intent or heads of terms, the seller grants access to a virtual data room containing the detailed documentation for each workstream. The buyer's deal team, supported by workstream advisors, begins systematic document review. V7 Go's guide to AI in virtual data rooms covers how the data room review phase is changing as AI tools make it possible to extract and analyze document content at a speed that was not previously feasible.

A structured AI triage output from a company's information memorandum gives the deal team an immediate overview of financial performance, business model risk, and deal-critical questions before deeper diligence begins.

Phase 3: DDQ submission and response. The buyer submits a due diligence questionnaire to the seller, requesting structured responses to specific questions by workstream. The DDQ response process is where the most significant resourcing challenges arise and where delays most commonly accumulate. This phase is covered in more detail in the section below on the DDQ bottleneck.

Phase 4: Management presentations and expert calls. The buyer's team meets with the seller's management team to review the business, challenge the financial projections, and probe any questions or gaps identified in the document review and DDQ stage. Subject matter experts may be engaged for specific workstreams (for example, a cybersecurity specialist to evaluate the technology posture, or a tax lawyer to work through transfer pricing arrangements).

Phase 5: Findings synthesis and SPA negotiation. The deal team produces a due diligence findings report that summarizes the risk profile across all workstreams, flags material issues, and identifies items that require resolution as conditions of closing or reflection in price. The findings inform the negotiation of the sale and purchase agreement, including representations and warranties, conditions precedent, and any price adjustments or escrow arrangements. Purchase agreement analysis tools can assist with reviewing the draft SPA against the findings from the diligence process.

The DDQ bottleneck: why the questionnaire phase stalls deals

The due diligence questionnaire is the most information-dense phase of the M&A process and the one most likely to create timeline pressure. A DDQ for a mid-market transaction typically contains 200 to 400 structured questions organized into sections corresponding to the main workstreams: corporate and legal, financial, tax, commercial, technology, HR, and (increasingly) ESG and cybersecurity. For larger transactions or regulated industries, the questionnaire can exceed 600 questions.

The first problem is format fragmentation. Unlike a structured data room where the seller organizes documents into folders, the DDQ arrives in whatever format the buyer's counsel uses as their template. Some DDQs are formatted as Excel workbooks with one tab per workstream and nested sub-questions. Others arrive as Word documents or PDFs. Sellers sometimes submit DDQ responses in a completely different format from the original, adding commentary in separate documents or providing answers inline in a scanned printout. The buyer's team must first identify, parse, and standardize all of this material before any substantive analysis can begin. In practice, this step alone can consume one to two days of analyst time per transaction.

The second problem is scale. Answering 300 questions from a data room with 8,000 documents requires matching each question to the relevant evidence across a large, unstructured document set. The questions span multiple workstreams, each requiring different domain knowledge. A financial analyst can answer the financial questions efficiently but will need to involve legal, tax, and technical resources for the other sections. Coordinating that review, ensuring each question is answered with reference to actual data room evidence (not inference or management representation), and producing a consistent output takes time that the deal clock does not always provide.

The third problem is the gap. When a DDQ response is incomplete, the buyer must identify exactly which questions were not answered or not answered adequately, formulate specific follow-up requests, wait for the seller to respond, and integrate the new material with the original response. In a competitive process with a fixed exclusivity window, incomplete DDQ responses are a common source of deal delay and occasionally deal collapse.

The due diligence software market has evolved to address parts of this problem, particularly around data room organization and document search. The extraction and answering layer, however, has historically remained manual.

M&A due diligence checklist: key questions by workstream

The following covers the essential questions across each of the seven M&A due diligence workstreams. It is not exhaustive (a full institutional DDQ typically runs to 40 to 80 pages) but covers the areas where material risk most commonly appears.

Financial

Are audited financial statements available for the last three to five years? What is the quality of earnings analysis showing as the recurring EBITDA base? How has working capital moved over the last 12 to 24 months, and is there evidence of pre-sale manipulation? What are the off-balance-sheet liabilities, earn-out obligations, or contingent liabilities? What is the revenue recognition policy, and is it consistent with the underlying contract terms? What does the debt schedule look like, including any covenant obligations and maturity dates? Is the cap table clean, with no outstanding equity commitments that will affect post-close ownership?

