Knowledge work automation

16 min read

—

There are roughly 16,000 private equity-backed companies waiting to be sold, according to McKinsey's 2026 Global Private Markets Report,. Most of them have been waiting for years. The average hold period globally reached 6.6 years, per McKinsey's 2026 Global Private Markets Report, years in 2025, and more than 4,000 US-based portfolio companies aged past five years without a completed exit. That is not a market cycle. That is a structural problem.

LPs who expected distributions in 2022 and 2023 are now in 2026 running models that assume another year of waiting. Fundraising for successor funds is harder when distributions from the current fund are thin. And the companies themselves are not standing still: management teams are fatigued, competitors are moving, and the original investment thesis is getting harder to defend with every quarterly board meeting.

The standard explanation is that markets are to blame. Interest rates, valuation gaps, a soft IPO window. All of that is real. But it is not the whole story. A significant portion of the exit backlog reflects firms that were not ready when the window opened, that started exit preparation too late, or that arrived at the market with a data room and a CIM that gave buyers reasons to slow down rather than speed up.

This piece examines what is actually blocking private equity exit strategy in 2026, where the preparation failures tend to occur, and what the firms that do exit cleanly have in common. For a broader look at how AI is changing document-heavy deal workflows, the AI in due diligence guide covers the full deal lifecycle.

In this article:

Why private equity exit strategy is more difficult in 2026 than the market alone explains

The three structural forces converging on the exit market right now

What leading sponsors do differently in the 18 months before a sale

Where AI document automation is compressing the exit preparation timeline

AI for document processing

Prepare exit documentation faster than your competition

Get started today

Why private equity exit strategy is failing the test in 2026

Three forces are converging to make exits structurally harder, and only one of them is out of a GP's control. Understanding which is which changes what you can actually do about it.

The market force is real: the valuation gap between buyers and sellers has not closed since 2022. GPs acquired companies in 2019 through 2021 at peak multiples. Those multiples no longer clear in most buyer conversations today. McKinsey's analysis of PE exit prospects found that earn-outs and price adjustment mechanisms became standard deal tools after 2022, not because buyers and sellers couldn't agree on terms, but because they couldn't agree on what the company was worth. A GP sitting on an asset marked at 12x EBITDA in the fund's quarterly NAV statement faces a painful choice when the market bids 8x. You can accept the haircut, refinance and wait, or move the asset into a continuation fund. Most have been choosing the latter two options.

The LP force is harder to ignore because it is now measurable. As of 2025, 21% of limited partners cite distributions to paid-in capital (DPI) as their most critical performance metric, per McKinsey's 2025 LP survey, performance metric, up from 8% just three years prior. IRR is easy to present favorably when you control the timing of capital calls and benefit from subscription credit lines. DPI is harder to massage. It simply reflects: did the fund return more money than it took in? For many 2018-2021 vintage funds, the honest answer in 2026 is: not yet. That creates pressure on GPs to move, even into a market that has not fully reopened.

The third force is the one GPs talk about least in LP updates: preparation. Exit processes fail or stall for reasons that have nothing to do with market conditions. The data room has gaps. The financial model has inconsistencies that surface in buyer due diligence. The CIM was written by someone who optimized for narrative over accuracy, and sophisticated buyers push back on claims that cannot be supported by the underlying documents. Management presentations go poorly because the CEO and CFO have not spent enough time aligning on the story.

These are not abstract risks. According to The Daily Upside, private equity firms are sitting on a record backlog worth trillions of dollars, often acquired during cheap-money years at lofty valuations, and even if deal activity accelerates sharply, working through that inventory will likely take multiple years. Not because every asset is unsellable. But because the firms that can actually close will be the ones that show up prepared.

The 16,000-company backlog and what it reveals

The exit backlog is not uniform. Some of those 16,000 companies are genuinely stuck because the business deteriorated or the category fell out of favour with buyers. A meaningful portion, though, are companies with real value, capable management teams, and sound unit economics that simply have not been prepared for the market in a way that makes buyers confident.

