15 min read

—

In every commercial real estate acquisition, the title and survey package ranks among the most consequential and most document-intensive components of due diligence. A title commitment can run 20 to over 100 pages of schedules, exhibits, and exception documents. The ALTA survey introduces boundary, encroachment, and access complexity that must be cross-referenced against the commitment line by line.

This guide is written for real estate counsel, acquisition analysts, and title officers reviewing these documents on active deals — institutional commercial real estate, not residential transactions. It covers what each document contains, what to look for at every stage of review, and how AI compresses the review cycle from days to hours.

In this article:

What a title commitment is and how its three schedules are structured

What an ALTA/NSPS survey shows and why it matters for Schedule B-II

The review process and the Title and Survey Memo that records it

Specific red flags in both documents that require further action

How AI automates extraction, cross-referencing, and T&S Memo drafting

AI for document processing

Review title commitments and ALTA surveys in minutes

Get started today

What Is a Title Commitment in Commercial Real Estate?

A title commitment is a written promise by a title insurance company to issue a title insurance policy, subject to the conditions and exceptions set out in its schedules. It is not a policy. It is the title company's conditional offer to insure, delivered after the title search is complete and before the policy is issued at closing.

The commitment arrives early in the due diligence cycle. In most commercial real estate acquisitions, it is the first document delivered to buyer's counsel after the purchase and sale agreement is executed. The effective date matters: defects recorded after that date are outside the title company's search and fall outside the eventual policy's coverage.

The major title companies (First American, Fidelity National Title, Stewart Title, Chicago Title, and Old Republic) issue ALTA-form commitments with a consistent three-schedule structure.

Schedule A: The Transaction Terms

Schedule A records the basic transaction parameters: the property's legal description, the proposed amount of insurance, the proposed insured (buyer and lender separately), the type of policy to be issued (typically an ALTA Owner's Policy and an ALTA Loan Policy), and the commitment's effective date.

This schedule is the foundation for cross-referencing. The legal description in Schedule A must match the legal description that the surveyor certifies in the ALTA survey. Any discrepancy signals either a data entry error or a genuine boundary problem, and both require resolution before closing.

Schedule B-I: Requirements

Schedule B-I lists the conditions the title company requires satisfied before it will issue the policy. Common requirements include: satisfaction of existing mortgages and deeds of trust, payment of delinquent taxes and special assessments, delivery of corporate or LLC authority documentation, gap indemnities, and execution of affidavits.

The review task is to distinguish routine requirements (which the closing attorney handles in standard practice) from outstanding title problems that require negotiation, court action, or renegotiation of deal terms. A requirement calling for a court order to clear a disputed boundary is not routine. A requirement calling for payoff of the seller's existing mortgage is.

Schedule B-II: Exceptions

Schedule B-II lists what the title insurance policy will not cover. This is the most critical review area in the entire title commitment.

Every exception is a limitation on the protection the buyer and lender receive. Standard exceptions appear in virtually every ALTA commitment: matters of survey, rights of parties in possession, unrecorded liens. Special exceptions are property-specific: a recorded utility easement, a deed restriction limiting use to office occupancy, a pending mechanic's lien.

The review questions for every Schedule B-II exception are consistent. Does this exception affect the buyer's intended use? Does it affect the lender's collateral value? Can it be removed before closing? And, critically, is it already shown on the ALTA survey?

What Is an ALTA/NSPS Land Title Survey?

An ALTA/NSPS Land Title Survey is the highest standard of real property survey in the United States, defined jointly by the American Land Title Association and the National Society of Professional Surveyors. It is what commercial lenders and title companies require when the standard survey exception must be removed from Schedule B-II.

The survey shows the property's boundary lines and dimensions, improvements on the land, easements and rights-of-way, encroachments onto or off the property, access to public roads, FEMA flood zone designation, and setback lines. Optional Table A items (requested by the buyer or lender) can add topography, utilities, zoning, parking counts, building square footage, and interior lease layout.

The certification runs to the buyer, the lender, and the title company. Most transactions require a survey dated within six months of closing. A stale survey requires re-certification or a new run, adding time and cost to the due diligence cycle.