Legal

Is the corporate structure documented and are all entities in the group clearly identified? Who are the ultimate beneficial owners? Do the top 20 customer contracts contain change-of-control clauses that require consent or permit termination? Are intellectual property assets (patents, trademarks, domain names, software code) clearly assigned to the target legal entity? Are there any outstanding or threatened litigation matters, regulatory investigations, or formal claims? Are all employment agreements in place for key personnel, and what are the termination provisions?

Tax

Are tax returns filed and current in all relevant jurisdictions? Are there any open audit disputes or outstanding correspondence with tax authorities? What deferred tax liabilities exist, and when are they likely to crystallize? Are transfer pricing arrangements between related entities documented and at arm's length? Are any tax losses available to the combined entity, and do they survive a change of control under the relevant tax legislation? What is the target's historic effective tax rate, and are there any structural features that will unwind post-acquisition?

Commercial

What percentage of revenue is attributable to the top 5 and top 10 customers? What are the contract durations and notice periods for those customers? What is the annual churn or retention rate, and how has it moved over the last three years? How does the pipeline convert, and is the pipeline figure in the information memorandum supported by documented, qualified opportunities? What are the primary competitive threats, and what evidence supports the target's claimed competitive advantages?

Technology and cybersecurity

What is the technology stack, and what proportion of it is proprietary versus licensed? What is the technical debt assessment, and what will it cost to resolve over the next 24 months? Does the target hold relevant security certifications (SOC 2 Type II, ISO 27001) and are they current? Has independent penetration testing been conducted, and by whom? Have there been any data breaches or cybersecurity incidents in the last three years, and how were they handled? Is there a formal data protection compliance program covering GDPR, CCPA, or other applicable frameworks?

HR and people

Who are the key personnel, and what retention arrangements exist? Are compensation packages at, above, or below market, and what is the retention risk if the acquirer adjusts them? Are non-compete and non-solicitation agreements in place for the senior team? How has headcount changed over the last 24 months, and are there any pending departures or restructuring plans? What is the cultural profile of the organization, and what integration work will be required to align it with the acquirer's structure?

ESG and cybersecurity governance

Does the target have a formal ESG policy, and if so, what commitments does it contain? Are there any outstanding environmental liabilities, remediation obligations, or regulatory compliance gaps? Does the target have a documented cybersecurity governance framework, including an incident response plan that has been tested? What is the target's data handling and retention policy, and is it consistent with its privacy commitments to customers and employees?

How V7 Go processes DDQs at scale

V7 Go's DDQ Diligence Agent was designed specifically for the extraction and answering problem described above. It operates in two distinct stages that together convert an unstructured DDQ in any format into a structured set of answered questions, each with a traceable evidence trail and an explicit flag for whether it was answerable from the available data room materials.

