Knowledge work automation

16 min read

—

The ILPA Reporting Template had not been meaningfully updated since 2016. In the decade since, PE fund structures grew more complex, fee arrangements more varied, carried interest calculations more contested, and LP scrutiny considerably more systematic. The January 2025 release of the updated suite of ILPA reporting templates is not a minor revision. It is a structural overhaul, and every GP with a fund in its investment period or a new fund launched after January 1, 2026 is now operating under its requirements.

The most consequential change is also the simplest to state: ILPA removed the ability to modify the template. The 2016 version allowed GPs to repurpose line items, reorder expense categories, and supplement the template with their own fields. In practice, this meant LPs received forty different interpretations of what was nominally the same standard. The 2025 update eliminates that discretion entirely. The structure is fixed. The line items are fixed. GPs must report into the template as designed, not as convenient.

This matters because it changes the LP's ability to compare. An LP with positions across twenty PE funds can now, for the first time, read twenty quarterly Reporting Templates that use the same expense categories, the same internal chargeback structure, and the same performance metric definitions. The comparison that was theoretically possible under the 2016 template but practically impossible due to structural variation is now, for new funds, actually achievable.

For context on the specific performance reporting requirements around IRR and subscription lines, the IRR reporting guide covers the Performance Template and DPI shift in depth. This article focuses on what the full three-template suite requires operationally and how GPs are building the workflows to deliver it.

In this article:

What changed in the 2025 ILPA templates and why the 2016 version needed replacing

What the three-template suite covers: Reporting, Performance, and Capital Call and Distribution

The four implementation steps GPs need to complete before Q1 2027

How AI document agents are compressing the quarterly reporting workflow

AI for document processing

Produce ILPA 2025 reports without rebuilding your process

Get started today

Why the ILPA reporting template needed a full rebuild in 2026

The 2016 ILPA Reporting Template set a floor, not a standard. GPs adopted it at varying levels of compliance, interpreted ambiguous line items according to their own conventions, and used the modification flexibility to produce templates that served their reporting needs rather than LP comparability needs. A fund administrator who worked with 50 PE clients in 2023 likely produced 50 distinct quarterly report formats that all claimed to be ILPA-compliant.

The new template eliminates that ambiguity. The structure is locked. ILPA explicitly states that the updated Reporting Template does not permit repurposing, reordering, or supplementing of line items. For GPs accustomed to adjusting the template to fit their reporting infrastructure, this requires genuine system infrastructure work, not a surface reformatting exercise.

The three substantive changes in the Reporting Template

Beyond the structural lock-in, the updated Reporting Template introduces three categories of new disclosure that the 2016 version did not require at this level of granularity.

The first is expanded fee and expense transparency. The new template requires greater detail on management fees, including fee offsets and step-downs, and on partnership expenses across a more granular set of categories. GPs who previously aggregated expenses at the fund level must now break them out by type and recipient in a standardized structure that LPs can compare across their portfolio of managers.

The second is internal chargeback disclosure. This is the most operationally demanding new requirement for many mid-market GPs. Internal chargebacks are expenses allocated or paid to the GP or related persons from the fund, including allocations for back-office services, compliance functions, and technology costs that the fund contributes to. The 2016 template treated these inconsistently; the new template requires them to be broken out explicitly. For firms that have historically kept this allocation methodology in a spreadsheet rather than their fund administrator system, this requires either a system change or a new data extraction process.

The third is subscription line interest. The updated template requires subscription line interest to be reported as a separate expense line, not bundled into general partnership expenses. This connects to the broader transparency agenda around subscription facilities and their effect on reported performance.

What the full three-template suite covers

The 2025 update is not a single document. It is a coordinated suite of three templates designed to work together, each covering a different dimension of the GP-LP reporting relationship.

The Reporting Template is the quarterly financial summary: fees, expenses, carried interest, and fund-level financial data. It is the primary mechanism through which LPs track the cost of the GP relationship and verify that fee structures are operating as disclosed in the LPA. This template applies to funds in their investment period during Q1 2026 and to all new funds from January 2026.

