16 min read

—

How VC analysts build deal sourcing engines, manage deal flow pipelines, and use AI document processing to screen hundreds of opportunities without scaling headcount.

A venture capital fund with $200 million under management might receive 3,000 inbound inquiries a year. It closes ten deals. The math is simple; the execution is not. Most venture capital firms do not lack access to companies. They lack the analyst bandwidth to evaluate them systematically.

Deal sourcing in venture capital is the systematic process of identifying, accessing, and evaluating investment opportunities before competitors do. It differs from deal flow, which describes the pipeline that results from sourcing activity. Deal flow is what you have; deal sourcing is how you build it.

This guide covers the methods VC associates and analysts use to source deals: inbound and outbound strategies, network development, sector mapping, accelerator scouting, and pipeline management. It also covers what happens when deal volume outpaces analyst capacity, and how AI document processing is changing that calculus.

In this article:

Inbound versus outbound deal sourcing: what each yields and when to use them.

Core methods for building a proprietary deal flow engine.

Investment screening criteria and the VC document stack.

How AI processes pitch decks, cap tables, and SAFEs at scale.

What is deal sourcing in venture capital?

Deal sourcing is the upstream work that determines deal quality, not the act of reviewing a pitch deck that appeared in your inbox. Most associates conflate deal sourcing with deal flow. They are related but distinct. Deal flow is the ongoing stream of investment opportunities that arrive: inbound emails, warm referrals, portfolio introductions. Deal sourcing is the deliberate activity that generates that stream: systematic outreach, conference attendance, sector mapping, and relationship building with founders before they are raising.

The distinction matters because deal flow is reactive; deal sourcing is proactive. Firms that only manage their deal flow take whatever the market sends them. Firms that source aggressively identify promising startups before they become widely known, and therefore before they become competitively priced. Top-quartile funds attribute their returns to proprietary access rather than analytical edge on widely shopped deals — a pattern NVCA research has tracked consistently across fund vintages.

Three terms anchor every sourcing conversation:

Investment thesis: The fund's defined criteria for what it invests in: stage, sector, geography, check size, ownership targets. Sourcing strategy flows from the thesis, not the other way around.

Proprietary deals: Companies the firm found before they were fundraising broadly. These tend to come at better valuations and with fewer competing term sheets.

Intermediated deals: Brought to the firm via a banker, placement agent, or syndicator. Common in growth equity; less common in pre-seed and seed.

Inbound vs. outbound deal sourcing

Both approaches yield different quality signals and require different time investments. Neither is sufficient on its own.

Dimension | Inbound | Outbound |

|---|---|---|

How deals arrive | Referrals, cold emails, LP introductions, portfolio founder referrals | Cold outreach, conference prospecting, data-driven company discovery, accelerator scouting |

Quality signal | High when sourced via portfolio founders or trusted LPs; noisy from cold email | Depends entirely on how well-defined your screening criteria are |

Effort level | Low per deal once brand is established; high brand-building investment upfront | High per deal; requires systematic process and clear thesis |

Competitive dynamics | Strong inbound signals often reach multiple funds simultaneously | Well-executed outbound can surface companies before they are fundraising |

Best for | Warm markets, branded funds, sectors where founders know who to call | Emerging sectors, geographic expansion, thesis-specific opportunities |

AI document analysis tools extract competitor identification data directly from pitch decks, mapping each screened company against its competitive field.

How to source deals: core methods for VC investors

Sourcing strategy is not one decision. It is a set of parallel activities that each feed a different part of the pipeline. The mix shifts as a fund matures and as the thesis sharpens. An early-stage seed fund operating in a narrow vertical might source 80% of deals through three university programs and two accelerator relationships. A multi-stage growth fund with $1 billion in assets might run a dedicated outbound team using data providers to map every Series B-eligible company in its target sectors.

The core methods are covered below. Most firms use all of them; the allocation of time across each depends on the fund's stage, sector focus, and existing brand.

Building your network for proprietary deal flow

The premise of proprietary deal flow is simple: if a founder calls you before they run a formal process, you have a chance to lead the round on your terms. Getting to that position requires years of relationship investment. It does not happen through a single conference appearance.