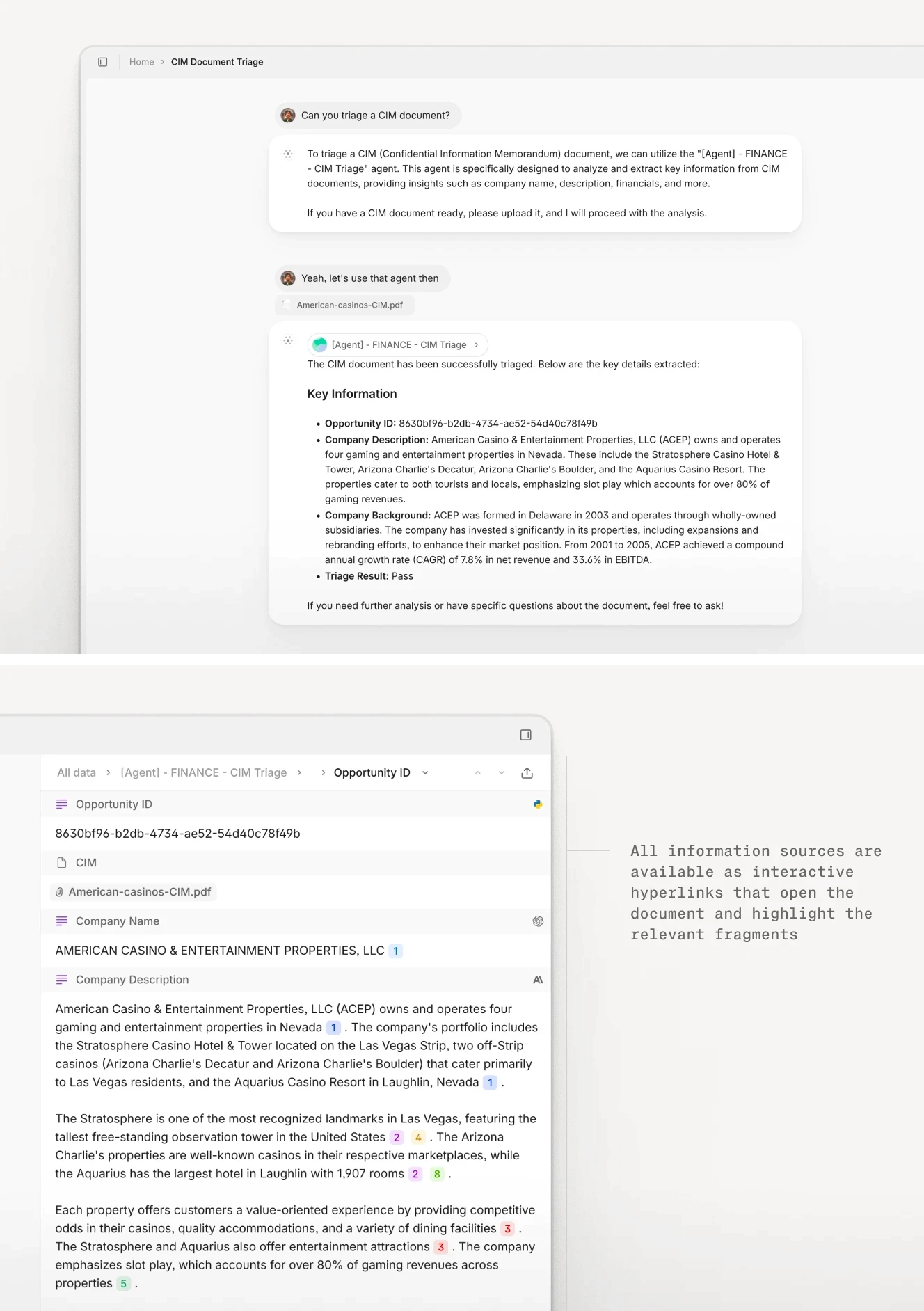

Stage 1: DDQ ingestion and question extraction. The agent accepts a DDQ file in any format: Excel workbooks (including multi-tab structures with nested sub-questions), PDFs, Word documents, plain text, or scanned images. It detects the file type automatically and routes it through the appropriate processing path. Excel files are converted to structured XML that preserves the workbook hierarchy. PDFs and documents are OCR-processed using Gemini 2.5 Pro, which handles both digital-native and scanned documents. Text-based files are read directly. Once the file is processed, GPT-5 extracts every question with its corresponding section label, producing a standardized JSON output: a list of objects, each containing a Section Name and a Question. For a 401-question DDQ, this produces 401 individually addressable records, organized by section, available in V7 Go's project view for team review before answering begins.

The following shows V7 Go applied to an M&A due diligence document package — from DDQ processing to financial statement extraction within a single unified workflow:

V7 Go processing an M&A due diligence workflow: ingesting DDQ responses, cross-referencing financial statements, and flagging gaps and inconsistencies across 40+ document categories with source citations.

Stage 2: Answering against the data room. Each extracted question is processed by a grounded AI agent that has access to the indexed data room via a retrieval tool. For each question, the agent parses the question to identify the required data fields, forms three to seven targeted search queries using relevant document terminology and time qualifiers, and searches the data room. If the initial results are insufficient, it refines its queries and searches again. Source selection follows a defined hierarchy: audited financial statements take precedence over management accounts; signed contracts over drafts; the most recent document over earlier versions. Where sources conflict, the agent selects the most authoritative, notes the discrepancy, and reconciles where possible.

The output for each question is a structured JSON record containing an executive answer in bullet-point format, a reasoning section that explains the logical chain from retrieved evidence to conclusion, a sources table with verbatim document snippets (each under 25 words) linked to the specific document and section, and an "ability to answer" flag: Yes or No. GPT-5 Mini serves as the primary answering model; Gemini 2.5 Flash processes each question in parallel as a secondary pass.

The "No" output is as valuable as the "Yes" output. Questions flagged as unanswerable (where the data room does not contain sufficient evidence) become an Information Request List: a structured list, organized by section and question, of exactly what documentation is missing. Rather than a general note that "additional information is required," the output specifies which question could not be answered and what evidence would be needed to answer it. This turns the DDQ gap analysis from an informal process into a structured document that can be submitted to the seller as a prioritized, section-by-section information request.

