AI implementation

16 min read

—

Add-on acquisitions now represent over 70% of PE buyout activity. But most integrations fail to capture planned synergies. Here is where execution breaks down and what the best-organized firms do differently.

Private equity buy-and-build is no longer a niche strategy. In 2024, add-on acquisitions represented approximately 73% of all US PE buyout transactions, according to Cherry Bekaert's 2025 Private Equity Report, (up from under 50% a decade ago). The logic is compelling: acquire a platform company at a mid-market multiple, layer in add-ons at similar or lower multiples, realize cost and revenue synergies across the combined entity, and exit a business that is larger, more defensible, and priced at a premium multiple to what each piece was worth individually. In a market where financial engineering has been compressed by higher rates and compressed entry multiples, the buy-and-build model is one of the few remaining routes to the return profiles LPs expect.

But the strategy has a failure mode that does not appear in the investment committee memo, and that most GPs are reluctant to discuss openly: integration execution. The thesis works on a spreadsheet. It works less reliably in the 12 to 24 months after close, when the management team that was acquired to run the platform company is simultaneously trying to manage three acquired add-on companies, prepare for the next acquisition, and produce the quarterly reporting package the GP needs to show LPs. More than 70% of post-merger integrations fail to capture planned synergies. In PE-backed buy-and-build programs, the number may be higher, because the pace of acquisition compounds each failure before the previous one is resolved.

This article examines where the execution breaks down, what the research on integration outcomes actually shows, and what the best-organized PE firms do structurally to make buy-and-build work beyond the second add-on.

In this article:

Why buy-and-build dominates PE value creation in 2026 and what the model depends on

The three failure modes that derail add-on programs after the second acquisition

What the integration research shows about synergy capture rates in PE-backed platforms

The operational levers that separate successful serial acquirers from the ones that stall

How AI agents are changing the integration execution workflow in 2026

AI for document processing

Track add-on integration progress across every portfolio company

Get started today

Why buy-and-build dominates PE value creation in 2026

The leverage-driven return model that defined PE in the 2010s depended on cheap debt, compressed entry multiples, and an exit environment that rewarded scale. All three of those conditions have become less reliable. Debt is more expensive and LTV ratios have compressed. Entry multiples in most mid-market sectors remain elevated relative to historical norms. And the exit window that GP after GP has been waiting for has been slower to open than anyone's fund model anticipated. Against this backdrop, buy-and-build is attractive precisely because it generates multiple sources of value simultaneously; these are sources that are, in theory, within the GP's control.

The multiple arbitrage component is the most straightforward: a platform company with 10 million USD in EBITDA might trade at 8x. A bolt-on with 2 million USD in EBITDA, acquired as a standalone business, might trade at 5x. Combined, the platform exits at 10-12x on a 14 million USD EBITDA base, which is a materially different outcome than either company would have achieved independently. The synergy component adds additional EBITDA: cost savings from back-office consolidation, revenue growth from cross-selling the combined customer base, and pricing power from increased market share. The operating improvement component benefits from the GP's active involvement in the platform company's management in ways that a standalone company might not have access to.

In sectors where the market is fragmented across healthcare services, professional services, specialty distribution, home services, and software. Buy-and-build is effectively the default mid-market strategy. The platform company thesis is the starting assumption, and the add-on pipeline is an underwriting criterion rather than an optional upside scenario. LPs understand this and, in many cases, expect it: the fund that returns 2.5x on a buy-and-build platform is doing the work LPs are paying for. The fund that returns 1.6x on the same model is the one that bought the thesis and could not execute it.

The three failure modes nobody writes into the IC memo

Integration failure in PE-backed buy-and-build programs tends to follow recognizable patterns. The specific circumstances differ by sector and management team, but the structural problems are consistent enough that experienced operating partners can identify them before close if they are looking for them. Three failure modes account for the majority of outcomes where synergies were modeled but not realized.

