23 min read

—

Most LP teams do not read the LPA, the limited partnership agreement that governs every private equity fund they commit to.

That is not quite true.

They read it, or they send it to outside counsel, who reads it, and then they sign it. The practical question is whether anyone on the investment team has worked through the waterfall structure, stress-tested the clawback mechanics, or mapped the LPAC's approval rights against the fund's conflict-of-interest policy. In many allocations, especially at smaller family offices or first-time LP relationships, the honest answer is no.

This is expensive ignorance. A limited partnership agreement is not a formality to clear before wire transfer. It is the governing contract of the fund for its entire life, typically ten years, sometimes longer. Every economic right an LP has, every governance lever they can pull, every protection against GP misconduct: it is in the LPA, or it is not there at all. What is not in the LPA cannot be enforced.

The structural problem is timing. An LP typically receives the LPA late in the process, after a long period of due diligence, relationship-building, and investment committee preparation. By that point, declining the commitment carries a real cost, and the GP knows it. The review window is short, often ten business days or fewer for a first close, and the document itself runs 80 to 150 pages in most buyout fund structures. Some of those pages are genuinely important. Most are boilerplate.

Knowing which pages to prioritize is the skill.

The Institutional Limited Partners Association published its Model Limited Partnership Agreement specifically to address what had become two decades of gradual, clause-by-clause erosion of LP protections in market-standard agreements. The ILPA model provides a reference point. What the market actually produces looks quite different, fund by fund.

This guide covers the structure of a private equity LPA, which terms determine most of the economic and governance outcome, and how to review one efficiently, including where AI-assisted LPA analysis changes the workflow.

In this article:

What an LPA is and what it actually governs

The economic terms: management fee, carried interest, hurdle rate, and distribution waterfall

The governance terms: LPAC, key person provisions, and GP removal rights

LP protections: clawback mechanics, MFN clauses, and co-investment rights

How to prioritize a review: and where AI changes the workflow

AI for document processing

Review LPA terms without reading every clause

Get started today

What is a limited partnership agreement in private equity

The LPA is the founding document of a PE fund. It creates the fund's legal structure, sets out every party's rights and obligations, and governs the fund from its first close through to final dissolution, typically a decade or more after the initial capital call.

The two parties are the general partner and the limited partners. The general partner manages the fund, sources and executes investments, and makes all decisions within the scope of the LPA. Limited partners are passive investors, their role is to commit capital when called, receive distributions according to the waterfall, and exercise governance rights where the LPA grants them. LP liability is capped at their committed amount, which is the central benefit of the limited partnership structure for investors. The GP, as managing entity, carries the fund's operational and legal responsibility.

What the LPA actually governs is broader than most first-time LPs expect. Beyond fee structure and distribution mechanics, it covers: when and how capital can be called, what happens if an LP defaults on a capital call, the scope of the GP's investment mandate (asset classes, geographies, deal sizes, exclusions), how conflicts of interest must be handled, what disclosures the GP is obligated to make and on what schedule, which decisions require LP or LPAC consent, and under what conditions the fund can be wound up before its scheduled end date. An LPA signed in 2025 still governs an LP's rights in 2034.

Timing matters as much as content. The LP with the most bargaining power is the one considering a first-close commitment, they are helping the GP achieve a milestone that allows fundraising to continue and demonstrates institutional validation to other prospective LPs. Subsequent-close investors join a fund with existing momentum; the GP has less reason to move on terms. This is why critical review and negotiation work happens before first close, not after it.

The ILPA Model Limited Partnership Agreement, available from the Institutional Limited Partners Association and grounded in the ILPA Principles 3.0 framework published in 2019, provides the closest thing the industry has to a neutral reference standard. It exists in two versions, one built around a whole-of-fund (European) distribution waterfall, one around a deal-by-deal (American) structure. ILPA published the model to address a documented problem: by the 2010s, incremental GP-favorable changes had moved market-standard LPAs significantly away from LP-protective terms across multiple dimensions simultaneously. The ILPA model is not a regulatory floor. It is a benchmark that many institutional LPs now use as their opening position in term negotiations, one that carries more weight as AI tools in finance make it easier to systematically identify deviations from the standard.