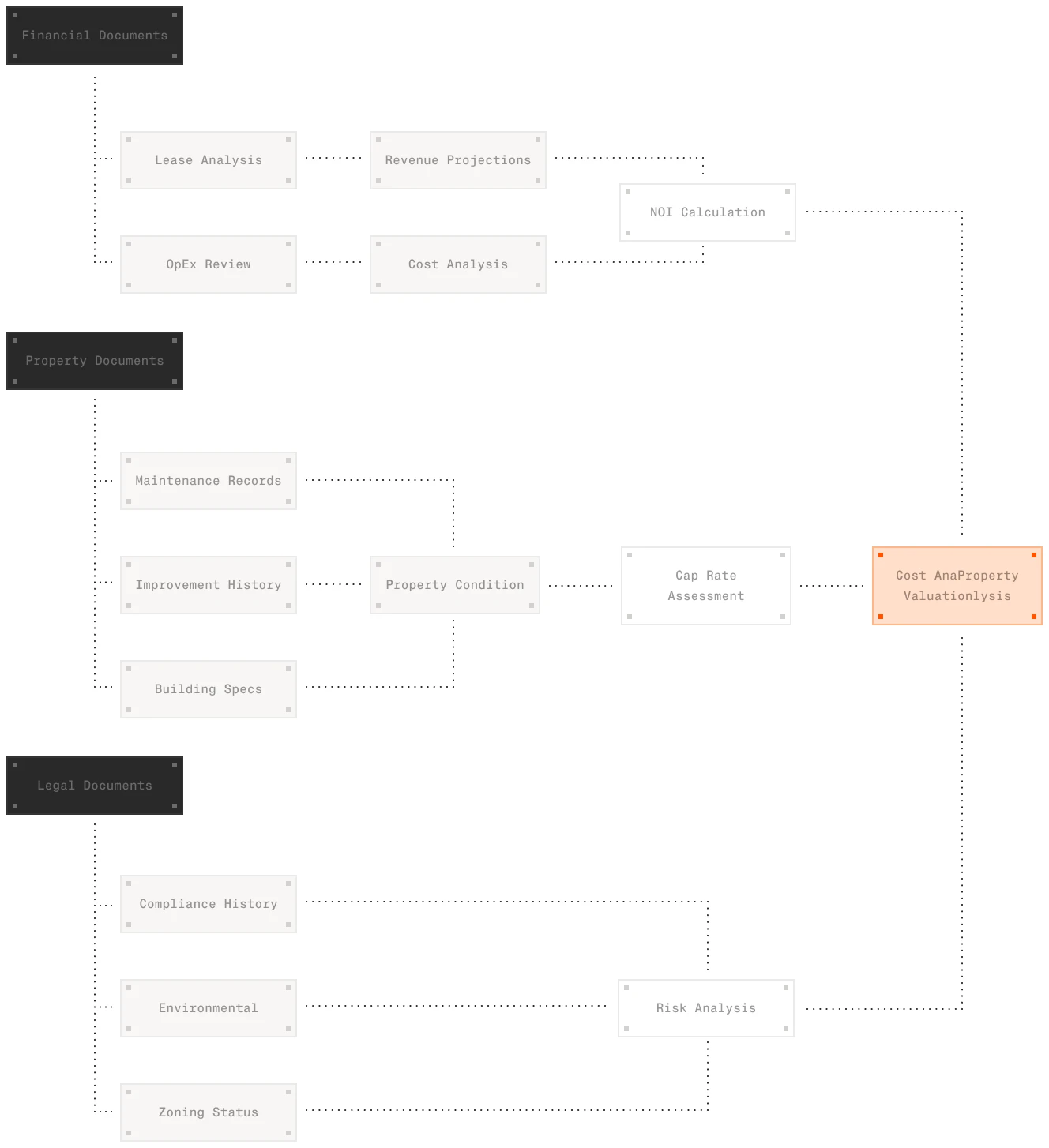

The ALTA survey does not replace the title commitment. It complements it. The commitment tells you what exceptions exist on record; the survey tells you where they are on the ground. Together, they form the complete picture that acquisition teams need before closing. For a broader look at technology's role across the CRE investment workflow, see our guide to AI in commercial real estate investment.

The Title and Survey Review Process in CRE Due Diligence

Both documents are typically ordered immediately after PSA execution, with active review beginning in weeks one through three of the due diligence period. Real estate counsel takes primary responsibility. On larger acquisitions, analysts support the review, and the title officer provides interpretive guidance on ambiguous exceptions.