The Performance Template covers fund-level return metrics: IRR and TVPI reported with and without subscription line impact, DPI, RVPI, and a cash flow table that allows LPs to verify the GP's calculations independently. Two methodologies are supported: the Granular Methodology for GPs that classify capital calls at the transaction level, and the Gross Up Methodology for those that do not. The Performance Template applies to funds commencing operations from Q1 2026, with the first delivery in Q1 2027.

The Capital Call and Distribution Template has been updated to align with the other two templates. It provides the accounting detail behind each capital call and distribution notice, creating a paper trail that feeds into the Performance Template's cash flow table. For funds on the Performance Template, the updated Capital Call and Distribution Template should be used for funds launched from Q1 2026. For others, it comes into effect from Q1 2027.

The manual quarterly reporting workflow for LP reports spans data collection from multiple systems, classification, reconciliation, and narrative writing. The ILPA 2026 templates add granularity requirements at each step that compound the existing workload.

The data silo problem that makes implementation harder than it looks

The practical challenge in implementing the new templates is not understanding what they require. It is that the data they require lives in disconnected systems that were not built to talk to each other at the level of granularity the templates now demand.

A typical mid-market PE fund's quarterly reporting data comes from at least three sources: the fund administrator's general ledger, which holds the financial statements and expense records; the portfolio monitoring system, which holds company-level KPIs and valuation data; and the GP's own records, which often hold the internal chargeback allocations, management fee calculations, and carry waterfall outputs. Each system has its own data format. None of them was designed to map directly onto the ILPA template's fixed line item structure.

The internal chargeback problem is the clearest example. Many GPs track the allocation of back-office costs across the fund, the management company, and portfolio companies in a spreadsheet maintained by their CFO or Controller. That spreadsheet is not connected to the fund administrator system. At quarter-end, someone has to reconcile the spreadsheet against the general ledger, map the allocations to the ILPA expense categories, and confirm that the totals agree before the template is issued. Under the 2016 template, this process had enough flexibility to smooth over inconsistencies. Under the 2025 template, the line items are fixed and the reconciliation has to be clean.

The reconciliation failure scenario is worth making concrete. A mid-market buyout fund closes its books for Q1 2026. The fund administrator extracts partnership expenses from the general ledger. The GP's CFO extracts internal chargeback allocations from a Controller-maintained spreadsheet. The two outputs use different cost center labels that do not map cleanly to the ILPA template categories. The person doing the mapping, typically a fund accounting associate, has to make judgment calls about where to classify three ambiguous expense lines. Those calls may be consistent with how the same associate classified the same expenses last quarter, or they may not be, if this is the first time the ILPA template is being completed and there is no established crosswalk document to follow.

What the LP receives is a template that balances, but whose internal allocations differ from what a different fund in their portfolio reported for similar expenses under the same ILPA categories. The LP's head of private equity is trying to compare management company chargeback rates across 12 managers. Six of them completed the mapping with documented methodology. Six did not. The ones that did not appear to be reporting lower chargebacks, but the LP cannot tell whether that reflects genuinely lower costs or a classification choice that buried some costs in general partnership expenses. This is exactly the comparability problem the ILPA template update was designed to eliminate, and it persists when GPs implement the template structure without resolving the underlying data discipline problem.

The BDO analysis of ILPA Q1 2026 implementation progress found that the majority of GPs who had begun template preparation were on track with the Reporting Template but significantly behind on the Performance Template, where the Granular Methodology classification requirements demand the kind of transaction-level funding source data that most fund administrators were not capturing in 2024 and early 2025. The practical implication is that a GP who starts the data assessment in Q3 2026 for a Q1 2027 Performance Template delivery will have less than two quarters to resolve gaps that may require system configuration changes with six-to-twelve week lead times.

Research on fund reporting practices in private equity is consistent on this point: GPs who treat investor reporting as a data management problem and invest in the systems to maintain clean, accessible records perform better on LP satisfaction and fundraising outcomes than those who treat it as a compliance exercise done under time pressure each quarter. Marketing Alternative Investments documents this directly: a GP who develops a reputation for sharing only good news, or for reporting that is accurate but inconsistent or hard to parse, damages the investor relationship in ways that are difficult to repair. The transparency the ILPA templates demand is not separate from that relationship. It is part of what defines it.

