AI implementation

18 min read

—

The version of LP due diligence that most GPs prepare for is not quite the version that most LPs actually run.

GP fundraising advisers coach their clients to prepare polished management presentations, anticipate questions about performance attribution, and rehearse answers about key person succession. This preparation is not wasted. But it addresses the visible portion of the process: the meetings, the formal Q&A, the data room review. The more consequential evaluation happens in the weeks before and after those meetings, in conversations the GP never participates in.

LP due diligence on GPs in 2026 is more structured than it was a decade ago, more data-intensive, and more likely to surface problems that a well-rehearsed management presentation cannot paper over. The ILPA DDQ 2.0, updated in November 2021, gave LPs a standardized framework covering strategy, track record, team composition, fund economics, and operational infrastructure. Most institutional LPs now use some version of it as a baseline. The questions it asks are not easy to answer with marketing language.

This article covers the actual mechanics: how long the process takes, what each workstream examines, where track records get stress-tested, who LPs call and what they ask, and why operational due diligence has become a silent disqualifier for managers who cannot demonstrate institutional-grade infrastructure. It also covers where AI document analysis has begun to change the process on both sides of the table.

How LP due diligence is structured across investment, organizational, and operational workstreams

Why performance persistence data should make GPs skeptical of their own track record narrative

Who LPs actually call during reference checks, and the four questions that matter most

How key person risk is evaluated as an underwriting question, not a contract clause

How AI document analysis is changing LP diligence workflows and GP preparation

AI for document processing

Automate the document review LPs actually do

Get started today

How LP due diligence on GPs is structured

The pre-commitment phase of LP fund due diligence runs four to twelve weeks for most institutional investors, though the range is wider in practice. Endowments and pension funds often run processes lasting six to eighteen months, particularly for first-time commitments to a manager. Fund-of-funds operate on three to six month timelines. Family offices range from two weeks to twelve months depending on their internal resources and the relationship history with the GP.

Within any of those windows, the process follows a consistent structure: the LP initiates contact or receives an introduction, requests and reviews a DDQ or data room, conducts a management presentation and written follow-up, runs reference calls in parallel with legal review of the limited partnership agreement, and submits the completed analysis to an investment committee for approval. These phases are sequential but often overlap, with reference calls beginning while LPA review is still in progress.

