Document processing

13 min read

—

The line appears in virtually every GP pitch deck. "We generate primarily proprietary deal flow through our deep industry relationships." It sits between the team slide and the track record table, stated with quiet confidence, rarely challenged.

This reflects what decades of practitioners have known but rarely say in an investor meeting: most private equity deals are not proprietary. They are competitive. And the firms that perform best have usually figured out a different edge than the one they advertise.

This piece is about that gap. Where deal flow actually comes from, why the proprietary story persists, what the research shows about performance, and where the real competitive edge in deal sourcing now comes from for firms willing to be honest about it.

Why "proprietary" almost never means what GPs imply in their LP pitches

What Bain's research shows about the IRR gap between proprietary and intermediary-sourced deals

How competitive deal processes actually work, from the "negotiauction" to the second-round shortlist

The real edge: processing speed, CIM depth, and institutional memory built from declined deals

Where lower middle market sourcing genuinely works differently, and where even that advantage depends on process

AI for document processing

Build real deal sourcing workflows without the manual work

Get started today

The proprietary deal: what GPs mean, what they get

Ask ten GPs to define proprietary deal flow and you will get twelve definitions. At the strict end: a transaction in which the GP is the only counterparty in conversation with the seller, no intermediary is involved, and price is negotiated bilaterally. At the loose end: any deal where the GP did not receive a banker's teaser. In practice, most firms operate somewhere in the middle of that spectrum and call it proprietary.

The research is less forgiving. Axial's deal sourcing research found that the median private equity firm captures roughly 18% of relevant deals in its target market. That figure covers all sourced deals, including intermediary-run processes. The implication is that the vast majority of available opportunities never reach a given GP's desk at all, not that the deals that do arrive are exclusive.

Bain's research on the performance dimension is more direct. Funds where more than half of closed deals originated from proprietary sourcing delivered a median internal rate of return of 23%, against 16% for funds that relied heavily on intermediaries. That is a meaningful gap. It also does not mean that proprietary sourcing is achievable at scale: it means that when firms do access non-intermediated transactions, they tend to get better entry prices and therefore better outcomes.