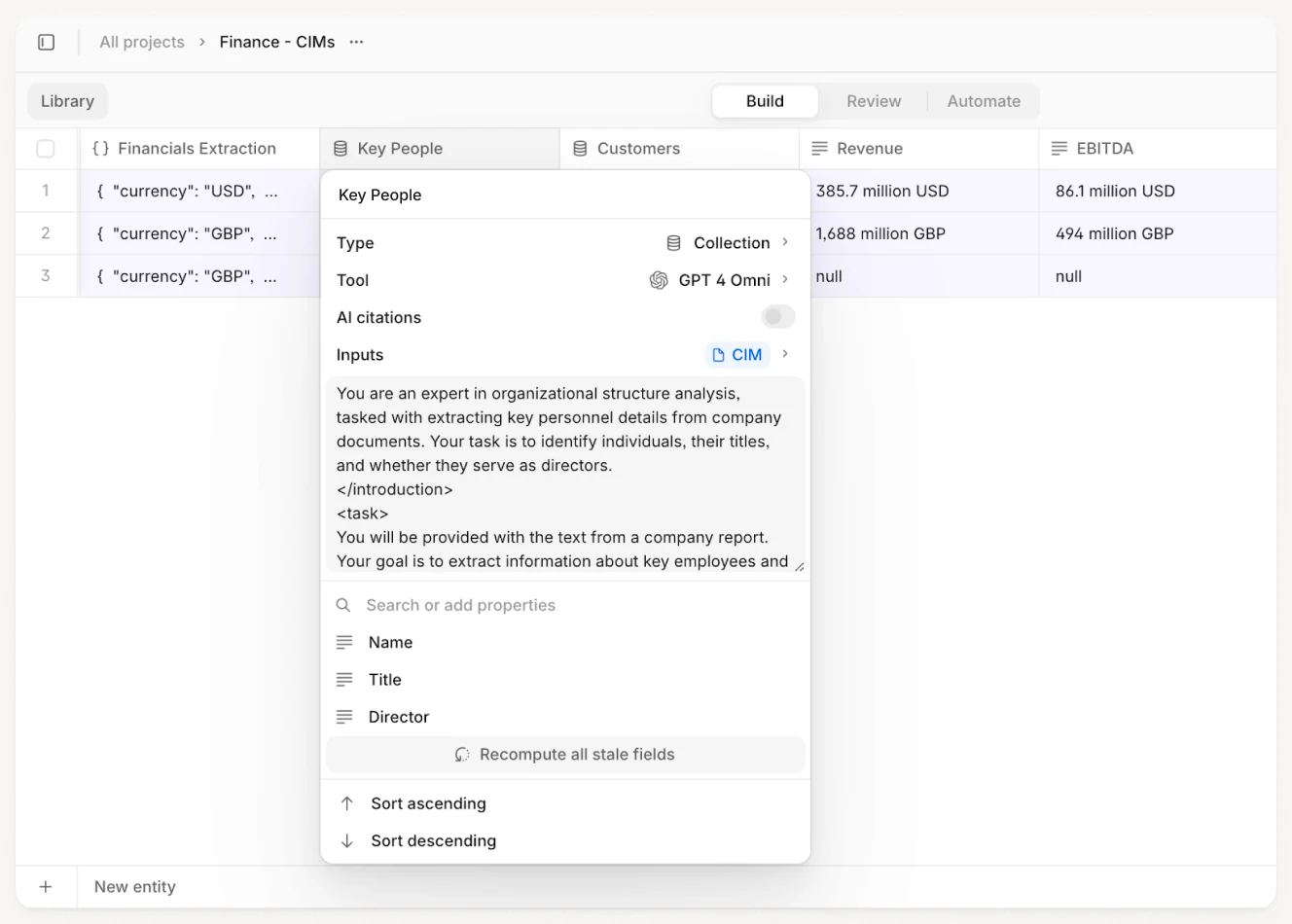

AI agents configured for fund administration documents extract expense classifications, chargeback allocations, and fee data from source records and map them to standardized output fields, reducing the manual reconciliation work that currently sits between raw data and the ILPA template.

