15 min read

—

A practical guide to LP reporting templates, software evaluation, and AI-powered automation for private equity IR teams.

LP reporting is the process by which fund managers (GPs) disclose financial performance, portfolio company updates, and capital activity to their investors (LPs) on a regular — typically quarterly — basis. A complete LP report includes fund-level financial statements, NAV calculations, IRR and TVPI metrics, individual portfolio company updates, capital account statements, and management commentary.

For most private equity firms, the quarterly LP report is the most time-intensive deliverable the IR team produces. Pulling data from portfolio monitoring systems, fund administrators, and custody platforms, validating figures against the general ledger, formatting reports to LP specifications, and shepherding drafts through compliance review can consume four to six weeks of senior staff time each quarter.

The stakes are high. A poorly formatted or delayed LP report signals operational immaturity. Sophisticated institutional LPs, including pension funds, endowments, and sovereign wealth funds, compare the quality of your reporting against every other manager in their portfolio. Weak reporting does not just irritate; it raises diligence flags at re-up time.

This guide covers everything you need to build a reporting process that satisfies today's LP expectations, including the role AI is starting to play in investor reporting and what a modern LP quarterly reporting workflow actually looks like at scale.

What LP reporting is and what goes into a complete quarterly report

The January 2025 ILPA reporting template: what changed and how to comply

How to evaluate LP reporting software and which platforms lead the market

How AI is compressing 6-week reporting cycles to under 8 days

A step-by-step LP reporting workflow you can implement immediately

AI for document processing

Automate LP report generation from your documents

Get started today

What is LP reporting?

LP reporting refers to the formal communications a general partner (GP) sends to limited partners (LPs) documenting the financial state of the fund and the progress of portfolio companies. The core deliverable is a quarterly update, though most LPs also expect an annual audited financial report and ad hoc communications on material events such as realizations, defaults, or capital calls.

At its simplest, an LP report answers three questions: How is the fund performing? What is happening inside the portfolio? Where does capital stand? A complete quarterly report typically includes:

Fund-level financial statements: Income statement, balance sheet, and statement of changes in partners' capital prepared under GAAP or IFRS.

NAV calculation and roll-forward: Fair value of all investments reconciled from the prior period, showing contributions, distributions, unrealized and realized gains.

Performance metrics: Net IRR, TVPI, DPI, and MOIC at both the fund and individual investment level, often compared against the relevant benchmark.

Portfolio company updates: Operational highlights, trailing twelve months revenue and EBITDA, key KPIs, and qualitative commentary for each portfolio company.

Capital account statements: Each LP's individual account showing contributions, distributions, management fees, carried interest, and NAV attributable to their interest.

Management commentary: Market context, deal pipeline, deployment pace, and forward-looking remarks from the investment team.

The production process is where most firms lose weeks. Finance teams export raw data from fund administration platforms, portfolio monitoring software, and accounting systems, then reconcile figures manually in Excel before passing drafts to legal and compliance for review. For a fund with 15 to 30 portfolio companies and 40 or more LPs, each with slightly different reporting preferences, that reconciliation work accumulates fast. A single mismatched figure between the fund administrator's NAV statement and the GP's internal model can trigger days of back-and-forth before the discrepancy is resolved and drafts can move forward.

Fund-level portfolio monitoring dashboards provide the raw inputs for LP reporting, but translating that data into formatted LP deliverables still requires substantial manual work at most firms.

LP reporting templates: The ILPA standard

The Institutional Limited Partners Association (ILPA) has published standardized reporting templates since 2011, and they have become the closest thing private equity has to a mandatory reporting format. Institutional LPs, particularly public pension funds and endowments, now require ILPA-compliant reporting as a condition of investment. For GPs raising institutional capital, the ILPA template is effectively non-negotiable.

In January 2025, ILPA released a significant update to both its Reporting Template and a new companion Performance Template. The central change to the Reporting Template addresses a longstanding friction point: the previous two-tier disclosure structure gave GPs the flexibility to report at either a higher or lower level of granularity depending on their LP base. The 2025 update removes that optionality, requiring a single uniform level of detail across all line items, with no reordering or repurposing permitted.

The January 2025 ILPA release also introduced a standalone Performance Template, separate from the Reporting Template, designed to standardize how performance metrics are calculated and disclosed.

The adoption timeline for planning purposes:

Q1 2026: Expected adoption for investment-period funds and all new funds launched from January 2026.

Q1 2026: Performance Template data capture begins for the quarter ending March 31, 2026.

Q1 2027: First Performance Template delivery deadline, for the quarter ending March 31, 2027.