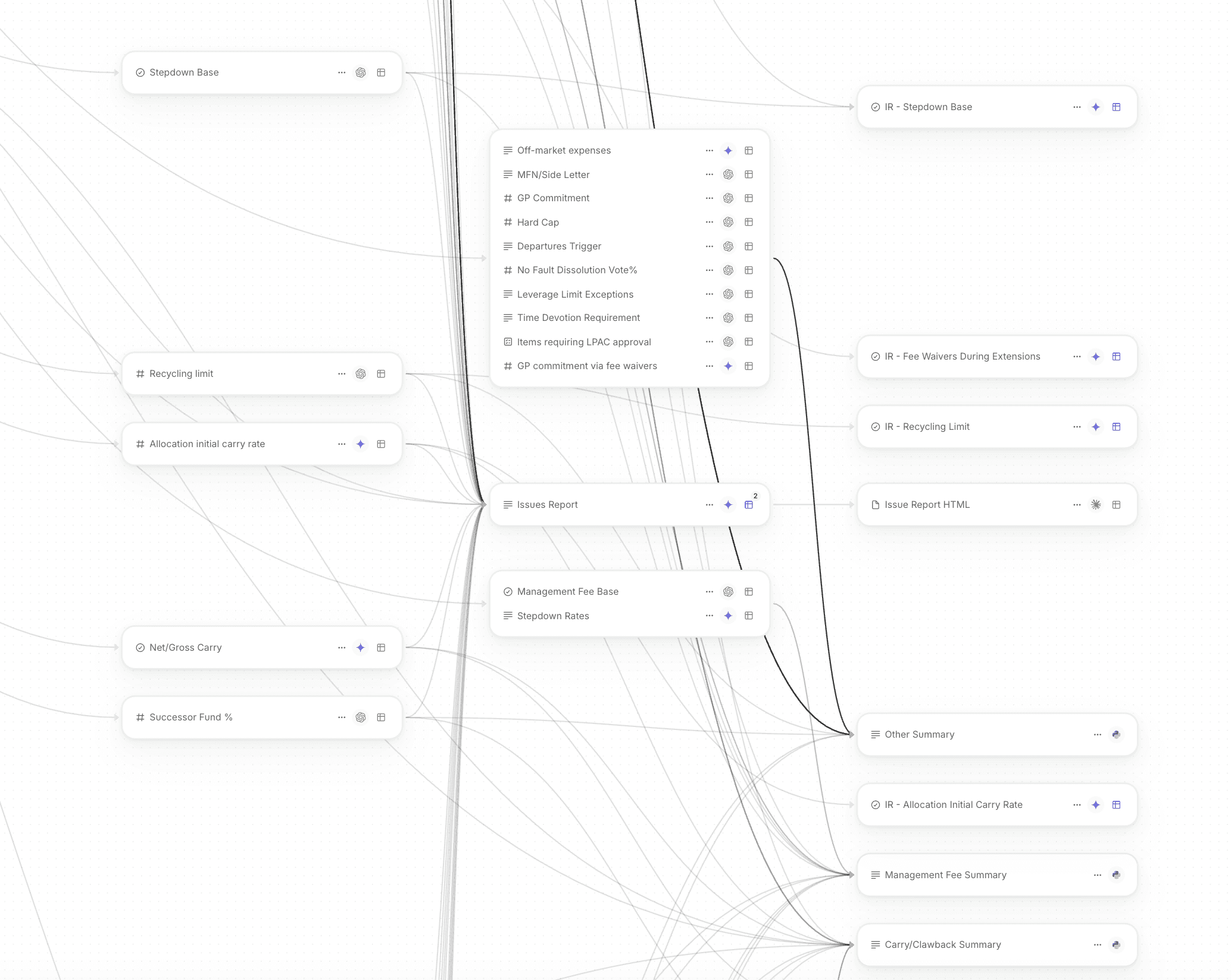

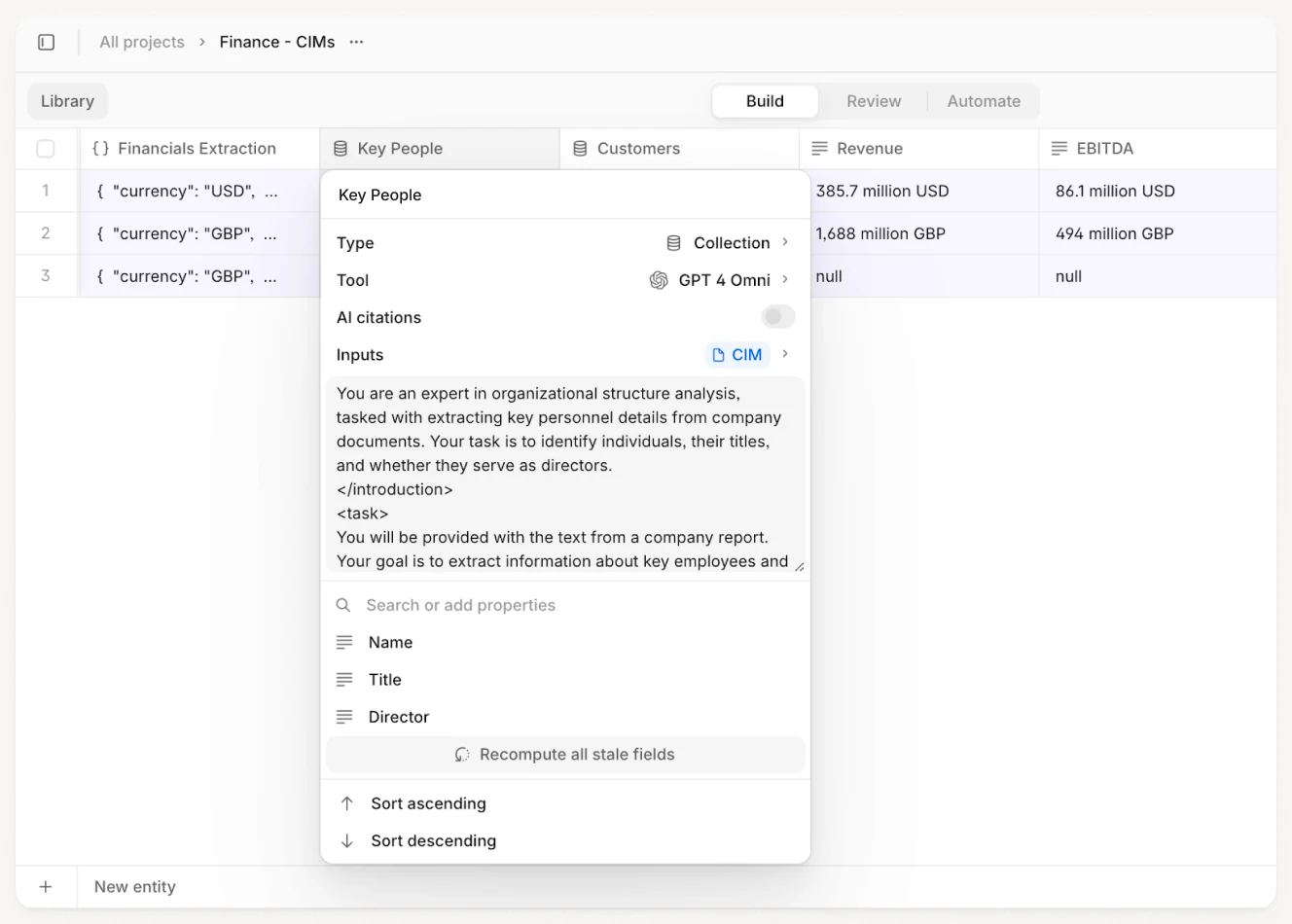

An example of a data extraction and LPA analysis workflow powered by V7 Go, using multiple nodes with Python, LLMs, and Excel parsing

LP teams that treat the LPA as a legal formality and route it straight to outside counsel without internal economic review are outsourcing the most important part of the analysis. Outside counsel can identify unusual provisions and flag legal risk. They cannot tell an allocations team whether the waterfall structure fits the fund's expected exit sequence, or whether the key person clause covers the specific individuals actually managing the portfolio. That judgment requires people who understand both the legal document and the fund, which is part of why AI-assisted due diligence programs treat LPA review as an internal function, not a delegation to outside counsel.

The economic terms: where LP returns are made or lost

Fee structure, carried interest, hurdle rate, and distribution waterfall are not equally important. The waterfall is where the most significant economic differences between LP-favorable and GP-favorable agreements are found. The management fee matters. The carry mechanics matter. But the waterfall structure, combined with the clawback provisions, is where large sums are won or lost across a fund's life, and where GP-drafted agreements most consistently favor the GP.

Management fee

The management fee funds the GP's operating costs during the fund's active period. Preqin's 2024 Private Capital Fund Terms Advisor confirms the market standard during the investment period is 1.5% to 2.0% of committed capital per year, with mean buyout fees trending toward the lower bound under sustained fundraising pressure. The fee steps down to 1.0% to 1.5% of