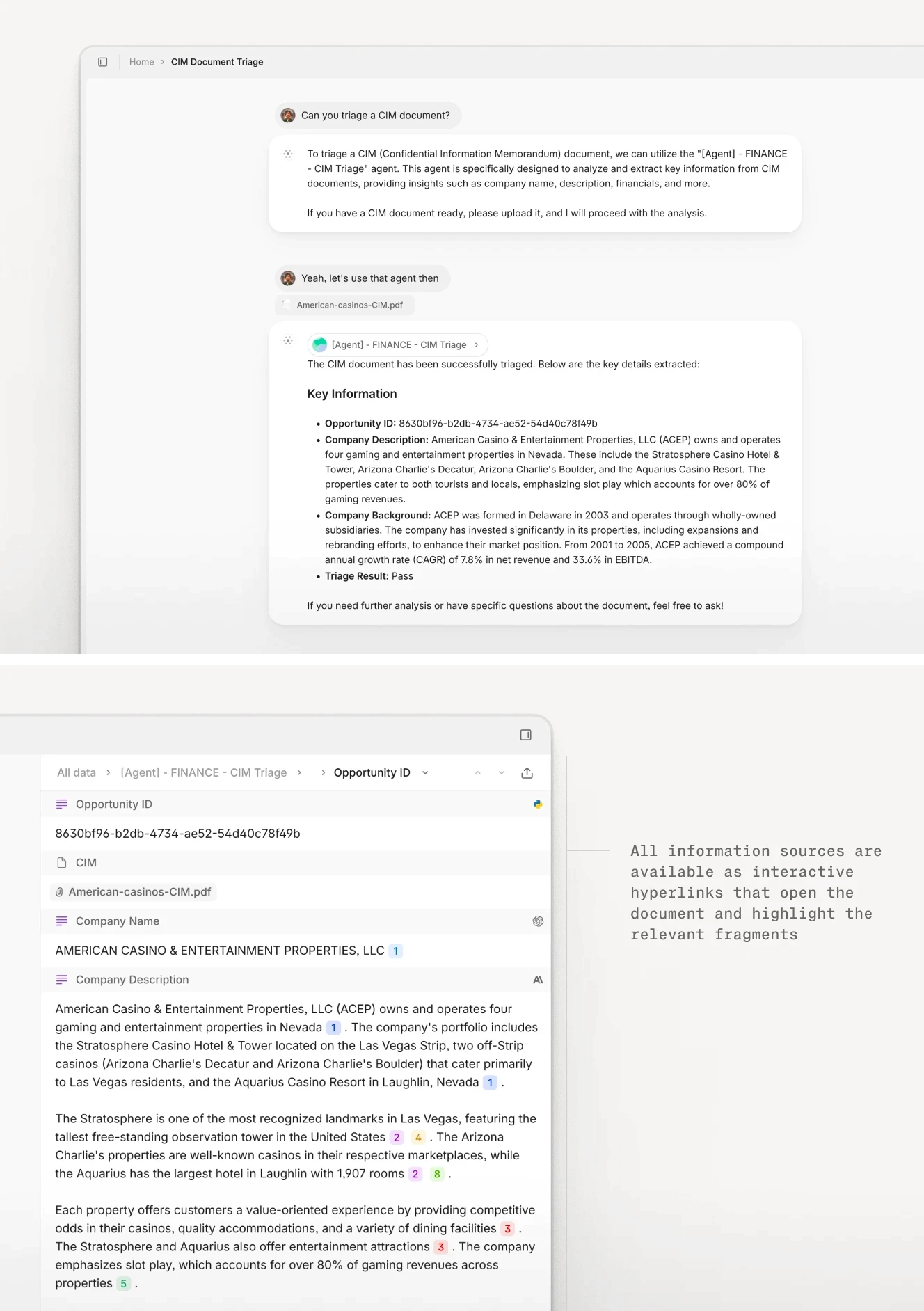

An AI triage workflow extracting key financial metrics from a CIM. The same document that takes an analyst a day to review manually can be processed in minutes when the extraction schema is predefined.

How the definition keeps moving

When a deal is sourced directly from a founder who called the GP personally: genuinely proprietary. When the GP heard about it informally from an accountant two days before the teaser went out: the GP will call it proprietary, but the accountant probably made the same call to three other firms. When a banker ran a "limited" process with five carefully selected buyers: every one of those five will describe it as a proprietary conversation in their next fund pitch.

Harvard Business School research coined the term "negotiauction" for processes that blend elements of both auction and direct negotiation. The typical mid-market deal is precisely this: formally structured enough that multiple buyers are involved at some stage, but not a full open-market auction. GPs who participate in these processes and end up as preferred buyers will often report the deal as proprietary. The seller's banker describes it as a tightly managed process. Both are technically accurate.

The Private Equity Toolkit is explicit about what the actual sourcing landscape looks like at the firm level: systematic deal sourcing requires turning reactive activities into intentional routines. Most of what practitioners experience as "proprietary flow" is the output of those routines: consistent coverage of sector events, maintained relationships with accountants and lawyers who call before they call a banker, rather than genuinely exclusive access.

The competitive reality in a typical deal is more stark. In secondary-round processes for larger transactions, it is common for three to six serious bidders to remain after the first-round shortlist. Each of those bidders arrived through a different channel. Most of them will call the deal proprietary.