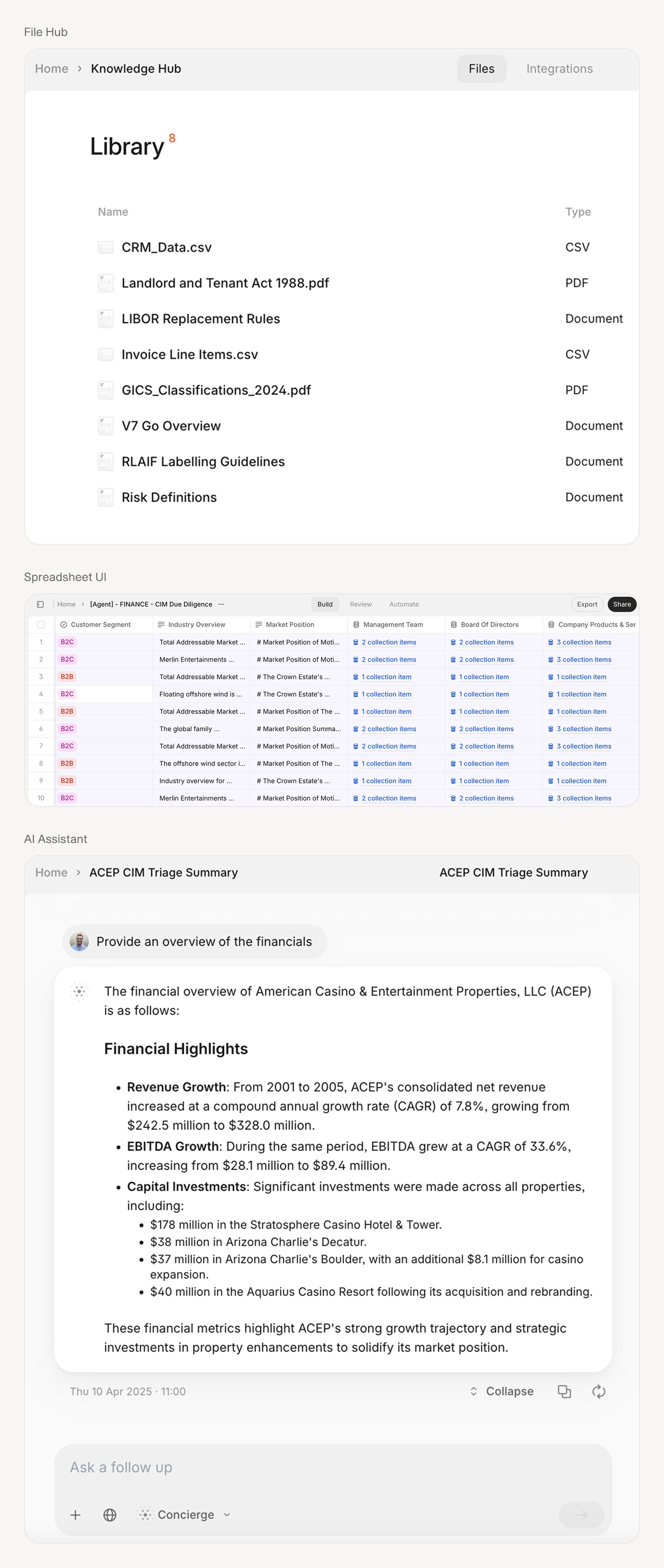

AI tools now sit inside LP data room workflows, surfacing structured summaries from financial documents during fund manager evaluation.

Investment due diligence

Investment due diligence covers the GP's strategy, track record, and deal-sourcing capability. LPs evaluate whether the fund's stated strategy is specific enough to be testable. "We invest in lower middle market healthcare services businesses with 5 USD to 15 million USD EBITDA" is testable; "We invest in high-quality companies with strong management teams" is not. They examine whether the historical portfolio reflects the current strategy, or whether it reflects a different strategy now being reframed retroactively.

Track record review focuses on consistency. LPs look for evidence that strong returns were generated by the same team, in the same market segment, using a repeatable investment thesis, not by one exceptional investment that carried the fund. The full mechanics of LP-side fund due diligence involve verifying the headline figures and the deal-level attribution underneath them.

Market conditions matter. The parameters underlying a track record may have changed since those investments were made: fund size has grown, the competitive landscape has shifted, the sector dynamics that created the original opportunity may no longer exist. LPs are expected to take the standard disclaimer ("past performance is not an indicator of future results") at face value and ask specifically what has and has not changed since the predecessor fund was deployed.

Organizational and people diligence

Organizational diligence addresses the question LPs are most reluctant to ask directly: what happens to this fund if the person who built the track record leaves? The 2021 ILPA DDQ 2.0 includes dedicated questions about team composition, tenure, how investment responsibilities are divided among partners, and what succession arrangements exist. LPs want to know how long the current team has worked together, whether investment decisions require consensus or can be driven by a single individual, and how carry is allocated across the team.

The concern is structural. A fund manager whose carry is entirely top-loaded to a single founding partner creates a retention risk for everyone below. An investment process that depends on one person's relationships for deal sourcing creates a concentration risk for the portfolio. In 2025, 18% of funds saw LPs exercise governance rights including key-man provisions and no-fault divorce clauses, a figure that reflects both the frequency of team disruption and the willingness of LPs to act on it when it occurs.

LPs also examine how a firm has handled personnel changes historically. If partners have left, LPs want a factual account: when they left, whether it was voluntary, and how existing portfolio companies were managed through the transition. GPs who describe every departure as a positive development invite skepticism. LPs do not require clean records. They require honest records.

Operational due diligence

Operational due diligence (ODD) has expanded substantially over the past decade, driven partly by post-crisis fraud cases and partly by the SEC's ongoing focus on fee calculation, expense allocation, and conflict-of-interest disclosure. By 2024, 79% of institutional LPs reported deepening their operational scrutiny compared to prior years.

ODD covers governance, compliance infrastructure, cybersecurity, valuation policies, fund administration, and the adequacy of controls around cash and asset management. Specifically, LPs want to understand who controls access to fund assets (cash, securities, credit facilities), whether the GP uses an independent fund administrator, and how valuation decisions for illiquid assets are made and documented. The SEC has flagged valuation methodology as a priority examination area for 2025 and 2026, particularly for managers with commercial real estate, private credit, or other hard-to-mark asset exposures.