The ILPA Reporting Template also standardizes how GPs report management fees and fund expenses. For a detailed breakdown of what the 2025 changes mean for GP compliance programs, see what the new ILPA reporting templates mean for GPs in 2026. ILPA accepts two methodologies:

Granular Methodology: Each expense line item is disclosed separately with no netting or aggregation, giving LPs full transparency on how fees and costs are charged to the fund.

Gross Up Methodology: Fees and expenses are reported at a higher level, with the gross management fee shown before offsets, enabling cross-manager comparison without line-item granularity.

Most institutional LPs prefer the Granular Methodology. Emerging managers who have historically used the Gross Up approach face increasing pressure to migrate, particularly from pension fund LPs with strong governance mandates. The practical implication: decide which methodology to standardize on across the full LP base before the Q1 2026 deadline, rather than maintaining bespoke versions for different investors. The compliance and reconciliation cost of running both methodologies simultaneously is higher than the one-time cost of migration.

What LPs actually want to see

Beyond the ILPA template structure, LP expectations around performance disclosure have shifted. The post-2022 vintage years tested many funds' return assumptions, and LPs have become more rigorous about how GPs calculate and present metrics.

IRR deserves particular attention. GPs have historically used subscription credit lines, short-term capital call facilities, to boost reported IRR by delaying LP capital calls. The practice inflates the headline number without changing actual investment performance. Sophisticated LPs now ask for IRR stated with and without subscription line credit, alongside TVPI, DPI, and MOIC, to get a complete picture. For a detailed look at how GPs report IRR and how LP scrutiny is evolving, see how GPs report IRR and why LPs are starting to distrust the number.

Institutional LPs also now expect:

ESG reporting: Greenhouse gas emissions data, workforce diversity metrics at the portfolio company level, and governance disclosures aligned with TCFD or UNPRI frameworks.

Private capital account statements (PCAP): Detailed transaction-level statements showing exactly how each LP's capital has been contributed, invested, and distributed, formatted for direct import into LP accounting systems.

Consistent valuation methodology: ASC 820 Level 3 fair value disclosures showing the key inputs and assumptions behind every unrealized mark, with sensitivity analysis where valuations are material.

Benchmark comparison: Performance measured against a relevant public market equivalent (PME), most commonly the S&P 500 or Cambridge Associates private equity index.

Transforming raw financial tables from portfolio company packages into structured LP report data is one of the highest-friction steps in the quarterly cycle and the first area where AI is delivering measurable time savings.

LP reporting software: What to look for

The market for LP reporting software has consolidated around a handful of platforms serving different segments of the private equity market. Before evaluating vendors, define your requirements against these seven criteria:

Data consolidation and source integration: Can the platform pull data directly from your fund administration system, portfolio monitoring tool, and general ledger without manual export and re-entry? Native integrations with Yardi, Geneva, and Investran reduce reconciliation risk and eliminate the data hand-off steps where most errors enter LP reports.

Template flexibility and ILPA compliance: Does the platform support the updated 2025 ILPA Reporting Template out of the box? Can you customize templates for individual LP preferences while maintaining a single canonical data source? The ability to generate LP-specific variants from one master dataset is the difference between scalable reporting and a per-LP manual process.

Workflow automation and approval routing: Does the platform automate data validation, flag discrepancies, and route draft reports through a structured approval workflow? Platforms with built-in workflow engines reduce the risk of errors reaching LP inboxes and provide an audit trail for compliance review.

LP portal and self-service access: Does the platform provide a secure LP-facing portal where investors can log in and access documents, capital account statements, and performance data on demand? LPs increasingly expect self-service access; document delivery by email attachment is becoming a reputational signal in itself.

Audit trail and version control: Does the platform maintain a complete log of every data change, report revision, and LP communication? Version control is essential for internal accountability and for responding to regulatory examination or LP data queries.

Security and compliance certifications: Is the platform SOC 2 Type II certified? Does it support role-based access control, multi-factor authentication, and data residency requirements for LPs in different jurisdictions? Institutional LPs conduct operational due diligence on GP technology stacks before committing capital.

Multi-strategy scalability: Can the platform handle multiple fund strategies (buyout, growth, credit, real assets) within a single instance, with strategy-specific templates and reporting hierarchies? Firms running parallel strategies need a platform that does not require separate instances for each fund type.

Leading platforms serve different segments of the market:

Chronograph: Purpose-built for private equity portfolio monitoring and LP reporting, with strong ILPA template support, a clean LP portal, and integrations with major fund administration platforms. Best suited for mid-market and upper-market buyout funds managing 15 to 50 or more portfolio companies.