invested capital, the capital actually deployed into portfolio companies, not the total commitment, once the investment period ends. The step-down matters because it reflects the actual work being done: a GP managing a portfolio of existing investments requires less resource than one actively deploying capital.

Three things to check. First, whether the step-down is automatic or requires LP action. Second, whether fees during any extension period are waived, reduced, or continued at full rate, the ILPA Model LPA specifies a full waiver during extensions; many GP-drafted LPAs default to continuation at the harvest-period rate, which means LPs pay fees on a fund that has stopped investing. Third, whether the management fee offset provision captures all fee income earned by the GP and its principals from portfolio companies, transaction fees, monitoring fees, director fees, break-up fees. The ILPA model requires a 100% offset: all such income reduces the management fee dollar-for-dollar. Market-standard LPAs often apply offsets at 80% and sometimes only to the GP entity rather than affiliated individuals, which allows a meaningful portion of portfolio company fee income to flow directly to carry recipients rather than offsetting LP costs.

Bad dilution refers to GP principals receiving management fee waivers that convert fee income into LP interests, diluting LP economics directly. The ILPA Model LPA explicitly prohibits it. Its absence from a fee offset provision is worth flagging.

Carried interest and hurdle rate

Carried interest is the GP's share of profits above the hurdle rate. Twenty percent carried interest with an 8% preferred return is close to universal in buyout funds. The meaningful variation lies in the catch-up provision and the net versus gross carry calculation.