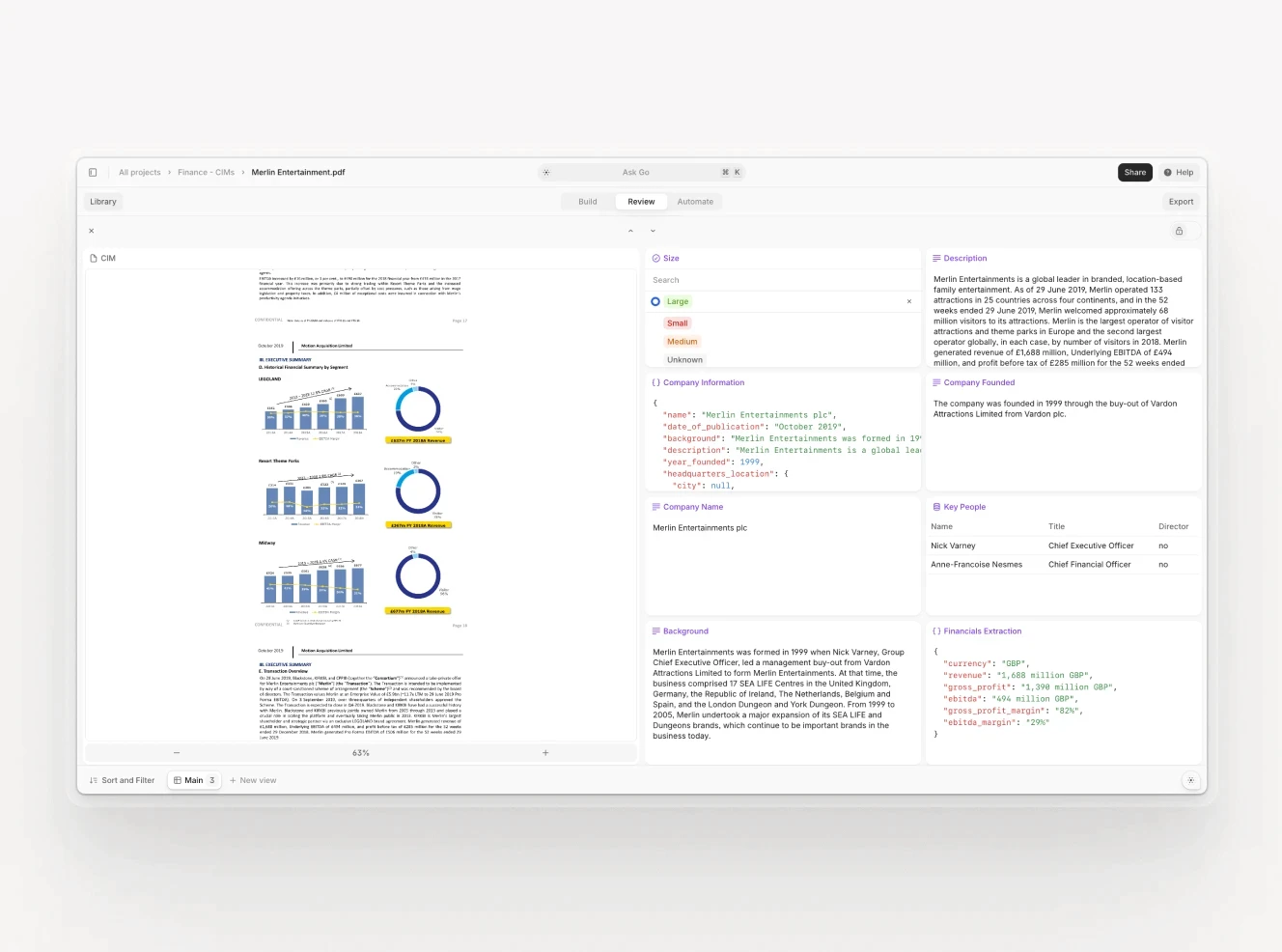

Document intelligence tools extract structured compliance and financial data directly from LP due diligence packages, reducing manual review time during ODD workstreams.

GPs who have already conducted third-party ODD reviews are better positioned to answer LP queries quickly and completely. The review is about demonstrating that the organization has thought carefully about non-investment risks and established procedures that would survive the departure of any single individual.