The data on hold periods tells part of this story. Median exit hold periods stretched from 4.3 years in 2017 to 5.4 years in 2024. The first decline in five years appeared in 2025, which is encouraging. But the backlog of companies held for more than four years represents 52% of all buyout-backed inventory globally, the highest on record. That figure includes companies whose funds have already passed their expected investment period, meaning every additional month of hold creates friction: LP reporting obligations intensify, management incentive plans need to be reset, and successor fundraising conversations get harder.

Continuation funds have become the default response for assets that cannot clear the market at an acceptable price. More than 1,600 funds were set to wind down in 2025 or 2026, and over half of all PE funds were six or more years old. Continuation vehicles are a legitimate tool, but they are also a signal: the original exit plan did not work. The company went into the continuation fund because the GP could not find a buyer or a public market at a price that justified the narrative in the last LP report.

None of this means 2026 will be a repeat of 2023. Trade sales represented roughly 60% of European PE exits in 2025, the highest share in ten years. The IPO pipeline is, by investment banker accounts, simmering. Analysts at J.P. Morgan and Morgan Stanley have estimated that up to a third of all IPO activity in 2026 could involve PE-backed companies. The window is open. The question is which sponsors come through it.

The exit preparation problem that most GPs underestimate

The honest answer to why exits stall is this: most GPs start preparing for sale six months before they want to go to market. That is too late. The preparation timeline for a mid-market company with a ten-year operating history is closer to 18 months, and the sponsors who consistently close clean, fast processes know this.

The document burden alone is substantial. A credible virtual data room for a company in a regulated or data-intensive sector will contain hundreds of files: audited financial statements, management accounts, customer contracts, supplier agreements, IP registrations, employment records, tax filings, insurance policies, compliance certifications, and any material litigation or regulatory correspondence. Buyers read these documents. Their advisors build diligence reports from them. Inconsistencies between what the CIM says and what the data room contains create red flags, and red flags create price chips.

The contents of a typical VDR span financial, legal, HR, and compliance documents across years of company history. Population and consistency-checking this library is the first place exit timelines slip.

The financial model is a separate problem. GPs often build the entry model at acquisition and update it periodically, but the exit narrative requires a model that tells a clean story: the EBITDA trajectory, the working capital profile, the growth capex story, the bridge from historical reported figures to a buyer-facing adjusted number. When the model has not been maintained with exit in mind, the reconciliation work surfaces surprises. A buyer's financial due diligence advisor running their own model will find the gaps. It is better to find them first.

The management team preparation question is underappreciated. The CEO and CFO who ran the business through a PE hold period did not spend most of that time thinking about how to present the company to an external buyer. The first management presentation is often rougher than expected. Key metrics are described inconsistently. The competitive positioning narrative has not been stress-tested. Buyers who see uncertainty in the room reflect it in their bids.

These are execution problems, not market problems. They are addressable with sufficient lead time and a systematic approach to preparation. The firms that are exiting cleanly in 2026 did not get lucky. They started earlier. For a detailed look at how portfolio monitoring data feeds into exit preparation, the portfolio monitoring guide covers what to track across the hold period to arrive at exit with credible data.

The management presentation is one of the most common points of failure in a competitive exit process. In a well-run sale, the first management presentation to a shortlisted buyer group happens at a carefully managed point in the process, after the CIM has generated interest and after the deal team has had weeks to prepare the CEO and CFO for likely questions. In a poorly run sale, it happens three weeks after the firm decided to go to market, with a management team that has never rehearsed the competitive positioning narrative and a CFO who gives different EBITDA figures depending on which slide they are looking at. Buyers who see uncertainty in the room reflect it in their bids. The price chip in a management presentation is one of the most expensive and least visible costs in a PE exit.

What makes this pattern persistent is that PE firms are genuinely busy during the hold period. Running portfolio company boards, managing add-on pipelines, supporting management teams through operational challenges, and maintaining LP relationships are all real demands on GP time. Exit preparation looks like it can wait until the right moment. The problem is that the right moment arrives faster than expected, and the preparation that was going to happen in Q3 is suddenly due in Q1. The companies that exit well in 2026 are the ones whose GPs treated exit preparation as an ongoing discipline during the hold period, not a project that starts when the clock runs out.