The critical requirement is paired review. Title commitment and ALTA survey must be analysed together, not sequentially. Schedule B-II exceptions must be mapped to the survey; survey easements must be traced to Schedule B-II. Discrepancies between the two documents are where the most material title issues surface.

The output of the review is the Title and Survey Memo (T&S Memo): a structured summary that identifies every material exception, maps each to the survey where possible, categorises issues by materiality (deal-stopper, negotiable, note-and-accept), and recommends curative actions or insurance endorsements.

Traditional review runs $3,000 to $8,000 in legal fees and takes two to three weeks for a comprehensive package. On portfolios or deals with complex encumbrance histories, time and cost increase proportionally. This expense compounds on deals that do not close, since the review cost is sunk regardless of outcome. For the broader impact of AI on transaction due diligence costs, see our analysis of AI in due diligence.

What to Look for in a Title Commitment

Experienced real estate counsel reads a title commitment with specific questions, not a general scan. The following is the structured checklist that informs a professional review.

Schedule B-I Requirements: What Could Delay Closing

Work through each requirement and classify it:

Outstanding mortgages and deeds of trust. Verify payoff amounts against the seller's representations. Confirm the title company's requirement for a payoff letter or discharge before policy issue.

Delinquent taxes and special assessments. Check amounts, confirm assessment periods, and identify any outstanding bonds or improvement districts tied to the property.

Pending court orders, judgements, and lis pendens. These require resolution before closing. A lis pendens recorded against the property signals active litigation affecting title, and that is not a routine requirement.

Authority documentation. If the seller is an LLC, LP, or trust, the title company will require evidence of authority to convey: an operating agreement, partnership agreement, or trust documentation confirming the signing party's authority. Missing or outdated authority documents surface late and delay closings.

Schedule B-II Exceptions: What Affects the Property's Title

Easements are the most common and most varied Schedule B-II item. Utility easements for electricity, gas, water, and sewer run across most commercial parcels. Their location on the survey determines whether they affect buildable area or proposed improvements. Access easements may benefit the property (required for ingress and egress) or burden it (a neighbouring parcel crossing yours). Drainage and conservation easements restrict use within their boundaries. The question is always whether the easement conflicts with what the buyer intends to do with the property.

Covenants, conditions, and restrictions (CC&Rs) cover use limitations (office only, no retail), maintenance obligations (shared car park), and rights-of-first-refusal or put options held by adjacent owners or an association. Use restrictions survive ownership changes and bind every subsequent buyer. They must be read in full, not summarised.

Liens. Mechanic's liens filed by unpaid contractors, judgment liens from court awards against the seller, and tax liens from federal or state authorities all attach to the property and travel with it unless discharged before or at closing. Confirm each lien's amount, holder, and the title company's plan for discharge or insurance.

Mineral rights. In states where mineral rights can be severed from surface rights, a prior conveyance of mineral interests means the buyer is purchasing surface rights only. If the property has active mineral extraction or development potential, the scope of the mineral exception requires specialist review.

Red Flags That Require Further Action

These items require a response before proceeding:

Exception documents referenced but not included. The commitment references a recorded instrument (a reciprocal easement agreement, a declaration of restrictions) but the document itself is not in the package. Demand it. You cannot evaluate an exception without reading what it says.

Legal description mismatch. The legal description in Schedule A does not match the legal description the surveyor certifies. This may be a typographical error or a genuine boundary discrepancy. Either way, it must be resolved before closing.

Commitment effective date more than six months old. A stale effective date means the title search may not reflect recent recordings. The title company needs to refresh the search and update the commitment.

Gap in chain of title. A period during which no recorded conveyance exists. The title company either cannot identify the owner during that period or the conveyance was never recorded. This requires a curative deed, affidavit, or court action.

Survey exception not removed. The buyer delivered an ALTA survey at the title company's request, but the standard survey exception remains in Schedule B-II. The title company has not processed the survey or has identified a reason not to remove the exception. Find out which.

What to Look for in an ALTA Survey

The ALTA survey is a technical document produced by a licensed surveyor, but it must be read alongside the title commitment. Many review errors come from treating it as a standalone document. Every relevant finding on the survey has a corresponding item in the title commitment, and discrepancies in either direction are the most consequential findings the paired review produces.