In one deployment against a mid-market B2B software company, the agent processed 401 DDQ questions across 12 sections. Of those, 293 were answered (73%) with traceable data room evidence. The remaining 108 questions could not be answered from available materials and were flagged as information requests, with each request specifying the document type and content needed. The flagged items mapped directly to documentation gaps that became conditions in the SPA. The extraction and initial classification phase, which would typically take a small deal team two to three days, was completed systematically and consistently in a fraction of that time.

The project view in V7 Go allows the deal team to filter the results by section, by ability to answer, and by individual question. Via API or MCP-connected systems, the structured output can populate a deal management system, CRM, or reporting database, making the findings accessible across the broader transaction workflow rather than siloed in a standalone document. For teams running multiple parallel processes, V7 Go's comprehensive guide to AI in due diligence covers how the capability fits within a broader deal pipeline. The best AI data rooms for due diligence guide covers the data room infrastructure layer that the DDQ answering agent works within.

M&A due diligence red flags: what matters and what to act on

Red flags in M&A due diligence are not simply items that require explanation. They are patterns that suggest a fundamental misrepresentation of the business, a risk that the buyer cannot adequately price, or a structural issue that will impair the investment thesis post-close. The following six recur with the highest frequency across deal types and sizes.

Revenue concentrated in customers with short-term or change-of-control-sensitive contracts. A business generating 40% of its revenue from two customers who each have annual rolling contracts with 30-day termination provisions represents a risk that aggregate revenue figures do not communicate. If either contract contains a change-of-control clause requiring consent (or worse, permitting the customer to exit on a change of control without penalty), the revenue base is structurally impaired at the moment of acquisition. This risk is found frequently in both B2B software and professional services acquisitions and is one of the first things experienced acquirers look for in the customer contract review.

Working capital significantly above the historical average in the reference period. When a seller knows a transaction is approaching, there is a natural incentive to maximize the working capital position (which typically forms part of the acquisition price mechanism as a normalized working capital target). Tactics include accelerating customer invoicing, delaying supplier payments, reducing inventory reorder frequency, and adjusting revenue recognition timing. A working capital position materially above the trailing 12 to 24 month average, particularly in the two to three months immediately preceding the measurement date, warrants close investigation. The IMAA has documented pre-sale working capital management as a recurring feature of deal disputes.

A gap between reported revenue and cash collections. Revenue recognition policies can be structured to recognize revenue significantly ahead of the cash it represents. In a subscription business, this might mean recognizing annual contract value at the start of the term rather than rateably. In a project business, it might mean recognizing milestones before the customer has formally accepted the work. If reported revenue growth is not accompanied by proportional growth in cash from operations, the quality of earnings analysis should interrogate the gap explicitly. This is among the most common sources of post-close valuation disputes.

Intellectual property that is not clearly owned by the target entity. IP ownership is a legal due diligence finding that recurs most frequently in technology acquisitions. Common issues include: software developed by contractors who were never required to sign IP assignment agreements (meaning the IP is technically owned by the contractor or jointly owned); open-source components incorporated into proprietary software under licenses that impose distribution or disclosure obligations on the combined entity; and trademarks or domain names registered in the name of a founder personally rather than the operating company. Any of these can become significant issues post-close, particularly if the acquirer plans to sublicense, distribute, or develop the technology further.

A data room organized to avoid specific questions. The structure of a data room is informative in itself. A data room with comprehensive financial and legal documentation but an almost empty technology folder, or one that contains policy documents but no evidence of their implementation, suggests that the seller is managing disclosure rather than facilitating review. The CFA Institute's research on M&A due diligence and deal outcomes identifies information asymmetry management by sellers as a consistent predictor of post-close disappointment. The gaps in a data room are as informative as the documents present, and experienced deal teams map what is absent as carefully as they review what is there.

Key management retention not secured. In acquisitions where the investment thesis depends on the continuation of the management team, the absence of retention agreements at or before signing is a material risk that is frequently discovered late. If the CEO, CTO, or a small number of senior revenue-generating individuals have not signed retention packages before the transaction closes, the buyer is exposed to the possibility that the core value of the acquisition walks out the door in the months following close. In competitive auction processes, sellers sometimes resist providing management retention arrangements until late in the process, which creates a negotiating window that experienced buyers should use carefully.

Common mistakes in M&A due diligence programs

Beyond specific red flags, a number of program-level mistakes recur across transactions and are worth addressing explicitly.