What leading sponsors do differently: multi-path planning and the 18-month window

The sponsors that exit cleanly in a constrained market have two habits in common: they plan for multiple exit routes simultaneously, and they start earlier than their peers. Neither of these is a secret. Both are harder to execute than they sound.

Multi-path exit planning

The conventional PE exit model was sequential: the firm picks the best route, prepares for that route, and runs that process. In practice, many firms still work this way. A GP decides the company is an IPO candidate, spends six months working with investment banks on the IPO preparation, and then — when the window closes — scrambles to run a parallel trade sale process with advisors who were not engaged from the start.

The firms that moved assets successfully through 2023 and 2024, when conditions were genuinely difficult, prepared all three core routes in parallel from the beginning: the strategic trade sale, the secondary buyout, and the IPO. That does not mean running three full processes simultaneously. It means ensuring that the documentation, the financial model, and the management narrative are built to support any outcome. A CIM written for a strategic buyer is different from an equity story written for a public market roadshow. But the underlying data room, the quality of earnings analysis, and the operational data are identical. Build the foundation once, then tailor the presentation to the audience.

The CFA Institute's analysis of what it called the new PE exit playbook found that leading sponsors increasingly develop credible alternatives early, rather than relying on a single buyer universe. The practical implication: the advisor team is engaged 12-18 months out, not 6 months out, and the process starts with a genuine assessment of which route is most likely to clear given the current buyer landscape.

The 18-month preparation window

At 18 months before a target launch date, the real work begins. Financial model alignment: does the model reflect the story the company will tell at exit, and can every adjusted EBITDA line be defended back to source documents? Management team assessment: are there gaps that need to be filled before a buyer sees the team? Operational narrative: what is the value creation story, and what evidence from the hold period supports it?

At 12 months: the first CIM draft, VDR population begins, advisor selection is finalized. This is where most firms are still starting. The firms that started at 18 months have already resolved the financial model inconsistencies and are walking into the 12-month phase with a clean data set. The firms that start at 12 months are discovering those inconsistencies at the same time they are trying to build the CIM. One group has a controlled process. The other has a fire drill.

At 6 months: buyer marketing, preliminary management presentations, LP communication. This should be a delivery phase, not a preparation phase. If preparation is still happening at 6 months, the process will slip.