The catch-up provision determines how quickly the GP reaches its 20% profit share after LPs have received their preferred return. The ILPA Model LPA specifies an 80% GP catch-up: after LPs receive their capital back plus 8% per year compounded annually, distributions shift to 80% GP and 20% LP until the GP has received an amount equal to 20% of cumulative profits. A 100% GP catch-up, where the GP receives all distributions after the hurdle until fully caught up, is more GP-favorable and appears regularly in fund LPAs. The difference is not trivial. On a $200M fund generating $400M in distributions, a 100% catch-up accelerates GP receipt significantly compared to the 80% model, reducing the period during which LP capital is compounding at the preferred return rate.

Net carry calculations deduct management fees and fund expenses from returns before calculating the carried interest base, meaning the GP's 20% is applied to LP-net returns. Gross carry applies the 20% to total returns before fees. The ILPA model specifies net carry. Gross carry provisions are a material economic difference for LPs in funds with above-average fee structures.

Ratchet waterfall structures appear in a minority of LPAs but are worth understanding. These step the GP's carry percentage upward as returns exceed defined thresholds, for example, 25% GP carry until cumulative returns exceed 200% of contributions, then a 50/50 split until a higher threshold is reached, then 30% GP carry on remaining profits. These structures require careful economic modeling because the LP's effective return depends heavily on the exit sequence and aggregate fund performance.

Distribution waterfall

The waterfall determines the order and proportion in which distributions flow to LPs and the GP as portfolio companies are realized. There are two fundamental architectures, and the economic difference between them is not academic, it is measurable in millions of dollars across a fund's life for a mid-market LP commitment.

A European (whole-of-fund) waterfall returns all LP capital and preferred return across the entire portfolio before the GP receives any carried interest. The GP does not see carry until every LP has been made whole on every investment, including the ones that underperformed. An American (deal-by-deal) waterfall allows the GP to receive carry on each realized investment individually, as soon as that specific investment generates a profit above the hurdle, the GP takes carry on it, regardless of what the rest of the portfolio has returned.

Blackstone Capital Partners V, whose LPA is publicly available, uses a deal-by-deal structure with two separate waterfalls: one governing distributions of current income and a separate one for disposition proceeds. Both allow per-investment carry receipt once the GP satisfies the hurdle on that specific investment. This was common practice for large buyout funds in the mid-2000s, before ILPA's model agreement drew clearer attention to the LP economics of deal-by-deal structures.

The LP risk in a deal-by-deal waterfall is carry acceleration. If the GP exits the fund's three strongest investments early, it receives carry on each. If the remaining portfolio then underperforms, the LP ends up having paid carry on profits that, at a whole-of-fund level, were partially offset by subsequent losses. Clawback provisions address this in principle. In practice, recovering already-distributed carry from individual carry recipients years after the fact is difficult.

For LPs who cannot move the GP off a deal-by-deal structure, the two key protective mechanisms are an escrow requirement, typically 20-25% of distributed carry held until final fund close, and a clawback with a short enforcement window, personal guarantee language, and clear recovery mechanics against individual carry recipients. Without these, the deal-by-deal waterfall is structurally advantageous to the GP.

An LPA review agent powered by V7 Go

The governance terms: who controls what when things go wrong

Governance provisions determine what LPs can actually do when a fund underperforms, a key investment professional leaves, or a GP acts against LP interests. These provisions are rarely exercised. Their value is mostly as a deterrent, a GP that knows its LP base can act has a different operating context than one that knows they cannot. GP-drafted LPAs minimize LP governance rights wherever the market allows.

Limited Partner Advisory Committee

The LPAC is a body composed of LP representatives, typically five to seven seats held by the largest investors by commitment size, that weighs in on conflicts of interest, related-party transactions, valuation disputes, fund extensions, and other matters where GP and LP interests diverge.

The critical structural question is whether the LPAC's involvement is binding or advisory. A GP-drafted LPA describes the LPAC as a body the GP "consults" or "keeps informed", which means the GP can proceed regardless of the LPAC's position. LP-favorable language requires LPAC approval for specified matters, creating a genuine blocking right. Under the ILPA Model LPA, LPAC approval is required, not merely sought, for GP-led secondary transactions, sales between GP-controlled vehicles, transactions between GP affiliates and the fund, and investments by GP personnel in companies within the fund's investment mandate.

LPAC members face a structural constraint worth understanding: they represent their own LP, not the broader LP base. The ILPA model includes a full fiduciary waiver for LPAC members, they can act solely in their own LP's interests, with no obligation to other LPs in the fund. LPs not represented on the LPAC cannot rely on LPAC members to protect their interests. The LPA itself is their only protection, which is why its specific terms matter more for non-LPAC LPs than for those with a seat at the table.

Items requiring LPAC approval are worth reviewing carefully. A list that includes only obvious conflict categories, sales between affiliated vehicles, GP-related party transactions, but excludes GP-led secondary transactions or fund restructurings leaves LPs without consent rights precisely when they are most needed.

Key person provisions

A key person clause names the specific individuals whose continued involvement is considered essential to the fund's investment strategy, typically two to four senior investment professionals. If a key person event occurs, the LPA specifies the consequence.