The most productive relationship categories for early-stage VCs:

Portfolio founders: A founder who received a fair process and genuine help from your fund becomes a referral machine. Warm introductions from portfolio founders carry the highest quality signal of any inbound channel because the founder has already validated the team and the opportunity.

Angel networks and scout programs: Well-connected angels with sector depth often see companies a full round before institutional money does. A formalized scout relationship, tied to economics or information exchange, brings these deal sightings into your pipeline systematically.

Other VCs in adjacent stages: A pre-seed fund will refer Series A opportunities to investors they trust. The relationship is reciprocal: you pass them companies that are too early for your fund; they pass you companies that have graduated past theirs.

Academic and research networks: For deep tech, biotech, or software infrastructure, university technology transfer offices and research labs surface companies that often have no other institutional relationships when they first incorporate.

A CRM is not optional here. It is the infrastructure for this kind of network. Records of every founder conversation, every warm intro, and every pass rationale turn individual relationships into institutional memory. When a company you passed on two years ago comes back around for a Series B, your notes from that first meeting are the difference between a fast decision and a wasted week of re-research.

Market and sector mapping

Outbound sourcing starts with the investment thesis, not with a database query. The thesis defines the criteria: stage, sector, geography, team profile, traction thresholds, and market size requirements. Only after those parameters are set does it make sense to run a systematic scan.

A concrete example: a fund focused on B2B SaaS targeting the Series A market might define its sourcing criteria as companies with annual recurring revenue (ARR) between $500K and $2 million, US-based, fewer than 30 employees, operating in software for financial services or healthcare compliance. That description narrows a universe of tens of thousands of companies to a manageable list of several hundred.

Data sources for sector mapping include:

Crunchbase and PitchBook: The standard starting points for identifying funded companies by sector, stage, and geography. Useful for mapping who has already received institutional capital and at what valuations.

LinkedIn: Underestimated as a sourcing tool. Searching for companies by headcount growth, recent hires in sales or engineering, and founding date can identify companies in the 10-30 employee range that fit early-stage criteria but have not yet raised an institutional round.

Harmonic and CrustData: Purpose-built for VC sourcing. These tools track company signals: hiring velocity, web traffic growth, and app store reviews that precede a fundraise by three to six months.

Sector mapping is not a one-time exercise. The best maps need active upkeep: add companies as they form, remove those that have clearly outgrown the thesis or closed, and update traction metrics quarterly.

Accelerator and event sourcing

Y Combinator, Techstars, 500 Global, and similar programs are high-concentration deal sourcing events. A single YC demo day surfaces 100-200 companies in a few hours, each of which has passed a non-trivial vetting process to join the batch. The challenge is not access — most institutional funds can attend — but throughput. Reviewing 200 pitch decks in the days following a demo day with any analytical rigor requires a process, not heroic effort from a single analyst.

University demo days and regional accelerator programs are underworked by most funds. The competitive intensity at MIT, Stanford, and CMU is high; the competition at a well-run regional program in a secondary city is much lower. Funds that build consistent scout relationships at three or four non-obvious programs often find less competitive deal access than funds that only show up at YC.

Conferences and vertical-specific events, whether RSA for cybersecurity, HIMSS for health tech, or Money20/20 for fintech, serve a different function. They identify founders who are far enough along to present at an industry event, which typically means post-product and often post-revenue. They are less useful for pre-seed sourcing and more useful for Series A and B pipeline development.

Data-driven and technology-assisted sourcing

CRM platforms designed for VC, including Affinity, Zapflow, and 4Degrees, have become standard infrastructure at funds that process more than a few hundred opportunities per year. They track relationship strength, meeting history, referral chains, and follow-up schedules. Affinity, in particular, uses email and calendar data to surface warm connections you may not remember you have.

Deal sourcing platforms like Cyndx and Grata extend the search function: they crawl company databases, news sources, and public records to surface companies that match thesis-defined criteria but are not yet visible in Crunchbase or PitchBook. For funds with specific geographic or vertical mandates, these tools can identify companies months before they appear in standard databases.

