23 min read

—

Most institutional LP programs have a private equity fund due diligence process. Documents get requested, track records get reviewed, reference calls get scheduled, and investment committee memos get written. The process exists. It is documented. It is followed.

That is a description of a process. It is not a discipline.

The distinction matters because the process almost always ends at commitment. The LP wires the capital, signs the subscription agreement, and files the LPA. At that point, a fund that will run for ten years or more disappears into a quarterly reporting cycle, a sequence of PDFs that arrive every three months and receive, at most, a brief scan. The MOIC figures get logged. The portfolio company names get noted. The LP moves on to the next due diligence task.

The problem is that the signal is in those quarterly reports. NAV marks that have not moved in three consecutive quarters. A portfolio company that has advanced from Series B to "early stage" in the LP's internal tracking, which means it has been marked down. A capital call pace that has slowed from $8M per quarter to $2M, with no GP explanation. A due diligence process built around AI-assisted document analysis catches these patterns across a fund portfolio without requiring someone to spend three hours per fund per quarter. Without one, the first time an LP finds out a fund is in trouble is when the GP calls to discuss a continuation vehicle.

This guide covers both halves of private equity fund due diligence, the pre-commitment evaluation phase that most LP programs run adequately, and the post-commitment monitoring phase that most LP programs run poorly or not at all.

In this article:

What private equity fund due diligence is and who runs it

The five dimensions of fund evaluation: strategy, track record, team, economics, and operations

The documents in a complete fund due diligence package

Post-commitment monitoring: what to track and why it is the neglected half

How AI changes the document extraction and analysis workflow for LP teams

AI for document processing

Run fund due diligence without the manual grind

Get started today

What is private equity fund due diligence: and who runs it

The phrase "private equity due diligence" covers two distinct activities that the industry often conflates. The first is what a GP does when evaluating a company it is considering acquiring, commercial due diligence, financial due diligence, legal review of the target. This is GP-side diligence on a portfolio company, and it is what most general guides on "PE due diligence" describe.

The second is what an LP does when evaluating a PE fund manager before committing capital, reviewing the GP's track record, investment strategy, organizational structure, fee terms, and operational infrastructure. This is LP-side fund due diligence, and it is a fundamentally different exercise. The LP is not buying a company. They are selecting a manager to whom they will give discretionary control over capital for the next decade.

