Document processing

15 min read

—

Management equity pools represent 15-20% of common equity in PE deals, but the structure behind that number: vesting, leaver provisions, ratchets, and dilution risk; it determines whether the MIP actually produces alignment.

When a private equity firm acquires a company, one of the first conversations it has with the existing management team concerns equity. The framework is presented as an alignment tool: management earns a meaningful share of the exit proceeds because management is responsible for the outcome. The numbers look attractive. A 15 to 20% equity pool on a company exiting at 10x EBITDA represents the kind of wealth generation that most operating executives never encounter in a corporate career. But the structure behind those numbers is considerably more complex than the headline figure suggests, and the terms that govern how that equity actually pays out are negotiated and documented before the management team has the experience to understand what they are agreeing to.

The information asymmetry in these conversations is structural. The GP's deal team has structured and negotiated management equity arrangements across dozens of transactions. The management team is typically doing it for the first time. The shareholder agreement that governs the equity arrangement runs to dozens of pages of definitions, conditions, and cross-references. The term sheet that preceded it was considerably simpler. In a mid-market buyout, management teams rarely engage specialist legal counsel to review the equity terms: the deal momentum, the existing relationship with the GP, and the assumption that the terms are standard all work against it. The provisions that matter most: leaver definitions, dilution mechanics, and ratchet triggers are the ones that receive the least scrutiny before signing and the most scrutiny after something unexpected happens.

This article covers the structural reality of management incentive plans in PE-backed companies: what the equity pool actually represents in the capital structure, how vesting works across time-based and performance-based components, what leaver provisions look like in practice versus what they sound like in an investment committee presentation, and how ratchets create upside potential that is real in good exit scenarios and irrelevant in bad ones. It also covers the GP's perspective — what the research shows about how management equity structure affects operating outcomes during the hold period, and what distinguishes MIPs that produce alignment from those that produce resentment.

In this article:

What the management equity pool represents in the PE capital structure

How time-based and performance-based vesting work together in PE-backed MIPs

Good leaver, bad leaver, and the provisions that management teams misread

How ratchets work and what dilution risks the original grant is exposed to

What the research shows about MIP structure and hold period operating outcomes

AI for document processing

Review MIP terms without parsing every clause manually

Get started today

What the management equity pool actually represents

The Private Equity Toolkit documents a consistent market standard: the total management equity award in a PE-backed company typically represents about 15 to 20% of the company's common equity. It is not unusual for up to half of that pool to be allocated solely to the CEO. The aim is to ensure that a successful private equity transaction produces transformational wealth for the person most accountable for delivering results. The remaining pool is distributed among a small group of senior executives and critical employees who take daily responsibility for driving financial performance.

The key phrase in the above is "common equity." Management equity is not 15 to 20% of enterprise value. It is 15 to 20% of the equity value that remains after the debt and preferred equity in the capital structure have been repaid. In a typical PE buyout, the GP uses a combination of debt and equity to acquire the business. The debt is senior. The GP's preferred equity often sits above the common equity in the distribution waterfall. Management's common equity sits at the bottom. This means that on a deal with significant leverage, management's equity can represent a substantial percentage of a relatively thin slice of the total enterprise value.

This structure exists by design. It is intended to make management's equity highly sensitive to performance outcomes: if the company does well and the enterprise value grows significantly above the entry price, management participates meaningfully. If the company performs at or below the entry price, the common equity may be worth little or nothing. This is the alignment mechanism the GP is creating. It is also the first thing that management teams discover, sometimes with surprise, when they read the actual documents rather than the pitch presentation.

The award is usually structured as sweet equity: shares purchased at a nominal price, typically well below fair market value at the time of the transaction. This creates an immediate economic benefit for management and a tax event that varies by jurisdiction and structure. In the United States, the most common structure is a profits interest or restricted stock unit. In the UK and much of Europe, share options at a nominal strike price are more common. The mechanics differ, but the economic intent is the same: management acquires the right to a percentage of the company's equity appreciation over the hold period at a cost well below what the PE firm paid per share of common equity.

How vesting works in PE-backed companies

The concept behind vesting is straightforward: a manager's equity is not fully owned until certain conditions have been met. In PE-backed companies, vesting serves two purposes simultaneously. It retains management for the hold period; you cannot leave in year two and take the full grant with you. And it links a portion of the award to the performance outcomes the GP modeled at deal close, creating an incentive to deliver rather than simply to endure.