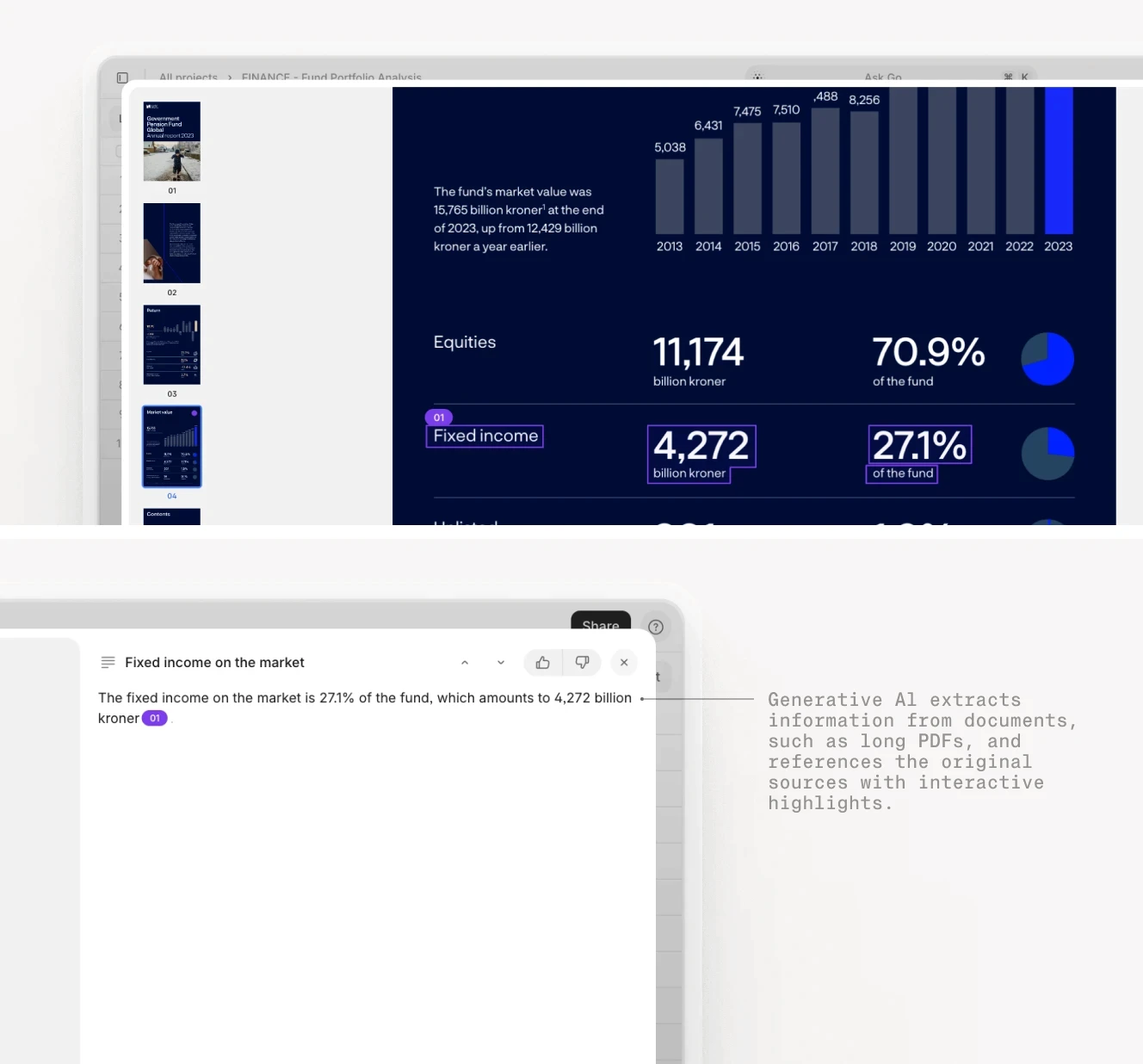

Portfolio-level analytics require structured data extraction from every underlying document. The challenge scales directly with the number of deals reviewed.

Why GPs keep saying it

The LP dynamics are straightforward. "We participate in competitive banker auctions with fifteen other bidders" is not a fundraising pitch. The GP narrative requires differentiation on sourcing even when the differentiation is largely fictitious.

Selection bias reinforces this. When a bilaterally negotiated deal returns 4x net, the GP attributes the outcome at least partly to the proprietary entry: bought at a fair price, not an auction premium. When a banker-run deal returns 5x, the entry mechanism becomes irrelevant and the thesis gets the credit. Over a fund cycle, GPs genuinely come to believe their own sourcing story because the deals they remember most clearly are the ones where the narrative held.

The persistence of the claim is also structural. LPs rarely have the information to challenge it. Track record attribution by sourcing channel is not a standard disclosure. The ILPA Principles set templates for fee, performance, and governance reporting, but deal-by-deal sourcing attribution is not part of the framework. GPs self-report.

Add-on acquisitions complicate the picture in the GP's favor. In 2024, add-ons accounted for approximately 74% of all private equity deals, according to the Harvard Law School corporate governance review of 2024 private equity activity. Add-ons are often genuinely less competitive: the platform company has an existing commercial relationship with the target, proprietary insight into the target's operations, and a buyer identity that makes it the natural acquirer. When GPs claim strong proprietary flow, they are often describing a concentrated add-on program where the claim is actually defensible.

But add-ons are not the same as original platform sourcing. And the distinction matters for how LPs should evaluate sourcing claims.

Where the edge actually comes from

Wrong answer: see more exclusive deals.

The firms that consistently outperform on deal sourcing are not the ones with the most exclusive access. They are the ones that process the most opportunities with the most depth, reject bad deals faster, and build a compounding intelligence base from everything they look at. Access is static. Process improves.