The four implementation steps and what each one actually involves

Gen II Fund Services and other fund administrators working through the 2025 template update have converged on a four-step framework for GP implementation. The steps are sequential, and the first two are where most firms are currently behind schedule.

Step 1: Data assessment

Before any template can be populated correctly, a GP needs to know whether the data the template requires is being captured in their current systems. The data assessment maps each line item in the new Reporting Template and Performance Template to a data source: which system generates this figure, in what format, at what frequency, and whether the figure is already being captured at the granularity the template demands.

For most mid-market GPs, this assessment produces a gap list. Common gaps include: internal chargeback allocations tracked in spreadsheets rather than the fund admin system; subscription line drawdown and repayment records not tagged to specific investments; management fee offsets calculated outside the administrator's general ledger; and partnership expenses categorized differently across the three or four cost centers the fund uses. Each gap requires either a system change or a new data extraction process before the template can be populated accurately.

Step 2: Expense mapping

The expense mapping step translates the GP's existing expense categories into the ILPA template's fixed line item structure. The new template's structure is more granular than most fund administrators' standard chart of accounts, which means this is not a one-to-one mapping. Some existing line items will split into two or three ILPA categories; some ILPA categories will require pulling data from fields that are currently aggregated together.

The expense mapping document is the deliverable from this step: a crosswalk table that shows, for each ILPA line item, which source system field populates it, what transformation is applied if any, and which team member is responsible for the extraction. Without this document, every quarterly report requires the same mapping exercise to be performed from scratch.

Steps 3 and 4: Internal chargeback reporting and system preparation

Internal chargeback reporting requires the GP to identify all expenses allocated or paid to the GP or related persons from the fund, break them out by category, and present them in the template's dedicated disclosure section. For firms that have historically included these in general partnership expenses without separate disclosure, this requires both a data change and a communication exercise: LPs will see, for the first time, an explicit line item showing what the fund pays to the GP for back-office and support services.

System preparation is the final step: updating the fund administrator's system configuration, the chart of accounts mapping, and the template population process to generate the required output automatically at quarter-end rather than through manual extraction and transformation. Firms that complete this step before Q1 2026 data capture begins produce their first template through an efficient workflow. Firms that do not will spend multiple quarters doing the mapping manually before the system configuration catches up.

The timeline for completing all four steps is longer than most GPs initially expect. The data assessment alone — step one — typically takes four to six weeks for a fund with a full investment period's worth of transactions. It requires input from the fund administrator, the GP's CFO, and whoever manages the portfolio monitoring system, and those parties often disagree on what data is available and in what format. A fund administrator may report that internal chargeback data is available in their system; the GP's CFO may clarify that the relevant data has never been entered there and has only ever existed in a spreadsheet that no one else has access to. Resolving these discrepancies takes time that is not visible in the implementation plan until it becomes a bottleneck.

Step two — expense mapping — is where the most implementation projects stall. The ILPA Reporting Template has approximately 60 distinct expense line items. A typical mid-market PE fund's chart of accounts has between 30 and 40 active expense categories. The crosswalk between the two requires a line-by-line review, a decision on how to handle items with partial overlap, and documentation sufficient for a different team member to follow the same mapping in a future quarter. Firms that skip the documentation in the interest of getting the first template out typically repeat the same mapping discussion in subsequent quarters, with slightly different conclusions each time.

The practical standard that experienced fund administrators apply is to treat the expense mapping document as a living contract between the GP and the administrator — specific enough that either party could produce the ILPA template output independently, and version-controlled so that methodology changes are tracked and disclosed. This document does not exist in most GP-administrator relationships today. Creating it is the work that makes subsequent quarterly reporting reproducible rather than a bespoke exercise each period.

Multi-agent workflows can work across fund administration records, GP spreadsheets, and portfolio monitoring data simultaneously, consolidating the data the ILPA template requires from disparate sources into a single structured output.

