Knowledge work automation

16 min read

—

The IRR your fund reports and the IRR your LP uses to evaluate you are probably not the same number. They might not even be using the same methodology to calculate it. This is not a technicality. It is the central problem in private equity performance reporting, and it is now the subject of the most significant industry standard overhaul in a decade.

Private equity IRR reporting has always required judgment: when to call capital, how to treat subscription credit facilities, which calculation method to apply at the fund versus the investment level. In practice, that judgment discretion has allowed meaningful differences in reported IRR between funds with identical underlying performance. A fund that delays capital calls through a subscription line and a fund that calls capital directly can report materially different IRRs on the same portfolio.

LPs have noticed. As of 2025, the share of limited partners citing distributions to paid-in capital (DPI) as their most critical performance metric is 2.5 times higher than it was three years prior, according to McKinsey's Global Private Markets Survey. IRR is still tracked. But cash returned to investors is now the number that determines whether a GP raises a successor fund on schedule or spends an extra year in the market explaining why the paper returns looked better than the actual distributions.

This article covers what those IRR calculation differences actually involve, why subscription credit lines became a structural reporting issue, and what the ILPA 2026 Performance Template requires GPs to disclose starting this year. For context on how LPs evaluate fund managers across the full due diligence process, the LP due diligence guide covers the complete picture.

In this article:

Why private equity IRR reporting produces different numbers from identical portfolios

How subscription credit lines inflate reported IRR and why LPs are now tracking it separately

What the ILPA 2026 Performance Template requires and when it takes effect

How AI document agents handle the transaction-level classification work the new standard demands

AI for document processing

Give LPs the performance transparency they now demand

Get started today

Why private equity IRR reporting is harder to read than it looks

The core problem with IRR as a PE performance metric is not the math. Any fund administrator can calculate IRR correctly given a set of cash flows and dates. The problem is that several legitimate choices made before that calculation begins can produce dramatically different outputs from the same underlying investment performance.

The most documented example is methodology selection. Academic research in Venture Capital, Private Equity, and the Financing of Entrepreneurship shows directly: switching from the calendar-time method to the time-zero method on the same portfolio data can materially inflate reported returns — research using Burgiss database data has documented significant gaps on identical portfolios depending on the methodology applied and decreases it from 43% to 34% in another. The direction of the swing is unpredictable. The magnitude is material. And until the ILPA 2026 template, there was no requirement to disclose which method was being used, let alone to calculate both.

The implication is direct: two GPs running identical portfolios, generating identical cash returns, can report meaningfully different IRRs depending entirely on their internal methodology choice. An LP comparing fund performance across their private markets portfolio may be comparing figures computed under different rules, without any way to tell from the quarterly report.

The methodology question extends beyond calendar-time versus time-zero. GPs also make choices about how to handle management fee offsets, how to treat transaction costs at the fund versus investment level, and whether to calculate gross IRR from fund-to-investor cash flows or from fund-to-investment cash flows. Each of these choices is defensible. None of them is standardized across the industry. A GP that calculates gross IRR using fund-to-investment cash flows will typically report a higher gross figure than one using fund-to-investor cash flows, because the former excludes fees from the denominator. The difference is not fraud. It is discretion. And discretion, applied consistently in one direction, produces performance figures that look better than they would under a more conservative convention.

The deeper problem is that LPs often do not know which conventions their GPs are using. Quarterly letters report IRR. They rarely report the methodology behind it. Fund LPAs (limited partnership agreements) sometimes specify calculation methodology, but the provisions are frequently vague and the interpretation is left to the GP. Academic research using data from the Burgiss database, covering 997 buyout funds and 1,074 venture funds, found documented evidence of return misreporting during fundraising periods, with underperforming managers more likely to manipulate reported returns and less likely to raise a successor fund. The manipulation is not always intentional. The point is that the reporting framework has historically made it easy, and the ILPA 2026 template is the first major structural attempt to close that gap through standardization rather than regulation.

Fund performance dashboards display IRR figures, but the calculation methodology behind those figures is rarely disclosed alongside them. The same underlying portfolio can produce different reported returns depending on which method a GP applies.