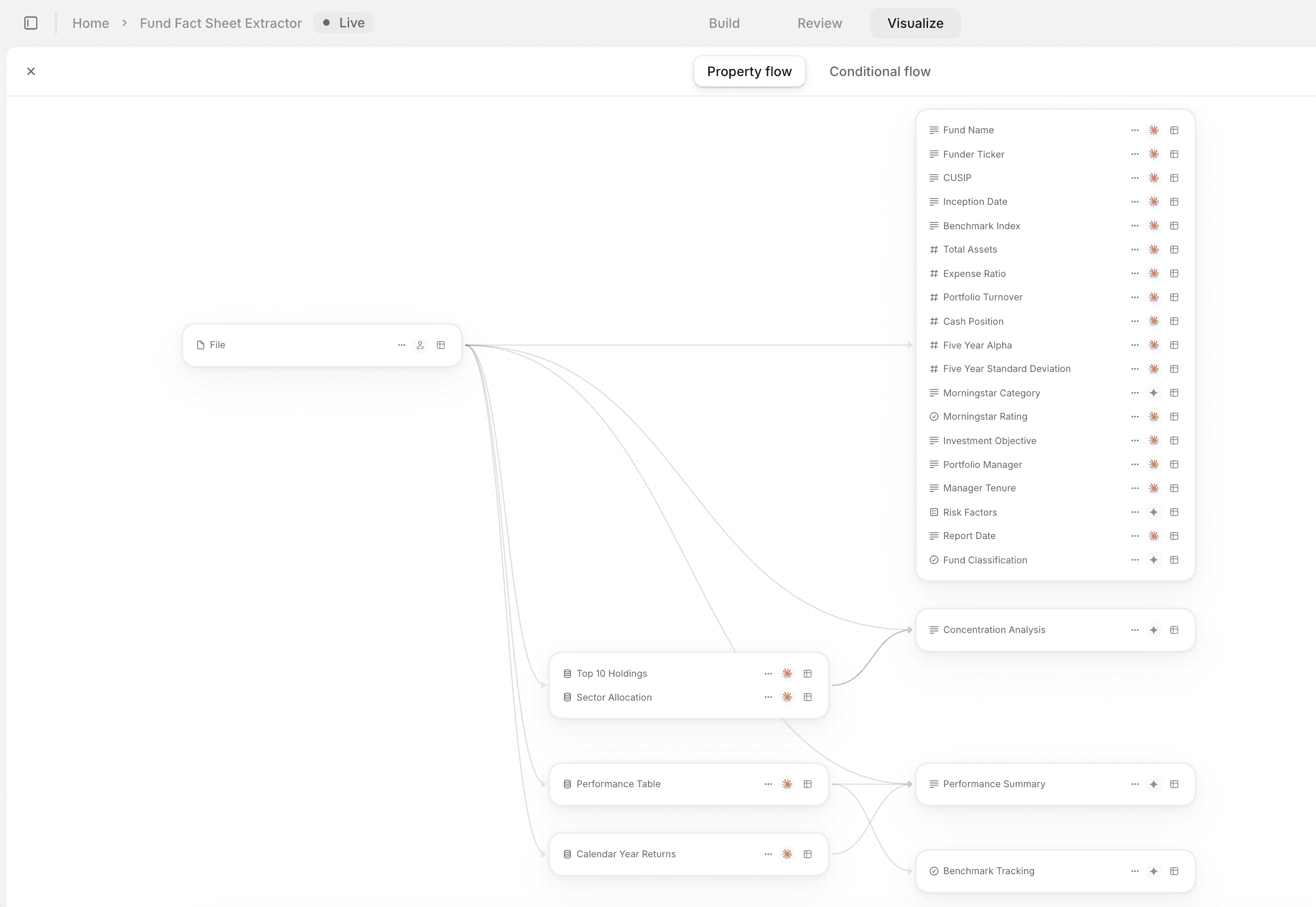

The AI Fund Fact Sheet Extractor schema: one fact sheet PDF maps to 19 structured fields and four nested sub-tables.

LP-side fund due diligence is conducted by institutional investors, pension funds, endowments, sovereign wealth funds, insurance companies, family offices, and fund of funds, that allocate capital to external PE managers. Gatekeepers and investment consultants also conduct it on behalf of smaller institutional investors that lack in-house PE teams.

The process has two distinct phases:

Pre-commitment evaluation happens before the LP decides whether to invest. It covers the GP's investment strategy, team, track record, fund economics, and operational infrastructure. This phase typically runs four to twelve weeks, involves a DDQ, one or more management presentations, reference calls with existing LPs, and legal review of the LPA. The outcome is an investment committee decision to commit or pass.

Post-commitment monitoring begins after the LP has committed capital and continues for the fund's entire life, often ten to fourteen years for buyout funds with extensions. It involves reviewing quarterly reports, audited financial statements, capital call notices, distribution notices, LPAC materials, and any interim communications from the GP. The outcome is an ongoing view of how the fund is performing against the assumptions made at commitment, and early identification of problems before they become losses.

Most LP programs run the pre-commitment phase with reasonable discipline. The monitoring phase is where execution breaks down. The volume is high, an LP with a $1B program invested across fifteen to twenty funds receives at least sixty to eighty quarterly reports per year, and the documents are dense, inconsistent in format, and easy to treat as record-keeping rather than analysis.

The five dimensions of private equity fund due diligence

A structured fund evaluation covers five areas: investment strategy, track record, team, fund economics, and operational infrastructure. Each has standard questions. The harder work is knowing which answers to probe and what the evasive answers look like.

Investment strategy and market edge

A fund's investment mandate defines what the GP is allowed to do, which sectors, geographies, deal sizes, and instrument types fall within scope. The evaluation question is not whether the mandate makes sense but whether the GP has a specific, defensible advantage in executing it.

A claim to have "deep operational expertise" in healthcare technology is not a strategy. A claim to have sourced 40% of the last fund's deals through a proprietary network of hospital CIOs, with documentation showing those deals outperformed the fund's market-sourced investments by 300 basis points on gross IRR, is a strategy, or at least the beginning of an argument for one.

LP teams should press for the following: what percentage of the last fund's deals came from proprietary versus brokered sources, and how did returns compare between those deal types. Whether the GP has co-invested with strategic partners in the target sector, and what those relationships provide beyond capital. How the fund's strategy has evolved across vintages and whether the team that executed the original strategy is still in place.

Strategy drift is one of the most common failure modes in PE funds. A mid-market healthcare buyout manager that raises Fund III and starts doing growth-stage software deals because healthcare valuations have compressed is executing a different strategy than the one LPs evaluated at commitment. The mandate rarely prevents this; monitoring must catch it.

Track record: what the numbers actually say

Track record evaluation in PE is technically straightforward and analytically treacherous. The standard metrics are MOIC (multiple on invested capital), IRR (internal rate of return), and DPI (distributions to paid-in capital). Each tells a different part of the story and each can be presented in ways that obscure the underlying reality.

MOIC shows total value created per dollar invested. A 2.5x MOIC means the fund returned $2.50 for every $1.00 committed. It does not account for time, a 2.5x return over four years is meaningfully better than a 2.5x return over eight years. IRR is the time-adjusted return, which makes it sensitive to the timing of capital calls and distributions; early distributions inflate IRR regardless of ultimate fund performance. DPI is the most conservative metric: it shows only what has actually been returned to LPs, excluding unrealized portfolio value. A fund with a 2.0x MOIC but 0.4x DPI has mostly paper gains and may look very different at final close.