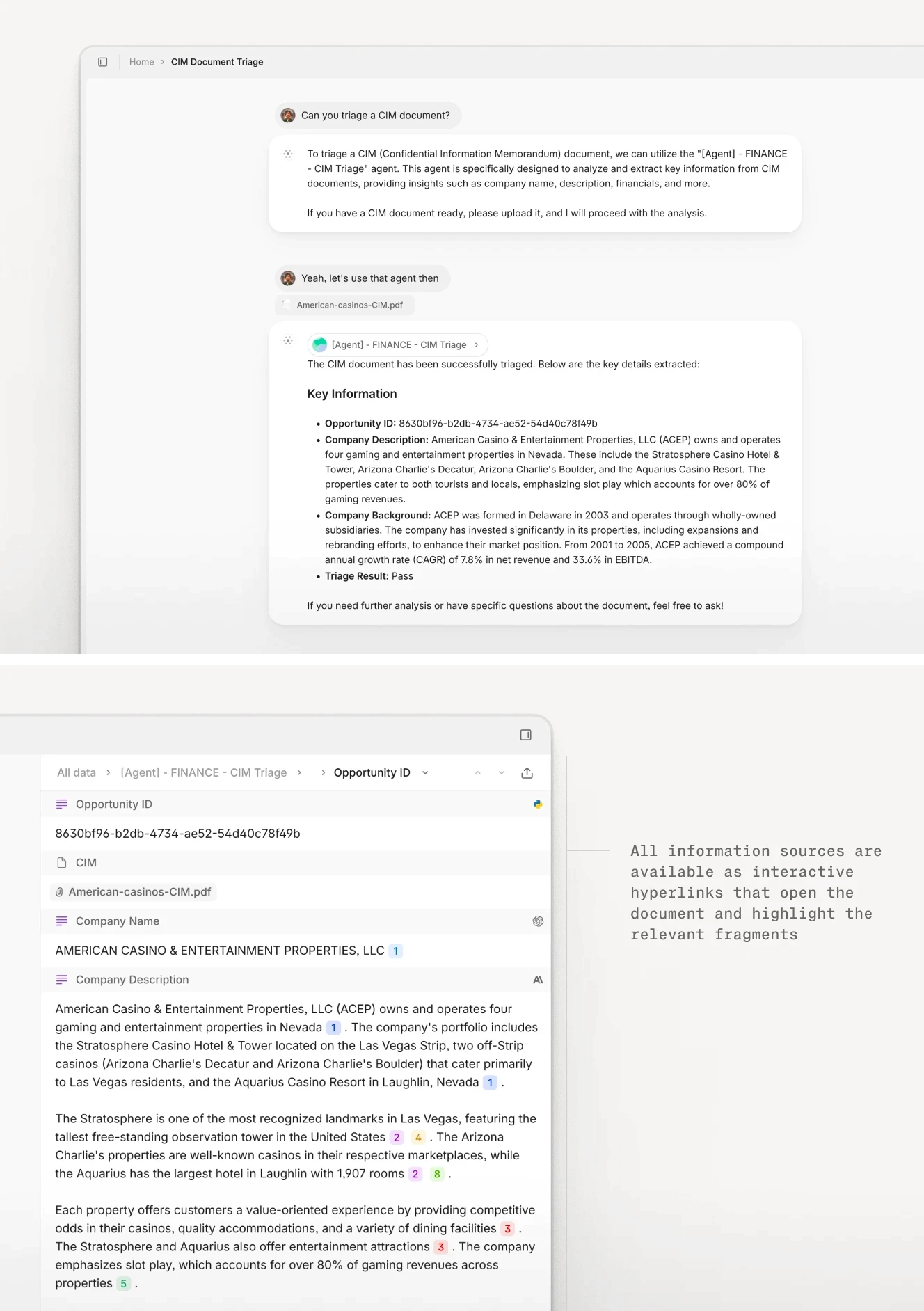

CIM analysis agents can extract and cross-reference key financial data across the document before buyers see it, surfacing inconsistencies that would otherwise surface in due diligence.

How AI compresses the exit preparation timeline

The document-heavy work of exit preparation is exactly where AI agents deliver measurable time savings. Not in judgment calls about pricing or route selection. In the mechanical but consequential work of extracting, organizing, and cross-checking the documentation that underlies every buyer conversation.

CIM preparation and data extraction

A Confidential Information Memorandum synthesizes years of financial and operational data into a narrative document that buyers use to form initial bids. The quality of that synthesis depends on the quality of the underlying data extraction: pulling EBITDA figures from management accounts, reconciling them with audited statements, mapping customer concentration data from contract files, extracting headcount and compensation trends from HR records. Done manually, that extraction work takes weeks. Done incorrectly, it creates discrepancies that surface in buyer due diligence and damage deal momentum.

An AI agent configured to work across a company's financial document library can run that extraction in hours, returning structured outputs with citations to the source documents. Each figure is traceable. Discrepancies between the management accounts and the audited statements surface immediately rather than six weeks into a due diligence process. The CIM review automation from V7 Go is built for exactly this workflow: define the extraction schema once across your CIM, run it across the source documents, and get a structured output that shows you where the numbers land and where they need to be defended.

AI-assisted VDR review flags document gaps, consistency issues, and missing required materials before buyers submit their first information request.

Virtual data room organization and quality control

A VDR populated under time pressure tends to have gaps. Documents are uploaded without standardized naming. The financial statements folder has three different versions of the same report. A material customer contract was not included because no one checked whether it had been executed. These are not hypothetical scenarios. They are the standard output of a VDR that was built in six weeks by a team also running the CIM process and preparing management for presentations.