LP-favorable language automatically suspends the investment period upon a key person event, halting new investments until either the LPs vote to continue or the GP replaces the departed professional to LP satisfaction. GP-favorable alternatives require notification of the LP base and continue the investment period unless LPs organize a vote to suspend, which, in a large and geographically dispersed LP base, takes time and coordination the GP can use to continue deploying capital. Some GP-drafted LPAs specify cure periods of six to twelve months, during which the GP can continue investing while formally seeking a replacement. ILPA's model requires a key person event to trigger automatic suspension; cure is possible but the investment period stays suspended during the cure period.

Time devotion requirements are the complementary provision. The ILPA model requires key persons to devote substantially all of their business time to the fund and associated vehicles. Looser language, "a majority of professional time" or "the primary focus of their investment activities", creates flexibility for GP partners to spread their attention across multiple funds simultaneously, which is precisely the situation key person clauses exist to prevent.

GP removal and the no-fault divorce clause

For-cause removal requires demonstrating that the GP has committed fraud, gross negligence, or material breach, a high bar that typically requires court confirmation before the removal takes effect. It is meaningful as a remedy for genuine misconduct but is too slow and too costly to serve as a practical governance lever for performance disputes.

No-fault removal is the provision that actually functions as a deterrent. It allows LPs to remove the GP without proving misconduct, typically requiring a supermajority vote. The ILPA standard is 75% in interest. This is high by design, it prevents a minority of disgruntled LPs from disrupting a functioning fund, while preserving the ability of a clear LP majority to act without litigation. GP-drafted LPAs push this threshold to 80% or higher. In a typical diversified LP base where no single LP holds more than 10-15% of the fund, reaching 80% requires near-unanimous agreement, which is practically impossible to organize except in the most extreme circumstances.

No-fault removal clauses are almost never used. That is not an argument against them. The GP who knows three-quarters of their LP base can terminate the relationship without going to court behaves differently in fee negotiations, in managing conflicts of interest, and in how they communicate bad news than one who knows the threshold is unreachable.

LP protections: the clauses built to counter GP structural advantages

Several LPA provisions exist specifically to correct for asymmetries built into the GP-LP relationship. Clawback provisions, Most Favored Nation clauses, and meaningful co-investment rights did not appear in early limited partnership agreements, they were added over time as LPs organized and pushed back. Their absence from a contemporary fund LPA is a signal about how the GP views LP protection.

Clawback provisions

The clawback requires the GP to return carried interest it has already received if, at the end of the fund's life, the LP calculates that the GP was overpaid, that is, the LP did not actually receive the preferred return and return of capital it was entitled to. In a deal-by-deal waterfall, this is the primary check on carry acceleration.

Clawback provisions have two structural weaknesses. The first is timing. An end-of-fund clawback means the LP waits until dissolution, potentially year twelve, to recover carry overpaid in year four. Annual true-up provisions, which adjust carry distributions on a rolling basis, are more LP-favorable and appear in a minority of market LPAs. The second weakness is enforcement. Carry is distributed to individual investment professionals, not held in the GP entity. If those individuals have spent the distributions, relocated, or the GP has been wound down by the time the clawback is triggered, recovery requires pursuing individuals directly. This is legally possible and has been done, but it is slow, expensive, and uncertain.

The ILPA model addresses enforcement risk via optional escrow provisions: a portion of distributed carry, typically 20-25%, is held in escrow until final fund close. Some LPAs offer personal guarantee language as an alternative to escrow. Both are more protective than a simple obligation on the GP entity without enforcement mechanism.

Tax benefit clawback reductions are a separate but related provision. The ILPA model permits the GP to reduce the clawback amount by taxes paid on carried interest income. LP teams should review whether the mechanism is a dollar-for-dollar reduction or a proportional one, and whether it applies to taxes paid at the fund level, the individual recipient level, or both. Broad tax-benefit provisions can substantially reduce the clawback amount actually recoverable by the time it is triggered.

Most Favored Nation and side letters

Side letters are separate agreements between the GP and individual LPs granting terms not available in the main LPA, fee reductions, expanded reporting obligations, co-investment allocations, LPAC seats, regulatory accommodations, or withdrawal rights. They are common, particularly for large institutional LPs or anchor investors at first close who have the position to negotiate them.

They create a structural problem. Without an MFN clause, the LP base divides into two tiers: those with side letters who have privately negotiated better terms, and those governed by the LPA alone. LPs in the second tier cannot know what terms others received or whether the GP is selectively favoring certain investors.

A Most Favored Nation clause requires the GP to notify all LPs of any more favorable economic terms granted to another LP via side letter, and to offer those same terms to any LP who requests them. The practical protection depends on the carve-outs. Many LPA MFN provisions exclude regulatory accommodations (provisions tailored to specific LP legal structures like ERISA requirements or tax-exempt status), terms specific to fund-of-funds investors, and anchor investor benefits tied to first-close commitment size. If the carve-outs are broad enough, the MFN covers only the provisions where GP flexibility was already limited.