The bottleneck these tools collectively do not solve is evaluation. They help you identify promising startups earlier. They do not help you evaluate them faster. That bottleneck sits at the screening stage, and it is where analyst time disappears.

Structured data extraction from financial documents lets analysts compare company metrics across hundreds of opportunities without manual data entry.

Building and managing your deal flow pipeline

A pipeline without structure is a list. The goal of pipeline management is to know, at any given moment, where every active opportunity stands, why it is there, and what the next action is. Most VC analysts operate on an implicit version of this; the best ones make it explicit.

A standard deal flow pipeline has five stages:

Sourced: Company identified but not yet reviewed. Could be from outbound scanning, an inbound email, or a referral that has not been qualified.

First screen: Initial review against thesis criteria. A 20-minute look at the deck and founding team. The outcome is pass, follow-up, or table for later.

Deep dive: Partner-level review, reference calls, follow-on conversations with the founder. This is where analyst time concentrates.

Investment committee: Formal recommendation with a memo. At most funds, fewer than 5% of sourced companies reach this stage.

Term sheet / Closed: The deal is in or out. Every closed deal should feed back into the pipeline: each pass creates a data point about what the fund will and will not invest in.

Pipeline metrics worth tracking monthly: deals sourced by channel, first-screen pass rate by channel, time from sourced to first-screen decision, and conversion rate at each stage gate. Source quality by channel, not just volume, tells you where to invest more sourcing time.

The common failure mode: deals pile up at the first-screen stage because analyst bandwidth is finite and inbound volume is not. A fund that sources 80 companies a month and can first-screen 20 of them is not running a pipeline; it is running a backlog. That backlog is where most missed deals live, not in the deals that were reviewed and passed on, but in the ones that aged out of the queue before anyone looked at them.

Investment screening: turning deal flow into investment decisions

Screening is the rapid first-filter that determines which companies enter the deep-dive stage. Done well, it protects analyst time. Done poorly, it either misses good companies (too narrow) or wastes the investment committee's time with unsuitable ones (too loose).

VC screening criteria generally fall into five categories:

Sector and thesis fit: Does this company match the fund's defined investment thesis? A sector mismatch disqualifies immediately, regardless of traction metrics.

Stage fit: Is the company at the right stage for this fund's check size and ownership model? A $15 million ARR company does not belong in a fund that writes $500K pre-seed checks.

Team quality signals: Founding team background, prior exits or relevant domain experience, co-founder relationships. Analysts make most screening decisions on team quality before they finish the market analysis.

Traction evidence: Revenue, growth rate, customer count, net revenue retention, churn. The specific metrics that matter vary by stage: a pre-seed company showing 20 customer letters of intent is strong; a Series A company with the same 20 LOIs and no signed contracts is not.

Cap table clarity: Who owns what, what previous terms look like, and whether the ownership structure will create problems at the next round. A cap table with 40 angels, convertible notes with multiple conflicting valuation caps, and pro-rata rights held by every early investor is a structural problem regardless of the company's operating metrics.

The document stack in VC screening differs from what private equity due diligence requires. PE firms review confidential information memoranda (CIMs) and management presentations prepared by sell-side advisors: structured documents with standardized financial disclosures. Venture capital works with a different set of materials: pitch decks that vary in length from 8 to 40 slides, cap table files in PDF or spreadsheet format, Simple Agreement for Future Equity (SAFE) notes with variable terms, and founder-prepared financial models that range from rigorous to speculative. These documents are unstructured, inconsistent, and non-standardized. The challenge is not analytical — it is a data extraction problem: pulling consistent fields from inconsistent documents at volume.

Most funds screening 500 to 1,000 companies per year convert fewer than 3% to serious due diligence. The failure is rarely that analysts made bad decisions on the companies they reviewed; it is that the companies that received a proper first look were a small fraction of the ones that arrived. The rest aged out of the queue or received a surface-level review that missed the actual signal. For more on how AI fits into the due diligence process once a company passes the screen, that is a separate set of considerations from sourcing.

How AI handles deal sourcing at scale

The honest description of what AI does in deal sourcing is narrow: it reads documents and extracts structured data from them. It does not identify which companies are worth investing in. It does not replace the judgment call on a founding team. What it does is eliminate the manual extraction step between receiving a document and having usable information, at a speed and scale that human analysts cannot match.