Research on management incentive plans finds that approximately 62% of PE-backed MIPs combine time-based and performance-based vesting criteria, according to Goodwin's 2024 incentive equity analysis,-based vesting criteria, according to Goodwin's 2024 incentive equity analysis. In the United States, a common split allocates 50% of the total grant to time-based vesting over four or five years, with the remaining 50% tied to performance targets. In Europe, the performance component is often linked to investor return thresholds rather than absolute financial metrics: the management team vests a larger portion of the pool when the GP achieves a specified multiple on invested capital or IRR. The distinction matters for incentive design — a target tied to the GP's return profile aligns management with LP outcomes, while a target tied to company EBITDA aligns management with operational execution.

Time-based vesting in PE-backed companies typically runs on a four or five year schedule, which corresponds to the expected hold period. This is intentional: if the GP plans to exit in year four, a four-year vesting schedule means that a fully engaged management team will have earned their full time-based allocation by the point the company goes to market. The structure breaks down when hold periods extend beyond the original vesting schedule, which has become more common as exit markets have tightened. A management team that is fully vested in year five of a seven-year hold period has no remaining time-based incentive for years six and seven. This is one of the structural drivers behind the recent interest in MIP resets and refreshed equity grants for extended hold scenarios.

Performance-based vesting schedules typically use a combination of absolute and relative targets. Absolute targets might include minimum EBITDA thresholds or revenue growth milestones. Relative targets compare performance to the original investment case, so a management team that delivers 110% of the modeled EBITDA in year three may accelerate vesting while one that delivers 85% may see performance-based vesting delayed or forfeited. The specific mechanics are documented in the shareholder agreement and are often far more granular than management's initial understanding of the structure.

Equity grant documents contain the specific vesting conditions, performance thresholds, and leaver provisions that govern how management's equity pays out. AI agents configured for shareholder agreements and equity grant letters can extract and structure these terms for the entire management team in hours rather than weeks.

The leaver provisions that management teams read too quickly

The leaver provisions in a PE-backed management equity plan are among the most consequential clauses in the shareholder agreement, and among the most commonly misunderstood. The Private Equity Toolkit defines good and bad leavers precisely: good leavers are those who die, become critically ill or incapacitated, retire at an appropriate age, or are deemed to be good leavers by the Board of Directors. Upon departure, good leavers most commonly sell their shares at market value. Bad leavers are those who resign for any other reason than the above, or who are terminated for cause. Bad leavers are typically compelled to sell their shares at the lower of cost or market value, which in most cases means they receive approximately nothing for unvested equity and a return of their nominal investment for vested equity.

The category that creates the most disputes is not good or bad leaver — it is the category between them. In the UK, it is common for three categories to exist: good, bad, and intermediate leavers, with intermediate covering situations like voluntary resignation without cause, where the management team member is leaving for personal reasons rather than to compete or to harm the company. Intermediate leavers typically receive fair market value for vested equity but forfeit unvested grants. In the United States, most agreements use only two categories, which means the full negotiating weight falls on where the line between good and bad is drawn.

What makes these provisions practically complex is the definition of resignation. A management team member who is given reduced responsibilities, relocated, or placed under a new reporting structure may argue that they have been constructively dismissed and should be treated as a good leaver. The GP will argue that the change in circumstances does not meet the threshold for constructive dismissal and that the departure is voluntary. The resolution of this dispute depends entirely on how the shareholder agreement defines these terms, and on whether the management team had legal counsel review the documents at the time they signed them. Many management teams in mid-market buyouts do not.

AI agents reduce the administrative burden of equity administration at scale.

The practical implication for GPs is that badly drafted leaver provisions are a source of litigation risk and management relationship damage at precisely the moment when the company is preparing for exit. A management team member who believes they are being treated as a bad leaver when they consider themselves a good leaver is unlikely to invest maximum effort in exit preparation. This is a deal execution risk that originates in the equity documentation, not in the operating plan.

Ratchets: how management earns above the base allocation

A ratchet is a mechanism that increases the management team's percentage of the equity distribution when the GP's return exceeds specified thresholds. Ratchets are designed to reward exceptional performance — the management team that delivers a 3x return for the GP earns a higher percentage of the exit proceeds than one that delivers a 1.5x return, even if both teams received the same base allocation at deal close.

There are two main ratchet structures. An excess equity ratchet applies the additional allocation only to equity value in excess of the threshold that triggers the ratchet. For example: the management pool is increased by 5% of the equity value in excess of a valuation at which the investor achieves a 2.5x return on invested capital. A total equity ratchet applies the additional allocation to the total ordinary equity value once the threshold is reached: the management pool is increased by 5% of the total equity value once the investor achieves a 2.5x return. The total equity ratchet is more valuable to management; the excess equity ratchet is less costly to the GP and more common in practice.