Kyung-Ah Park's Two and Twenty describes a deal team that won a competitive process not because they had a proprietary position, but because their "accuracy and speed" made them look, to the seller, "as if they have been a fly on the wall for years." The indication of interest they submitted reflected depth of analysis that the other bidders had not achieved in the same timeframe. That depth, the ability to know a target's unit economics, competitive position, and management history as well as or better than the target's own advisers, is what actually wins deals. The deal was not proprietary. The preparation was.

The conversion rate data supports this framing. Only about 1.48% of deals that private equity firms source actually transact. The average firm evaluates roughly 80 opportunities before closing a single investment. At that ratio, the firm that can review three times more CIMs per analyst per month does not need the same level of exclusive access to close the same number of deals. The funnel is wide enough that throughput matters more than exclusivity.

The CIM as a competitive test

A Confidential Information Memorandum is a marketing document. Its function is to present the target in the best possible light while technically disclosing enough to satisfy legal requirements. An experienced deal team reads a CIM the way an experienced reader reads a political speech: it is not what is said but what is conspicuously absent that carries the real signal.

Customer concentration buried in a single paragraph. Normalized EBITDA that adds back items which will recur. A management team section that describes current roles without mentioning previous tenures. Covenant headroom presented as adequate without specifying the threshold. Every CIM contains these patterns. Finding them reliably, at speed, is a skill that determines whether a firm submits an IOI grounded in reality or one that reflects the seller's narrative back at them.