The subscription credit line effect: a concrete illustration

Subscription credit lines, also called capital call facilities, let GPs borrow against LP commitments rather than calling capital directly. A GP that uses a subscription line to fund an investment in January, then calls LP capital to repay it in June, has effectively shortened the LP's measured investment period by six months. Since IRR is time-sensitive, a shorter investment period on a given return produces a higher reported IRR.

This is not fraud. The investment may have genuinely performed well. The IRR figure is mathematically accurate under the chosen measurement convention. But an LP comparing this fund's IRR against a fund that called capital directly in January is comparing figures computed under different timing assumptions. The fund that used the subscription line will show a higher IRR even if the underlying investment returns are identical. The difference can run to several percentage points on a fund level.

The research is clear on the scope of this. The use of subscription credit facilities has expanded substantially across the industry. A significant share of reported fund-level IRRs in recent vintages include the timing benefit from delayed capital calls. This is not a fringe practice by a few aggressive managers. It became standard procedure across many mid-market and large buyout funds through the 2015-2022 period, and many LPs only realized the scope of the effect when they started asking for calculations with and without the subscription line separately.

The effect can be quantified. A fund that delays the average capital call by six months through a subscription line and generates a 2x return over a five-year investment period will show a materially higher IRR than the same fund calling capital directly. The six-month delay shortens the measured investment period from the LP's perspective while the actual investment timeline is unchanged. On a five-year hold, this timing adjustment can inflate the reported IRR by several percentage points. On a three-year hold, the effect is proportionally larger because the delay is a bigger fraction of the total period.

What made this practice defensible for so long is that subscription credit lines serve legitimate operational purposes. They allow GPs to move quickly on investments without waiting for LP capital call mechanics. They reduce the administrative friction of calling small amounts of capital from large LP bases. A fund with 100 LP investors cannot realistically call capital in 48 hours; a subscription line bridges the gap. The problem is that a tool designed for operational efficiency became a tool for performance presentation, and the two uses are hard to distinguish from outside the GP's books.

Classifying each capital call transaction by funding source (LP capital vs. subscription line drawdown) is the core data requirement of the ILPA 2026 Performance Template. AI agents can work through capital call notices and fund administration records to produce this classification at scale.

What happens when an LP runs the numbers themselves

An increasing number of sophisticated LPs no longer accept the IRR in a quarterly letter at face value. They run their own calculations. This is not a sign of adversarial relationships; it is a sign of a more analytically mature LP base, and GPs who understand this are better prepared for the conversations it produces.

The LP calculation process is straightforward in principle. The LP takes the cash flow history they have received over the fund life: capital calls, distributions, and their estimated share of remaining net asset value. They compute IRR from those cash flows using their own system, using their own methodology. If their number matches the GP quarterly report, the conversation is over. If their number does not match, the conversation begins.

The divergences LPs commonly find fall into three categories. First, the subscription line timing effect: the LP's calculation starts the clock from when they received a capital call, not from when the underlying investment was made. If the GP's reported IRR starts the clock from when the investment was made (before the LP was called), the two calculations will differ. Second, methodology differences: the GP may be using a different IRR calculation convention than the LP's system defaults to. Third, NAV timing: if the GP marks the portfolio at a different date or using a different methodology than the LP assumes for the residual value, the terminal cash flow input differs.

None of these divergences is necessarily evidence of wrongdoing. But each requires an explanation, and a GP that cannot provide a clear account of why their reported IRR differs from an LP's independent calculation has a relationship problem on their hands. The ILPA 2026 Performance Template addresses this directly by providing the cash flow table that allows LPs to replicate the GP's calculation from first principles. When both parties start from the same transaction-level data, the source of any divergence becomes visible immediately rather than requiring weeks of back-and-forth between fund administrators.

What LPs are actually asking for now

The shift in LP performance priorities is measurable, not anecdotal. McKinsey's 2026 Global Private Markets Report found that 2.5 times as many LPs ranked DPI as a most critical metric compared to three years ago. Private Equity International went further, publishing a piece titled "DPI: the three-letter metric that will drive fundraising in 2026." The language is unambiguous.