Failure mode 1: Management bandwidth

The management team that built the platform company was hired or incentivized to run one business. After the second or third add-on, they are running three or four businesses simultaneously while also managing the integration work streams from the previous acquisitions and doing diligence on the next one. The 100-day integration plan assumes that the platform CEO has the capacity to execute it. In practice, the platform CEO is the single biggest constraint on how fast and how well integration proceeds.

The M&A Integration Handbook documents this precisely: after the intense focus required to advance a deal to signing, companies often call on management teams that lack merger-management experience to execute the integration. Although the leaders may be experienced in running their companies, they often realize too late that integration is a different discipline requiring highly specific expertise. In a buy-and-build program, this realization typically arrives at the third add-on, when the cumulative integration debt from the previous two acquisitions makes the third deal significantly harder than the model suggested.

The firms that manage this well treat integration as a firm-level resource problem, not a portfolio company problem. They either hire a dedicated integration leader at the platform level before the third add-on or deploy operating partner time specifically to integration work streams rather than strategic oversight. The firms that struggle treat integration as something the management team will figure out alongside everything else they are doing.

Failure mode 2: Systems and data fragmentation

Every add-on comes with its own financial reporting stack, ERP, CRM, payroll system, and industry-specific software. A platform company that has completed four add-ons is, on average, running four different accounting systems, three different CRM instances, and two or three different payroll platforms simultaneously. The integration plan typically includes a systems rationalization work stream scheduled for Year 2. Year 2 arrives and the platform is preparing the fifth add-on.

The consequence is that no one in the GP's organization has a real-time, accurate view of the combined platform's performance at any given point in the quarter. The quarterly board pack is assembled manually by someone at the platform company who pulls data from each add-on's system, reformats it into a common template, and passes it to the GP. The process takes two to three weeks every quarter, and the output is as accurate as the person doing the reformatting could make it under time pressure. Management decisions are made on data that is 30 to 45 days old by the time it reaches the board.

The systems fragmentation problem compounds into a diligence problem for the next acquisition and for the eventual exit. When the GP is evaluating a fifth add-on, the financial data available from the combined platform is the product of four different accounting systems reporting through a manual consolidation process. Historical performance figures that appear consistent may reflect different accounting conventions across the add-ons rather than actual operating trends. A prospective buyer conducting diligence on the platform at exit will find the same data quality issues the GP has been managing internally, and will price the uncertainty accordingly. The multiple expansion the GP modeled at entry is harder to achieve when the data room reflects four years of fragmented reporting rather than a coherent financial history. Resolving the systems problem early in the hold period is an investment in exit credibility, also a quarterly reporting improvement.

Failure mode 3: Synergy timing mismatch

Synergies are underwritten at close. They are realized, when they are realized at all, 12 to 24 months later. The disconnect between these two timelines creates persistent pressure on the GP: the model shows synergies beginning to appear in the quarters immediately after close, while the operating team is still in the process of understanding what it acquired and building the working relationships required to capture anything.

Research on integration outcomes is consistent on this point: overlooking integration planning considerations delays synergy realization by 6 to 12 months, compressing the return profile on deals that were modeled on earlier synergy timing. In a buy-and-build program where the GP is doing four or five add-ons over three years, each synergy delay compounds. The exit multiple the LP was shown at commitment is achievable in theory. In practice, it requires every add-on to realize synergies on the modeled schedule, which requires integration to work, which requires someone to be accountable for it full-time.

Each add-on acquisition adds new workflows, systems, and reporting dependencies to the platform. Without a documented integration playbook, the cumulative complexity of managing simultaneous work streams across multiple acquired entities compounds with each new transaction.

What the research on M&A integration outcomes actually shows

The claim that most acquisitions fail to create value is not a new observation, but the research is worth revisiting in the specific context of PE buy-and-build programs. The aggregate numbers apply with particular force to multi-add-on platforms, where each acquisition is a bet that the previous integrations have reached sufficient maturity to absorb another one.