How AI compresses the quarterly reporting workflow

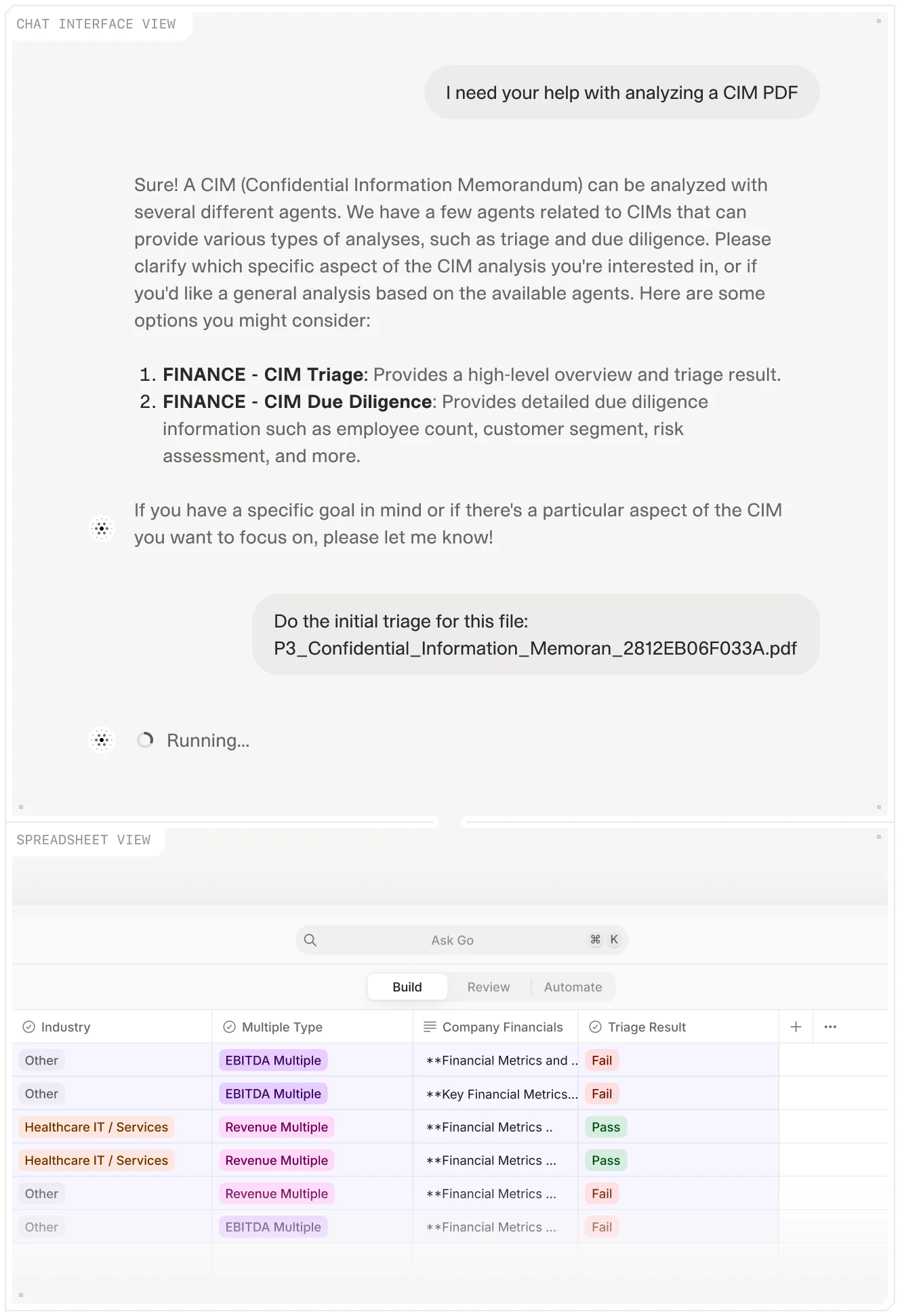

The ILPA template implementation challenge is fundamentally a document processing and data extraction problem. Each of the four implementation steps involves reading source documents (expense statements, capital call notices, chargeback allocation schedules), extracting the relevant fields, applying a mapping, and populating a structured output. This is exactly the workflow that AI document agents handle well.

Expense classification from source documents

A fund's quarterly expense record arrives as a combination of fund administrator statements, external invoices, and internal allocation schedules. Classifying these expenses against the ILPA template's fixed categories requires reading each document, identifying the expense type, determining the correct ILPA line item, and recording the amount. An AI agent configured for this document set can process an entire quarter's expense documentation in hours and output a structured expense schedule mapped to ILPA categories, with every line item cited back to its source document. The financial statement spreading automation from V7 Go applies the same extraction logic to fund-level financial statements, enabling the quarterly financial data in the Reporting Template to be populated directly from source records.