Boundary and Legal Description

The survey boundary must match Schedule A's legal description precisely. The surveyor's metes-and-bounds description (bearing, distance, monument) should be identical to the legal description in the commitment. Any variation, even in format or units, requires clarification from the surveyor and the title company before closing.

Check the corner monuments. A survey showing "monument not found" at a key corner weakens boundary confidence and may require the surveyor to re-establish the corner before the title company will remove the survey exception. Check adjoining property descriptions for consistency: a neighbour's recorded legal description that overlaps yours is a boundary dispute waiting to surface.

Encroachments

Encroachments are one of the most material findings an ALTA survey can reveal.

An encroachment onto the property (an adjacent structure crossing the boundary) is a title defect. The encroaching structure may give the adjoining owner a claim to adverse possession if it has been in place long enough. Unless the title company agrees to insure over the encroachment with a specific endorsement, the buyer acquires a property with an unresolved boundary conflict.

An encroachment off the property (the subject's improvements crossing into an easement area or onto the adjacent parcel) also requires resolution. An improvement sitting inside a utility easement may need to be relocated if the easement holder exercises their rights. An improvement crossing onto the adjacent parcel requires either a boundary adjustment or a written agreement with the neighbour.

Access to Public Roads

Recorded, unencumbered access to a public road is a legal requirement for a marketable title. A landlocked parcel, with no direct frontage and no recorded easement providing ingress and egress, is unmarketable in most jurisdictions.

Confirm that the access shown on the survey corresponds to a recorded instrument in Schedule B-II. An easement shown graphically on the survey must appear as a Schedule B-II exception; if it does not, either the exception was omitted from the commitment (request an amendment) or the easement is unrecorded, which is a more serious problem. Confirm there are no physical obstructions blocking the recorded access route.

Easements and Rights-of-Way on the Survey

This is the most important cross-referencing task in the entire paired review. Every easement graphically shown on the ALTA survey should correspond to a Schedule B-II exception, and every Schedule B-II easement exception should be locatable on the survey. Discrepancies in either direction require action:

Survey easement not in Schedule B-II. The surveyor found a recorded easement that the title search missed. Request a commitment amendment to add it as an exception, and confirm the title company has reviewed the underlying instrument.

Schedule B-II easement not on the survey. The title search found a recorded easement that the surveyor did not plot. This may be because the instrument's legal description is too vague to locate, or because the easement has been vacated but the title company does not have the vacating instrument. Get an explanation from both the surveyor and the title company before proceeding.

Flood Zone and Setback Lines

The ALTA survey must show the property's FEMA flood zone designation. Zone A or AE designations indicate the improvements are in a Special Flood Hazard Area: lenders will require flood insurance as a condition of the loan. Confirm the flood zone against the FEMA Flood Map Service Center directly, since survey designations can lag FEMA remapping updates.

Setback lines (the minimum distances improvements must maintain from property boundaries, easements, and public roads) must be shown on the survey. Confirm that existing improvements respect all applicable setbacks. An improvement within a setback line requires either a variance or a title insurance endorsement, and some endorsements may not be available depending on lender requirements.