The M&A Integration Handbook identifies the consistent factors behind failed integrations: companies calculate the deal in terms of acquisition cost and expected benefits rather than total cost of ownership, including integration resources; integration knowledge and experience are not respected as a core competency; and there is no senior executive serving as a dedicated integration champion with authority to make and enforce decisions across the acquired and acquiring entities. These are structural deficits, not execution mistakes, and they are present in most buy-and-build programs from the first add-on.

The private equity-specific research adds a further dimension: a GP that successfully exits one buy-and-build platform may have no replicable integration capability. The last investment worked because of the management team, the sector, and the timing, not because the firm had built an integration competency that transfers to the next fund. This is the trap that experienced LPs are beginning to probe more specifically: not whether the last platform worked, but whether the firm has the operational infrastructure to execute the same strategy again under different market conditions.

The gap between modeled and actual synergy realization becomes visible when actual financial performance is systematically compared against the pro-forma assumptions built at deal close. Most GP organizations do not currently do this comparison in a structured, documented format across all add-ons.

The operational levers that separate successful serial acquirers from the ones that stall

The integration playbook: written before the second add-on

The firms that consistently execute buy-and-build programs treat integration as a firm-level competency codified in a playbook that exists before the second add-on closes. The playbook is not a checklist; it is a decision framework that specifies: Day 1 stabilization priorities (what must be done before the first weekend to preserve customer relationships, employee stability, and financial controls); the 90-day work stream structure; systems rationalization decision criteria; the post-close KPI set that will be reported to the GP; and escalation protocols for integration issues that require GP involvement.

The M&A Integration Handbook is direct on this point: if a platform is doing many bolt-ons in succession or concurrently, a robust integration playbook is the prerequisite for managing the complexity. For lower and middle market transactions, the goal is to complete the bulk of integration initiatives within 90 to 120 days. The work streams that exceed this timeline should be explicitly defined with completion dates, not left open-ended on a master roadmap.

The firms that struggle with buy-and-build tend to build the playbook after the third add-on, when the absence of one has already created a crisis. By that point, the platform company's management team is demoralized from three consecutive integration experiences that were longer and harder than they were told to expect, the GP's operating partner is fielding escalations from three different work streams simultaneously, and the fourth add-on is already in diligence. Building a playbook in this environment is possible, but it takes longer and the first draft is written defensively rather than from a position of strategic clarity about what the combined platform is supposed to become.

The post-close KPI discipline that a playbook enables is worth quantifying. A GP operating without a standardized post-close KPI set is receiving different metrics from each add-on each quarter, defined differently, reported on different timelines, and covering different aspects of the business. A playbook that establishes a common reporting template before the first add-on closes means the GP receives comparable data across all portfolio companies from day one. That comparability is what makes synergy tracking possible, and synergy tracking is what enables the GP to demonstrate to LPs that the value creation thesis is being executed rather than modeled. The firms that produce this evidence consistently at quarterly board meetings are in a different fundraising conversation than those that rely on management commentary to describe how integration is progressing.

Talent retention in founder-led add-ons

The majority of mid-market add-ons are founder-led businesses. The founder sold because they wanted liquidity and, in some cases, access to capital for growth. They did not necessarily want to become a regional general manager in a PE-backed rollup reporting to a corporate structure they had no hand in creating. The standard retention mechanism (rollover equity, a management carve-out, a two-year employment agreement) is sufficient to keep the founder in the building for 12 months. It is rarely sufficient to keep them engaged as a collaborative team member in an entity where their operational autonomy has been reduced and their cultural norms have been absorbed into someone else's platform company.

Research on integration and talent outcomes is consistent: it is often better to obtain a third-party assessment of key players in both merging organizations, using consistent criteria, rather than relying on the GP's own judgment about who will stay and who will leave. This assessment needs to happen before close, not after. By the time a GP discovers that the add-on's head of sales is disengaged and preparing to leave, the customer relationships that made the acquisition attractive are already at risk.