Cross-template consistency verification

The three ILPA templates are designed to be consistent with each other: the capital call data in the Capital Call and Distribution Template feeds the cash flow table in the Performance Template, which in turn must reconcile with the financial data in the Reporting Template. A figure that appears in two templates must agree. A document comparison agent can run this consistency check automatically before the templates are issued, flagging any discrepancy between the three outputs and pointing to the specific lines that differ.

The document comparison agent from V7 Go handles exactly this: compare two structured documents, identify any numerical discrepancy, and report it with citations to the specific fields in each document. Applied to the ILPA template suite before quarterly delivery, it catches the cross-template inconsistencies that currently surface in LP review rather than in GP quality control.

Capital call notice extraction for the Performance Template

The Performance Template's cash flow table requires transaction-level data on every capital call and distribution over the fund's life, classified by funding source. Capital call notices contain this information: they specify the investment, the amount, the date, and whether the call is drawing from LP commitments or repaying a subscription facility. An agent configured for capital call notice documents can build the cash flow table from the underlying notices, producing the input the Performance Template requires without the analyst time that manual extraction currently demands.

For context on the broader portfolio data workflow that feeds into quarterly reporting, the portfolio monitoring guide covers how KPI collection from portfolio companies connects to fund-level reports. The ILPA template output is only as good as the underlying data discipline that produces it.