LPs reviewing the MFN clause should check: what the carve-outs specifically exclude, whether the notification obligation is proactive (GP must notify) or reactive (LP must ask), and whether the MFN covers the full investment period or only the initial closing period.

Co-investment rights

Co-investment allows LPs to invest directly alongside the fund in individual portfolio companies, typically without management fees or carried interest. The economics are materially better than fund-level exposure to the same underlying investment, which is why co-investment is a valued LP benefit and why the specific drafting of the co-investment right determines whether it is actually useful.

A "right to co-invest subject to GP sole discretion" is not a co-investment right. It is a statement that the GP will think about it. LP-favorable language specifies a notice period (the GP must notify the LP of a co-investment opportunity within a set number of days), a minimum allocation as a percentage of the LP's fund commitment, and whether the right is exclusive or shared across multiple LPs on a pro-rata basis. Without these mechanics, the GP retains full control over allocation, and attractive opportunities flow to the LPs whose relationships the GP is most interested in cultivating.

V7 Go extracts structured LP governance rights from fund agreements, including LPAC approval items, key person triggers, and no-fault removal thresholds.

How to review a limited partnership agreement in private equity

A 130-page LPA has roughly 20 pages that determine most of the economic and governance outcome. The skill is knowing which twenty.

The sequence that works in practice: economics first, governance second, LP-specific protections third, boilerplate last. Within economics, prioritize the distribution waterfall and carry mechanics before management fee, the waterfall has more total economic impact over the life of the fund. Within governance, prioritize the LPAC structure and key person provisions over removal mechanics, both are live issues; removal is the remedy of last resort.

The ILPA Model LPA is publicly available and provides a clause-by-clause reference. The most efficient review technique is to redline the actual fund LPA against the ILPA model as a starting point. Any provision that deviates from the ILPA baseline is a candidate for negotiation. This turns a document review from reading 130 pages cold into a gap analysis, a more tractable problem.

First-close position matters. LPs committing at or near first close help a GP hit a fundraising milestone, demonstrating institutional validation and sustaining fundraising momentum. The GP has more reason to move on terms at first close than at any subsequent close. LPs who have decided they want the allocation should still use their first-close position to negotiate, particularly on the waterfall structure, management fee offset mechanics, and LPAC composition. The deal does not need to be declined to extract better terms; it needs to be held until the GP decides the cost of accommodation is lower than the cost of losing the commitment.

Red flags worth escalating immediately: a deal-by-deal waterfall with no escrow requirement, an advisory-only LPAC with no binding approval rights on any matter, no step-down in management fees after the investment period, clawback provisions with broad tax-benefit carve-outs and no escrow mechanism, and key person clauses that only require notification rather than automatic investment period suspension.

The challenge for active allocators is volume. An LP running a $1-2B program may review four or five new LPAs per year alongside annual reporting obligations, DDQ responses for existing managers, and ongoing portfolio monitoring. A thorough LPA review by experienced in-house counsel or outside advisors takes 20 to 40 hours per document. Stretched teams often over-invest in reviewing provisions that will not move and under-invest in the economic mechanics that determine actual returns.

This is the workflow the V7 Go LPA Analysis Agent addresses. It ingests the complete LPA, 80 to 150 pages, and extracts 67 distinct fields covering every major economic and governance term: management fee and step-down rates, fee offset mechanics and whether bad dilution is present, carried interest terms, catch-up rate (net vs. gross), waterfall type, waterfall tiers with their LP/GP percentage splits and LPA section citations, clawback structure and escrow provisions, GP commitment percentage, leverage limits, investment period length, key person definitions and departure triggers, no-fault dissolution threshold, LPAC composition and approval items, MFN provisions, and side letter terms.