The reason is structural, not cyclical. Five-year rolling DPI as a share of AUM for buyout funds hit its lowest recorded level in 2025. Distributions as a percentage of AUM fell to approximately 6% in the six months ending June 2025, according to McKinsey's 2026 Global Private Markets Report,, against a ten-year average of 14%. LPs who had been patient through 2022 and 2023, reassured by paper IRRs that looked healthy, found that those IRRs were not converting into actual cash. The metric that was supposed to measure return was measuring something else.

Wrong.

The shift to DPI is not a rejection of IRR as a concept. IRR measures the rate of return on invested capital over time, which is genuinely useful for comparing investments with different timing profiles. The problem is that IRR as reported in PE has accumulated so many discretionary inputs that it has lost much of its comparability. LPs are not saying IRR is useless. They are saying they no longer trust it as a standalone number, and they want cash in hand to confirm the story the IRR is telling.

Return misreporting is also documented in the academic literature. Research using data from the Burgiss database covering 997 buyout funds and 1,074 venture funds found that some underperforming managers manipulate reported returns during fundraising, and that those managers are less likely to raise a next fund. The manipulation is not always intentional. Some is a product of the discretion inherent in the methodology. But the outcome is the same: an LP reading a quarterly report cannot always tell whether the IRR reflects what the fund actually achieved or what the fund chose to report.

What the ILPA 2026 Performance Template actually requires

The Institutional Limited Partners Association released its updated Reporting Template and two Performance Templates in January 2025, following a year-long Quarterly Reporting Standards Initiative (QRSI) that involved extensive consultation with both GPs and LPs. Mandatory adoption applies to new funds from Q1 2026. The first delivery under the new standard occurs in Q1 2027, covering inception-to-date data through March 31, 2027. According to BDO's analysis of the new templates, this represents the most significant update to PE reporting standards in ten years, and it directly addresses the subscription line problem by requiring IRR and TVPI reported both with and without subscription line impact.

The dual disclosure requirement

The core change is structural: every fund-level IRR figure must now be accompanied by the same figure calculated as if no subscription credit facility was used. GPs can no longer report a single IRR without disclosing the subscription line component. For funds where that component is material, the two numbers will diverge visibly, and LPs will know exactly how much of the reported return is attributable to timing rather than investment performance.

The template also introduces a cash flow table that gives LPs the transaction-level data they need to recalculate IRR themselves under their own assumptions. This is significant: LPs have historically had to trust the GP's reported figure because the underlying data was not available. The new template changes that. An LP with a data analyst and access to the cash flow table can verify the GP's calculation, run the alternative methodology scenario, and identify any divergence.