Benchmarking is essential and rarely done rigorously. Aggregate IRR means little without a vintage-year comparison, a 2016-vintage buyout fund at 18% net IRR is mediocre relative to the Cambridge Associates upper quartile for that vintage. A 2020-vintage fund at the same figure might be excellent. The relevant comparison is peer funds in the same strategy, geography, and size range, raised in the same period. Most GPs provide carefully selected peer comparisons; LPs should reconstruct the peer group independently using Preqin, PitchBook, or Cambridge Associates data.

Audited versus unaudited figures matter more than most LP teams acknowledge. Quarterly reports show unaudited NAV marks, which are the GP's own valuation. Annual audited statements verify those marks against a third-party standard. Funds that consistently revise marks downward at year-end audit versus the preceding Q3 unaudited report are providing aggressive interim valuations, a pattern worth flagging if it recurs across multiple portfolio companies over multiple years.

Team stability and key person concentration

PE funds are managed by people, not by strategies. The firm that raised Fund I with a three-person partnership and a compelling thesis may have evolved into an eight-person team where the original partners have reduced their involvement to senior advisory roles and three of the five current deal partners joined after Fund I's investment period closed. That fund may or may not be a good investment, but it is not the same team the LP evaluated at commitment to Fund I.

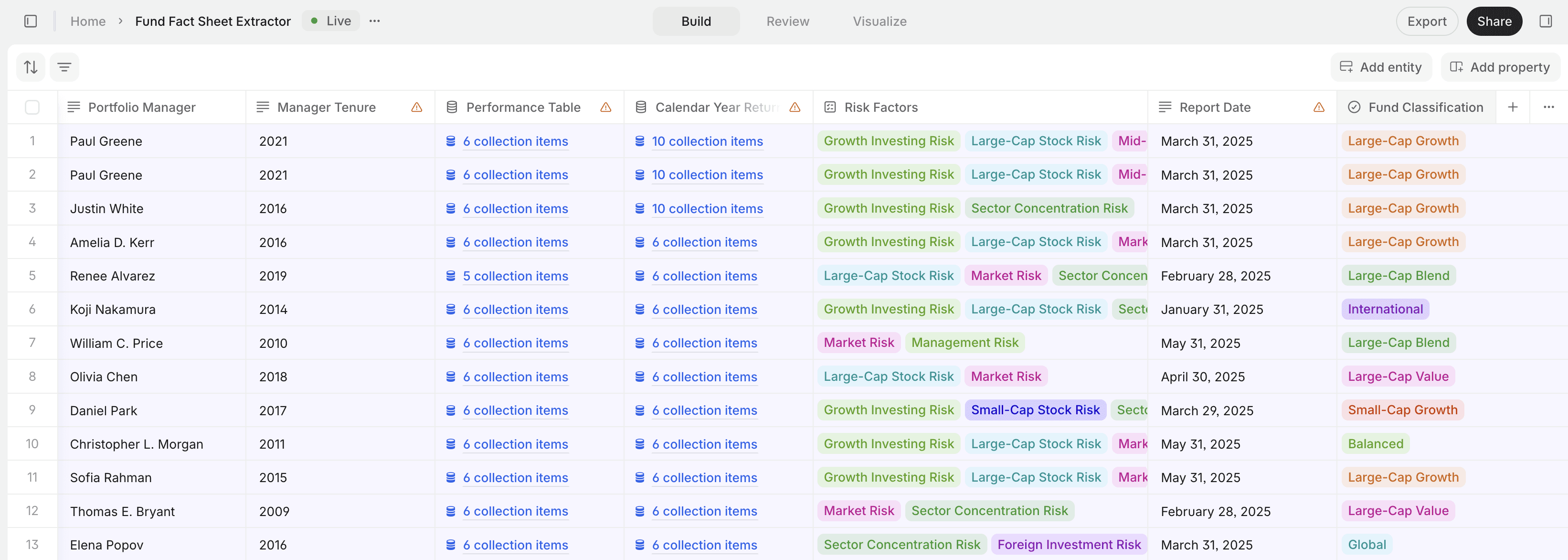

Thirteen fund fact sheets processed in V7 Go. Each row is one fund.

Key person concentration is the central risk. A buyout fund where one partner sources 60% of deals and makes the final call on all investment decisions is dependent on that individual's continued availability in a way that a fund with more distributed decision-making is not. The LPA's key person clause governs what happens if that individual departs, but the clause's protections are only as strong as their drafting, automatic investment period suspension versus notification-only requirements represent very different LP positions.

Team evaluation should cover: how deal decisions are made and who has veto authority, the percentage of deals sourced by each deal partner over the last two funds, what roles junior professionals play and whether there is a credible succession pipeline, and what the GP's track record is on retaining talent outside the founding partnership. Reference calls with existing LPs are particularly valuable here, GPs will not volunteer information about partner disputes or turnover, but existing investors usually will.

Fund economics: fees, carry, and waterfall structure

The economic terms of a PE fund, management fee, carried interest, hurdle rate, and distribution waterfall, determine how much of the fund's gross returns reach LPs versus the GP. These terms are set in the LPA and vary meaningfully from fund to fund.