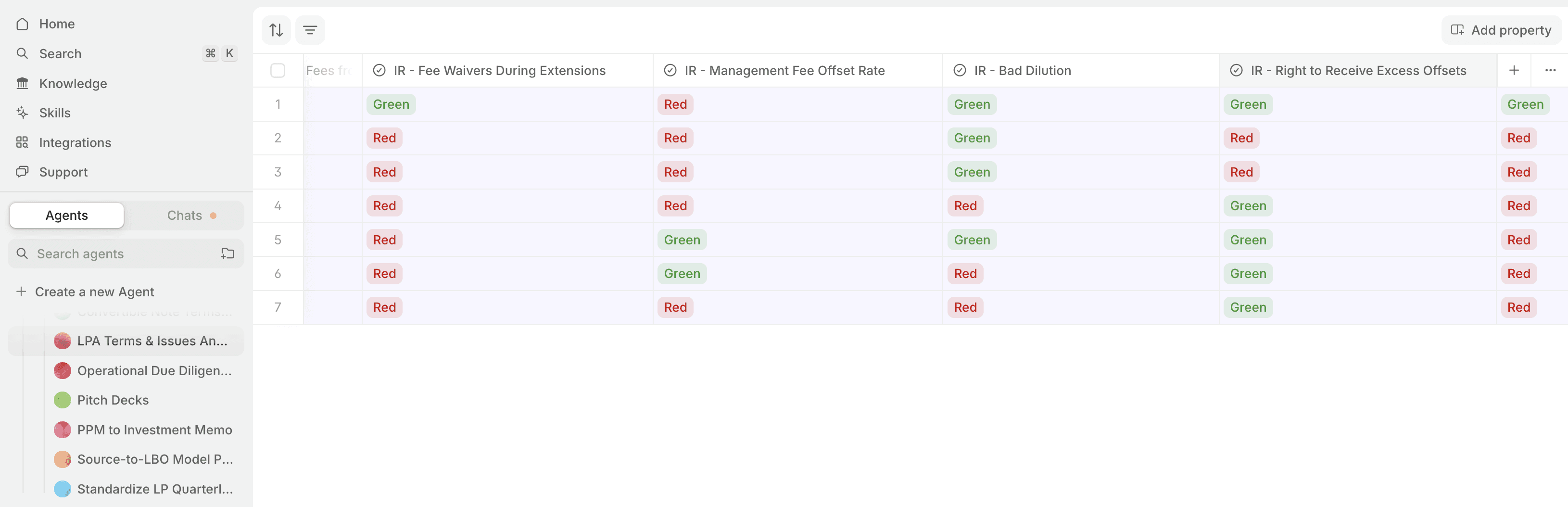

V7 Go LPA Terms and Issues Analyzer output table showing traffic-light status flags for fee provisions across seven private equity fund agreements

The output is two documents. First, a structured spreadsheet with every extracted field and its value from the actual LPA text. Second, an issues report, a traffic-light analysis that compares the fund's terms against acceptable LP ranges and generates specific negotiation notes against each flagged item. A field marked red means the term falls outside market standard and warrants a counter-proposal. Green means the provision is within the acceptable range. The notes are specific: not just "management fee is too high" but "propose a management fee of 1.5% on committed capital during the investment period, stepping down to invested capital after, with a 100% offset against portfolio company fee income."

When a market-standard buyout fund LPA is run through the same analysis, the issues report flags the absence of a successor fund step-down provision (the management fee does not step down when the GP raises a successor fund and LP capital is effectively stranded in the predecessor) along with the absence of a lookback provision and no-waiver language for management fees during fund extensions. These are matters of public record for a vintage fund, and they reflect where market standard sat before ILPA's model agreement gave the sector a clearer LP-protective reference point.

The agent does not replace legal review. Negotiation judgment, relationship context, and legal sign-off require people with direct knowledge of the situation. What it replaces is the extraction and benchmarking work, the part that takes 15 to 20 hours and produces a picture that legal counsel can then argue from. An allocations team that spends three weeks on LPA review typically spends the first week building that picture. The agent builds it in minutes.

The same process applies when reviewing the full range of fund documents beyond the LPA itself, subscription agreements, side letters, DDQ responses, and annual reports all sit within the same document intelligence workflow. The AI Due Diligence Agent extends the same structured extraction approach to fund-level due diligence packages, and for the PE workflow from fund selection through CIM review to transaction closing, each stage involves document-heavy analysis that follows the same basic pattern: extract, benchmark, flag, review.

The LPA Terms and Issues Analyzer output from V7 Go: 67 extracted fields per fund, with an issues report comparing each term against acceptable LP ranges.

The LP agreements signed today govern distributions, governance rights, and dispute resolution for the next decade. Funds raise successor vehicles, acquire new portfolio companies, and run into situations their GPs did not plan for, continuation vehicles, NAV loans, GP-led secondaries, portfolio restructurings. Each of these creates new conflict points between GP and LP interests. Each of them is governed by the existing LPA's provisions, however those were drafted. The teams with better-negotiated agreements have more tools when these situations arise.

The ones without them do not.

To see how the V7 Go LPA Analysis Agent reviews a fund agreement and produces the issues report, the agent page includes worked examples of the extraction output and the negotiation note format.

LP teams that negotiate the best fund terms do not do it by spending more time on documents. They do it by having a clear position on each material provision before the review window closes, and by applying that discipline at every fund they seriously consider, not just the largest commitments.

The V7 Go LPA Analysis Agent makes systematic review achievable at program scale. The structured field extraction and issues report is the starting document for legal review and LP discussion, not the end of the process. The deal gets better terms when the review starts from a complete picture.

What is an LPA in private equity and what does it govern?

An LPA (limited partnership agreement) is the founding legal document of a private equity fund. It establishes the fund's legal structure, defines the rights and obligations of the general partner and limited partners, and governs every aspect of the fund's life from first close through final dissolution, typically ten to twelve years. The LPA covers: when and how the GP can call capital, the investment mandate (asset classes, geography, deal size limits), fee structure and distribution mechanics, governance rights including the LPAC composition and approval items, key person definitions and departure consequences, GP removal rights, reporting obligations, and end-of-fund wind-down procedures. Every economic right an LP has, including the right to receive preferred return before the GP takes carry, exists because it is written into the LPA. Rights not documented in the LPA cannot be enforced regardless of side conversations or informal GP commitments. For LP teams, this means the LPA review is not an administrative step before commitment, it is the primary document that determines what an LP can and cannot do for the life of the fund.