The behavioral effect of ratchets is well-understood: they create strong incentives to push operating performance beyond the base case, particularly in the final 12 to 18 months before exit when the GP and management team are preparing the company for sale. The risk is that management makes decisions oriented toward exit-period metrics at the expense of long-term business health — under-investing in product development, delaying capital expenditures, or optimizing reported EBITDA in ways that a sophisticated buyer will identify and discount in their valuation. The GP that structures the ratchet thoughtfully specifies targets that require genuine operating improvement rather than accounting adjustments.

The dilution problem that the base grant does not reflect

The management equity pool described at deal close is not a fixed percentage of the company's equity for the life of the investment. It is a percentage of the common equity at a point in time, and that percentage is subject to dilution from two common sources during the hold period.

The first is new management hires. A company that acquires new capability (a CFO brought in to prepare for exit, a Chief Revenue Officer hired to lead a sales build-out, who typically grants equity to the new hire as part of the compensation package. That equity comes from the same pool. If the original pool was 15% of common equity and the new CFO receives 1.5% of common equity, the remaining management team's proportional share of the pool has been reduced. The original shareholder agreement will specify whether new grants can dilute the existing participants or whether they come from a reserved pool. Management teams that do not read this provision carefully at signing discover it when the first new hire is announced.

The second source of dilution is add-on acquisitions. When the platform company acquires a bolt-on in a buy-and-build program, the acquired management team often receives equity in the combined entity as part of the acquisition terms. This equity may come from the existing management pool or from a new issuance, depending on the structure negotiated at the time of the add-on. Either way, the original management team's effective ownership of the combined entity changes, sometimes materially, after each acquisition. A management team that modeled their equity outcome on a standalone company and then watched the platform complete four add-ons may find at exit that their percentage of the combined entity is substantially different from what they initially understood.

What the data shows about MIP structure and hold period outcomes

The research on management equity and operating performance in PE-backed companies is consistent on the directional finding: companies where the management team holds meaningful equity stakes with achievable performance conditions outperform those where equity is nominal, heavily diluted, or structured around unreachable targets. Private Capital notes that the award of substantial share packages to management, sometimes tied to a requirement to invest a portion of their personal wealth alongside the GP, was historically a powerful alignment mechanism precisely because it put management's personal financial interests at risk alongside the GP's. The co-investment requirement, where management reinvests a portion of their own capital rather than receiving a pure grant, strengthens this alignment further.

Research on European PE-backed companies documents a related finding: investors place significant weight on the fact that members of the management board hold equity stakes of up to 20%, because equity ownership at this level correlates with the level of engagement and operational focus that drives value during the hold period. The implication is symmetric: management teams with nominal or heavily conditioned equity are less likely to demonstrate the same level of engagement, particularly in years three and four of a hold period when the initial excitement has faded and the complexity of running a PE-backed business has become clear.

The design failure that GPs most commonly identify in retrospect is performance targets set too high relative to what the management team could realistically control. A performance-based vesting schedule tied to an EBITDA target that required both operational improvement and favorable market conditions effectively converted the management team's equity from an incentive into a source of frustration by year two of the hold period. The GP that recalibrates those targets mid-hold through a documented MIP reset preserves more alignment than the one that leaves an unreachable target in place and watches the management team disengage.