Two methodologies, one standard

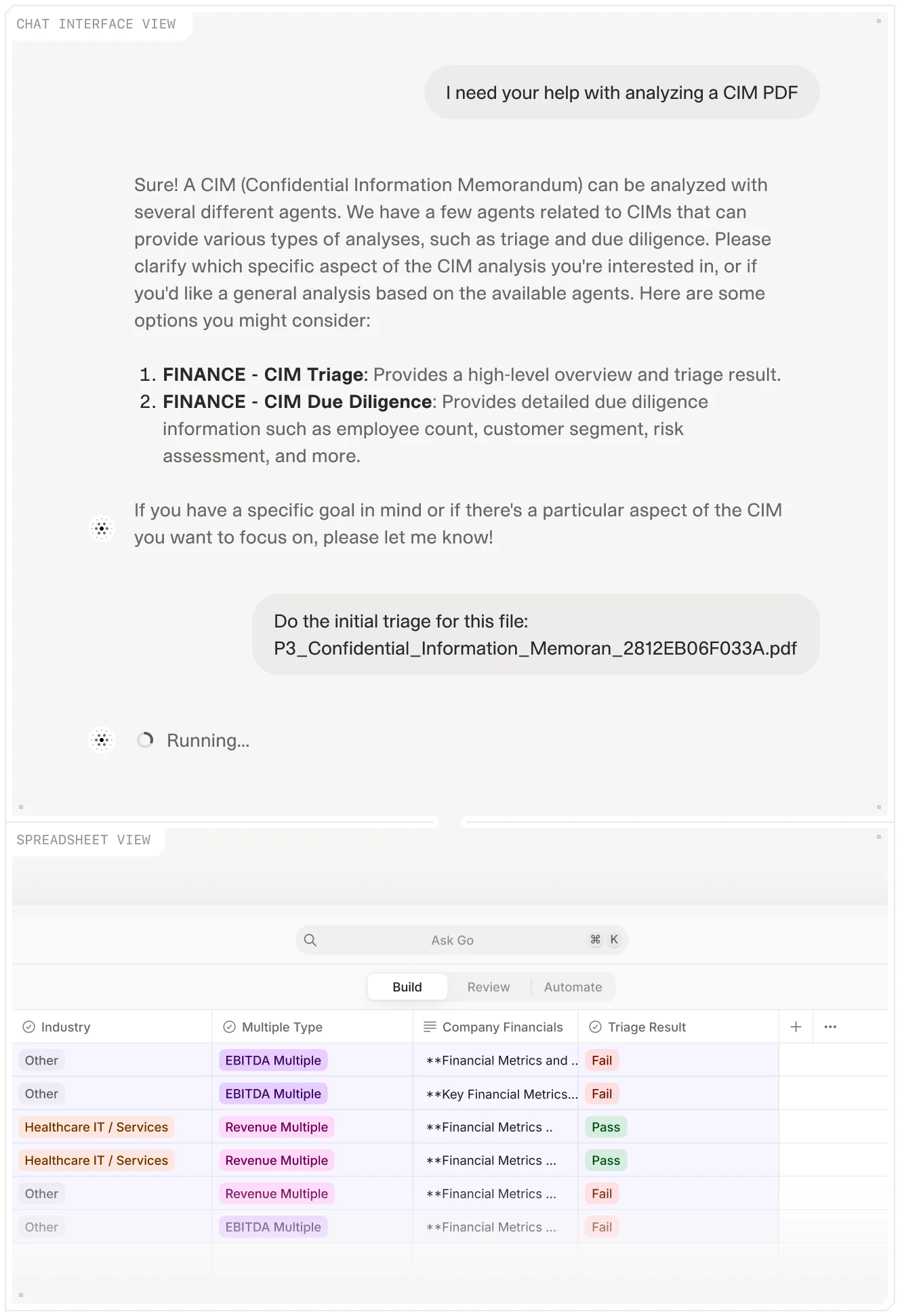

ILPA has published two versions of the Performance Template based on how GPs currently calculate gross fund-level performance. GPs that track capital calls at the transaction level and classify each by funding source use the Granular Methodology. GPs that do not itemize capital calls at that level use the Gross Up Methodology, which produces the subscription-line-adjusted figure through a different calculation path.

The practical implication: GPs on the Granular Methodology path need to classify every capital call transaction by funding source, every subscription line drawdown and repayment, and every capital contribution from LPs. For a fund with 15 portfolio companies over a 10-year life, that is hundreds of individual transactions. Each needs a source classification. Each needs to flow correctly into the performance template. The data work required is substantial, and it starts now for any fund launched after January 1, 2026.

AI agents extract and classify financial transaction data from fund administration records with citations to source documents, which is precisely the transaction-level classification work the ILPA Granular Methodology requires.

Where AI handles the document burden in performance reporting

The ILPA 2026 Performance Template does not require new math. It requires new data discipline: classifying transactions correctly, maintaining the subscription line separation at the individual capital call level, and producing the cash flow table in the standardized format. That is document processing work, and it is exactly where AI agents reduce cost and timeline without changing the judgment calls that GPs still need to make.

Capital call notice classification

The practical challenge for GPs adopting the Granular Methodology is not conceptual. It is a data problem. Each capital call transaction needs a funding source classification: was this capital called from LP commitments, or was it drawn from the subscription credit facility? For a fund with 15 portfolio companies making add-on acquisitions, follow-on investments, and multiple fund closings over a 10-year life, this can amount to hundreds of capital call notices, subscription line drawdown confirmations, and repayment records. Before the ILPA 2026 template, most fund administrators maintained this data somewhere, but not necessarily in a format ready for the performance calculation. The template requirement is forcing GPs and administrators to reconstruct the transaction record in a standardized form, and for older funds that predate the requirement, that reconstruction can be extensive.

