Document processing

11 min read

—

This guide is for investment professionals who live inside that process; PE and VC associates, investment banking analysts, M&A advisors, and corporate development teams who review, negotiate, or summarize term sheets as part of daily deal work.

We'll cover what term sheets actually contain, how they differ by deal type, where manual review creates real risk, and how AI-assisted workflows are beginning to change the economics of the whole thing.

AI for document processing

Stop reviewing term sheets line by line

Get started today

What Is a Term Sheet?

Also known as a letter of intent or memorandum of understanding, a term sheet is a non-binding document that captures the proposed financial and legal terms of a deal. It sits between informal conversations and a definitive agreement, giving both sides a shared reference point before lawyers start generating expensive paper.

The "non-binding" label is important but easily misread. Most of the document is non-binding in the sense that neither party is legally committed to complete the transaction on those terms. But certain provisions typically are binding from the moment of signing: exclusivity clauses, no-shop periods, and confidentiality obligations.

A term sheet is therefore simultaneously a preliminary document and a legally operative one, which is one reason careful review matters even before formal diligence begins.

Where Do Term Sheets Fit in the Deal Cycle?

Term sheet review sits at a precise point in the deal lifecycle: after enough diligence to form a view on terms, but before the detailed legal work of definitive documentation begins. That placement creates pressure in both directions.

On one side, you're racing to respond before a competitive process closes or a preferred seller moves on. On the other, you're trying to ensure you haven't agreed to provisions that will create problems in diligence, in the definitive agreement, or post-close. The firms that navigate this well have institutionalized the process, including a standard review framework, a clear view of what's market versus what's a deviation, and defined escalation paths when something unusual surfaces.

The output of term sheet review feeds several downstream processes:

Investment Committee materials

Negotiating strategy

Legal handoff

Deal tracking and portfolio operations

What Do Term Sheets Contain?

Here's what you'll typically find inside a term sheet:

Valuation and deal structure.

In a VC context, this means pre-money valuation, post-money valuation, and the resulting ownership percentage. If a company is valued at $19M pre-money and an $8M investment is being contemplated, the post-money is $27M (the "8 on 19" shorthand you'll hear in deal discussions.) In PE, this translates to enterprise value, purchase price, and the equity contribution alongside debt structure. These figures anchor everything else in the document.

Investment instrument

The form of the capital: common equity, preferred stock, convertible note, SAFE, or debt. Each instrument carries materially different rights and risk profiles. Convertible notes and SAFEs defer valuation but include mechanics — valuation caps and discount rates in particular — that determine the eventual conversion price and can significantly affect dilution at a later round.

Liquidation preferences

This is where a lot of the economic tension lives, and it's the clause that founders and deal teams alike tend to underweight relative to the headline valuation number. A liquidation preference defines who gets paid first, and how much, in an exit or liquidation event.

The current market standard, per Cooley's Q2 2025 data, is a 1× non-participating preference. That mean investors get their money back first, but don't participate further in upside once they've been repaid. Participating preferred, where investors take their preference and then participate in remaining proceeds, is now largely considered off-market in early-stage deals. But it still surfaces in bridge rounds and later-stage transactions, and a deal team that doesn't flag it is leaving real money on the table.

Anti-dilution protections

If a future round closes at a lower valuation (a down round), anti-dilution provisions protect earlier investors by adjusting their conversion ratio. Broad-based weighted average anti-dilution is standard and generally fair to all parties.

Full ratchet, which adjusts the earlier investor's conversion price all the way down to the new lower price, regardless of the size of the down round, is highly investor-favorable and can be severely punitive to founders and common shareholders. It's rare in early-stage VC today, but still surfaces in certain situations and should always be flagged.

Pro-rata rights

The right to invest in future rounds to maintain one's percentage ownership. Standard pro-rata lets you keep your stake steady. Super pro-rata lets you grow it. Median seed ownership by lead investors hovers around 12.6%, and pro-rata rights are the primary mechanism through which investors protect that stake as companies scale through subsequent rounds.

Board composition and governance

How many seats exist, who appoints them, and what decisions require board or investor approval. This is less visible than valuation but often more consequential over the life of a company.

Protective provisions, like investor veto rights over major decisions like new share issuances, asset sales, and changes to the certificate of incorporation, are standard.