Allvue Systems: Broad platform covering portfolio management, fund accounting, and LP reporting in a single system. Strong for credit and private debt strategies alongside buyout. Well suited for multi-strategy firms wanting one platform across the fund lifecycle.

Dynamo Software: CRM and reporting platform with a strong LP relationship management layer. Best for funds where LP communication management is as important as financial reporting, particularly those with heavy co-investment programs or family office LP bases.

Fundwave: Cloud-native platform aimed at emerging managers who need ILPA-compliant reporting without enterprise implementation timelines or pricing. Lower friction and cost structure, targeted at sub-$500M fund managers building their first formal reporting infrastructure.

iLEVEL (ION): Portfolio monitoring-first platform with reporting capabilities. Well established, with deep integrations into fund administration ecosystems. More commonly used for portfolio company data aggregation than for LP-facing report generation, but relevant for firms already running iLEVEL for monitoring.

Cobalt LP: A platform for the LP side of the table rather than the GP side. LPs use Cobalt to track their GP relationships and portfolios. Worth understanding because LPs using Cobalt have specific data format preferences that GPs should accommodate in their reporting output, particularly around capital account statement structure and performance data formatting.

How AI is transforming LP reporting

The central constraint in LP reporting is not data quality. Most private equity firms have adequate data by the time quarterly reporting begins. The constraint is manual effort: moving data from source systems into formatted LP deliverables, validating it for internal consistency, generating narrative commentary, and routing drafts through review cycles. At a typical mid-market fund with 20 portfolio companies and 30 or more LPs, this process consumes 500 to 800 hours of senior staff time per quarter.

AI is compressing that timeline by automating five discrete steps in the reporting workflow:

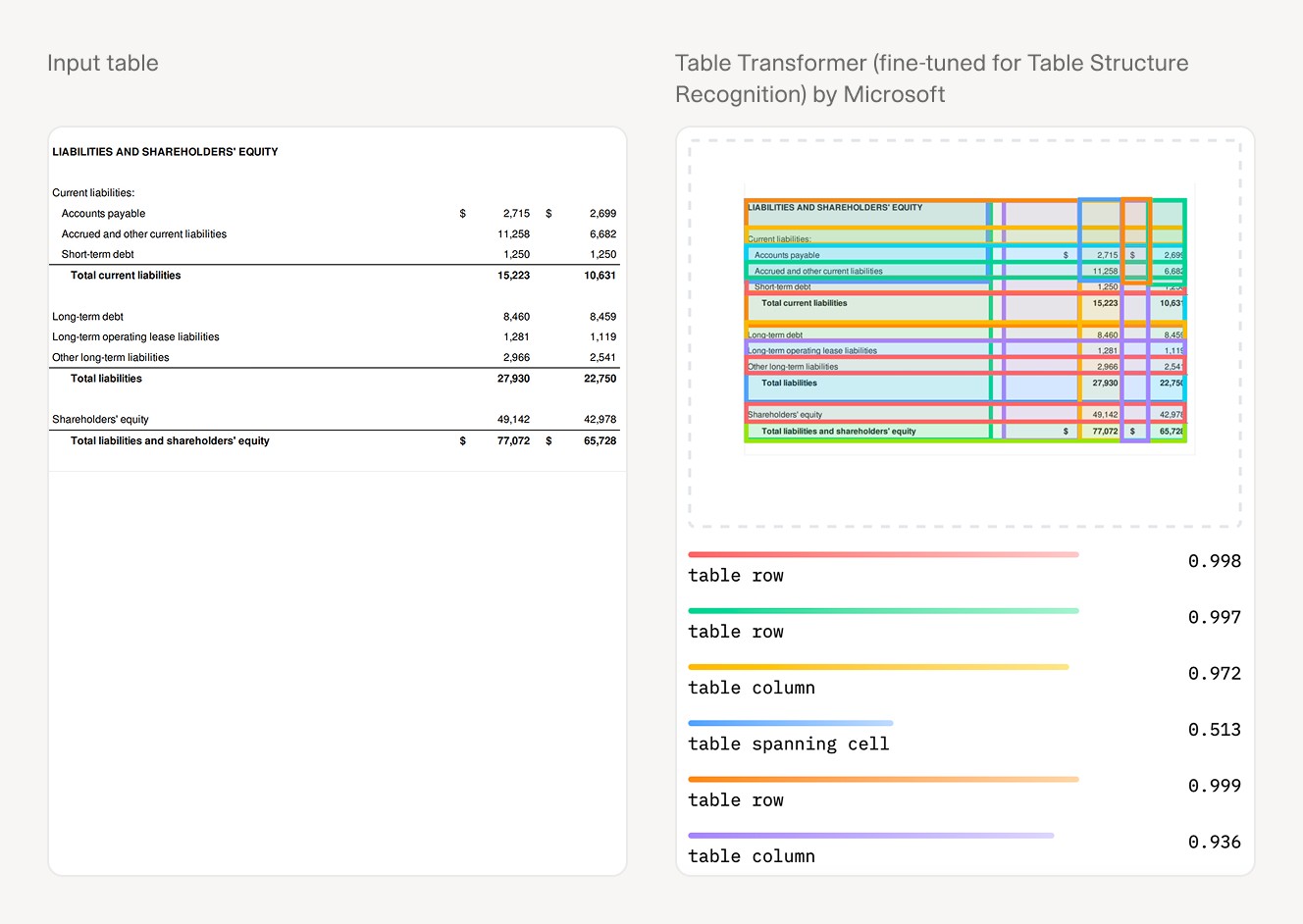

Document ingestion and data extraction: AI models trained on financial document structures can ingest portfolio company financial packages, board decks, and management accounts, extract structured financial data (revenue, EBITDA, net debt, cash), and load it into reporting templates without manual data entry. Computer vision handles tables and formatted PDFs that traditional OCR fails on.

Cross-source validation: AI can reconcile figures across fund administration reports, portfolio monitoring data, and GP accounting entries, flagging discrepancies for human review rather than passing errors downstream to LP-facing reports. Automated validation shifts the human review from finding errors to resolving them.

Narrative generation: AI can draft management commentary, portfolio company updates, and market context sections from structured data inputs, which the investment team then edits rather than writes from scratch. This converts the commentary step from a blank-page writing exercise to an editing exercise, compressing what typically takes two to three days to half a day.

LP customization at scale: AI can generate LP-specific variants of a master report, applying each investor's preferred format, currency, language, or performance attribution method without requiring separate manual formatting per investor. A firm with 40 LPs no longer needs 40 separate formatting passes.

Compliance review: AI can scan draft reports for missing disclosures, ILPA template compliance gaps, and regulatory filing requirements before reports go to the compliance team, reducing the review cycle from days to hours by catching structured issues before human review begins.