+

What is the difference between a European and American distribution waterfall in a private equity LPA?

The distribution waterfall defines the order in which realized proceeds from fund investments are distributed to LPs and the general partner. A European (whole-of-fund) waterfall returns all LP capital and preferred return across the entire fund portfolio before the GP receives any carried interest. The GP does not receive carry until every LP has been made whole on all investments, including underperforming ones. An American (deal-by-deal) waterfall allows the GP to receive carry on each individual investment as it is realized, as long as that specific deal exceeds the hurdle rate, the GP takes its carry share, regardless of overall fund performance. The practical difference is carry acceleration risk. In a deal-by-deal structure, if the GP exits the fund's three strongest investments early, it receives substantial carry. If the remaining portfolio then underperforms, the LP has paid carry on profits that were partially offset by subsequent losses. The clawback provision is the primary protection in this scenario, but recovery of already-distributed carry from individual recipients is legally possible and practically difficult. The ILPA Model LPA uses a whole-of-fund waterfall as its recommended structure for LP-protective fund terms.

+

Which LPA provisions are typically negotiable, and how much leverage does an LP have?

Negotiability depends almost entirely on timing and commitment size. An LP considering a first-close commitment has meaningful bargaining power, they are helping the GP hit a fundraising milestone, and the GP has reason to accommodate reasonable requests rather than lose the commitment. By subsequent closes, the GP has fundraising momentum and less reason to move on terms. Provisions that institutional LPs regularly negotiate: management fee step-down mechanics (automatic vs. discretionary, extension period treatment), the fee offset percentage (ILPA standard is 100% offset; many GPs start at 80%), distribution waterfall structure (European vs. American), carry catch-up rate (80% ILPA standard vs. 100% GP-drafted), no-fault removal threshold (75% ILPA standard; GPs push to 80% or higher), LPAC approval rights (binding vs. advisory), and clawback escrow requirements. Provisions that rarely move: the management fee percentage itself (1.5-2.0% is near-universal), carried interest percentage (20% is market standard), and the preferred return rate (8% compounded annually). LP teams with the strongest negotiating positions are those who have done the economic analysis before first close and know exactly which provisions they need the GP to move on, rather than redlining the entire document.

+

How does AI review a limited partnership agreement, and how accurate is the extraction?

AI-powered LPA review works by ingesting the full fund document, 80 to 150 pages of legal text, and applying a structured extraction workflow to identify and populate defined fields. Rather than summarizing the document, the agent extracts specific values: the exact management fee percentage and step-down mechanics, the fee offset rate, carried interest terms, catch-up rate, waterfall type, waterfall tier structure with LP/GP percentage splits at each tier, clawback provisions, GP commitment percentage, key person names and departure triggers, LPAC composition and the specific items requiring LPAC approval, no-fault dissolution threshold, and MFN clause scope. Each extracted value is accompanied by a citation linking back to the specific page and clause in the source document. The V7 Go LPA Analysis Agent extracts 67 distinct fields per agreement and generates an issues report comparing each field against acceptable LP ranges, with specific negotiation notes against flagged items. Accuracy depends on document quality and structure. Digitally-native PDFs with clear clause headers extract with high precision. Scanned documents or agreements with non-standard structures may require human review of flagged extractions. The agent is designed as a starting document for legal review, not a replacement for it, the value is in eliminating the 15 to 20 hours of extraction and benchmarking work so legal review can focus on judgment rather than data collection.

+

What is the ILPA Model LPA and how should LP teams use it in fund negotiations?

A thorough LPA review by experienced in-house counsel or outside advisors typically takes 20 to 40 hours per document for a standard buyout fund LPA. The range reflects document complexity: a 90-page LPA with straightforward mechanics takes less time than a 150-page fund-of-funds structure with multiple side letter references and complex co-investment arrangements. The standard review process involves: initial read for structure and material provisions, economic modeling of the waterfall and carry mechanics against fund return scenarios, comparison against ILPA model or prior fund LPAs from the same GP, identification of provisions requiring negotiation, outside counsel review for unusual legal structures or jurisdiction-specific provisions, and LP committee presentation for material flags. For active allocators managing multiple new investments alongside ongoing portfolio obligations, the extraction and benchmarking phase, building the picture of what the LPA actually says on every material provision, often takes the majority of the review time. AI-assisted extraction addresses specifically this phase: the V7 Go LPA Analysis Agent builds the structured 67-field extraction and issues report in minutes rather than days, allowing the review team to begin the judgment-intensive work, negotiation strategy, legal risk assessment, relationship considerations, without waiting for the initial data gathering to complete.

+

How long does a proper LPA review take, and what does the process involve?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.