The management fee is typically 1.5% to 2.0% of committed capital during the investment period, stepping down to 1.0% to 1.5% of invested capital afterward. The step-down matters, a fund that delays calling capital while maintaining a committed-capital fee basis is collecting more in fees per dollar of deployed capital than one that moves to invested capital promptly. The ILPA model specifies a 100% fee offset (all portfolio company fees reduce the management fee) and a full waiver during fund extensions. Many market-standard LPAs offer 80% offsets and continued fees during extensions.

Carried interest at 20% with an 8% preferred return is universal in buyout. The variation is in the waterfall structure, European (whole-of-fund) versus American (deal-by-deal), and in the catch-up provision. A comprehensive breakdown of how these terms interact and what they mean in economic practice is covered in the guide to reviewing a private equity LPA. For due diligence purposes, the key question is whether the fund's economic terms meet ILPA guidelines and, if not, which deviations are material enough to negotiate before commitment.

Operational infrastructure and compliance

Operational due diligence, the review of a GP's back-office, compliance, valuation, and reporting infrastructure, was once considered optional for smaller LP programs. A series of fraud cases and valuation irregularities across the industry over the past fifteen years has made it standard practice for institutional LPs, regardless of fund size.

The areas to review: who administers the fund (in-house vs. independent fund administrator, and what controls the administrator applies to NAV marks), who audits the fund and what their PE-specific experience is, how the GP handles conflicts of interest between funds it manages simultaneously, what cybersecurity practices protect LP data and deal information, and how the GP's compliance function is staffed and what its relationship is to the investment team.

Reporting quality is a proxy for operational maturity. A GP that sends quarterly reports within 45 days of quarter-end in a consistent format with clear NAV attribution and portfolio company commentary has built the infrastructure to produce that output reliably. A GP that sends reports 90 days late in different formats each quarter, without clear attribution of NAV movement, is telling you something about its operations whether or not the investments are performing.

The documents in a PE fund due diligence package

A complete fund due diligence package contains several distinct document types, each serving a different analytical purpose. LPs who route the entire package to outside counsel are delegating analysis that is partly legal and partly operational and partly financial, and outside counsel is qualified for only the first of those three.

Due Diligence Questionnaire

The DDQ is the structured questionnaire the GP completes at the LP's request. The ILPA and AIMA have published standardized DDQ templates that most institutional GPs now complete as a baseline. The ILPA DDQ covers organizational structure, investment process, track record, ESG practices, and operational infrastructure across roughly 100 questions. The AIMA DDQ adds specific sections for hedge fund and alternative credit structures.