Starting full due diligence without a preliminary screen. In competitive auction processes, buyers often feel pressure to commit to a full diligence scope immediately after submitting an indicative bid. In practice, a targeted preliminary review of the two or three highest-risk areas (customer contract structure, IP ownership, and open litigation are the most common) before committing to full exclusivity can reveal deal-breaking issues in days rather than weeks. Spending three weeks on a full diligence program to discover at the end that a change-of-control clause in the top customer contract makes the deal unworkable is an expensive way to do due diligence.

Treating the DDQ response as complete without verification. A DDQ response from the seller is a self-assessment, not an audit. The seller has a natural interest in presenting its business in the best light, and the answers to specific questions will reflect that. Every answer in a DDQ that matters to the investment thesis should be verifiable against primary documentation in the data room. An answer that says "all intellectual property is owned by the company" requires verification against IP assignment agreements, contractor agreements, and any open-source licenses used. Accepting the DDQ response as equivalent to independent verification is one of the most common diligence failures.

Siloing workstreams so that cross-functional risk is missed. A customer concentration identified in the commercial workstream may have implications in the legal workstream (are those customer contracts terminable?), the tax workstream (are revenue recognition arrangements consistent with the contract terms?), and the HR workstream (which individuals own the key customer relationships?). Workstreams that operate independently, with findings shared only at the final report stage, frequently miss the most significant risks, which are almost always intersectional.

Under-resourcing the extraction phase relative to the analysis phase. Deal teams often resource the analytical phase of due diligence (financial modeling, legal review, commercial analysis) extensively but underestimate the time required to extract the underlying data from the data room and DDQ response into a usable format. The extraction phase is where AI agents create the most leverage: moving the structured extraction from days to hours frees analyst capacity for the judgment work that technology cannot replace.

For a complete overview of AI-native tools that support the full due diligence workflow, including document extraction, contract review, data room analysis, and DDQ answering, V7 Go's AI Financial Due Diligence Agent covers the end-to-end capability in detail.

What is the purpose of due diligence in M&A?

M&A due diligence is a structured investigation conducted by a buyer before completing an acquisition. Its purpose is to verify that the target company is what it appears to be in the initial materials, to identify risk factors not visible in summary data, and to determine whether the agreed price remains appropriate given what the investigation reveals. It is conducted after the letter of intent is signed but before the definitive sale and purchase agreement is executed.

+

How long does M&A due diligence take?

M&A due diligence typically takes 30 to 90 days, depending on the size and complexity of the transaction, the completeness of the data room, and the responsiveness of the seller to DDQ requests and management presentation scheduling. Smaller deals with clean data rooms and responsive management can close the diligence phase in four to six weeks. Larger, cross-border, or more complex transactions often require 60 to 90 days, and regulatory or antitrust review can extend this further.

+

What is a DDQ in M&A?

A DDQ, or due diligence questionnaire, is a structured set of questions submitted by the buyer to the seller, typically organized by workstream (financial, legal, tax, commercial, technology, HR). A mid-market DDQ usually contains 200 to 400 questions. It may arrive as an Excel workbook, a Word document, a PDF, or in other formats depending on which template the buyer's counsel uses. The DDQ response phase is one of the most time-intensive parts of the due diligence process because each answer requires verification against data room documentation rather than simply accepting the seller's self-assessment.

+

What are the main types of due diligence in M&A?

The seven main types of M&A due diligence are financial (quality of earnings, working capital, debt), legal (corporate structure, contracts, intellectual property, litigation), tax (tax returns, deferred liabilities, transfer pricing), commercial (customer concentration, pipeline, competitive position), operational (management team, supply chain, business processes), technology and cybersecurity (tech stack, technical debt, security posture), and HR and people (retention risk, compensation, key-person dependency, culture).

+

What are the most common M&A due diligence red flags?

AI is primarily changing M&A due diligence by addressing the extraction bottleneck: the process of converting unstructured data room documents and DDQ responses into structured, searchable, analyzable data. AI agents can ingest DDQ files in any format, extract all questions with their section labels, and then answer each question against an indexed data room by searching for relevant evidence, applying source hierarchy rules, and producing structured outputs with executive answers, reasoning, source citations, and a yes/no flag for whether the question could be answered from available materials. Questions that cannot be answered become an Information Request List specifying exactly what documentation is missing, turning an informal gap analysis into a structured follow-up document.

+

How is AI changing M&A due diligence?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.