The talent retention failure is particularly damaging in professional services and knowledge-intensive sectors where the add-on's value is substantially its people. A healthcare practice acquired for its patient volume and its physician relationships is worth materially less if half the physicians leave within 18 months of close. The synergy model assumed the revenue base was stable. The integration plan did not have a line item for physician retention bonuses or a cultural onboarding process designed specifically for high-autonomy professionals who are not used to operating within a corporate governance structure.

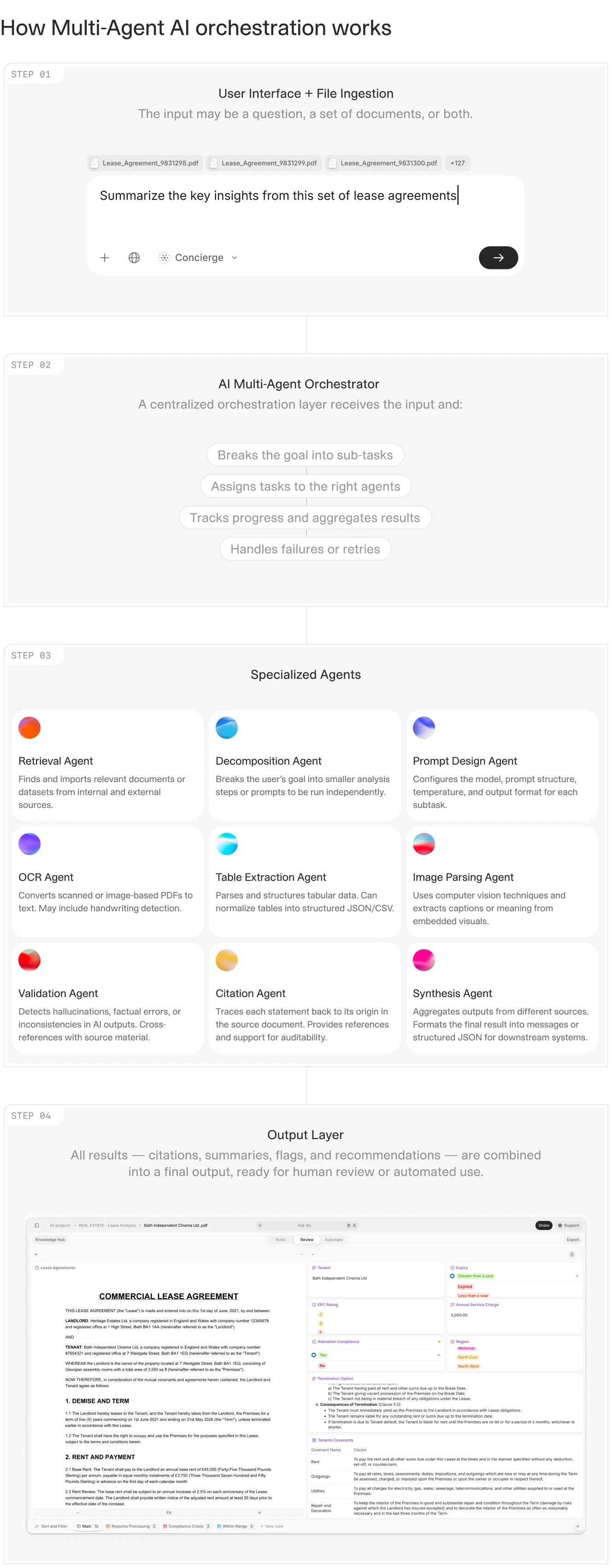

Multi-agent AI architectures divide integration document processing into specialized tasks: one agent ingests financial statements, another extracts KPIs, a third compares outputs across add-ons. The orchestration layer coordinates these agents and consolidates the results into a structured output without manual assembly at each step.

How AI agents change the integration execution math

The three failure modes described above are all, at their core, data and workflow problems. Management bandwidth is consumed by manual processes that could be automated. Systems fragmentation creates a reporting problem that compounds quarterly. Synergy timing mismatch is invisible because no one is tracking actual versus modeled performance in a structured, documented format. AI document agents address all three of these problems at the level where the work actually gets done.