The practical result: analysts spend their time on the 5% of opportunities where their judgment matters, not on extracting data from the 95% that clearly do not fit.

For a broader look at how generative AI is being applied across finance workflows, the applications extend well beyond deal sourcing — though sourcing is where the document volume problem is most acute.

Pitch deck analysis at scale

A pitch deck is an unstructured document. Slide two might be the market size slide; it might be the team slide. The founder's traction metrics might appear in a table on slide six or in a paragraph of text on slide twelve. There is no standard format, no consistent field definition, and no guarantee that the same data point appears in the same place across decks.

AI document processing handles this variability. Upload 50 pitch decks and define the fields you want extracted: founding team background, stated market size, current ARR or MRR, growth rate, funding ask, use of proceeds, key competitors named. The agent reads each deck, extracts the defined fields, and returns a structured table. The analyst reviews the table, not 50 individual PDFs.

What this produces is a screening shortlist. The agent filters out companies that clearly miss on sector, stage, or team profile — no analyst review consumed. It flags the companies that hit most criteria for follow-up. The analyst's first-screen conversation with a founder is informed by extracted data rather than starting from a blank slide.

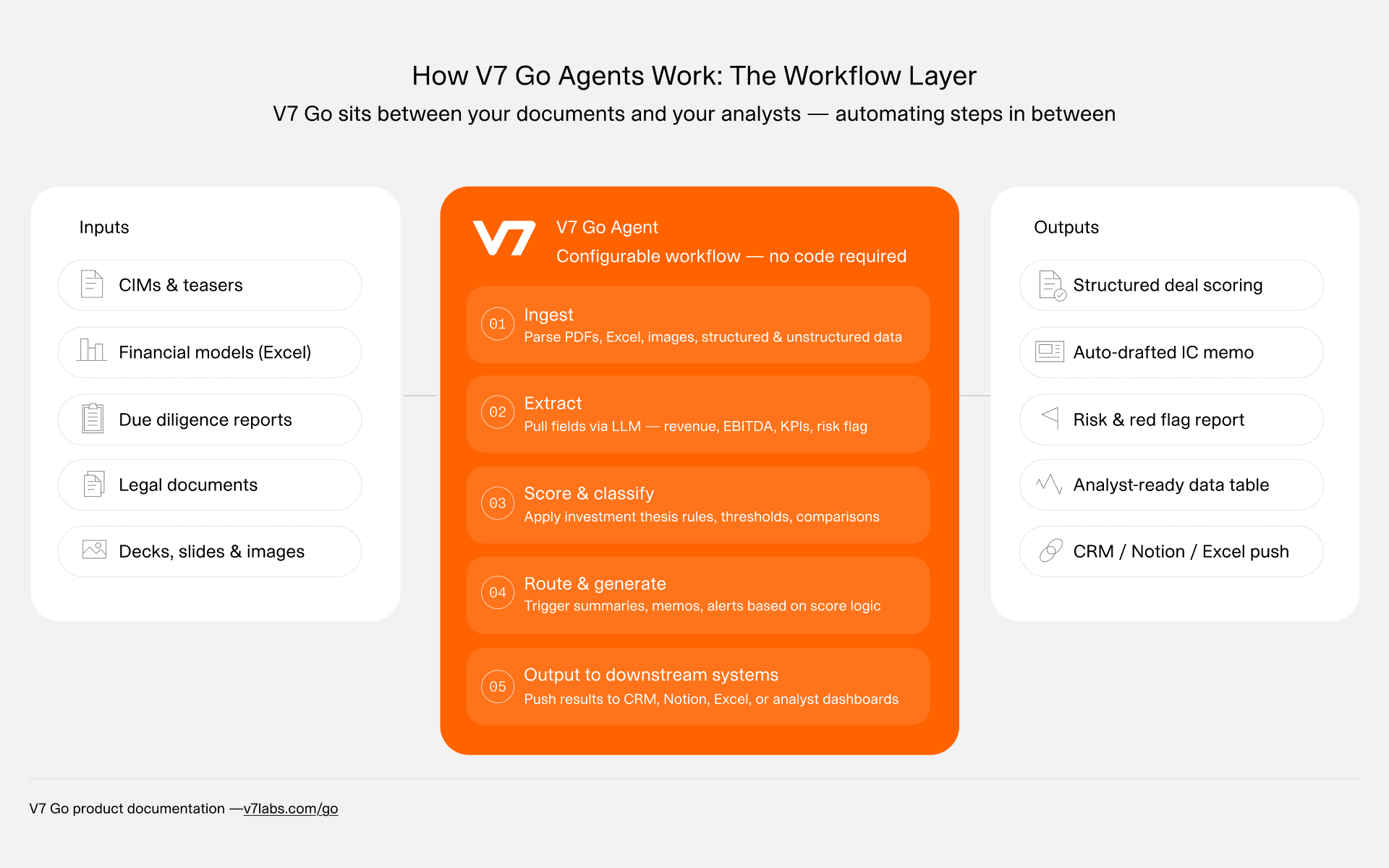

V7 Go handles this workflow directly: upload a batch of pitch decks, define the extraction schema, and the agent returns a structured output for each document. The workflow runs against new batches as they arrive. Post-demo-day processing that used to take a week completes overnight.

V7 Go agents process pitch decks and investment documents through a configurable pipeline: ingestion, extraction, scoring against thesis criteria, and routing to downstream systems.

Cap table and document screening

Cap tables are screening documents. They reveal prior investor quality (which funds invested in previous rounds, and at what valuations), dilution trajectory (how much founder ownership remains at the current round), and structural complexity (how many convertible notes, SAFEs, and pro-rata rights are layered into the cap).