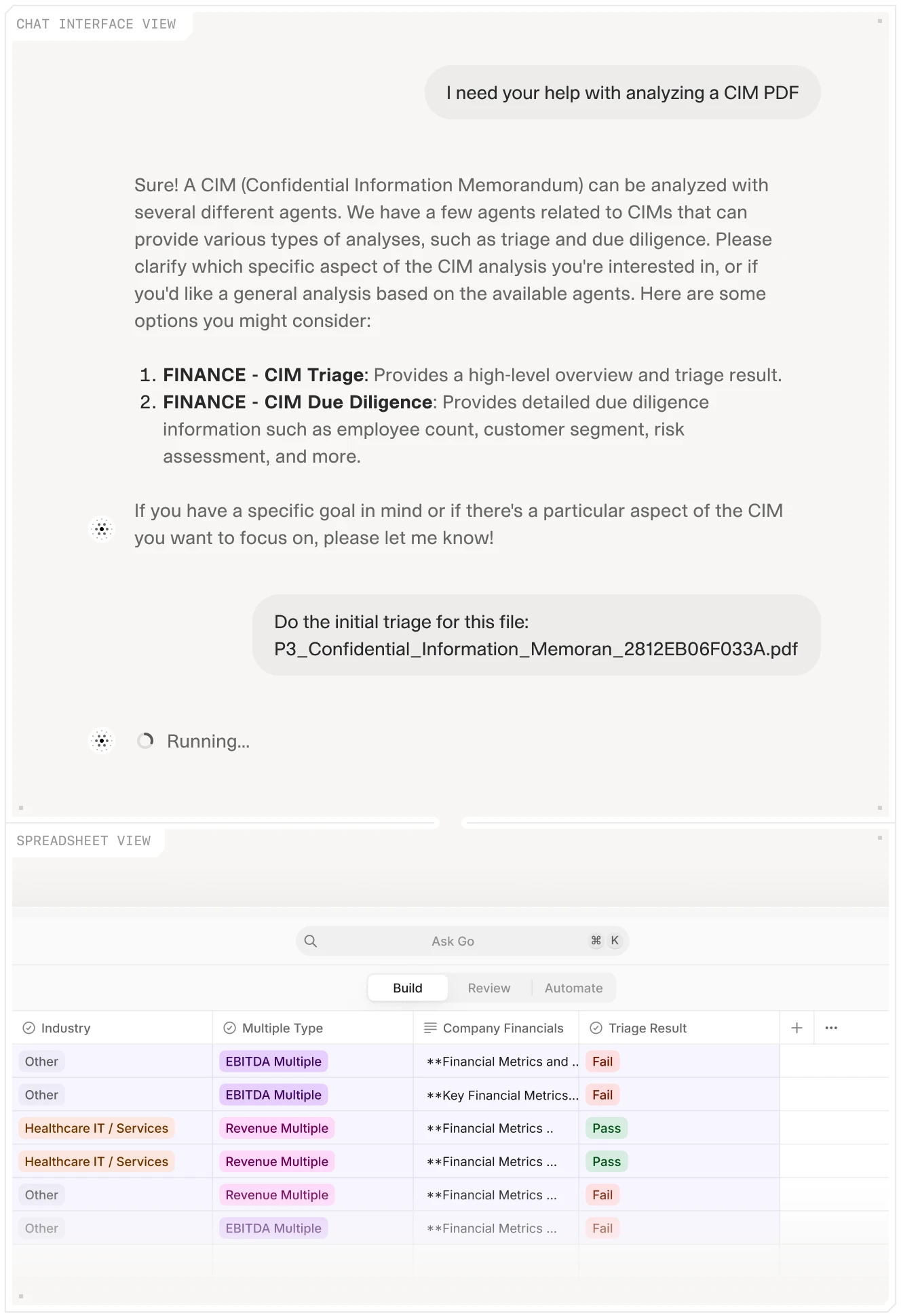

This is precisely the problem that automated CIM review addresses. Define an extraction schema once: revenue, EBITDA, add-backs, customer concentration, management tenure, competitive landscape, and debt capacity. Apply it consistently to every CIM that enters the pipeline. One PE team reduced CIM review from a full analyst day to under ten minutes per document. The reduction is not in quality; it is in the mechanical extraction work that precedes the actual judgment call.

The AI PE screening and deal flow agent takes this a step further: it reads the CIM, scores the opportunity against the fund's investment thesis, flags red flags from the document, and produces a standardized summary that the deal team can act on. The analyst's job becomes reviewing structured output and making the judgment call, not extracting raw data from a 90-page PDF.