The ILPA DDQ as an organizational map

The ILPA DDQ 2.0, finalized in November 2021 after a public comment period and working group review, is the closest thing private markets has to a standardized diligence curriculum. It covers fifteen major topic areas: firm overview, investment strategy, deal sourcing and pipeline, investment decision-making, portfolio management, ESG integration, team and governance, fund economics, co-investment policy, fund terms, track record (including a comparison of LP returns with and without subscription credit facilities), regulatory compliance, operational infrastructure, reporting, and diversity metrics.

The DDQ is not a questionnaire LPs fill out on behalf of GPs. It is a structured request for information that GPs complete and that LPs use to anchor their analysis. Institutional LPs often maintain a master version with annotations from previous GP submissions, which allows them to compare how different managers answered the same questions. A vague answer to a clear DDQ question is itself a data point.

For GPs raising a first fund, the DDQ presents a particular challenge. There is no predecessor fund track record to point to, no portfolio company references from current investments, and limited institutional name recognition. The LP-side diligence process for first-time GPs places proportionally more weight on the principals' prior attribution records, the soundness of the investment philosophy relative to current market conditions, and the quality of the service providers (administrator, auditor, legal counsel) the GP has engaged. Backing from a credentialed anchor investor, such as a major endowment or institutional fund-of-funds, carries more weight than the GP's own assessment of its strategy.

What track record review actually uncovers

Most GPs enter LP meetings believing their track record is their strongest asset. It often is. But the way LPs evaluate that track record is not the same as the way the GP presents it, and the gaps between those two interpretations are where allocations are lost.

The first question is attribution. For multi-partner firms, LPs want to know which partners sourced, underwrote, and managed each investment. They want a deal-by-deal account: sourcing role, investment thesis at entry, how the thesis evolved during the holding period, and the realized outcome. They are not interested in anecdotes about how the team "worked together" on every deal. That framing is precisely what makes attribution analysis difficult. When a firm's best-performing vintage was led by a partner who has since left, the track record does not transfer.

For buyout funds, academic research on performance persistence offers a sobering baseline. Post-2000 data shows "little or no evidence" of persistence at the time of fundraising, meaning that a GP's prior fund quartile ranking has limited predictive value for the next fund. Only bottom-quartile persistence remained statistically significant, which is a polite way of saying that bad managers tend to remain bad. LPs who understand this use track records as one input among several rather than as a primary decision criterion.

The second question is the interim fund warning. Research on private capital markets has found that the interim results of a predecessor fund (the valuations showing in the portfolio when the next fund is being raised) have very little predictive value for final outcomes. Unrealized marks can be written up or down with considerable discretion under current accounting standards, and GPs who raise successor funds while their prior fund is still in the holding phase have an obvious incentive to maintain optimistic interim valuations. LPs who have experienced this dynamic discount interim marks significantly and focus on realized multiple and DPI from fully or nearly fully liquidated positions.

The third question is scale. A GP that generated 25% net IRR deploying 200 million USD is not necessarily capable of generating the same return deploying USD 800 million. Deal size increases, competitive dynamics change, and the sector coverage required to find enough qualified investments at larger fund sizes is different in kind, not merely in degree. LPs ask explicitly: how will your strategy change at this fund size? What is the largest single investment you anticipate making, and how does that compare to the largest investment in the predecessor fund?

LP diligence workstreams increasingly use AI to process and compare track record data, LPA provisions, and DDQ responses across multiple manager submissions simultaneously.

Reference calls: who LPs actually contact

The reference call process is the part of LP due diligence most GPs manage least effectively. This is partly because GPs do not control it, and partly because they underestimate the range of people LPs contact.

LPs draw references from six sources: current and previous LPs who have committed to prior funds; senior leadership of portfolio companies, both current and exited; investors who were presented with the fund opportunity and chose not to commit; service providers including administrators, auditors, and outside counsel; background checks on unknown service providers; and past employees of the GP firm. That last category is the one most GPs overlook. A former associate who left the firm two years ago and is now at a different shop is likely to give a candid account of investment process quality, team dynamics, and how the GP actually behaved with portfolio companies under stress.

LPs also use their networks to identify references the GP did not provide. They ask their own contacts in the industry who else has worked with or evaluated this manager. Those second-degree references are often more candid than the references GPs submit directly, for an obvious reason: they have not been pre-selected for their willingness to say positive things.

The questions asked on reference calls follow a consistent pattern. Does the GP's reporting quality and frequency match the commitments made during fundraising? Has there been any situation where GP and LP interests diverged, and how did the GP handle it? Has the GP requested any amendments to the LPA since closing, and what were the circumstances? Would the LP commit to a successor fund from this manager, and why or why not?