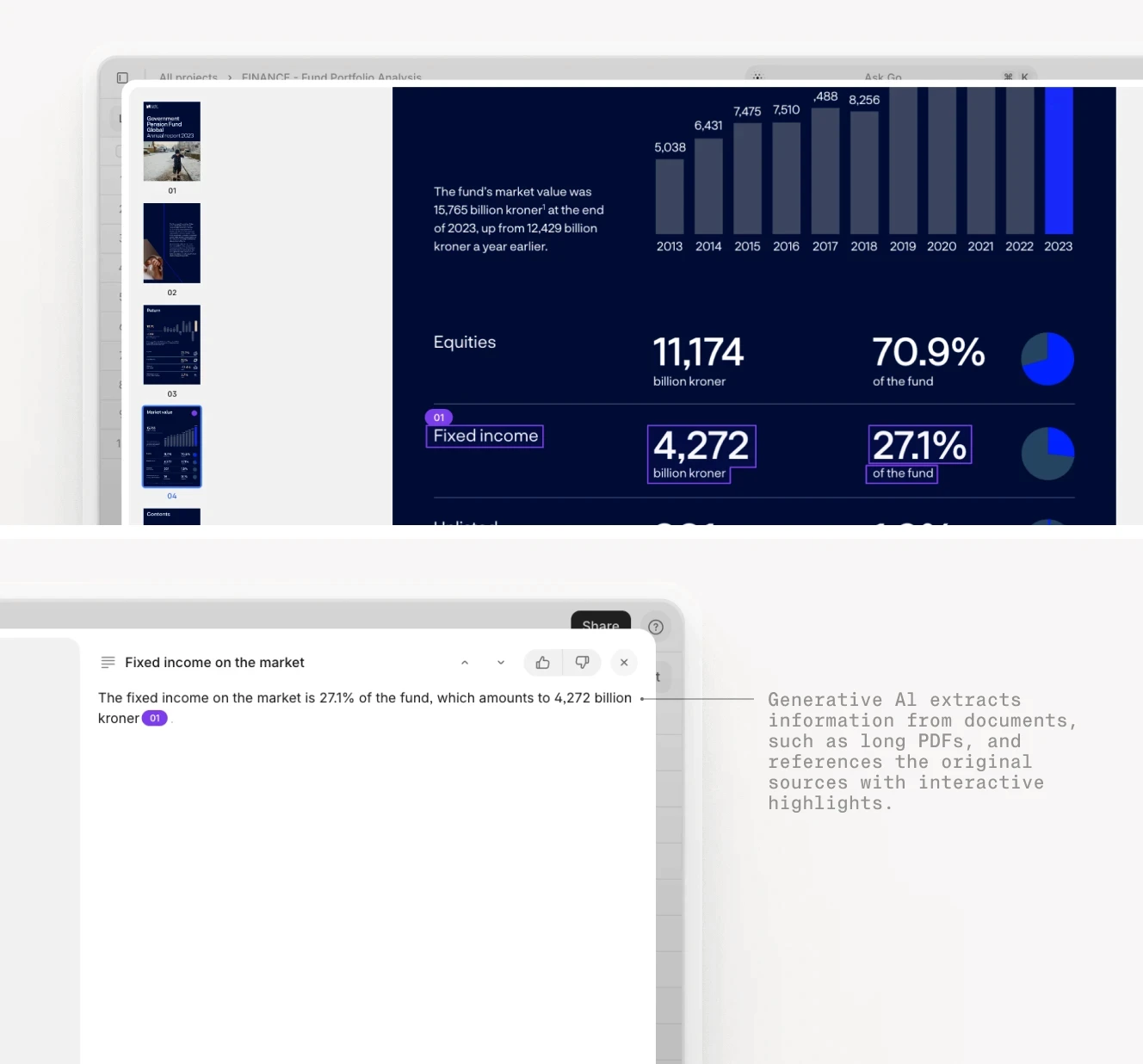

Extraction with source citations means every figure in the ILPA template can be traced to its originating document. This supports LP verification and reduces the Q&A cycles that typically follow each quarterly delivery.

The firms that arrive at Q1 2027 in the best position are those that treated 2026 as a systems and workflow year, not a compliance deadline year. They completed the data assessment, built the expense mapping, resolved the internal chargeback disclosure, and configured their extraction workflows before the first template delivery was due. For a look at how AI applies across the full PE deal workflow including due diligence, the generative AI in finance guide covers the complete picture.

The firms that treat this as an opportunity will look different from the ones that treat it as compliance

The ILPA 2026 template suite is a transparency standard. But it is also a test of operational maturity. A GP that can produce clean, consistent, timely templates across all three documents from day one of implementation is signaling something specific to LPs: that the fund's data infrastructure is capable, that its internal controls are strong, and that its reporting does not require manual heroics each quarter.

That signal matters for fundraising. LPs doing due diligence on a GP's operations will now have standardized data to compare both performance and operational process. A fund that delivers ILPA templates with consistent formatting, no reconciliation discrepancies, and complete internal chargeback disclosure from the first quarter is a different category of manager than one that delivers delayed, inconsistent, or incomplete reports.

The LP due diligence process three years from now will look different because of this standard. When an LP is evaluating a re-up decision for a Fund III in 2028, they will have six to eight quarters of ILPA template data from both the GP in question and the other managers in their portfolio. The comparison will be quantitative in a way it has not historically been: chargeback rates, subscription line usage, fee offset application, and performance attribution will all be visible in a standardized format. A GP that has delivered clean, consistent templates from the first quarter will have built a credibility record. A GP that has had recurring reconciliation discrepancies, delayed submissions, or incomplete disclosure sections will have built a different kind of record — one that cannot be revised before the re-up conversation arrives. The time to start generating that data cleanly is 2026, before the track record is set.

The work required to get there is real. It involves systems, it involves data, and it involves internal chargeback conversations that some GPs have been avoiding for years. But the firms that do the work in 2026 will not be doing it again in 2027, 2028, and 2029. The ones that delay will be rebuilding from a reactive position while their reporting credibility erodes with each imperfect quarterly delivery.

If the document extraction and mapping work is the current constraint, V7 Go's document intelligence platform is built for the fund administration document types the ILPA templates require: capital call notices, expense statements, chargeback schedules, and financial statements. Define the extraction schema once, run it each quarter, and get a structured output ready for template population with every figure cited to its source document.

What is ILPA and why do its reporting templates matter?