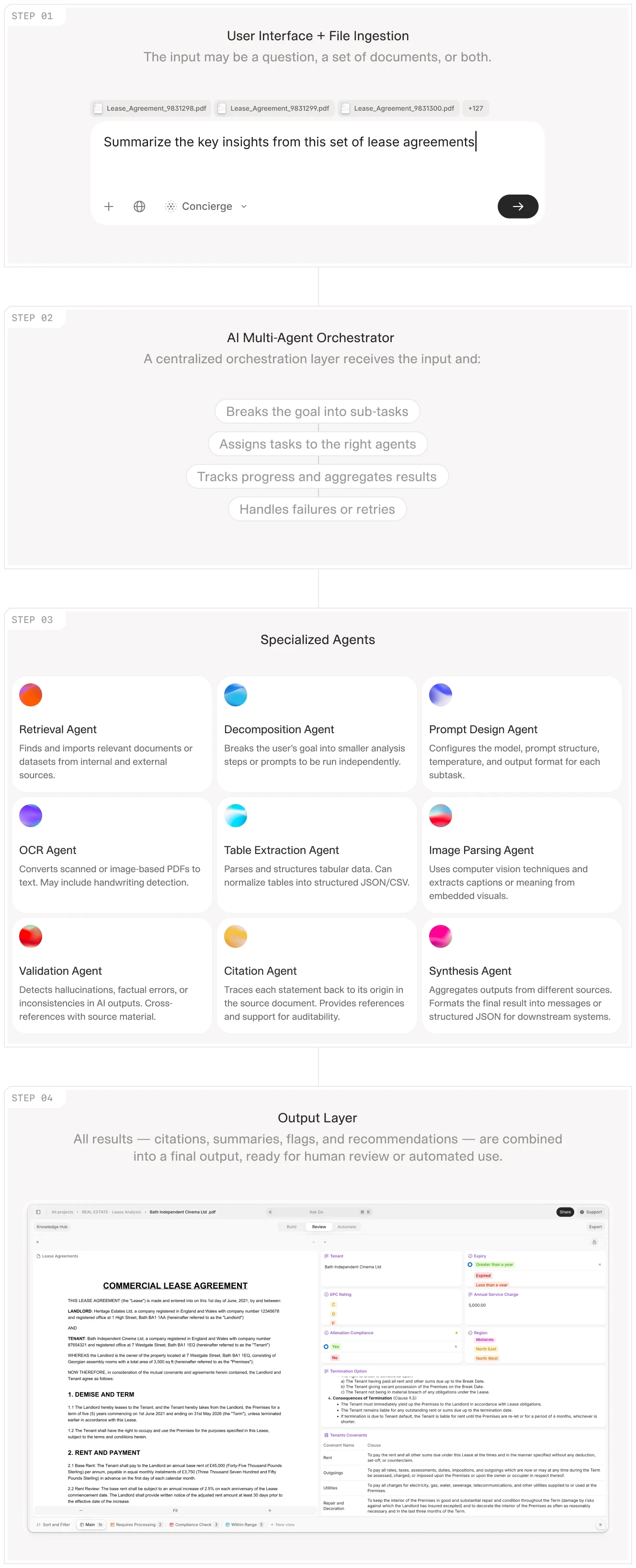

Where AI agents reduce the administrative burden of equity management

Managing the equity position of a PE-backed portfolio company's management team requires tracking, across each participant, the grant date, grant type, total award size, vesting schedule, performance conditions, leaver category definitions, and any amendments made during the hold period. For a portfolio company with eight management team members, two add-on acquisitions that brought their own equity arrangements, and a refreshed grant for a CFO hired in year three, the equity ledger is a document set, not a single spreadsheet. The source documents include the original shareholder agreement, individual equity grant letters, amendment agreements, and any consent documents related to add-on equity structuring.

An AI agent configured for these document types can extract the key terms from each document in the set: grant amounts, vesting start dates, performance thresholds, leaver definitions, and ratchet triggers. The output is a structured equity summary for each participant, with every figure cited to its source document. This matters for two reasons. First, it makes the equity position auditable: when a management team member has a question about their entitlement, the answer can be traced to the specific clause in the specific agreement. Second, it enables the GP to identify inconsistencies across the management team's grant letters, such as different definitions of the leaver categories or different vesting schedules for participants who were told they had equivalent arrangements.

For context on how AI document extraction applies to the full private equity workflow, the AI in private equity guide covers use cases from initial screening through portfolio management. The document comparison agent from V7 Go handles cross-document consistency checks directly — comparing equity grant letters across participants to flag where the terms differ and surfacing those differences for the GP's review before they become disputes at exit. The portfolio monitoring guide covers how performance data tracked during the hold period feeds into the performance-based vesting calculations that determine the final equity entitlement at exit.

The same multi-agent orchestration architecture that processes lease agreements and commercial contracts applies to equity documentation: separate agents handle extraction, comparison, and summarization tasks, with an orchestration layer coordinating outputs and flagging inconsistencies for review.

The MIP that produces alignment versus the one that produces resentment

The gap between a well-designed management equity plan and a poorly designed one is not usually in the headline pool size. It is in the details that determine whether management's experience of the hold period is one of shared purpose or accumulated frustration. A management team that understood what they signed, has realistic performance targets, and knows exactly what their equity is worth at various exit scenarios is a fundamentally different partner than one that is discovering the complexity of the structure two years into the hold.

The GPs that get this right invest time before signing in explaining the full structure to the management team in plain terms: here is what the pool represents in the capital structure, here is the vesting schedule and what accelerates or delays it, here is the precise definition of good leaver and bad leaver and here are the scenarios that fall into each category. This conversation is uncomfortable because it involves explaining downside scenarios that neither party wants to dwell on at the time of a deal close. But it prevents the far more uncomfortable conversation that arises when a management team member is leaving under circumstances that both parties interpret differently based on the same document.