That fourth question is the most informative. An LP who says they would re-up but cannot articulate a clear reason is giving a different signal than one who says they would re-up and explains why their experience matched expectations in three specific ways. An LP who declines to answer, or who becomes evasive, is giving the clearest signal of all.

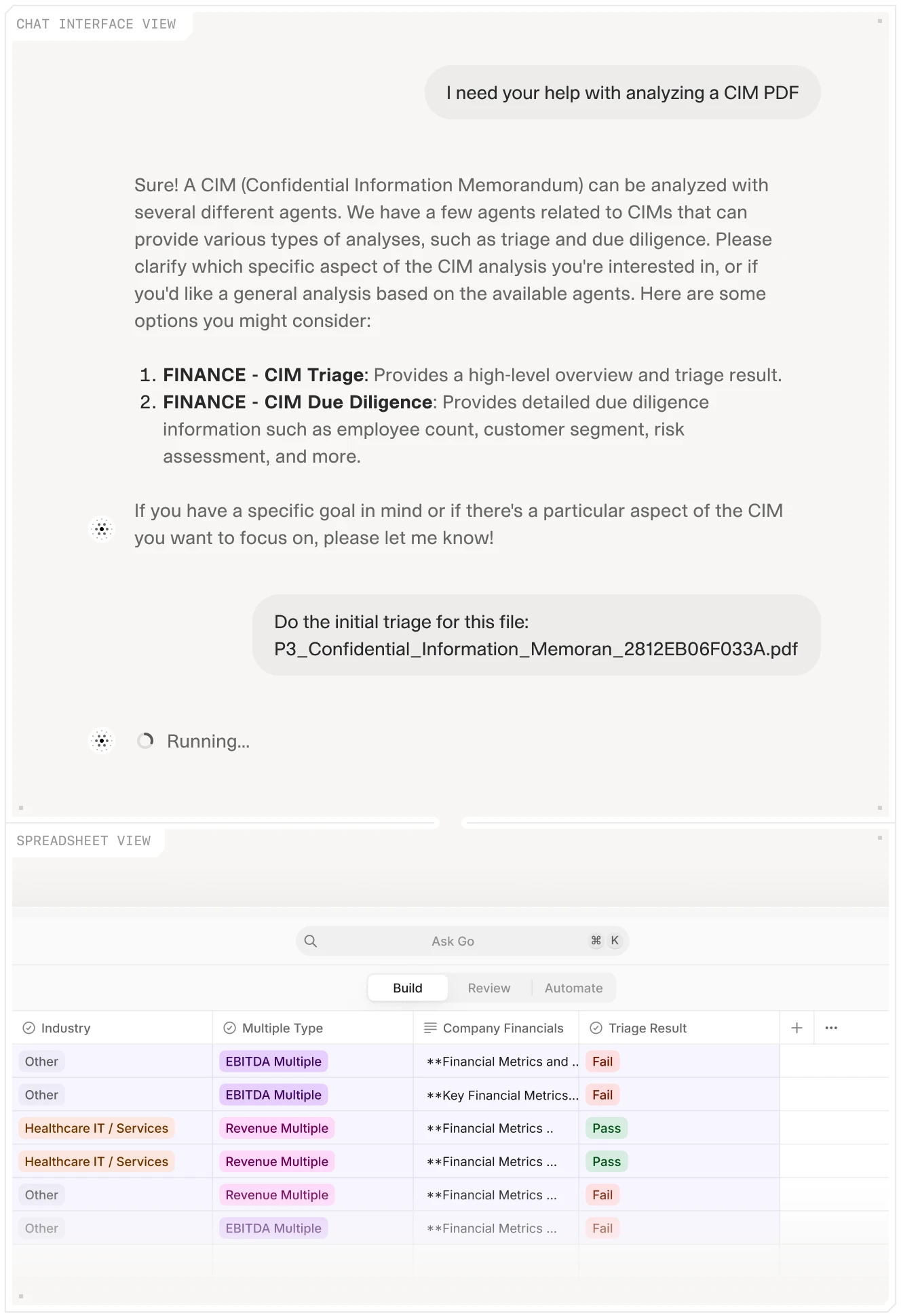

The AI due diligence agent structures document review outputs into consistent formats, allowing LP teams to compare GP responses and financial data across multiple fund submissions in the same analytical framework.