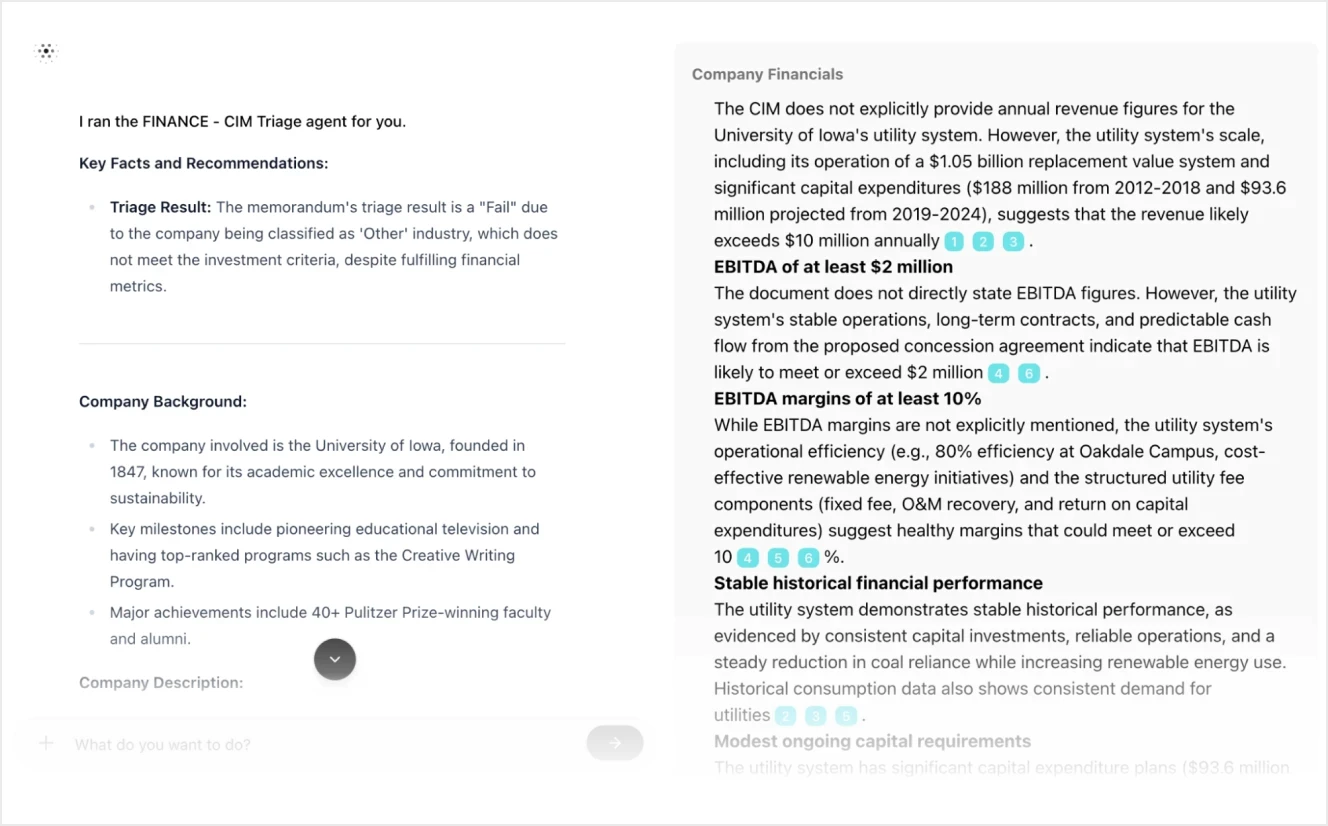

A CIM triage agent surfaces the data that matters: revenue, EBITDA, customer risk, and debt structure. It surfaces this in a format the deal team can act on within hours rather than days.

Institutional memory: what happens to the deals you pass on

The median mid-market PE firm passes on more than 98 out of every 100 deals it reviews. That is an enormous dataset. At most firms, it is also almost entirely inaccessible.

The declined deals live in email threads, internal memos, and the memories of analysts who left for business school three years ago. When a similar company comes through the pipeline eighteen months later, the firm effectively starts from scratch: re-building the sector model, re-evaluating the customer concentration question, re-litigating the management team assessment that was settled the last time. The institutional memory exists, theoretically. It is not retrievable.

This is the less visible sourcing edge, and it compounds in a way that exclusive access never does. A firm that captures the reasoning behind every declined deal, structured consistently, builds something genuinely proprietary over time: a living model of what the sector looks like, what good companies within it share, and what the red flags look like before they appear in the headline numbers.

The AI deal flow synthesis agent is designed exactly for this: every CIM processed becomes part of a searchable knowledge base. When the next deal in the same sector arrives, the extraction runs against the same schema and the output lands in the same structured format as the previous 40 deals in that space. The firm is faster. More importantly, it is comparing the new deal to a dataset the competitor does not have.

Every reviewed CIM contributes to an institutional knowledge base. The second deal in a sector is analyzed against the first; the tenth against nine prior observations.

When proprietary sourcing is genuinely real

The lower middle market is different. Not different in principle. The competitive dynamics of price still apply. But different in structure.

A founder-owned manufacturing business with USD 8M in EBITDA has likely never worked with an investment banker. The owner has a relationship with a local accountant, maybe a regional lending bank, and peers in the industry trade association. The GP that has spent three years attending the same industry conference, developing a reputation as a buyer who completes deals and doesn't retrade, and staying in genuine contact with that accountant is in a meaningfully different position than a firm that receives the same opportunity through a process run six months later.

At this market level, the sourcing claim holds. The GP that arrives first, with credibility already established, has a material pricing advantage. The seller does not want the uncertainty of a banker process. The transaction is bilateral in a meaningful sense.

But even here, the advantage is not static. The GP managing 40 relationship conversations simultaneously, with structured follow-up and systematic sector research, covers the same ground more thoroughly than one relying on relationship memory. The market analysis agent can map a target sector, identifying comparable companies, recent transactions, and buyer activity, in a fraction of the time a junior analyst would spend on the same research. The GP focused on genuine lower-middle-market origination benefits from AI not by replacing relationship work but by expanding the volume of companies they can meaningfully track.