The Institutional Limited Partners Association (ILPA) is a global organization representing institutional investors in private equity funds. Its reporting templates are industry-developed standards that define how GPs should report financial and performance information to their LP investors on a quarterly basis. Unlike SEC regulations, ILPA templates are not legally mandated for most funds, but they have become the de facto standard that sophisticated institutional LPs expect GPs to follow. When an LP asks a GP whether they use ILPA reporting, they are asking whether the quarterly reports they receive will be structured in a way that allows comparison across their portfolio of fund managers. The 2016 ILPA Reporting Template was the first widely adopted version and remained the standard for nearly a decade. The 2025 update, effective for qualifying funds from Q1 2026, represents the most significant structural revision since the original template's release and adds new requirements on fee transparency, expense disclosure, and performance metric standardization that the 2016 version did not include at comparable granularity.

+

What changed from the 2016 ILPA template to the 2025 update?

Several significant changes distinguish the 2025 ILPA templates from the 2016 version. The most fundamental is the removal of template modification flexibility: the 2016 template allowed GPs to repurpose, reorder, and supplement line items, resulting in inconsistent application across the industry. The 2025 template locks the structure completely. On substance, the update adds more granular fee and expense categories, introduces an explicit internal chargeback disclosure section that requires GPs to break out expenses allocated to the GP or related persons from fund assets, and requires subscription line interest to be reported as a separate expense line. The new Performance Template, which did not exist in 2016, adds standardized IRR and TVPI reporting with and without subscription line impact, a cash flow table for LP verification, and dual calculation methodologies (Granular and Gross Up). The Capital Call and Distribution Template has also been updated to align with the new structures. Together, these changes make the 2025 suite a materially more demanding standard than its predecessor.

+

What is the implementation timeline for the new ILPA templates?

The implementation timeline varies by template type. The updated ILPA Reporting Template applies to funds still in their investment period during Q1 2026 and to all new funds commencing operations on or after January 1, 2026. For these funds, the first delivery under the new Reporting Template format should occur with the Q1 2026 quarterly report. The new Performance Template applies to funds commencing operations on or after January 1, 2026. Data capture under the Performance Template begins in Q1 2026, but the first actual delivery is not required until Q1 2027, covering inception-to-date data through March 31, 2027. The updated Capital Call and Distribution Template is aligned with the Performance Template timeline for new funds: those on the Performance Template should use the updated Capital Call and Distribution Template for funds launched from Q1 2026, while for all other funds the updated Capital Call and Distribution Template is not required until Q1 2027. GPs should confirm with their fund administrators which templates apply to their specific funds and begin the data assessment and system preparation work as early as possible before their first required delivery date.

+

What are internal chargebacks and why is their disclosure new?

Internal chargebacks are expenses that are allocated or paid from the fund to the GP or related persons for services provided to the fund. Common examples include allocations for compliance functions, back-office services, technology platforms, legal services, and similar support costs where the GP or a GP affiliate provides the service and the fund bears part or all of the cost. Under the 2016 ILPA template, these allocations were often reported within general partnership expenses without separate identification. The 2025 update requires them to be broken out as a distinct disclosure category, identifying specifically what was allocated to or paid to the GP or related persons. For LPs, this disclosure answers a question they have historically had limited ability to answer from the quarterly report alone: exactly how much of the fund's expenses is flowing to the GP's own organization rather than to third-party service providers. The disclosure does not prohibit these arrangements, but it makes them transparent and allows LPs to assess whether the GP's internal cost allocation practices are consistent with what was disclosed in the LPA.

+

How does the Performance Template differ from the Reporting Template?

ILPA templates are industry standards, not legal mandates. There is no regulatory penalty for failing to adopt them. However, the practical consequences of non-adoption are significant and are becoming more so as LP adoption increases. Sophisticated institutional LPs are increasingly making ILPA template compliance a condition of their due diligence process and, in some cases, of their commitment to a new fund. A GP that declines to adopt the 2025 templates or that adopts them inconsistently is signaling to LPs that its reporting infrastructure is either unable to meet the standard or that it prefers less transparency on fees and expenses. Both signals are negative. Additionally, as more GPs adopt the standard, LPs will have a growing pool of compliant GPs to benchmark against. A non-compliant GP's reporting will stand out increasingly as an outlier. The business risk is not a fine. It is a fundraising disadvantage and a relationship cost with LPs who value the comparability the standard provides.

+

What happens to GPs that do not comply with the ILPA templates?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.