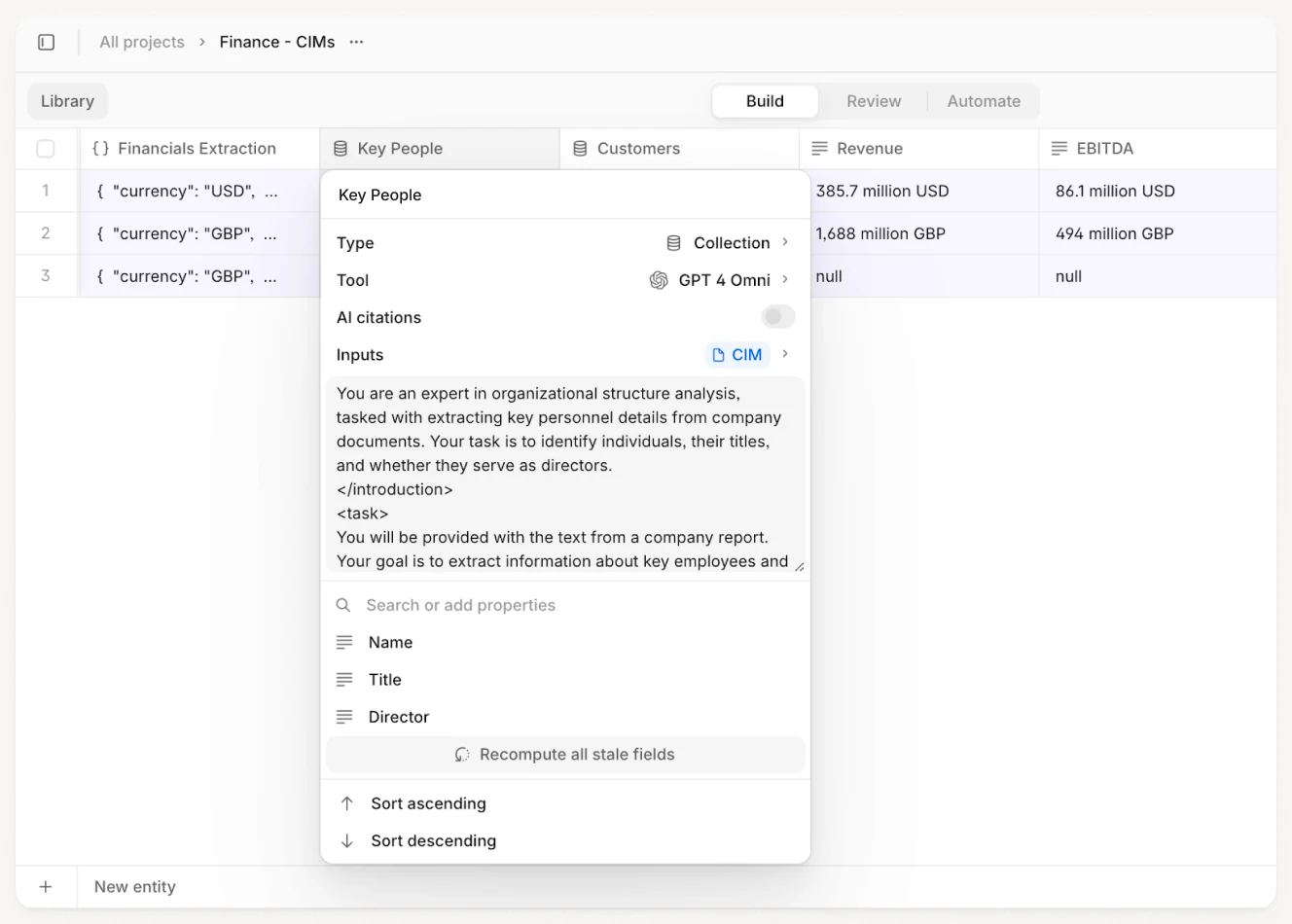

The DDQ is a starting document, not a conclusion. Its value is in establishing a baseline against which to probe during management presentations and reference calls. Gaps in the DDQ, questions where answers are vague, redirected, or simply blank, are exactly the areas to press in person. A GP that cannot clearly explain its conflict-of-interest management policy in a DDQ response is unlikely to produce clarity in conversation either. For the document processing workflow involved in analyzing DDQ responses across multiple managers simultaneously, the same extraction approach used for reviewing CIMs applies to DDQ document analysis.

The Limited Partnership Agreement

The LPA governs the fund's entire legal existence, economic terms, governance rights, LP protections, and the conditions under which the GP can be removed. It is almost always reviewed by outside counsel, but the economic and governance analysis should be conducted internally. Outside counsel can identify unusual provisions; they cannot tell an LP whether the waterfall structure fits the fund's expected exit sequence, or whether the LPAC's approval rights cover the situations where GP and LP interests are most likely to diverge.

The key provisions to prioritize: distribution waterfall structure, management fee step-down and offset mechanics, catch-up rate, LPAC composition and approval requirements, key person definitions, no-fault removal threshold, and clawback provisions. The LPA review guide covers each of these in detail, and the LPA Analysis Agent extracts all 67 standard fields from a fund LPA and benchmarks them against ILPA standards automatically. For the purpose of fund due diligence, the practical question at each provision is: does this term meet ILPA standards, and if not, is it material enough to negotiate?

Financial statements and quarterly reports

Audited annual financial statements are prepared by an independent auditor and represent the most reliable view of a fund's financial position at year-end. They contain the fund's balance sheet (investments at fair value, cash and other assets), the statement of operations (investment income, expenses, net gains and losses), and the statement of changes in partners' capital. For funds with portfolio company investments, notes to the financial statements typically include a fund-by-fund breakdown of fair values and the valuation methods applied.

Quarterly reports are unaudited and prepared by the GP. They follow whatever format the GP has chosen, which varies considerably across managers. A well-structured quarterly report includes a NAV summary, a capital account statement for each LP, a schedule of investments with current fair values, a portfolio company update section, a capital call and distribution summary, and a commentary on fund performance and market conditions. The ILPA Reporting Template, updated and released in January 2025 as part of the Quarterly Reporting Standards Initiative, defines what a complete quarterly report should contain. Many fall short of this standard.

The quarterly report is the primary monitoring document. It is also frequently the document that receives the least rigorous analysis in LP programs. An LP managing fifteen fund relationships receives sixty quarterly reports per year. If each takes two hours to analyze properly, extract the key metrics, compare against prior quarters, flag anomalies in portfolio company marks, that is 120 hours annually just for monitoring. In practice, most reports receive 15 to 20 minutes.

Fund fact sheets and performance attribution

Publicly marketed funds, including certain interval funds, business development companies, and some PE-style strategies distributed to wealth management platforms, publish quarterly fact sheets. These are standardized, typically two to four pages, and contain performance tables, portfolio statistics, sector and geographic allocation, top holdings, and benchmark comparisons.

For managers who distribute to wealth management channels, fact sheets provide a consistent, quarterly data point that supplements the private fund quarterly report. The key data points: total assets under management, inception-to-date and trailing-period performance versus benchmark, year-over-year performance by calendar year, sector concentration and any significant shifts since the prior quarter, and top-10 holdings by position size.