An agent configured for VDR review can work through a document library systematically: checking for required document types by category, flagging naming inconsistencies, identifying date gaps in financial records, and surfacing any document that references a material contract or obligation not represented elsewhere in the data room. The document comparison agent can cross-reference representations in the CIM against the underlying documents to confirm that what the information memorandum says matches what buyers will find when they look.

Buyer Q&A and due diligence acceleration

Once a buyer's team is in the data room, they submit information requests. In a competitive process, the speed and quality of responses to those requests affect how buyers perceive the seller's preparedness, and that perception feeds into price. A team that answers 40 due diligence questions in 48 hours signals a well-organized data room and a confident management team. A team that takes two weeks and returns partial answers signals the opposite.

AI agents configured against the VDR can run buyer information requests against the full document library and return sourced responses: the exact clause in the contract that addresses a specific question, the page in the financial statements that contains a particular figure, the compliance certificate that satisfies an audit inquiry. Every output cites its source in the original document. This is the workflow V7 Go was built for: a deal team can point the agent at a specific buyer question, and within minutes receive a structured response grounded in the actual documents, not in the team's memory of what those documents contained.

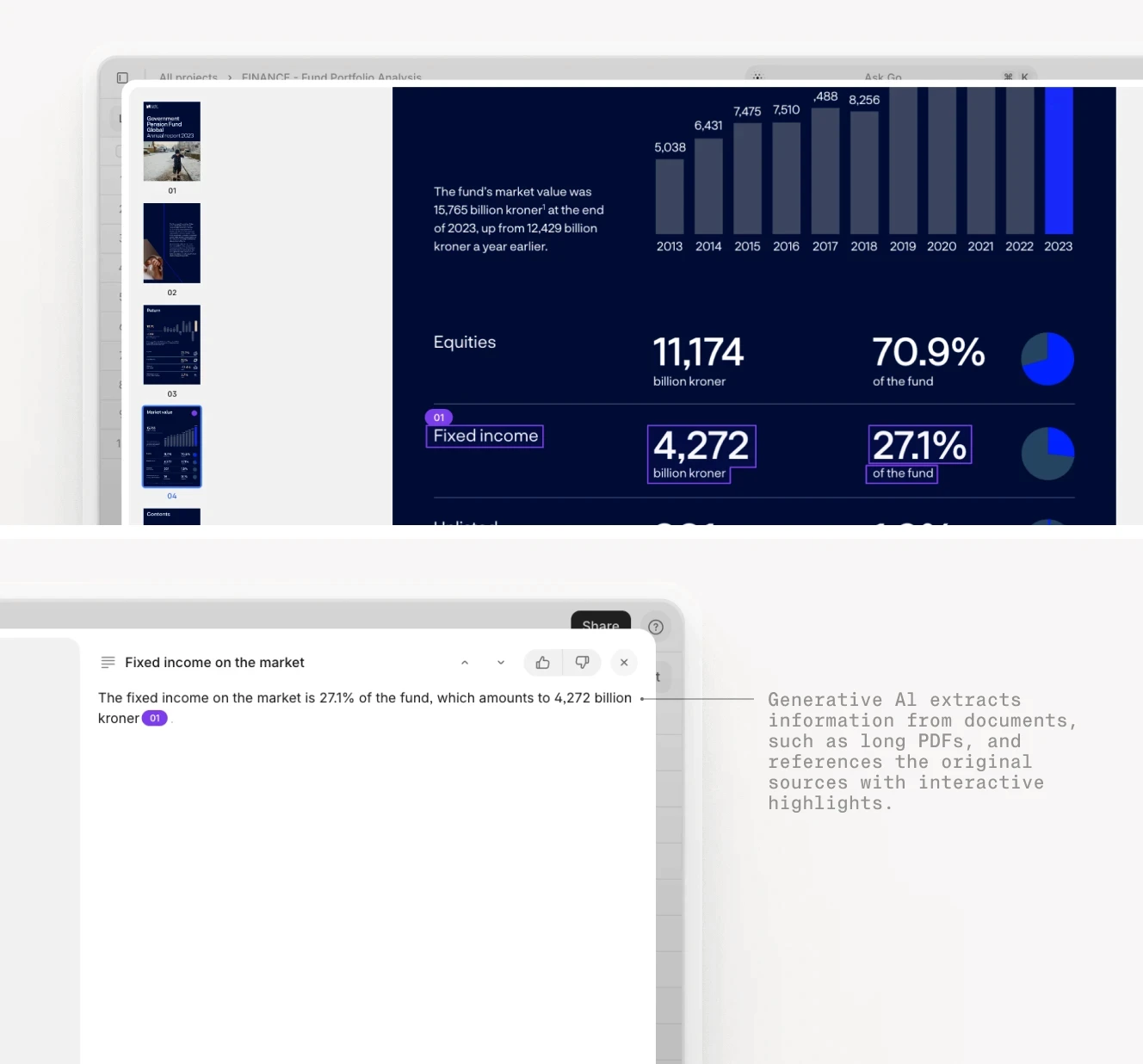

AI agents extract financial metrics from source documents with citations that link each output directly to its page in the original file, making buyer Q&A responses faster and defensible.

This matters most in competitive processes where multiple buyers are running parallel due diligence. The seller team that responds fastest with the most credible sourcing tends to maintain price tension longer. The one that responds slowly gives buyers time to find gaps on their own and chip the price before final offers arrive. For context on how AI is changing the broader due diligence workflow, generative AI in finance covers the full range of document-intensive applications across the deal cycle.

What AI cannot replace in exit execution

The important caveat is that AI accelerates the document-intensive preparation work. It does not replace the judgment calls that determine whether the exit succeeds. Pricing strategy, route selection, buyer targeting, negotiation tactics, and management team preparation all require human expertise and situational knowledge that no agent can replicate. What AI does is ensure that when the human judgment calls are made, they are made from a position of information rather than uncertainty: the financial model has been checked, the VDR is complete, the CIM claims have been verified against the source documents, and the buyer Q&A responses are fast and accurate.