SAFE agreements and convertible notes contain terms that directly affect future round economics: valuation caps, discount rates, most-favored-nation (MFN) clauses, and pro-rata rights. A company with a $3 million SAFE round that includes a $6 million valuation cap and an MFN clause may look straightforward until you calculate what the effective pre-money valuation will be at the priced round. That calculation is deterministic. It does not require judgment. It requires reading the document and running the arithmetic.

AI extracts these terms without analyst time. The agent reads every cap table in the pipeline, pulls the key fields, and surfaces the ownership structure in a format the analyst can review in minutes rather than hours. For a fund reviewing 50 companies per month, this frees several days of analyst time: time that goes to founder conversations, reference calls, and actual judgment work instead of document parsing.

For teams managing the full cap table management workflow across a portfolio, the tooling requirements extend beyond screening, but the extraction problem is the same at every stage.

Investment thesis matching at scale

The highest-leverage application of AI in VC deal sourcing is thesis matching: running every sourced company against a defined set of criteria and returning a ranked shortlist. The analyst reviews the shortlist, not the full pipeline.

The workflow: define the thesis criteria as a structured schema (sector tags, stage range, ARR threshold, geography, team profile requirements, deal-breaker flags). Upload the sourced companies' pitch decks and cap tables. The agent reads each document, extracts the relevant fields, scores each company against the schema, and flags deals that meet the threshold for analyst review.

The result is not that AI replaces analyst judgment. The analyst still decides which companies to pursue. What changes is what the analyst is looking at when they make that decision: they review the 10% of deals that passed the automated screen, not the 100% that arrived. The 90% that clearly do not fit get a fast, consistent first-filter rather than aging out of a backlog.

V7 Go's AI due diligence agent and investment memo generation workflow extend this further. Once a company passes the screen, the same infrastructure that processed the pitch deck can begin the deeper extraction needed for the IC memo. The pipeline from sourcing to investment committee becomes a connected workflow rather than a sequence of manual handoffs.