Exclusivity and no-shop provisions

Once signed, the seller or founder typically agrees not to shop the deal to other buyers or investors for a defined window. This is standard practice, but the length matters. Thirty to forty-five days is typical for most early-stage transactions.

Founder vesting and lock-ups

In VC deals, reverse vesting of founder shares is common. That means founders who leave early forfeit unvested equity. In PE, management incentive plans and rollover equity structures perform a similar alignment function, though the mechanics differ substantially.

Representations and warranties, and conditions to close

The scope of what the seller is legally affirming about the business, and what must happen before the deal can actually close. These provisions become the foundation for diligence and, later, for any indemnification claims post-closing.

Types of Term Sheets

VC term sheets are typically short (often fewer than ten pages) and investor-prepared. The key battlegrounds are valuation and option pool sizing, liquidation preference structure, and the scope of protective provisions.

PE term sheets and LOIs are longer, more complex, and often two-sided. The economics live in enterprise value, EBITDA multiples, purchase price adjustments (working capital, net debt, earnouts), and the financing structure. Governance terms involve management retention, rollover equity, and board structure post-close. The legal architecture is heavier: representations and warranties are extensive, escrow and indemnification arrangements are common.

M&A term sheets in strategic transactions blend elements of both. Synergy assumptions affect valuation; deal protection mechanisms (matching rights, termination fees, go-shop provisions) shape the competitive dynamics; and earnout structures introduce contingent consideration that can be highly complex to model and to negotiate.

Why Manual Term Sheet Review Creates Risk and Delay

The core structural problem with manual term sheet review is talent concentration. The ability to review a term sheet accurately (flagging non-standard provisions, recognizing the market context for each clause, identifying which provisions are worth pushing back on) is concentrated in a small number of people at any firm. Those people are expensive, scarce, and already stretched across multiple live deals.

When a term sheet arrives at an inconvenient time, the review process compresses in ways that create real risk. But time pressure isn't the only problem.

Version control. Term sheets circulate as redlined Word documents across email threads, often with multiple parties marking up different versions simultaneously. In a competitive process with multiple rounds of negotiation, establishing which document represents the current agreed position can be genuinely difficult.

Consistency. Without a standardized review framework, different team members flag different things. Institutional knowledge about what the firm will and won't accept lives in people's heads rather than in a system. A new associate reviewing their first PE LOI has no reliable way to know which deviations from standard terms the firm has accepted historically and which it's consistently pushed back on.

Cross-document reconciliation. A term sheet doesn't exist in isolation. Agreed terms need to be checked against the CIM, the financial model, the data room materials, and any prior correspondence. Does the revenue figure referenced in the deal economics align with what's in the model? Does the cap table representation in the term sheet match the data room documentation? This cross-referencing is tedious to do manually and easy to skip under time pressure.

Downstream surprises. The provisions that don't get flagged in term sheet review tend to resurface as problems in the definitive agreement negotiations, in diligence, or post-close. An option pool expansion that wasn't modeled correctly affects cap table calculations throughout the company's life.

The cost of these failures is concrete. Slow review costs firms competitive deals. Inconsistent review creates legal exposure. Missed provisions create surprises, and in deals operating at the scale typical of the current PE market, those surprises are expensive.

How AI Is Changing Term Sheet Review

Modern document AI and large language models can now read, extract, and analyze term sheets at speeds that weren't possible a few years ago.

Respondents who say they are using gen AI in their M&A activities report an average cost reduction of roughly 20 percent. Forty percent of respondents report that gen AI enabled 30 to 50 percent faster deal cycles. Of all respondents, 42 percent say they believe gen AI has the potential to transform or to bring highly differentiating capabilities to the deal process.

— McKinsey, Gen AI in M&A: From theory to practice to high performance

General tools can be a huge help in manual workflows. But the shift that matters most in 2026 is perhaps the move from single-document AI tools to agentic workflows that can execute an entire review or generation process end-to-end, without a human orchestrating every step.

The distinction is important. A single-pass AI model reads a document and produces a summary. An agentic system receives a term sheet, triggers a multi-step workflow, extracts structured data at the provision level, cross-references that data against the CIM and financial model, flags deviations against the firm's playbook, generates a structured IC memo section, routes flagged items to the appropriate reviewer, and logs the entire process with citations back to source documents.