The firms that have invested in AI-assisted exit preparation report a consistent pattern: the document review and extraction work that previously consumed two to three weeks of analyst time is completed in two to three days. That time saving reduces cost and moves the entire timeline forward, giving the deal team more runway for the work that actually requires judgment. An analyst who is not spending their week manually pulling figures from management accounts is instead helping the CFO prepare for the questions buyers are likely to ask in the management presentation. That reallocation of effort is where the competitive advantage shows up most clearly at the final offers stage.

The shift in how LPs evaluate GPs at the fund level is also relevant here: firms that demonstrate disciplined exit execution, backed by well-documented processes, build the kind of track record that makes the next fundraise easier. Exit execution is a financial outcome and a data point about how the firm operates.

Exit execution is where PE firms show what they are actually made of

The companies that exit well in 2026 will have one thing in common before the process begins: preparation that started well before the market opened. What happens in the sale process itself is largely determined by the work that happened 12 to 18 months earlier.

The 16,000 companies in the exit backlog are not all the same. Some have genuine structural problems: businesses that deteriorated, categories that collapsed, management teams that were not strong enough to drive the exit narrative. Those companies will be hard to move regardless of preparation.

But a significant proportion are sound businesses with real value that have been held back by process failures: exits that were not started early enough, data rooms that gave buyers reasons to slow down, financial models that surfaced inconsistencies mid-process, management presentations that did not inspire confidence. These are solvable problems. They are just easier to solve at 18 months than at 6.

The sponsors that move through 2026 successfully will share a common characteristic: they treated exit preparation as a parallel workstream to portfolio management, not as a separate project that starts when the fund is almost out of time. They built the documentation disciplines, the financial model hygiene, and the management team readiness before the window opened. When the window opened, they were ready to step through it.

If your firm is working through exit preparation and the document burden is where time is being lost, the AI due diligence agent from V7 Go handles the extraction, cross-referencing, and sourcing work that currently sits on your deal team's plate before the first buyer call. The speed of your response to buyer information requests is a signal. Make it a positive one.