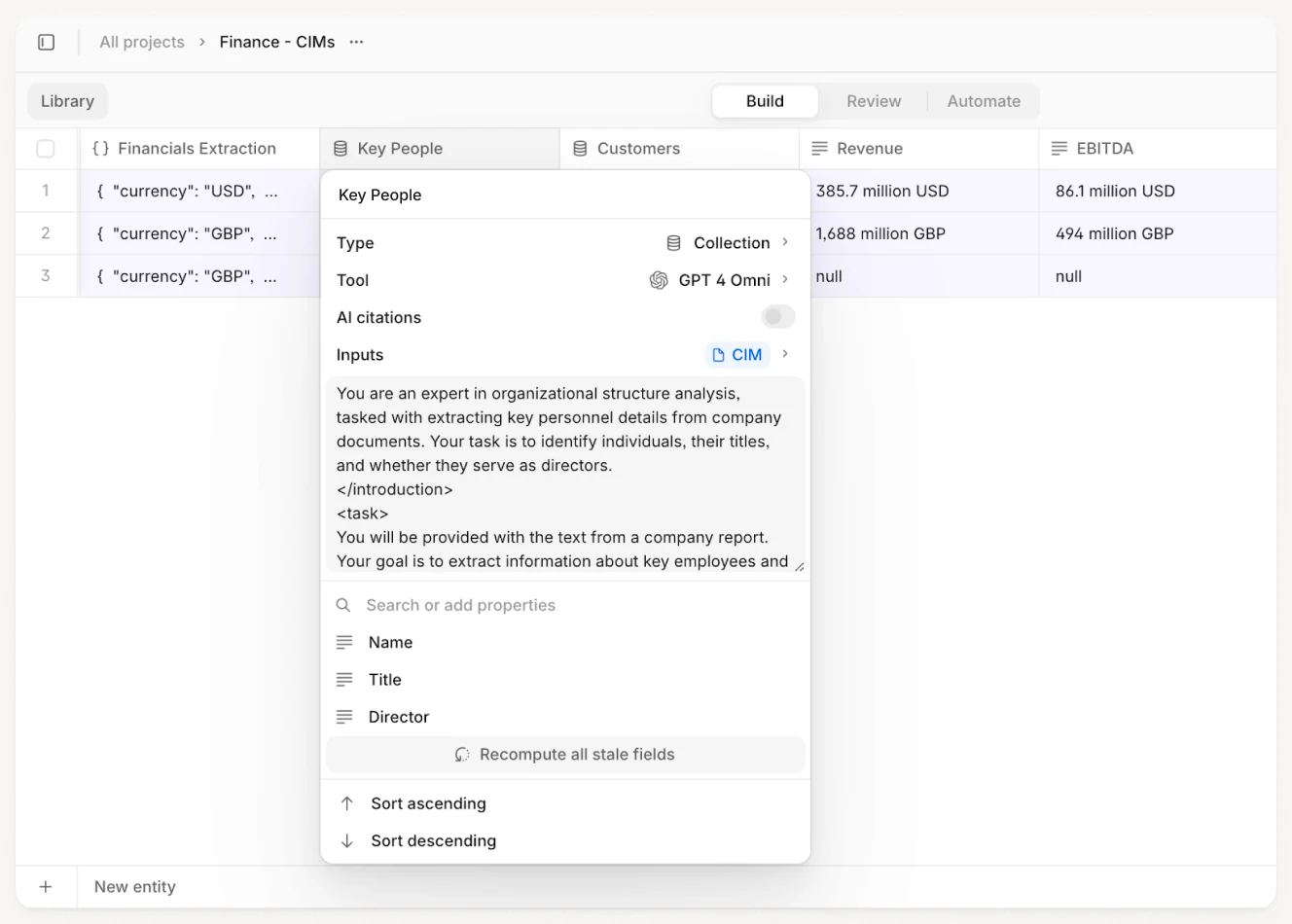

V7 Go lets VC teams build document processing workflows for pitch decks, cap tables, and term sheets without engineering resources. See how VC teams use V7 Go for dataroom-to-IC-memo workflows.

V7 Go extracts structured fields from investment documents, whether pitch decks, CIMs, or cap tables, and returns analyst-ready data without manual review of every source file.

How do VCs source deals?