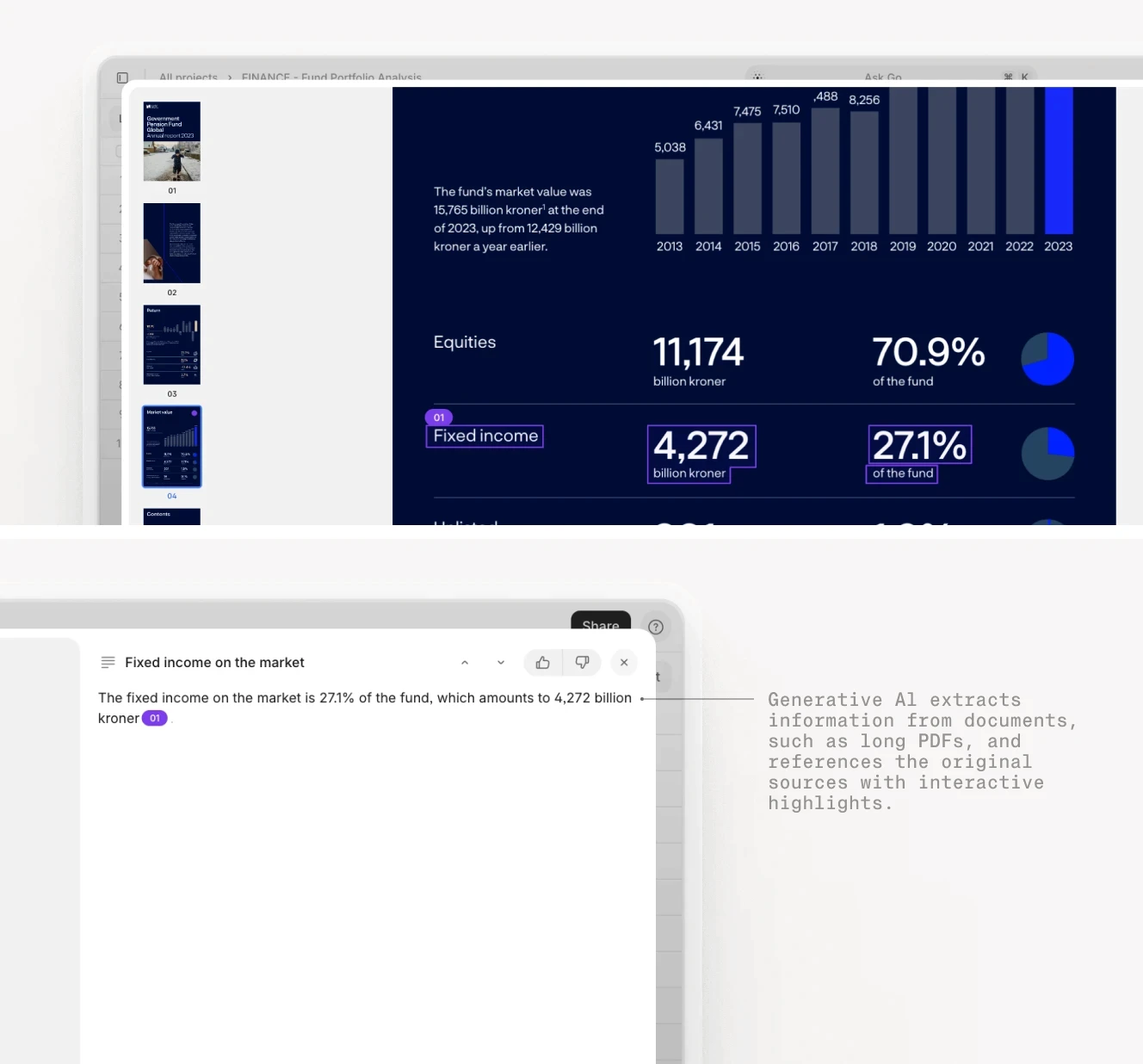

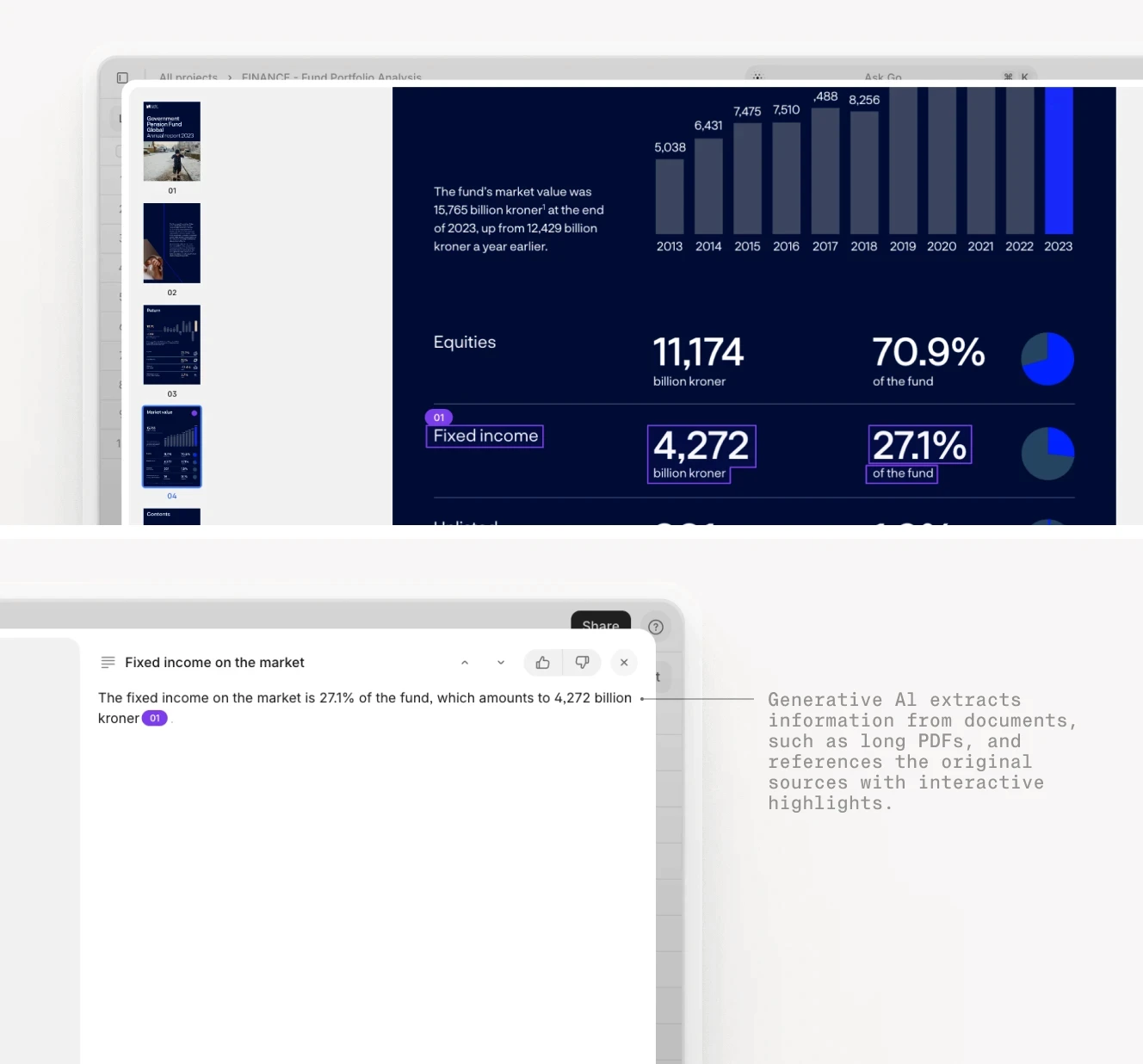

The workflow impact at scale is material. Here is what that looks like in practice: a private equity firm managing 45 LP relationships across 18 portfolio companies restructured its quarterly reporting process using V7 Go agent-based automation. The prior process required six weeks from period close to LP delivery. The AI-augmented process reduced that to 8 days, with the largest gains from automated extraction of portfolio company financial packages and AI-assisted