LPs doing operational due diligence on a GP's portfolio are increasingly treating the management equity structure as a diligence item. The question goes beyond what percentage management holds, but whether the structure has been documented clearly, whether the performance conditions are grounded in the investment case, and whether the leaver provisions have been tested by actual departures. A GP that has handled a management departure cleanly, with the equity terms applied as documented and the relationship preserved for exit preparation, and has demonstrated something about their operational standards that a pristine portfolio without any departures cannot.

If the administrative and documentation work behind equity management is a constraint on the GP's ability to maintain accurate, auditable records across the portfolio, V7 Go's document intelligence platform is built for the legal and financial document types that equity administration requires: shareholder agreements, equity grant letters, amendment schedules, and consent documents. Define the extraction schema once, run it across every management team member's documentation, and get a structured equity ledger with every term cited to its source document and every inconsistency flagged before it becomes a dispute.

What is a management incentive plan (MIP) in private equity?

A management incentive plan (MIP) in private equity is an equity compensation structure that grants the portfolio company's management team a stake in the company's equity. The goal is to align management's financial interests with the GP's return objectives by making a significant portion of management's compensation dependent on the company's exit value. Typical MIP pools represent 15 to 20% of the company's common equity, distributed among a small group of senior executives and critical employees. The CEO often receives up to half of the total pool. Management's equity sits at the bottom of the capital structure below debt and preferred equity, which means it is highly sensitive to performance outcomes: significant above-entry value creation produces meaningful wealth for management, while performance at or below entry value may result in little or no payout.

+

How is management equity typically structured in a PE-backed company?

Management equity in PE-backed companies is most commonly structured as sweet equity, meaning shares shares purchased at a nominal price that creates immediate economic value for the recipient. In the United States, the typical structure uses profits interests or restricted stock units. In the UK and Europe, share options at a nominal strike price are more common. Vesting is divided between time-based and performance-based components, with approximately 62% of PE-backed MIPs combining both criteria. The United States standard allocates roughly 50% of the grant to time-based vesting over four or five years and 50% to performance-based conditions. Performance targets may be linked to absolute financial metrics like EBITDA, to relative performance against the original investment case, or to investor return thresholds such as a minimum multiple on invested capital.

+

What is the difference between a good leaver and a bad leaver in a PE management equity plan?

In a PE-backed management equity plan, leaver provisions determine what happens to a management team member's equity when they depart before exit. Good leavers are typically those who die, become critically ill or incapacitated, retire at an appropriate age, or are deemed good leavers by the Board. Good leavers generally receive fair market value for their vested equity. Bad leavers are those who resign voluntarily for other reasons or are terminated for cause. Bad leavers are typically required to sell their vested equity at the lower of cost or market value, which in most scenarios means they receive approximately their original investment back and nothing for the equity appreciation. Unvested equity is typically forfeited entirely regardless of leaver category. In the UK, a third intermediate category is common; in the United States most agreements use only good and bad leavers, which concentrates the negotiating significance on how each category is defined.

+

What is a ratchet in a private equity management incentive plan?

A ratchet in a private equity MIP is a mechanism that increases the management team's percentage of the equity distribution when the GP's return on investment exceeds defined thresholds. Ratchets are designed to reward exceptional performance by giving management a larger share of the proceeds in high-return exit scenarios. There are two common types: an excess equity ratchet, which applies the incremental allocation only to equity value above the threshold that triggers it, and a total equity ratchet, which applies the incremental allocation to the total equity value once the threshold is reached. The total equity ratchet is more valuable to management but more costly to the GP. Ratchets are particularly significant in strong exit scenarios where the GP achieves a 2.5x or higher return on invested capital, and effectively irrelevant in scenarios where the GP's return falls below the minimum ratchet threshold.

+

How does dilution affect management equity in PE-backed companies?

Management teams entering a PE-backed equity arrangement should negotiate and clearly understand several key terms before signing. First, the exact definition of good and bad leaver, including which scenarios fall into the intermediate category and how constructive dismissal is defined. Second, the dilution provisions governing how future grants to new hires and add-on management teams affect the existing pool. Third, the specific performance conditions attached to the performance-based vesting component, including the measurement methodology, the time periods, and the consequences of missing a threshold by a small margin. Fourth, the ratchet thresholds and their precise calculation basis. Fifth, any drag-along and tag-along rights that govern what happens to management equity in scenarios where the GP exits through a transaction that management has not initiated or approved. Legal counsel familiar with PE equity structures is advisable before signing a shareholder agreement, even when the overall deal relationship is positive.

+

What should management teams negotiate in a PE equity plan before signing?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.