Key person risk as an underwriting question, not a contract clause

Every fund LP agreement includes key person provisions: if a defined set of senior investment professionals devote less than a specified percentage of their time to the fund, LP rights are triggered. This clause is standard. What is less standard is the rigor with which LPs think through key person risk before making a commitment, as opposed to relying on the clause to protect them after a problem arises.

In practice, LPs treat key person evaluation as a qualitative underwriting question. They want to know whether the firm's investment process is person-dependent or system-dependent. A firm that sources deals through one partner's relationships, underwrites through another's judgment, and manages portfolio companies through a third's operational instincts has concentrated risk in three individuals. A firm with documented investment processes, shared deal coverage, and an associate class that has been promoted to principal roles has distributed that risk across a larger organization.

The alignment question reinforces this. The average GP commitment to a fund is 4.8% of fund size, according to a 2021 survey of 219 general partners. First-time managers often exceed this, contributing more than the requirement as a signal of conviction. But the distribution of that commitment within the partnership matters as much as the total. If one founding partner holds 90% of the GP commitment and the rest of the team holds 10% combined, the retention incentive structure for non-founding partners is weak, and the key person risk is concentrated regardless of what the LPA says about it.

LPs who discover that key person definitions in the LPA are narrow, covering only the founding partner rather than the broader investment team, sometimes negotiate expanded definitions during LPA review. This negotiation, combined with management fee offsets and LPAC representation, represents the governance lever LPs can pull before the relationship begins. The no-fault divorce provisions that 18% of funds saw exercised in 2025 represent what happens when those levers were not sufficient.

Fund economics: when management fees signal misalignment

The standard private equity fee structure (2% management fee, 20% carried interest above an 8% preferred return) is a starting point, not a norm. LPs evaluate fund economics for their absolute terms and for what they reveal about the GP's incentive structure and financial dependence on the fund.

The concern with management fees is not that they exist. They exist to cover the operating costs of running the fund: salaries, office expenses, travel, legal, and administrative overhead. The concern is when management fees substantially exceed those costs, which turns the fee structure into a profit center in its own right. A GP that is comfortable generating significant income from fee streams regardless of investment performance has a weaker incentive to prioritize carried interest, which is the alignment mechanism the whole structure is supposed to depend on.

LPs who are examining a larger fund from a manager that previously ran a smaller fund look at this question carefully. As fund size grows, management fee revenue grows proportionally, while the cost of running the fund grows less than proportionally. The economics improve significantly for the GP. Whether those improved economics come at the expense of LP alignment depends on whether the carry structure has been updated to reflect the changed economics, and whether the team that will earn that carry is the same team that built the prior track record.

Some LPs are open to non-standard economics when they believe superior results justify them: a higher carry share in exchange for a lower management fee, or back-ended management fees that increase only after a certain deployment threshold. What raises flags is when economics are non-standard in the GP's favor without a corresponding explanation of what the LP receives in exchange.

How AI document analysis is changing LP due diligence

The ILPA DDQ 2.0 alone runs to 75 pages in its complete form. Add a fund prospectus, a track record document, five years of audited financial statements, and a draft LPA, and an LP is managing several hundred pages of structured and semi-structured text before the first management presentation. The information is present. Extracting it consistently, and making it comparable across multiple GP submissions being reviewed simultaneously, is where AI document tools have begun to change the workflow.

The LPA analysis use case is illustrative. LP legal teams traditionally review limited partnership agreements manually, flagging provisions that deviate from market standard: key person definitions, LPAC composition, no-fault divorce thresholds, management fee offsets, and waterfall structures. An AI LPA analysis agent can run that review against a defined extraction schema, surfacing the specific clause language for each defined provision, flagging deviations from the LP's preferred terms, and producing a structured comparison across multiple LPA submissions. The human lawyer still makes the judgment about whether to negotiate; the AI compresses the time required to understand what is in front of them.

Track record document review follows the same pattern. A GP submits a track record in a format that reflects their own preferences: which investment to present first, how to define the relevant universe, how to handle the fund that underperformed. The LP receives it in whatever form the GP chose. An AI extraction agent applies a consistent schema across all GP track record submissions: realized and unrealized IRR, MOIC, DPI, holding period, deal size, and whether realized investments account for more or less than half the total capital deployed. The schema does not eliminate judgment. It ensures the comparison is made on equivalent terms.