Cross-add-on KPI consolidation

The most immediate consequence of data fragmentation in a multi-add-on platform is that no one has a consolidated view of the combined entity's performance at any point in real time. Each add-on's quarterly reporting package arrives in a different format, populated from a different system, using different metric definitions. The analyst assembling the board pack has to normalize these inputs manually, a process that takes two to three weeks and produces output that is as accurate as the normalization decisions made under time pressure.

An AI agent configured for the platform's reporting document types can ingest each add-on's quarterly package, extract the relevant KPIs, apply the platform's standard metric definitions, and output a consolidated performance view without manual assembly. For context on how this connects to the broader portfolio data infrastructure, the portfolio monitoring guide covers how KPI collection from portfolio companies feeds fund-level reporting; the same extraction logic applies within a buy-and-build platform across its add-on companies.

Integration document processing at close and ongoing

Every add-on close generates a document workload: employment agreements to review, customer contracts to catalogue, supplier terms to compare against the platform's existing agreements, financial statements to spread for the prior-period analysis. This workload is proportional to the number of add-ons and compounds over time: a platform with five add-ons maintains five separate document archives alongside the platform's own records, and every new add-on adds to the pile.

The document comparison agent from V7 Go is designed precisely for this work stream: compare two structured documents, identify differences in key terms, and report results with citations to the specific clauses that differ. Applied to add-on integration, this means the GP can see, within hours of receiving an add-on's contract library, which customer agreements have different termination clauses, which supplier contracts have pricing terms that need to be renegotiated under the platform umbrella, and which employment agreements contain non-compete language that affects the integration plan.

The financial statement spreading automation handles the historical financial statements for each add-on, extracting the prior-period data the GP needs to validate the synergy model against actual pre-close performance and build the post-close baseline for tracking synergy realization.

Synergy tracking across the post-close period

The most consequential AI application in buy-and-build integration is not about processing speed. It is about the quality of the information the GP uses to make decisions. Synergy tracking requires comparing actual financial performance against the pro-forma synergy model built at deal close, for each add-on, by synergy category, at each reporting period. This comparison reveals whether the cost synergies underwritten at close are materializing, whether the revenue cross-selling assumptions are on track, and which add-ons are performing below the modeled baseline.

The GP that can answer these questions with data — at every quarterly board meeting, for every add-on in the portfolio — is managing the buy-and-build program with the operational discipline that the strategy requires. The GP that cannot answer them is managing by narrative: the CEO says integration is going well, synergies are tracking, the next add-on will be different. For context on how AI applies across the broader private equity workflow, the generative AI in finance guide covers the full picture from diligence through portfolio management.

Extraction with source citations means the GP can trace every figure in the consolidated platform report back to its originating document. Applied to synergy tracking, this makes variance analysis between modeled and actual performance a routine output rather than a quarterly manual exercise.

The GP's honest conversation about integration capacity

The buy-and-build strategy is not fundamentally a deal sourcing or underwriting challenge. It is an execution challenge. The firms that perform consistently well on multi-add-on programs are the ones that built integration as a firm-level competency: with a documented playbook, a dedicated operating resource, and the discipline to review integration performance as rigorously as they review financial performance. These are not large-firm advantages. They are organizational choices that are available at any fund size.

LPs are beginning to ask for this evidence during fund raises. When a GP is raising Fund III on a buy-and-build track record from Fund II, the question that sophisticated LPs are asking is whether the platform worked — and how. It is: what is the integration scorecard from Fund II? How many add-ons closed, how many are on track against the original synergy model, and what is the post-close management retention rate across the portfolio? These are questions that require data, and the GP that cannot produce that data is in a different fundraising conversation than the one that can.