All this, before anyone has opened their laptop!

Here's what that looks like in practice:

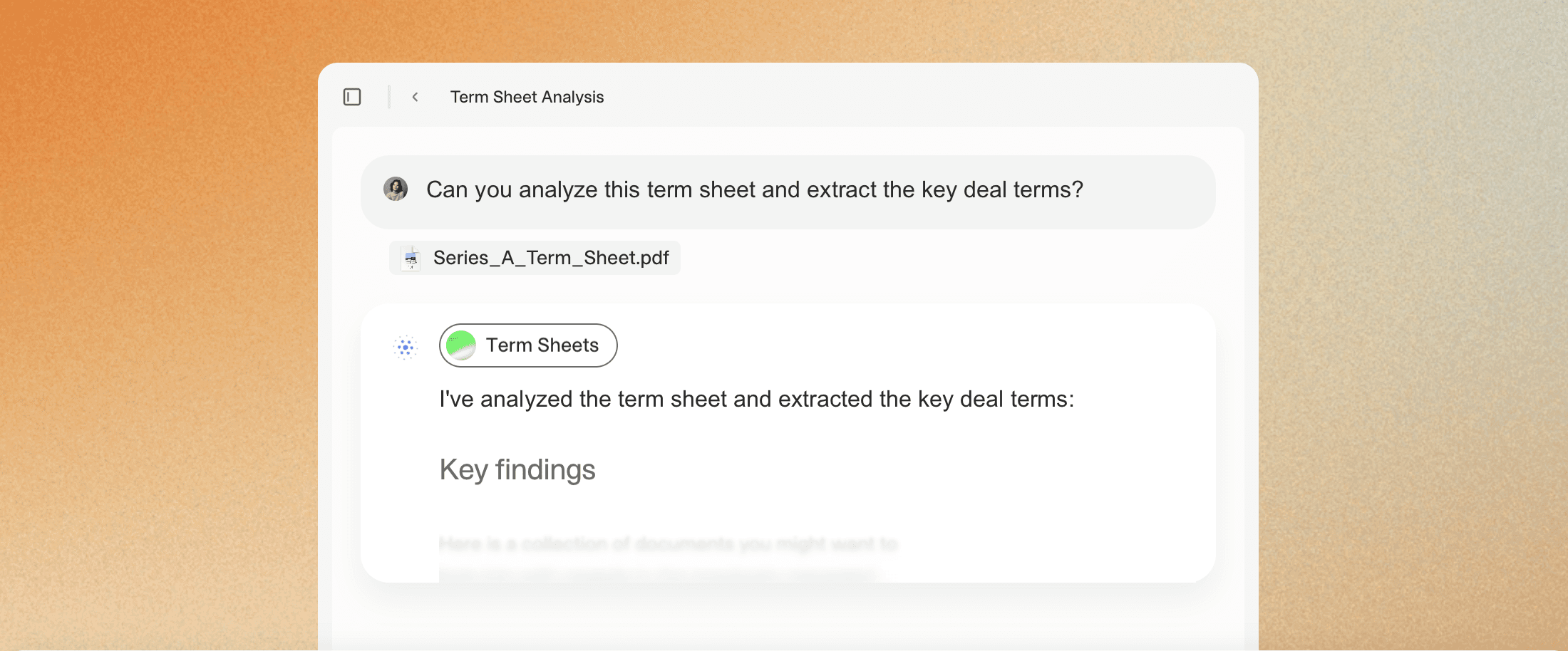

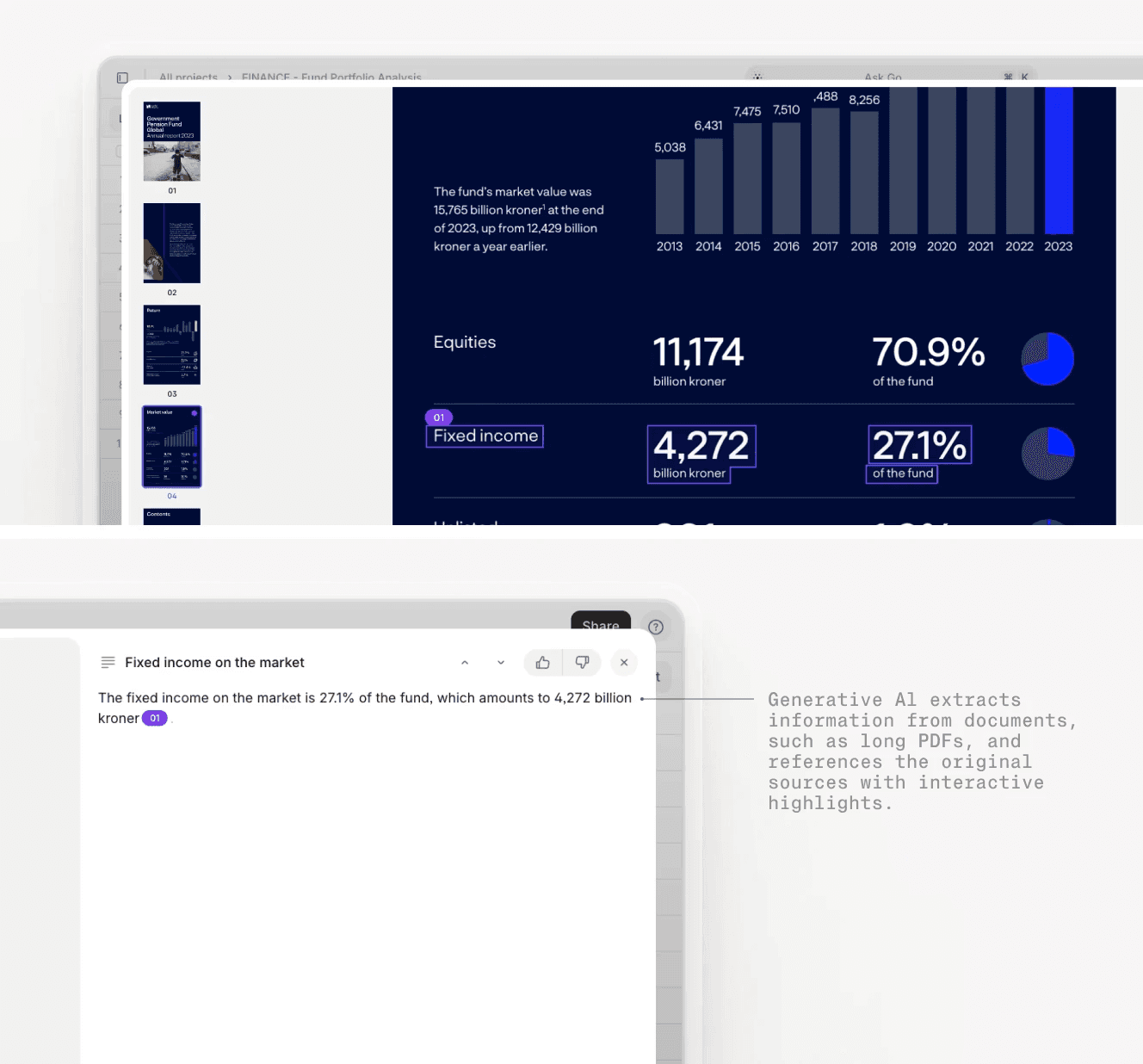

Clause-level extraction with visual grounding. AI doesn't just summarize, say, the liquidation preference section, it extracts the specific mechanics, cites the exact page and paragraph where it found them, and outputs structured data that can be imported directly into a deal tracker.

Deviation flagging against the firm's playbook. The agent compares extracted terms against the firm's own standards and surfaces only the deviations that require human judgment.

Redline and version comparison. Tracking changes across a circulating document, including changes that were introduced as tracked changes and then accepted, and therefore no longer appear as redlines in the final version but are nonetheless material.

Cross-document reconciliation. Comparing term sheet provisions against the CIM, data room materials, and financial model. Does the revenue representation align with the model? Does the cap table in the term sheet match the data room?

Automated workflow triggers. No manual queue management, no documents sitting in a shared inbox waiting for someone to pick them up.

V7 Go for Term Sheet Review

As deal volume increases, traditional term sheet review quickly becomes a bottleneck. Analysts and legal teams are forced to spend hours extracting the same core information such as valuation, dilution mechanics, and control rights across documents that differ widely in structure and wording. This is where V7 Go changes the workflow.