VCs source deals through a combination of inbound and outbound methods. Inbound deal flow arrives via referrals from portfolio founders, LP introductions, and warm connections from other investors. Quality inbound typically comes from trusted relationships built over years. Outbound sourcing is more deliberate: VCs map their target sectors using platforms like Crunchbase and PitchBook, attend accelerator demo days at programs like Y Combinator and Techstars, build relationships with university tech transfer offices, and reach out directly to founders who fit their investment thesis before those founders have started a formal fundraise. Most funds also maintain CRM systems to track every founder interaction and referral chain. Data-sourcing platforms like Harmonic and Grata help identify companies that are growing quickly but have not yet appeared in standard databases. The most effective sourcing programs combine strong brand, which drives quality inbound, with a systematic outbound process that surfaces deals before they become competitive. The allocation between inbound and outbound depends on fund size, sector focus, and stage.

+

What is the difference between deal sourcing and deal flow?

Deal flow and deal sourcing describe different things, though the terms are often used interchangeably. Deal flow is the ongoing stream of investment opportunities that arrives at a fund: inbound emails, referrals, portfolio introductions, banker-submitted opportunities, and cold outreach from founders. It describes the pipeline that exists at any given moment. Deal sourcing is the deliberate activity that generates and shapes that pipeline. It includes building relationships with founders before they are raising, mapping target sectors systematically, attending events and accelerator demo days, and running outbound campaigns to companies that fit the investment thesis. The distinction matters operationally: a fund that only manages its deal flow is reactive, reviewing whatever arrives and deciding whether to pursue it. A fund that actively sources deals is proactive, identifying promising companies before they run a formal process, which typically means lower competition and better entry terms. Strong deal flow is a lagging indicator of good sourcing. The sourcing activity comes first; the deal flow is the result.

+

What is a good deal flow for a VC?

A good deal flow for a VC generates enough volume at each stage to produce the number of investments the fund needs, while maintaining a quality level that makes the review work tractable for the team's size. In practice, most funds targeting two to four investments per year need to source between 500 and 1,500 companies annually, convert roughly 5 to 10 percent to meaningful first conversations, and move fewer than 5 percent to deep diligence. The specific volume depends on stage and sector: a highly focused pre-seed fund investing in a narrow vertical might only see 200 companies per year and invest in four to six. A generalist multi-stage fund might see 2,000 opportunities and close eight to twelve deals. What makes deal flow good is not raw volume but source quality. Deal flow sourced through portfolio founder referrals, trusted angel networks, and direct outbound typically converts to investments at a higher rate than cold inbound. Tracking conversion rates by source channel is the practical way to identify where a fund's deal flow is actually strong versus where it only appears to be.

+

How do you build deal flow as a new VC?

Building deal flow as a new fund or first-time investor requires constructing credibility before you have the track record to attract it organically. The most reliable early-stage tactics: pick two to three sectors and go deep, attending every relevant conference, reading meaningful research, and becoming known as a knowledgeable investor before you have a portfolio to show. Publish publicly on LinkedIn or Substack about trends in your focus areas; founders and other investors who find your analysis useful become referral sources. Build relationships with angels who are active in your target sectors and with accelerator program managers who see early companies before they raise. Offer genuine value to early founders you cannot yet invest in: introductions, customer referrals, feedback on their decks. These relationships compound over two to three years into a referral network that generates proprietary deal flow. Track every company you meet, every referral source, and every pass rationale in a CRM from day one. The database becomes a competitive asset as the fund matures.

+

Can AI replace VC deal sourcing?

During initial deal sourcing and first-screen evaluation, VCs typically review a shorter set of documents than what appears later in due diligence. At the sourcing stage: pitch decks covering team, market, product, traction, and fundraising ask; one-pagers or executive summaries for very early companies; and cap tables in PDF or spreadsheet format when available. For companies that have already raised capital, SAFE agreements and convertible note terms become relevant at the first-screen stage because they directly affect what the current round's economics will look like. Some funds also review founder-prepared financial models at first screen; others reserve that for the deep-dive stage. The document stack at the sourcing stage differs significantly from private equity screening, which involves standardized confidential information memoranda prepared by sell-side advisors. Venture documents are founder-prepared, non-standardized, and variable in quality and format. This is the core reason that volume-based VC screening creates a data extraction problem: the same information appears in different places across decks, with different levels of specificity.

+

What documents do VCs review during deal sourcing?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.