narrative drafting. That team now focuses on LP relationship management instead of report production. The V7 Go finance walkthrough covers why chat-based AI falls short for finance workflows like this one, with DDQ and CIM accuracy benchmarks behind the difference.

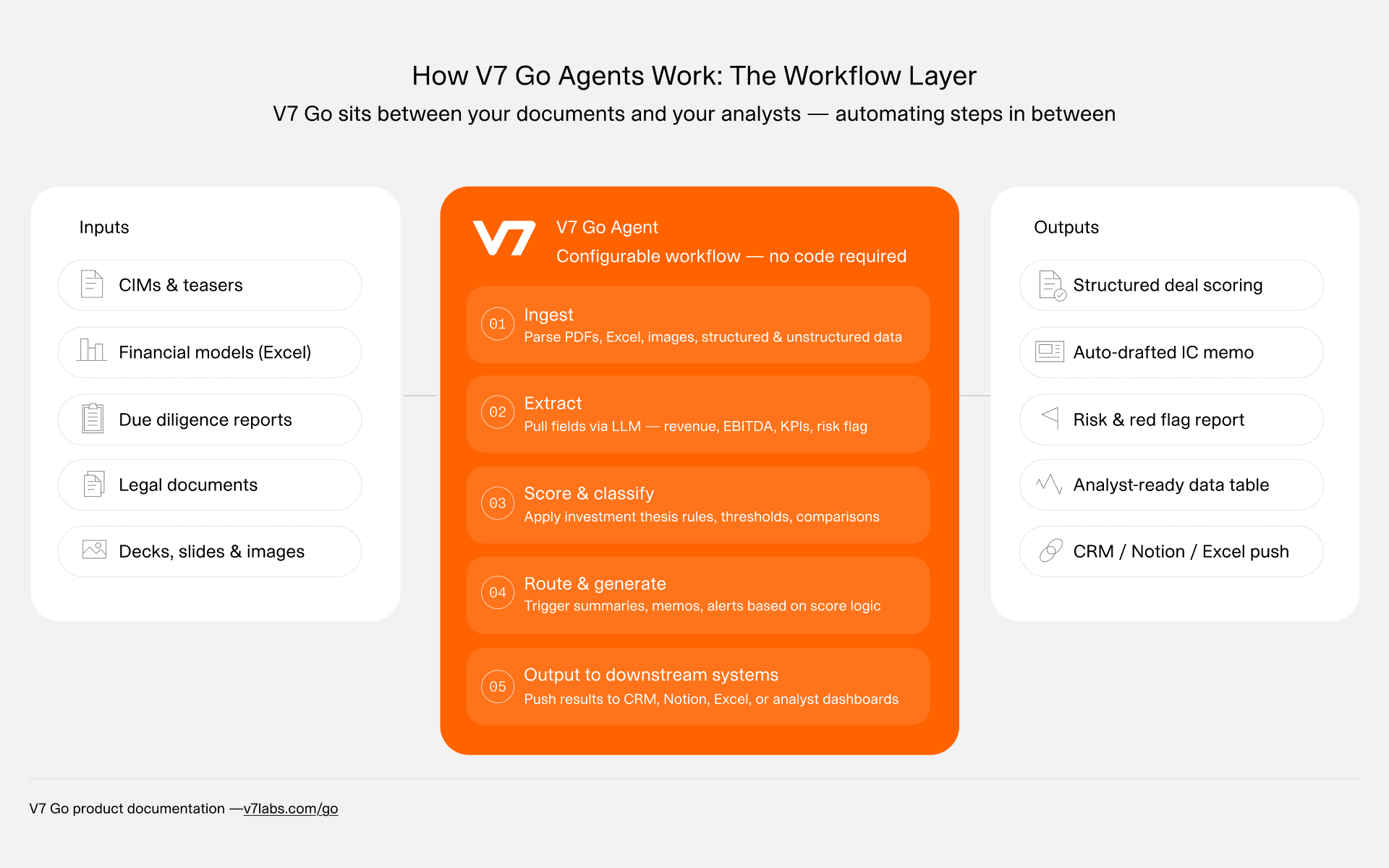

V7 Go agents ingest unstructured inputs from portfolio companies, extract structured financial data, validate and classify it, and route outputs into LP reporting workflows, with each step auditable and traceable to source documents.