The firms that will win the buy-and-build game in the next cycle are not the ones with the most aggressive add-on pipelines. They are the ones that can show, with documentation and data, that the integrations from the previous fund are working. That evidence starts accumulating the day after each close, and it requires the operational discipline to track it, report it, and improve it with each successive transaction.

If the data management and document processing work that integration requires is consuming analyst time that should be going toward value creation, V7 Go's document intelligence platform is built for the document types that buy-and-build integration generates: financial statements, employment agreements, customer contracts, and quarterly operating reports from add-on companies reporting in non-standard formats. Define the extraction schema once, run it across every add-on's document library, and get structured, cited outputs that feed the integration work streams rather than adding to the manual processing backlog.

What is a buy-and-build strategy in private equity?

A buy-and-build strategy, also called a platform strategy or roll-up, involves a private equity firm acquiring a primary company (the platform) and then making a series of smaller add-on acquisitions that are integrated into the platform over the hold period. The strategy creates value through multiple arbitrage (buying smaller companies at lower multiples than the combined entity will trade at on exit), cost and revenue synergies from combining operations, and operating improvements that a standalone company might not have access to. Add-on acquisitions have grown to represent approximately 73% of all US PE buyout transactions, making buy-and-build the dominant value creation strategy in mid-market private equity. The strategy works when integration is executed well and creates significant problems when it is not.

+

What percentage of PE add-on integrations fail to capture their planned synergies?

Research on post-merger integration outcomes consistently finds that more than 70% of integrations fail to capture the synergies that were modeled at deal close. In private equity buy-and-build programs, this rate may be higher because the pace of acquisition means each new add-on is integrated before the previous ones have reached operational maturity. Synergy delays of 6 to 12 months are common even in integrations that ultimately succeed, because the operating team needs time to understand what was acquired before they can systematically extract value from combining it with the platform. The firms that consistently capture synergies treat integration as a full-time competency, not a secondary task for the management team to complete alongside running the business.

+

What is the most common reason add-on integration fails in PE-backed companies?

The most common structural reason add-on integration fails is management bandwidth: the platform company's leadership team is asked to manage integration work streams simultaneously with running the operating business and preparing for the next acquisition. Integration requires a different skill set than operating a business, and leaders who are effective at building companies often lack experience with the specific disciplines — work stream management, systems rationalization, talent assessment under uncertainty — that integration demands. A contributing factor is that most PE firms do not calculate integration cost as part of the total cost of ownership when evaluating a deal, so the resources required to execute integration well are chronically underfunded relative to what the process actually requires.

+

What should a PE integration playbook include?

An effective PE integration playbook for a buy-and-build program should include: Day 1 stabilization priorities covering customer communication, employee retention, and financial controls; a 90-day work stream structure with defined owners and deliverables for each functional area; systems rationalization decision criteria specifying which systems get consolidated onto the platform and which are left independent during the integration period; a post-close KPI set that will be reported to the GP in a standardized format; and escalation protocols for integration issues that require GP involvement. The playbook should be written before the second add-on closes and updated after each integration with lessons learned. For lower and middle market transactions, the goal is to complete the bulk of integration initiatives within 90 to 120 days, with any longer-tail work streams explicitly scoped with completion dates.

+

How do AI agents help with post-close integration in PE-backed platforms?

In private equity buy-and-build programs, the platform company is the primary acquisition that anchors the strategy. It is typically large enough to serve as an organizational base for subsequent acquisitions, has an established management team, and is in a sector where fragmented smaller competitors can be acquired and integrated. An add-on is a smaller acquisition made by the platform company during the hold period, typically at a lower entry multiple than the platform itself, that is integrated into the platform to increase scale, add geographic coverage, expand the customer base, or add capabilities. The value creation thesis for the combined entity depends on the platform and its add-ons being worth more together, post-integration, than they were worth separately at their respective acquisition prices. This spread between acquisition multiples and exit multiples is the multiple arbitrage component of buy-and-build returns.

+

What is the difference between a platform company and an add-on in private equity?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.