Every capital call notice issued by a fund tells a story: which investment triggered it, when it was issued, which LP commitments it drew against, and whether the capital was called directly or preceded by a subscription line drawdown that is being repaid. An AI agent configured for fund administration documents can read a library of capital call notices, extract the key fields from each, and output a structured table that maps each call to its funding source. What a junior analyst would spend two weeks building manually, the agent produces in hours, with citations to the source document for every classification.

The financial statement spreading automation from V7 Go works across fund-level financial statements in the same way: define the extraction schema once, run it across each period's statements, and get a structured output that is ready for the performance template. The human review step is not eliminated. But the input preparation is no longer a weeks-long manual process.

Multi-agent architectures can process fund-level financial records across multiple document types simultaneously, producing the structured data tables that the ILPA Performance Template requires at transaction level.

LP report generation and consistency

Beyond the template itself, the quarterly LP report requires consistency across periods. An IRR figure reported in Q2 2026 needs to reconcile with Q1 2026. The TVPI reported in the performance template needs to match the figure in the narrative section of the investor letter. These consistency checks are easy in principle and time-consuming in practice when the source data sits across multiple systems: the fund administrator's records, the portfolio monitoring system, and the financial model.

An AI agent configured to work across these document sources can flag discrepancies before they reach LP inboxes. The AI due diligence agent handles precisely this kind of cross-document consistency work: extracting figures from multiple sources, comparing them against a reference data set, and surfacing discrepancies with citations to the documents that contain them. Adapted for the LP reporting workflow, the same approach catches the inconsistencies that currently get found by LPs rather than by GPs.

For context on the broader portfolio management and monitoring data challenge that feeds into quarterly reporting, the portfolio monitoring guide covers the full data collection workflow from portfolio company through to fund-level reporting. The quality of quarterly LP reports is largely determined by the quality of data collection that happens in the months before the report is due.

The firms that manage this process well, and arrive at Q1 2027 with a clean cash flow table and a defensible subscription-line-adjusted IRR, will be in a different position than those scrambling to retrofit their records to the new standard after the fact. For a broader look at how AI is applied across finance document workflows, generative AI in finance covers the full landscape of document-intensive use cases.

The reporting credibility question is not going away

The shift from IRR to DPI as the metric LPs care most about reflects something deeper than a preference for cash over paper. It reflects a loss of confidence in reported performance numbers that accumulated through years of methodology discretion, subscription line timing, and inadequate disclosure. LPs are not wrong to want more transparency. The funds that provide it proactively, before they are required to, are building something more durable than a compliance record.

The ILPA 2026 Performance Template moves the floor. Every fund launched from Q1 2026 will report IRR with and without subscription line impact, provide the cash flow table, and use a standardized methodology that makes cross-fund comparison possible for the first time at this level of granularity. LPs will be able to see the subscription line effect directly. The GPs whose reported IRR has historically depended on that effect will face harder questions in the next fundraise.

The preparation work starts now. A fund that begins Q1 2026 with clean transaction-level records, a defined classification methodology, and a document workflow that produces the cash flow table without a manual fire drill is ready. A fund that waits until Q4 2026 to ask what the new template requires will spend its first reporting cycle in catch-up mode.

The GPs who will be best positioned when Q1 2027 delivery arrives are the ones who treated the ILPA template as an operational project starting in 2026, not a reporting exercise starting in 2027. That means confirming now which methodology applies to your fund, mapping the transaction-level data that the template requires, identifying any gaps in how your fund administrator currently captures funding source classification, and building the document workflow that keeps the classification current with each new capital call. For most funds, this is a 90-day project if started early and a six-month recovery if left until the first report is due. The difference shows up in how the LP conversation goes when Q1 2027 arrives: either you deliver a clean template with a clear subscription-line adjustment, or you deliver a delayed report explaining why your systems were not ready.

If the document processing work behind performance reporting is the current constraint, the AI-assisted workflows that are compressing exit preparation timelines apply equally here: structured extraction from capital call notices, subscription line records, and financial statements, with every output cited back to its source document. The math is unchanged. The data preparation does not have to be manual.

What is IRR in private equity?