V7 Go extracts structured performance data from fund fact sheets, including returns, sector allocation, top holdings, and benchmark comparisons, across multiple share classes simultaneously.

LP references

Reference calls with existing LPs are the most reliable source of information about a GP that the GP cannot curate. GPs provide reference lists; the reference list will not include investors who had a poor experience. The standard practice is to ask the GP's contacts who else they know in the fund, and to reach out to those LPs directly rather than only the references provided.

The questions worth asking on reference calls: whether the GP's reporting quality and frequency matched commitments made during fundraising, whether there have been any situations where GP and LP interests diverged and how the GP handled them, whether the GP has asked for any amendments to the LPA since closing and what the circumstances were, and whether the LP would commit to a successor fund and why.

Post-commitment monitoring: the part most LP programs skip

Most LP due diligence processes end the moment capital is committed. The investment committee approves the allocation, the subscription agreement is signed, the wire is sent, and the fund joins the portfolio as a line item. What follows is a decade of quarterly reports that receive varying degrees of attention depending on how busy the LP team is.

That is a description of how LP programs operate. It is not how they should.

The argument for rigorous post-commitment monitoring is not academic. Capital loss events in PE funds, write-downs, failed exits, GP misconduct, continuation vehicle requests, are almost always preceded by observable signals in the quarterly reporting data. A portfolio company NAV that has not moved in three consecutive quarters in a market where comparable companies are appreciating. A capital call schedule that has slowed from the pace projected at commitment without explanation. An increasing concentration in a few positions that are supporting the fund's aggregate MOIC while a long tail of weaker investments remains unresolved. GPs running into trouble communicate it indirectly in the reporting long before they communicate it explicitly.

An LP that reads quarterly reports analytically, comparing each quarter against the prior four, tracking portfolio company progression through funding stages, comparing NAV movement against public market equivalents, will identify these signals months or years before the GP calls to discuss a restructuring. An LP that files the PDFs finds out when it is already too late to do anything productive.

What to track every quarter

A practical quarterly monitoring framework tracks six things: net asset value movement and attribution, capital call pace versus commitment schedule, distribution pace versus projections made at closing, portfolio company stage progression and any markdowns, concentration risk (the five largest positions as a percentage of fund NAV), and any LPAC notices or GP communications about fund-level events.

NAV movement requires attribution. An increase in fund NAV is good; an increase driven entirely by unrealized marks on a single late-stage company in a fund with a 2024 vintage is different from an increase driven by broad operational improvement across five portfolio companies that have each added revenue. The GP commentary in quarterly reports is meant to provide this attribution, whether it actually does is a measure of GP transparency.

Capital call pace is an underused signal. PE funds project a deployment schedule at fundraising, typically calling 25-30% of committed capital in years one and two, with the remainder deployed over the investment period. A fund that calls capital significantly faster or slower than its projection is deviating from the strategy underwriting. Faster calls may mean the GP is finding deals quickly, or may mean they are rushing deployments before market conditions change. Slower calls may mean the market is competitive and the GP is maintaining discipline, or may mean they cannot find deals. The distinction requires asking the GP directly and evaluating the answer against the portfolio data.

Portfolio company stage progression tells you whether the GP's value creation thesis is working. In a VC-style fund, early-stage investments should generally progress through later funding rounds over time. Investments that remain at "early stage" for four consecutive quarters in a fund with a 2019 vintage are not progressing, something has stalled. In a buyout fund, portfolio companies should show revenue growth and EBITDA expansion if the operational thesis is executing. A company that enters the portfolio at 6x EBITDA and three years later is marked at 5x on flat EBITDA is not creating value; it is waiting.

Red flags that precede larger problems

The following patterns in quarterly data are not proof of a problem. They are signals that warrant direct conversation with the GP and closer attention in subsequent quarters.

Consecutive quarters of flat NAV without portfolio company explanation. In a market where the broad PE index is generating positive returns, a fund with no NAV movement across two or three quarters is either not marking assets to market or holds a portfolio that is genuinely not performing. Either case needs explanation.

Concentration increasing over time. A fund that started with seventeen portfolio companies and now shows 60% of NAV in three positions is increasingly bet on those three exits. If any one of them is delayed or fails to exit at the projected multiple, the fund's overall return profile changes substantially.

GP-led secondary transaction request. If the GP proposes a continuation vehicle, rolling unrealized assets into a new fund structure to extend the holding period, this is a significant event. It means the GP cannot exit at a satisfactory price within the original fund's timeline. It creates a conflict of interest between LPs who want liquidity and the GP who earns continued management fees on the rolled assets. Continuation vehicles are not inherently bad; the terms on which they are offered matter enormously. LPs who have not been paying attention to the fund's performance have almost no basis to evaluate the offer.

How AI changes the PE fund due diligence workflow

The document problem in LP-side fund due diligence is a volume and consistency problem. An LP managing a $1-2B program across fifteen to twenty fund relationships receives dozens of different documents per quarter in dozens of different formats. A quarterly report from one manager is a 40-page PDF with detailed portfolio company commentary and a clear attribution of NAV movement. A quarterly report from another is a 12-page summary with a schedule of investments and nothing else. A fund fact sheet arrives monthly in a standardized format. A financial statement arrives once a year in a format governed by GAAP and the fund's specific accounting policies.