AI document tools applied to LP due diligence reduce the time-to-insight gap between receiving a GP submission and completing structured analysis across investment, organizational, and operational workstreams.

For GPs, the operational implication runs in the other direction. If LPs are applying extraction schemas to DDQ submissions and track record documents, the quality of structured data in those documents becomes more consequential. A DDQ completed with consistent formatting, precise figure conventions, and unambiguous answer structures will fare better in an automated extraction workflow than one built around narrative paragraphs that require manual interpretation. This is an argument for GPs to think about their submission documents not only as investor communication but as machine-readable data.

The AI due diligence agent supports both sides of this workflow: LPs using it to process GP submissions at scale, and GPs using it to review their own documents before submission, identifying where structured data is missing or where claims require clearer evidence. The role of AI in due diligence is not to replace the judgment calls that determine whether to allocate. It is to ensure those judgment calls are made on the basis of complete, consistently extracted information rather than on whatever the GP chose to highlight and whatever the LP's analyst happened to notice.

What LPs are asking that they were not asking five years ago

The questions LPs ask today reflect regulatory changes, structural shifts in private markets, and a decade of lived experience with what actually goes wrong in GP-LP relationships.

On the regulatory side: the SEC's 2026 examination priorities explicitly include valuation methodology for illiquid assets, management fee calculation and offset practices, and disclosure of conflicts around fund-level credit lines, adviser-led secondaries, and affiliated service providers. LPs now ask GPs directly: have you been subject to an SEC examination in the last five years? What was the scope? Were there any deficiency letters? These questions used to feel aggressive. They now feel standard.

On the structural side: subscription credit lines have become common, and LPs have become more sophisticated about their effect on reported IRR. The ILPA DDQ 2.0 updated Section 14.0 to require GPs to report track record returns both with and without the effect of subscription credit facilities. LPs who receive only the facility-inclusive figures now ask for the gross-up explicitly. A fund that reports 28% IRR with a credit line and 21% IRR without it is not necessarily misrepresenting its performance, but an LP who allocates based on the 28% figure without understanding the difference has made a more leveraged bet than they may have intended.

On operational infrastructure: ESG integration questions have migrated from optional addendum to core DDQ. Over 65% of new institutional commitments in 2024 required ESG reporting as a condition of investment. LPs ask whether a GP has an ESG policy and whether ESG considerations are integrated into investment screening, and whether portfolio company reporting includes quantitative environmental and social metrics. GPs without processes to support those commitments face follow-up questions they cannot answer with a policy document.

The cumulative effect of these additions is that LP due diligence now covers ground that investment-focused GPs did not historically think of as diligence territory. A buyout manager who has spent thirty years thinking about investment strategy and deal execution may be less prepared to discuss cybersecurity incident response protocols or attribution methodology than they are to discuss market entry multiples. That gap is exactly what thorough LP due diligence is designed to find.

What thorough preparation actually signals

GPs who go through a rigorous LP due diligence process and come out with a committed anchor investor have learned something useful about their own organization. The process surfaces gaps in documentation, inconsistencies in how different team members describe the investment strategy, and areas where the operational infrastructure does not yet match institutional expectations.

The GPs who find these gaps early are better positioned than those who discover them when an LP declines to re-up. That outcome rarely comes with detailed feedback. The LP closes the process politely, attributes the decision to portfolio construction considerations, and moves on. The GP is left without a clear understanding of what failed the review.

AI document analysis tools support GP preparation in the same way they support LP review. An LPA analysis agent applied to a draft fund agreement before it goes to LP counsel surfaces the same issues that LP counsel will eventually flag: key person clause scope, management fee offset mechanics, LPAC rights. Weeks earlier in the process. A due diligence agent run against a draft DDQ identifies where answers are vague, where data is missing, and where a pattern emerges that an LP will notice and follow up on.

The reference call process cannot be prepared for in the same way. LPs will call people the GP did not suggest, ask questions the GP did not anticipate, and draw conclusions from the texture of the conversation as much as its content. What GPs can control is the actual record: whether reporting was consistent with promises made during fundraising, whether LP interests were respected when they diverged from GP interests, whether the organization responded to personnel changes in a way that protected the fund. Those are operational outcomes, not presentation outcomes. They are what LP due diligence is designed to evaluate.