V7 Go is a knowledge work automation platform built for document-intensive industries — finance, insurance, and real estate. It orchestrates AI agents that can read, analyze, extract, and generate structured outputs from complex documents with up to 99% accuracy. Every output is grounded through AI Citations, meaning each finding is visually linked back to its exact source passage for full auditability. It handles PDFs, spreadsheets, tables, graphs, and handwritten notes, and can handle dozens or hundreds of documents simultaneously.

Instead of treating term sheets as static PDFs that must be read line by line, V7 Go transforms them into structured, queryable data. Its AI agents read the document in context, identify key clauses, and extract critical terms into a consistent format, while linking each output back to the original source for full transparency.

With this foundation in place, review shifts from document parsing to decision making. Teams can instantly compare multiple term sheets side by side, spot deviations from standard terms, and surface potential risks without combing through pages of legal text. V7 Go handles the first pass of analysis by highlighting what matters and standardizing how it is presented, allowing investors and legal teams to focus on interpreting the implications and negotiating better outcomes.

See the V7 Term Sheet Review agent in action.

V7 can also automate processes accross the whole investment cycle, including

Accelerate Your Term Sheet Review with Secure, Trusted AI

Term sheet review is one of the highest-leverage activities in the deal process. A provision that doesn't get caught at the term sheet stage tends to become more expensive to address at every subsequent stage, in the definitive agreement, in diligence, post-close.

Getting this right, consistently, at deal velocity, requires both institutional frameworks and, increasingly, tools that can handle the mechanical layer of extraction, structuring, and deviation flagging at speed. The firms building those capabilities now are compressing their review timelines, reducing their legal exposure, and generating IC-ready materials faster than they could when everything ran through a single senior associate.

The term sheet is where deals are made or broken. The review process should match those stakes.

To learn more about how you could automate and accelerate your term sheet review, book a no-obligation chat with our expert team.

What's the difference between a term sheet, an LOI, and a definitive agreement?

These three documents represent sequential stages of a deal. A term sheet is typically the earliest and shortest — a high-level outline of proposed economics and governance terms. A letter of intent (LOI) performs a similar function but is more common in M&A transactions and often goes into greater legal detail. Both are largely non-binding. A definitive agreement — the purchase agreement, merger agreement, or investment agreement — is the legally binding document that governs the actual transaction. The terms negotiated in the term sheet or LOI become the basis for the definitive agreement, which is why gaps or ambiguities at the term sheet stage tend to resurface as expensive problems later.

+

How long does term sheet review typically take?

For a straightforward VC term sheet, a thorough first-pass review by an experienced associate takes two to four hours. A more complex PE LOI or M&A term sheet, particularly one requiring cross-referencing against a CIM and financial model, can take a full day or more — especially if it arrives mid-process when the team is already stretched. The review timeline compresses significantly under deal pressure, which is precisely when the risk of missing something material is highest. AI-assisted workflows are compressing first-pass review to under an hour, with structured outputs ready for senior review before the deal team has assembled.

+

How is AI being used for term sheet review?

AI is being applied across several layers of the term sheet review process. The practical result is that first-pass review that previously took several hours can be completed in under an hour, with senior associate time focused on the flagged items that require judgment rather than the mechanical layer of extraction and structuring.

+

What should I look for in an AI term sheet review tool?

The capabilities that matter most for actual deal work: clause-level extraction with source citations (so every data point is traceable back to its page in the source document — essential for IC materials); firm playbook integration (so flagging reflects your standards, not generic market benchmarks); cross-document reconciliation (comparing term sheet terms against CIM, model, and data room); redline and version comparison (tracking changes across circulating documents, including accepted tracked changes that no longer appear as redlines); agentic workflow triggers (so review initiates automatically on document arrival); and an audit trail that logs what was extracted, flagged, and reviewed. The distinction between a useful single-pass summarization tool and a genuine workflow change is the agentic layer — whether the system can execute a multi-step review process end-to-end or whether it requires a human to orchestrate each step manually.You've

+

Imogen is an experienced content writer and marketer, specializing in B2B SaaS. She particularly enjoys writing about the impact of technology on sectors like law, finance, and insurance.