Extracting comparable data across these documents, building the monitoring framework described above, requires either a consistent analytical process applied to each document individually, or a system that does the extraction automatically. The V7 Go fund due diligence workflow covers both types of documents an LP team encounters.

The LP Fund Report Extractor ingests LP quarterly and annual financial statements and extracts a standardized set of fields across every fund in the program. For each fund document, it extracts: Fund Name, Statement Year, Statement Quarter, Vintage Year, Term, Fund Currency, Fund Manager, Security Type, Board Representation, the Fund's Role in Initial Investment (Lead Investor, Co-Investor, or Other), portfolio company count, and Net Asset Value. It also produces a sub-table for each portfolio company covered in the report: Company Name, Investment Date, Initial and Current Stage, Initial and Total Invested Amount, Initial Post-Money Valuation, Current Fair Value, Initial and Current Ownership Percentage, Type of Investment, MOIC, Gross IRR, DPI, Distributions, and Performance Comments.

The output from seventeen LP fund documents, spanning a representative set of fund documents including a US-based venture capital fund (96 portfolio companies, $51M NAV), an AI-focused early-stage fund (18 portfolio companies, $42M NAV, 10-year term, 2019 vintage), and a gaming-sector venture fund (33 portfolio companies, $216M NAV, 2021 vintage), is a single structured spreadsheet covering all seventeen funds in a consistent format, regardless of the format variation in the underlying documents.

The LP Fund Report Extractor output: a single structured dataset across multiple funds with consistent field definitions, regardless of format variation in the underlying quarterly report documents.

The Fund Report Extraction and Analysis workflow handles institutional fund documents, pension fund quarterly investment reports, CLO reports, pooled investment fund statements. It extracts 33 structured fields covering performance metrics, risk metrics, sector and geographic allocation, top holdings, benchmark comparison, share class information, and fund manager data. Beyond extraction, it generates an HTML analysis report that includes AI-powered commentary, risk assessment, benchmark performance comparison, and investor action recommendations. This workflow has processed quarterly reports from institutional fund documents including a state land-office investment fund ($2.6B balanced portfolio, Q3 2023), a public-sector pension plan ($5.3B, Q1 2022), and a $7.3B pooled investment fund.

The Fund Statement Metrics Extractor handles PE fund financial statements specifically, the annual audited documents that contain the most accurate fund-level data. It extracts general fund information, governance data, and per-company investment metrics in a structured JSON format that feeds directly into downstream integrations via Zapier. LP teams that run quarterly monitoring against a consistent database of fund metrics can compare each annual statement against the prior years' data in a single view, rather than reading each document independently.

For LP teams running AI-assisted finance workflows, the practical result of automated fund document extraction is that the monitoring framework described above becomes operational rather than aspirational. The 120 hours per year of quarterly report analysis does not disappear, but the extraction work that precedes analysis does. An LP team that previously spent half its monitoring time pulling numbers out of PDFs can redirect that time to the judgment questions: is this NAV movement explained, does this portfolio company stage change make sense, should we be calling the GP about this capital call slowdown.

The agents do not evaluate strategy, conduct reference calls, or determine whether a fund's track record reflects skill or market conditions. Those judgments require people with direct knowledge of the managers and the markets. What the agents replace is the manual extraction layer, the part where someone opens a 40-page PDF and spends two hours building a comparison table that should have taken fifteen minutes if the data were already structured.

To see how the V7 Go fund document workflows handle real LP reports, the AI Due Diligence Agent page includes examples of the extraction output and the monitoring report format for PE fund documents.

LP programs that run the full due diligence cycle, rigorous pre-commitment evaluation followed by systematic post-commitment monitoring, do not necessarily generate higher returns. But they do identify problems earlier, exercise governance rights more effectively, and enter continuation vehicle negotiations with actual data rather than a vague sense of how the fund has performed. That is a material advantage over the program that clears the commitment gate and then waits for the GP to call.

The discipline is in the monitoring. The monitoring is in the documents. The documents are now extractable.

LP programs running systematic fund due diligence, rigorous pre-commitment evaluation followed by disciplined post-commitment monitoring, do not guarantee superior returns. What they produce is better information at every decision point that follows: whether to commit to a successor fund, whether to tender in a secondary market offering, whether to exercise LPAC governance rights on a proposed restructuring. Those decisions are only as good as the monitoring data behind them.

The document extraction and analysis workflows described above handle the data layer, pulling consistent, structured metrics from the varied formats that quarterly reports, annual statements, and fund fact sheets arrive in. The judgment layer stays with the LP team. That is the right division of labor: AI extracts, the investment professional evaluates.

What is the difference between LP-side and GP-side private equity due diligence?