Security and data privacy

LP reporting data sits among the most sensitive information a PE firm handles: portfolio company financials, fund-level performance figures, and individual LP capital account details are all material non-public information. Any AI system involved in LP reporting must meet institutional-grade security requirements before workflow design begins.

The minimum requirements for a production LP reporting workflow:

SOC 2 Type II certification for the AI platform

Zero-retention processing architecture: data used for inference is not stored or used to train models

Role-based access control ensuring analysts see only the portfolio companies and LPs relevant to their work

Multi-factor authentication on all accounts

Data residency controls for LPs in jurisdictions with strict localization requirements, including Germany, Japan, and Saudi Arabia

V7 Go operates on a zero-retention architecture and maintains SOC 2 Type II certification. For firms evaluating private equity fund report automation, assess security architecture before workflow design, not after. For the broader context of where LP reporting fits into the portfolio monitoring picture, see portfolio monitoring in private equity.

Building an LP reporting workflow that scales

A repeatable LP reporting workflow is a process architecture, not a task list. The difference is that a workflow can be handed off, incrementally improved, and eventually automated, while a task list gets rebuilt every quarter. The six foundational steps:

Step 1: Standardize data collection from portfolio companies. Define a standard financial data request for portcos: what line items you need, in what format, and by what deadline. A standardized template reduces the incoming variation that drives manual reformatting work. Track submission completion rates by company each quarter and follow up systematically. Late portco data is the single most common cause of delayed LP reports, and it is almost always predictable from prior quarter patterns.

Step 2: Build a master reporting data model. Create a single source-of-truth data model in your portfolio monitoring or reporting platform that maps every field in your LP reports to a specific upstream data source. When a figure changes upstream, the change flows through to all LP report variants automatically. This eliminates the reconciliation step that currently consumes the most reporting hours at most firms: the manual comparison of figures across multiple systems to identify which version is current.

Step 3: Automate data validation before drafting begins. Build validation rules that flag missing data, mathematical errors, and consistency breaks before report drafting begins. Examples: NAV roll-forward that does not reconcile to the prior period; IRR that has moved more than 100 basis points without a corresponding realization or write-down; portfolio company revenue that is materially inconsistent with the prior period without a commentary note. Human reviewers should spend their time on judgment calls, not arithmetic.

Step 4: Document LP-specific customization requirements. Record each LP's reporting preferences, template requirements, currency, language, and performance attribution method in a single reference document. Apply them systematically using the platform's LP configuration settings rather than relying on institutional memory held by individual team members. Customization at scale requires documented rules, not recollection.

Step 5: Build a structured review and approval workflow. Map the approval chain for the quarterly report: who reviews financial statements, who approves portfolio company commentary, who handles legal and compliance sign-off, and in what sequence. Workflow management software can route drafts automatically and track sign-off status. Unstructured review processes using email chains and shared drive comments are where factual errors and outdated figures survive to LP delivery.

Step 6: Automate distribution and access tracking. Use a platform with LP portal functionality to distribute reports, log which LPs have opened them, and send reminders to investors who have not accessed their reports within 72 hours. Track LP questions and requests in a centralized system so the IR team can identify recurring data gaps to address in the next cycle rather than answering the same questions manually each quarter.

For emerging managers: Firms below $500M AUM often defer formal LP reporting workflows on the assumption that their LP base is small enough to manage informally. This assumption costs more at fundraising time than it saves during operations. LPs who experienced inconsistent or underpowered reporting during Fund I apply a governance discount when evaluating the Fund II commitment. Building a proper reporting infrastructure at the $150M fund stage is low-cost relative to the fundraising headwind of not having it when raising $400M or $600M.

AI extraction tools link every figure in an LP report back to its original source document, providing the audit trail that compliance teams require and that LPs request when they ask to verify a number.

LP reporting is not a compliance exercise. It is a competitive differentiator. The funds that report well — clearly, consistently, and on time — build the LP trust that drives re-up decisions, secondary transactions, and referrals to new investors. The funds that report poorly spend their re-up conversations managing operational credibility questions rather than discussing investment performance.