Internal rate of return (IRR) is the discount rate at which the net present value of a fund's cash flows equals zero. In private equity, it measures the annualized return on invested capital, taking into account both the amount invested and the timing of cash flows in and out. A fund that returns capital quickly will show a higher IRR than a fund that takes longer to return the same total amount, even if both return identical multiples on capital. This time-sensitivity is IRR's core feature and its core weakness: it can be influenced by anything that changes the timing of cash flows, including subscription credit facilities that delay when LP capital is actually deployed. Fund-level IRR is typically reported on a gross basis (before management fees and carried interest) and a net basis (after fees and carry). Gross IRR reflects investment performance; net IRR reflects what LPs actually receive. The gap between them is a meaningful data point about fee and carry structures.

+

How do subscription credit lines affect reported IRR?

Subscription credit lines, also called capital call facilities, allow GPs to borrow against LP commitments rather than drawing capital directly when making investments. When a GP uses a subscription line to fund an investment in, say, January, and then calls LP capital to repay the facility in June, the LP's measured investment period begins in June rather than January. Because IRR is time-sensitive, a shorter investment duration on the same cash return produces a higher reported IRR. The effect can add several percentage points to the reported fund-level figure compared to what would have been reported if capital had been called directly. This is not fraudulent; the calculation is mathematically accurate under the chosen timing convention. The problem is that it makes comparison across funds unreliable when some funds use subscription lines extensively and others do not. The ILPA 2026 Performance Template addresses this directly by requiring GPs to report IRR both with and without the subscription line impact, giving LPs visibility into the timing contribution for the first time at a standardized level.

+

What is DPI and why are LPs shifting to it?

Distributions to paid-in capital (DPI) measures the total cash returned to LPs as a multiple of the capital they invested. A fund with a DPI of 1.5x has returned one and a half times the total capital called. Unlike IRR, DPI is not time-sensitive: it measures actual cash received, not the rate at which it was received. LPs are shifting emphasis to DPI because the extended hold period environment since 2022 revealed that many funds with attractive reported IRRs were not generating proportionate distributions. IRR can look healthy while actual cash returned to investors is low if exits are delayed or if subscription line timing inflated the measured rate. McKinsey's 2026 Global Private Markets Survey found that 2.5 times as many LPs ranked DPI as their most critical performance metric compared to three years prior. DPI is a harder number to massage: the money either came back or it did not. For LPs managing liquidity needs and re-up decisions for successor funds, actual distributions matter more than the theoretical rate at which they were generated.

+

What does the ILPA 2026 Performance Template require?

The ILPA 2026 Performance Template, released in January 2025 and effective for funds launched from Q1 2026, requires GPs to report fund-level performance with several new disclosures that were not standardized before. The core additions are: gross and net IRR reported both with and without subscription line impact; a cash flow table providing transaction-level data that allows LPs to recalculate performance under their own assumptions; standardized metrics including TVPI, DPI, and RVPI alongside IRR; and a fund-level transaction type mapping table that makes calculation methodology transparent. ILPA has published two versions of the Performance Template: the Granular Methodology for GPs that track capital call funding sources at the transaction level, and the Gross Up Methodology for GPs that do not. The first delivery under the new standard occurs in Q1 2027, covering inception-to-date data through March 31, 2027. The templates are designed to become the de facto industry standard and are already being adopted voluntarily by many GPs ahead of the formal requirement.

+

What is the difference between gross IRR and net IRR in private equity?

AI agents address the most time-consuming data preparation work behind PE performance reporting without changing the judgment calls that GPs need to make on methodology and disclosure. The ILPA 2026 Granular Methodology requires classifying every capital call transaction by funding source at the individual transaction level, which means reading capital call notices, subscription line agreements, and fund administration records to determine which draws came from LP capital and which came from credit facility drawdowns. An AI agent configured for these document types can work through a fund's full transaction history, extract the relevant fields from each document, and produce a structured classification table with citations to the source records. This is the same extraction workflow that takes analysts weeks when done manually. Beyond transaction classification, AI agents can run consistency checks across the quarterly report: comparing the IRR figure in the performance template against the narrative letter, flagging discrepancies between the current report and the prior quarter, and identifying any missing required fields in the ILPA template before the report is sent to LPs. These are mechanical checks, but they are the ones that currently get found by LP administrators rather than by the GP's own review process.

+

How can AI help with private equity performance reporting?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.