LP-side fund due diligence is the evaluation process an institutional investor (limited partner) conducts before committing capital to a PE fund manager, and the ongoing monitoring they perform afterward. It focuses on the GP's investment strategy, track record, team composition, fund economics, and operational infrastructure. GP-side due diligence is what the GP itself conducts when evaluating a company it is considering acquiring, commercial due diligence, financial diligence, legal review of the target. These are fundamentally different exercises. LP-side diligence answers the question: is this fund manager worth entrusting with discretionary capital for the next ten years? GP-side diligence answers the question: is this company worth acquiring at this price? Most general-audience guides on 'PE due diligence' describe the GP-side portfolio company process. LP investors need the LP-side fund evaluation framework, which covers a different set of documents, metrics, and judgment questions.

+

What documents should an LP request as part of private equity fund due diligence?

A complete LP fund due diligence package includes: (1) a Due Diligence Questionnaire (DDQ), most institutional GPs complete the ILPA or AIMA standardized template, covering organizational structure, investment process, track record, ESG practices, and operational infrastructure; (2) the draft LPA, reviewed by internal team for economic and governance terms and outside counsel for legal risk; (3) the fund's track record in audited form, the GP's presentation of historical performance should be verifiable against audited fund financial statements; (4) quarterly reports from prior funds, which show the GP's reporting quality and monitoring transparency over time; (5) fund fact sheets if the fund has a public distribution channel; and (6) reference contacts, both the GP-provided list and independently sourced existing LPs from prior funds. The DDQ and LPA are the two most analytically demanding documents. The quarterly reports from prior funds are often the most revealing, they show how the GP communicates when a portfolio company is struggling, not just when it is succeeding.

+

How long does private equity fund due diligence typically take?

The pre-commitment phase of LP fund due diligence typically runs four to twelve weeks, depending on the LP's internal process, the availability of GP management for presentations, and the complexity of the fund structure. First-close commitments at the short end of this range, some GPs expect a six-week process for returning LPs with existing relationships. First-time fund managers or complex structures (fund of funds, co-investment vehicles, credit facilities) typically require the longer end. The phases within that window: initial screening and DDQ review (one to two weeks), management presentation and follow-up questions (one to two weeks), reference calls with existing LPs (one to two weeks), LPA review and negotiation (two to four weeks, running in parallel with the above), and investment committee preparation and approval (one to two weeks). Post-commitment monitoring is ongoing for the fund's entire life, ten to fourteen years for a standard buyout fund with extension rights. The monitoring phase is lower intensity than the pre-commitment phase but requires systematic discipline: quarterly report review, annual financial statement analysis, and periodic check-in calls with the GP.

+

What track record metrics matter most in private equity fund due diligence?

The three standard metrics are MOIC (multiple on invested capital), IRR (internal rate of return), and DPI (distributions to paid-in capital). Each tells a different part of the story. MOIC shows total value per dollar invested but ignores time, a 3.0x return over four years and a 3.0x return over ten years look identical on MOIC but are very different investments. IRR is time-adjusted and is the most commonly cited headline figure, but it is sensitive to the timing of capital calls and distributions: early distributions inflate IRR mechanically. DPI is the most conservative and arguably most meaningful metric for mature funds, it shows only what has actually been returned to LPs in cash, excluding unrealized portfolio value that may or may not ever be realized. For funds that are less than five years old, DPI is typically low by construction and not a reliable quality signal. For funds eight to ten years into their lives, a low DPI relative to MOIC means the fund holds substantial paper gains that have not been monetized. Benchmarking against vintage-year peers is essential, a 20% net IRR for a 2015-vintage buyout fund and a 2020-vintage fund mean very different things relative to what was achievable in each market environment.

+

What should LP programs monitor after committing to a private equity fund?

AI changes the LP fund due diligence workflow primarily through document extraction, the process of pulling consistent, structured data from the inconsistent and varied document formats that GPs produce. The most time-consuming part of fund DD and monitoring is not making judgments; it is extracting the data on which judgments are made. A quarterly report from one manager is a 40-page PDF with clear attribution; from another it is a 12-page summary with a schedule of investments only. An LP managing fifteen fund relationships receives sixty quarterly reports per year in fifteen different formats. AI fund document workflows, like the V7 Go LP Fund Report Extractor, Fund Report Extraction and Analysis, and Fund Statement Metrics Extractor, ingest these varied document formats and produce structured, comparable output across all funds in a consistent field schema. The extraction covers fund-level fields (NAV, vintage year, portfolio company count, fund term) and per-company fields (MOIC, IRR, DPI, current fair value, stage). For the pre-commitment phase, AI-assisted DDQ processing and LPA review reduce the extraction and benchmarking work so the review team can focus on judgment. The agents do not conduct reference calls, evaluate strategy quality, or determine whether a track record reflects skill or market conditions. Those judgments require people. What AI replaces is the manual extraction layer that precedes those judgments, and which, without automation, consumes the majority of the monitoring team's time.

+

How does AI help with private equity fund due diligence and monitoring?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.