The shift from manual reporting to AI-augmented workflows is an operational maturity decision as much as a technology one. The question is where your team stands on that path, relative to the funds competing for the same LP capital at your next fundraise.

V7 Go is built for the document-intensive workflows at the core of private equity operations: extracting portfolio company financials, validating fund-level data, and generating the structured deliverables that institutional LPs require. If your firm is ready to compress a 6-week reporting cycle into 8 days, start with V7 Go's LP reporting automation.

What is LP reporting in private equity?

LP reporting is the formal process by which fund managers (general partners, or GPs) communicate financial performance, portfolio updates, and capital activity to their investors (limited partners, or LPs). In private equity, LP reporting is delivered on a quarterly cycle, with a more comprehensive annual audited financial report. A complete quarterly LP report includes fund-level financial statements, net asset value calculations, performance metrics (IRR, TVPI, DPI, MOIC), individual portfolio company updates, capital account statements showing each LP's interest, and management commentary. LP reporting is a formal, structured communication with defined data requirements, often governed by the fund's limited partnership agreement (LPA) and, for institutional LPs, by the ILPA Reporting Template standard. LPs increasingly evaluate the quality of reporting during due diligence as a signal of GP operational maturity.

+

What should be included in an LP report?

A complete LP report includes six core sections. First, fund-level financial statements prepared under GAAP or IFRS, including an income statement, balance sheet, and statement of changes in partners' capital. Second, a NAV roll-forward showing how the fund's net asset value moved from the prior period, accounting for contributions, distributions, unrealized gains, and realized gains. Third, performance metrics: net IRR, TVPI, DPI, and MOIC at fund level and for individual investments, benchmarked against the S&P 500 PME or Cambridge Associates index. Fourth, portfolio company updates covering trailing revenue, EBITDA, key operational KPIs, and management commentary. Fifth, individual LP capital account statements (PCAP) showing each investor's contributions, distributions, management fees, carried interest, and attributable NAV. Sixth, management commentary providing market context, pipeline updates, and remarks on deployment pace.

+

What is the ILPA reporting template?

The ILPA Reporting Template is a standardized format for private equity fund reporting published by the Institutional Limited Partners Association. First issued in 2011, the template defines how GPs should structure and disclose management fees, fund expenses, portfolio company fees, carried interest calculations, and transaction costs. In January 2025, ILPA released a significant update alongside a new standalone Performance Template. The 2025 update removes the prior two-tier disclosure structure, requiring GPs to report at a single uniform level of detail with no reordering or repurposing of line items permitted. ILPA expects adoption for investment-period funds and new funds from Q1 2026. The Performance Template, which standardizes how IRR, TVPI, and other metrics are calculated and disclosed, begins data capture in Q1 2026, with first delivery required for the quarter ending March 31, 2027. ILPA template compliance is increasingly a condition of institutional LP investment.

+

What is the best LP reporting software?

The best LP reporting software depends on your fund's size, strategy, and integration needs. Chronograph suits mid-market to upper-market buyout funds with 15 or more portfolio companies, offering strong ILPA template support and an LP portal. Allvue Systems works well for multi-strategy firms (buyout alongside credit or real assets) wanting a single platform from portfolio management through LP distribution. Dynamo Software is strongest for funds where LP relationship management is as important as financial data reporting. Fundwave serves emerging managers needing ILPA-compliant reporting without enterprise implementation timelines or pricing. When evaluating any platform, the seven key criteria are: data source integrations, ILPA template compliance, workflow automation capability, LP portal functionality, audit trail depth, SOC 2 security certification, and scalability across fund strategies. Firms should also assess the vendor's roadmap for AI-assisted reporting automation, which is becoming a meaningful differentiator in the market.

+

How can AI improve LP reporting?

Manual LP reporting at a typical mid-market private equity firm takes four to six weeks from quarter close to LP delivery, consuming 500 to 800 hours of senior staff time per cycle. The largest time sinks are portfolio company data collection (waiting for portco financial packages), manual data reconciliation across fund administration and accounting systems, per-LP report formatting and customization, and internal review and compliance sign-off. AI-augmented reporting workflows have demonstrated the ability to compress this to 8 to 12 days. The largest gains come from automated extraction of portfolio company financial packages, which eliminates the manual data entry and reformatting step, and from AI-assisted narrative drafting, which converts management commentary from a writing exercise to an editing exercise. For teams at funds with 20 or more portfolio companies and 30 or more LPs, the time savings typically justify the workflow investment within the first reporting cycle.

+

How long does LP reporting take?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.