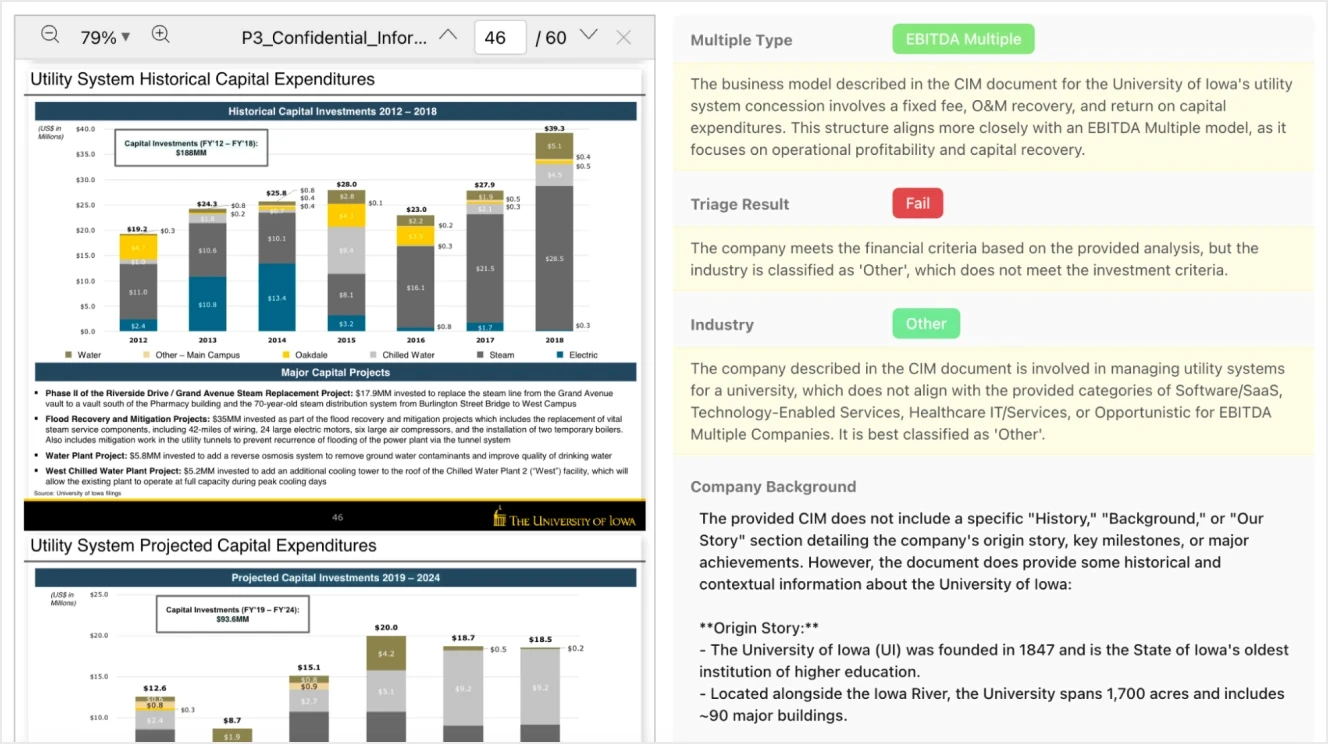

The AI Concierge delegates CIM analysis to the right specialist agent, then surfaces extracted financials alongside qualitative flags. The deal team makes the decision; the agent handles the extraction.

Speed as credibility: what sellers actually observe

A seller who has engaged a banker to run a limited process receives first-round indications of interest from eight qualified buyers. Four arrive within a week. Four arrive in the third week, with a request for a two-week extension.

The seller does not know which group has done better analysis. What they observe is who took the process seriously. Early, clean, research-grounded IOIs signal internal alignment, sector conviction, and a deal team that does not need to wait for a committee meeting to approve a preliminary view. Late, hedged IOIs signal the opposite.

This dynamic is well understood by experienced deal teams. What is less well understood is that it is now addressable through process rather than through headcount. A five-person deal team that has pre-defined its investment thesis, built a structured extraction schema for CIM review, and connected that schema to a standardized triage output can turn a 90-page CIM into a first-pass IC summary in under a day. A ten-person team without those structures may still be in the Excel stage three days later.

The AI deal screening and triage agent operationalizes this: one analyst configures the extraction schema for the fund's target sector, the agent processes each new CIM against that schema, and the output arrives in the same structured format regardless of who conducted the review. Consistency across analysts eliminates the quality variance that comes from relying on whoever happens to be least overloaded that week.

The seller's banker, evaluating which buyers seem serious, is reading these signals even if they do not name them explicitly. Being the firm that sends the credible IOI first is worth more than the proprietary sourcing claim in the fund pitch ever was.

The metric that actually matters

Most PE deal teams track the wrong numbers on sourcing. Pipeline volume. Deals reviewed. Intermediary relationships maintained. These are activity metrics, not outcome metrics.

The sourcing metric that correlates with outcomes is IOI turnaround time: how long it takes the team to go from receiving a CIM to submitting a credible, research-grounded indication of interest. A firm that can turn this around in 24 to 48 hours is signaling to the seller and their banker something about internal discipline, sector conviction, and decision-making clarity that a two-week timeline does not. Speed is a proxy for preparation.

The second metric worth tracking: the quality of the first-pass triage. Not whether it is correct in every detail, but whether it is structured consistently enough to compare against prior deals in the same sector. A triage memo that captures twelve comparable data points in the same format for every deal in a vertical is qualitatively different from one that reflects whatever the reviewing analyst happened to focus on that day.