The firms that build strong LP relationships over multiple fund cycles are not the ones with the best-rehearsed management presentations. They are the ones whose organizational records, when examined by a thorough LP, say what the GP said they would say.

What is LP due diligence on GPs?

LP due diligence on GPs is the process institutional investors use to evaluate a fund manager before committing capital to a new fund. It covers three main workstreams: investment due diligence (strategy, track record, deal sourcing), organizational diligence (team composition, key person risk, succession planning, carry allocation), and operational due diligence (governance, compliance, fund administration, valuation policies, cybersecurity). The process typically runs four to twelve weeks for most institutional investors, though endowments and pension funds often conduct reviews lasting six to eighteen months. Most institutional LPs use the ILPA DDQ 2.0 as a baseline framework for structuring their information requests. The process includes management presentations and written Q&A, reference calls with current and former LPs, portfolio company leadership, and past employees of the GP firm, as well as legal review of the limited partnership agreement.

+

How long does LP due diligence on a GP typically take?

LP due diligence timelines vary significantly by investor type. Endowments and pension funds typically run processes lasting six to eighteen months, reflecting their larger team resource constraints and more rigorous governance requirements. Fund-of-funds operate on three to six month timelines. Family offices range from two weeks to twelve months depending on their internal staffing and prior relationship with the manager. RIAs and OCIOs typically run three to six month processes. The formal stages within any of these windows follow a consistent sequence: initial screening and DDQ review (one to two weeks), management presentation and written follow-up (one to two weeks), reference calls with existing LPs and portfolio company contacts (one to two weeks), LPA review and negotiation (two to four weeks, often running in parallel with other stages), and investment committee preparation and approval (one to two weeks). First-time commitments to a GP typically take longer than re-up decisions, as LPs have no prior fund history to anchor the evaluation.

+

What do LPs look for when reviewing a GP's track record?

LPs evaluate track records along three dimensions beyond headline IRR and MOIC. First, attribution: they want deal-level attribution showing which partner sourced, underwrote, and managed each investment, with a clear account of the realized outcome. A fund-level return generated by one exceptional investment does not demonstrate repeatable skill in the same way that consistent returns across a diversified portfolio does. Second, context: the conditions that produced a track record may not persist, so LPs examine how much of the return was attributable to sector tailwinds, financial leverage, or market conditions that no longer exist. Third, scale: a strategy that worked at USD 200 million in fund size may not transfer to USD 800 million, as deal size requirements, competitive dynamics, and portfolio construction all change. LPs also require track record reporting with and without subscription credit facility effects, following the ILPA DDQ 2.0 update to Section 14.0, because credit lines can significantly inflate reported IRR relative to the underlying investment performance.

+

What questions do LPs ask during GP reference calls?

LP reference calls typically cover four core questions, though the specific framing varies by investor. The first is whether the GP's reporting quality and frequency matched the commitments made during fundraising. A GP who promises quarterly updates and delivers annual ones has established a pattern that LPs in the current fund will also experience. The second is whether there have been situations where GP and LP interests diverged, and how the GP handled them. Alignment of interests is easy to claim; behavior under pressure reveals it. The third is whether the GP requested any amendments to the LPA after closing, and what the circumstances were. Amendments are not automatically negative, but the process by which they were obtained and the reasons behind them are informative. The fourth, and most revealing, is whether the LP would commit to a successor fund from this manager and why. Beyond the provided reference list, LPs also conduct off-list calls with former employees, investors who considered the fund but did not commit, and industry contacts who have observed the GP in other contexts.

+

What is operational due diligence in private equity?

The ILPA DDQ 2.0, finalized in November 2021, provides a standardized framework for LP due diligence on GPs that covers fifteen major topic areas: firm overview, investment strategy, deal sourcing and pipeline, investment decision-making, portfolio management, ESG integration, team and governance, fund economics, co-investment policy, fund terms, track record (including returns with and without subscription credit facility effects), regulatory compliance, operational infrastructure, reporting standards, and diversity metrics. Most institutional LPs now use some version of the DDQ as a baseline for structuring their information requests, which means GPs can anticipate the scope of diligence questions even before a formal process begins. The DDQ is designed to be completed by the GP and reviewed by the LP, allowing LPs who manage multiple simultaneous manager reviews to compare responses across standardized fields rather than evaluating each submission on its own terms. The complete DDQ is publicly available through the Institutional Limited Partners Association at ilpa.org.

+

How does the ILPA DDQ structure LP due diligence?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.