What is a private equity exit strategy?

A private equity exit strategy is the plan a GP (general partner) uses to sell or otherwise monetize a portfolio company and return capital to its LPs (limited partners). The main exit routes are trade sales to strategic or financial buyers, secondary buyouts to other PE firms, IPOs, and dividend recapitalizations. In practice, most mid-market PE firms exit through trade sales, which accounted for roughly 60% of European PE exits in 2025. IPOs are less common and are typically reserved for companies of sufficient scale and predictability to attract public market investors. Continuation funds have become an increasingly common alternative when GPs cannot clear the market at an acceptable price but believe the asset still has meaningful upside. A well-designed exit strategy identifies the most likely route 18 months or more before the target launch date and prepares the documentation, financial model, and management team for that route while keeping alternatives open.

+

Why are PE exit timelines getting longer?

PE exit timelines have extended for three overlapping reasons. First, the valuation gap: companies acquired at 2019 to 2021 peak multiples cannot clear the current buyer market at those same multiples, and sellers have been reluctant to accept the markdown. Second, LP pressure has shifted in character: limited partners who were patient about IRR in previous years are now explicitly prioritizing DPI, which means actual cash distributions rather than paper returns. This creates conflicting pressures on GPs, who face pressure to move but also face the risk of selling below their marked value. Third, many firms simply did not start exit preparation early enough and found themselves launching into a soft market without the documentation quality, management team readiness, or advisor relationships needed to move quickly. The companies that have exited successfully in 2024 and 2025 did so because they were positioned before conditions improved, not because they timed the market perfectly.

+

What is a continuation fund and when do PE firms use it?

A continuation fund, also called a continuation vehicle, is a structure that allows a PE firm to transfer one or more portfolio companies from a fund approaching the end of its life into a new vehicle with a fresh investment horizon. LPs in the original fund are typically offered the choice to cash out at a current valuation or roll their interest into the continuation vehicle. New investors can also come in alongside. GPs use continuation funds when they believe an asset has significant remaining upside but the original fund's life is too short to capture it, or when market conditions do not support a sale at the price they want to achieve. Continuation funds can be a legitimate value-maximization tool, but they also function as a mechanism for avoiding a below-mark sale. As of 2025, more than 1,600 PE funds were approaching the end of their intended lives, which explains the surge in continuation fund activity and the growing scrutiny from LPs about the governance and pricing of these transactions.

+

How long does a typical PE exit process take from launch to close?

From the formal launch of an exit process to signing, a typical PE trade sale takes six to nine months for a mid-market company. Highly competitive processes with strong buyer interest can close faster, in four to six months. Complex situations, regulatory approvals, or extensive buyer due diligence can extend the timeline to twelve months or beyond. The preparation phase before formal launch, which includes data room population, CIM drafting, advisor selection, and management presentation preparation, adds another three to twelve months depending on the company's size and documentation readiness. Firms that begin preparation 18 months before their target signing date give themselves the most flexibility to handle process delays, manage LP expectations, and keep alternative exit routes viable in parallel. Firms that begin six months before the target date are typically running the preparation and the process simultaneously, which increases the risk of errors surfacing during buyer due diligence.

+

What documents are needed to exit a PE-backed company?

AI agents accelerate the most time-consuming parts of exit preparation without changing the judgment calls that still require human expertise. In CIM preparation, agents extract and cross-reference financial metrics across management accounts, audited statements, and board materials, surfacing discrepancies before buyers find them. In VDR population, agents work through document libraries to flag missing required document types, identify naming inconsistencies, and check that material contracts referenced in the CIM are actually present in the data room. In buyer Q&A, agents run incoming information requests against the full VDR and return structured responses with citations to the source documents, allowing the deal team to respond faster and more accurately than is possible with manual document review. The measurable benefit is timeline compression: tasks that previously took weeks of analyst time can be completed in hours, allowing the GP to launch a better-prepared process earlier and respond to buyer requests with a speed and precision that signals organizational competence to the buyer's team.

+

How can AI help with PE exit preparation?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.