The AI investment memo generation workflow and the due diligence AI workflow both reflect the same principle: define the standard once, enforce it mechanically across every deal, and reserve the analyst's judgment for the decisions that actually require judgment. Proprietary access is one edge. Proprietary process is a different one. And unlike access, process can be systematically built.

The honest LP conversation

Accepting this reframing does not require changing the LP pitch. It requires sharpening it.

"We have a proprietary sourcing strategy" can honestly mean: "Our deal team turns around a research-grounded IOI in 48 hours. We have reviewed 400 deals in this sector over the last five years and captured the reasoning behind every one. When a new deal arrives, we are comparing it against a structured dataset the seller's other counterparties do not have. And in the lower middle market, where our primary platform sourcing happens, we have built genuine relationships over years that give us access to conversations that never go to a banker."

That is a proprietary sourcing claim. It is also an accurate one.

The firms that will outperform on sourcing over the next decade are not the ones with the most exclusive network. Networks commoditize. Information travels. The firms that build a document intelligence flywheel: every CIM reviewed makes the next review faster and the triage more accurate. The advantage compounds in a way that relationship cultivation alone does not. The deal you see proprietary today is the one you can evaluate with the most precision because you have seen ninety similar deals before it.

That is a different kind of edge. It is also the one worth building.

What is proprietary deal flow in private equity?

Proprietary deal flow refers to investment opportunities a private equity firm accesses before or outside a formal intermediary-run sale process. In strict terms, it means the GP is the only buyer in conversation with the seller, with no investment banker involved and price negotiated bilaterally. In practice, the term is used loosely to describe any situation where the GP had early or exclusive access relative to other buyers, even if a banker was involved at some stage. The Private Equity Toolkit describes the search for the fully proprietary deal as mythical at scale, because most sellers eventually optimize for competitive pricing.

+

How do private equity firms source deals?

PE firms source deals through several channels: investment bank-run auction processes (where the banker sends a teaser and information memorandum to a list of qualified buyers), direct outreach to companies that match the firm's investment thesis, relationships with accountants, lawyers, and lenders who refer clients before a formal process begins, and add-on acquisitions where the platform company identifies and approaches targets in its sector. In practice, the large majority of deals at any given firm come through intermediaries in some form, though the degree of competition varies. Lower middle market firms with narrow sector focus are more likely to access genuinely bilateral transactions.

+

What percentage of PE deals come from intermediaries?

Precise figures vary by firm size and strategy, but Bain's research found that funds with more than 50% proprietary deal flow delivered median IRRs of 23%, versus 16% for funds relying heavily on intermediaries, suggesting that most funds do lean toward intermediary-sourced deals. Axial's deal sourcing research found that the median PE firm captures only 18% of relevant deal flow in its target markets, which underscores how competitive and fragmented the sourcing landscape is. In large-cap buyouts, nearly all deals are banker-run. In the lower middle market, founder-to-GP direct transactions are more common, particularly for firms with established sector reputations.

+

How does AI improve private equity deal sourcing?

AI improves deal sourcing primarily through CIM analysis speed and consistency. An AI CIM review agent extracts standardized data fields from every information memorandum the firm receives: revenue, EBITDA, add-backs, customer concentration, management tenure, debt capacity, competitive position. This reduces the extraction time from a full analyst day to under an hour per document, allowing the team to cover more opportunities without increasing headcount. The second improvement is institutional memory: when extraction follows a consistent schema, every reviewed deal becomes a comparable data point. A firm that has processed 300 CIMs in a target sector with structured output has a research advantage over one starting fresh each time. AI market analysis agents also accelerate sector mapping, helping relationship-based sourcing teams identify relevant companies faster.

+

What is the difference between proprietary and auction processes in PE?

The practical approach is to define a standard extraction schema for every CIM reviewed: a fixed set of data fields captured consistently regardless of which analyst conducts the review. When the schema is applied systematically, declined deals accumulate as structured data rather than anecdotal memory. A firm that has reviewed 400 deals in industrial distribution over five years and captured EBITDA margin, customer concentration, management tenure, and leverage profile for each has a model of what the sector looks like that no new entrant can replicate quickly. AI document agents make this feasible at scale by automating the extraction step. The analyst reviews the structured output and records the investment decision and rationale. Over time, the firm builds a proprietary dataset from public-ish documents, which is a durable form of competitive advantage in sourcing.

+

How can PE firms build institutional memory from declined deals?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.