How AI Automates Title Commitment and ALTA Survey Review in CRE

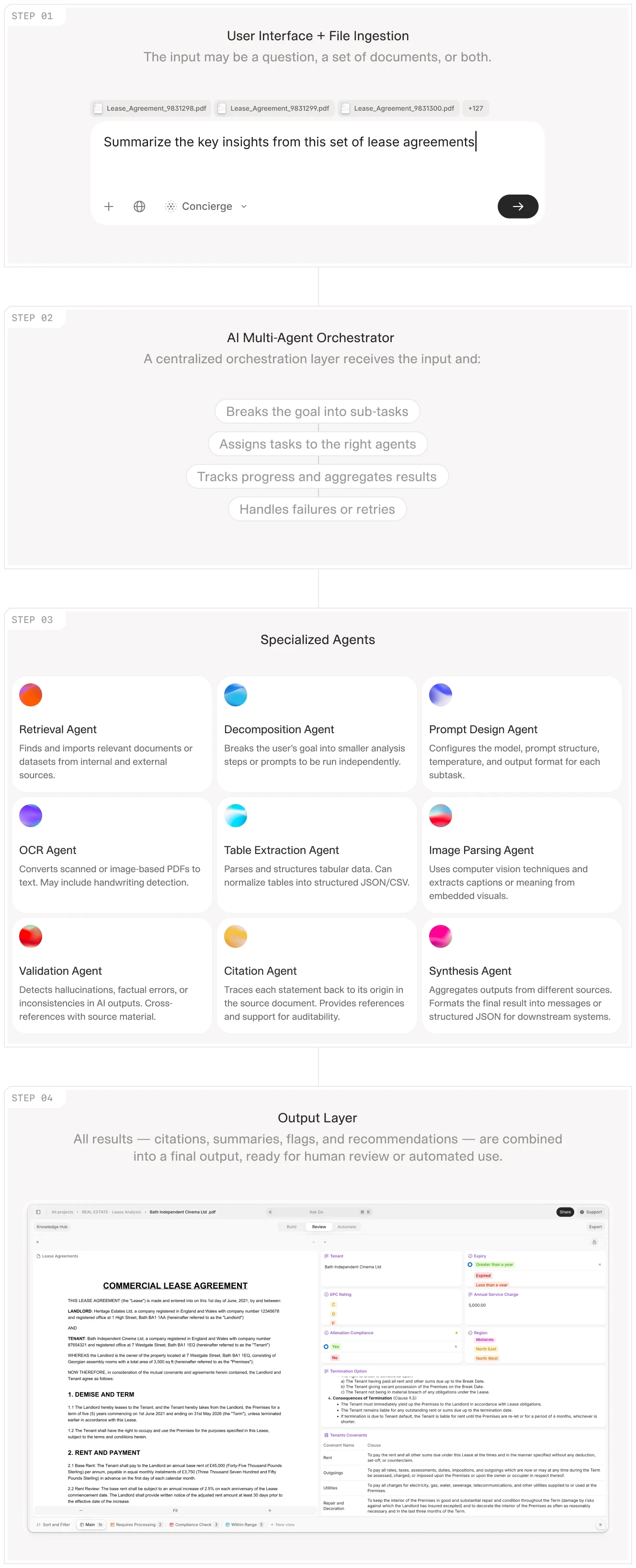

The scale problem is structural. Acquisition teams managing 20 to 50 active transactions simultaneously cannot give every title and survey package the senior counsel attention it warrants. The traditional response is delegation — junior attorneys or paralegals handle the initial review pass. That introduces inconsistency and creates a bottleneck whenever complex issues surface and require senior judgment.

AI changes the economics of that first pass. The extraction and cross-referencing tasks that consume hours of paralegal time are well-suited to intelligent document processing: reading structured documents, extracting named entities, classifying items by type, and mapping data across multiple documents. The judgment tasks (materiality assessment, negotiation strategy, curative recommendations) remain with counsel.

Here is what a document AI workflow does on a title and survey review:

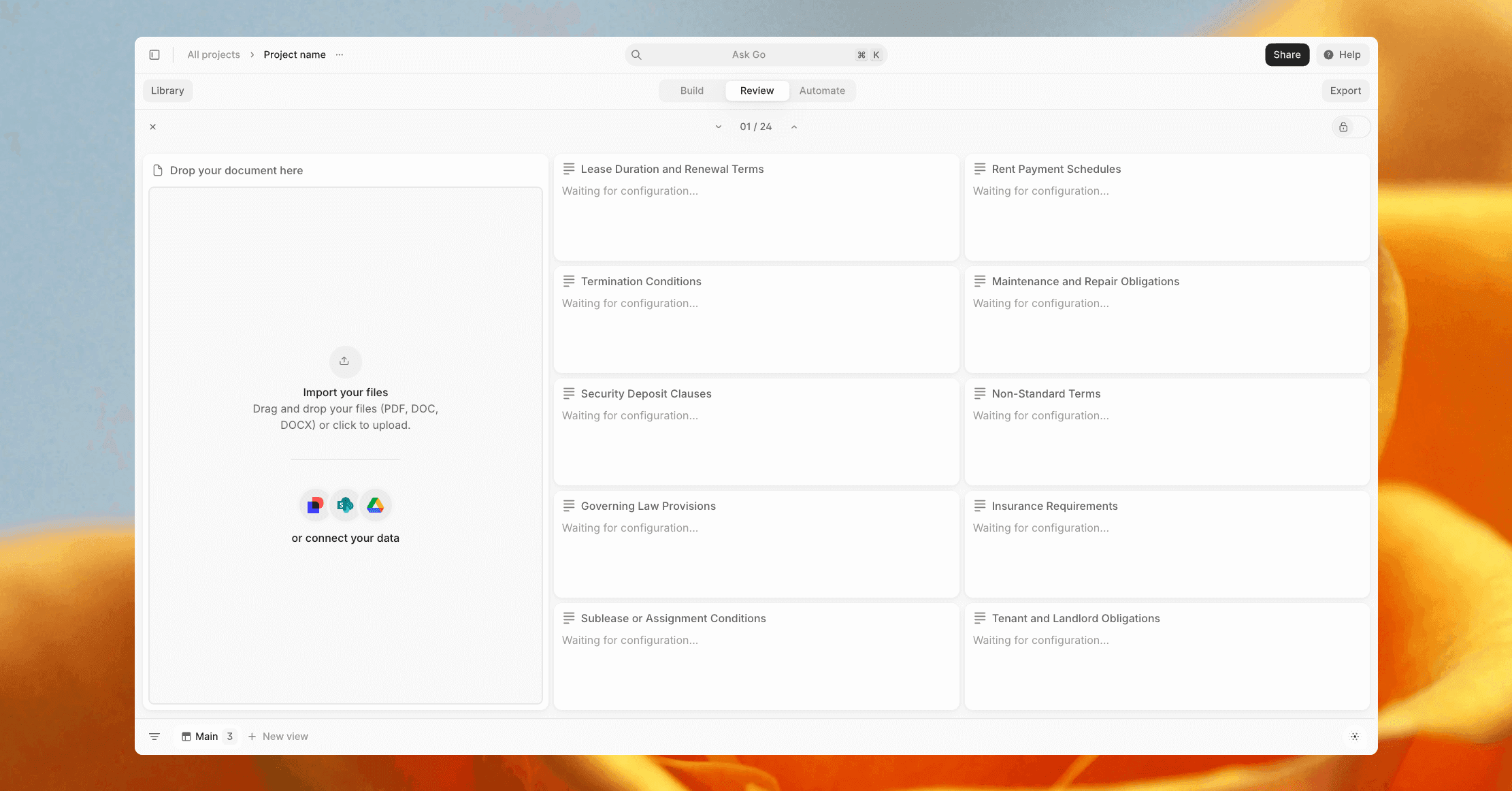

1. Schedule B extraction and classification. The AI reads the title commitment and extracts every Schedule B-I requirement and every Schedule B-II exception, classifying each by type (mortgage, lien, tax, easement, CC&R, mineral rights, court order). It flags non-standard exceptions (items not in the title company's standard exception template) for priority counsel review.

2. ALTA survey data extraction. The AI extracts boundary dimensions, easement locations and widths, encroachment findings, Table A items, flood zone designation, and setback lines from the survey document. Where the survey includes a text report alongside the graphical exhibit, both sources are parsed.

3. Cross-document reconciliation. The AI cross-references Schedule B-II exceptions against the ALTA survey and flags discrepancies: survey easements not appearing in Schedule B-II, and Schedule B-II easements not locatable on the survey. It also cross-references the Schedule A legal description against the surveyor's certified legal description and flags any variation.

4. Issues list generation. The AI produces a structured issues list, prioritised by materiality, with a gap in chain of title or an encroachment rated above routine requirements. The issues list is the raw material for the T&S Memo and the title objection letter.

5. Title and Survey Memo drafting. The AI produces a first-draft T&S Memo using the extracted data and issues list. Counsel reviews, edits for judgment calls, and delivers the final memo to the deal team. What previously required four to six hours of drafting time takes 30 to 45 minutes.

6. Title objection letter generation. Where issues require the seller to cure or the title company to respond, the AI drafts the initial title objection letter, flagging each issue with a reference to the relevant schedule or survey finding.

The category has established proof points. Orbital Witness reports a 70% reduction in title review time across law firms including Goodwin, BCLP, and Vinson & Elkins. For commercial real estate specifically, the gains come not just from faster extraction but from consistent cross-referencing: the AI checks every Schedule B-II exception against the survey on every document, every time, without the attention fatigue that affects manual review on complex packages.

V7 Go's Deed Analysis Agent processes title commitments, ALTA surveys, and supporting exception documents. It extracts metes-and-bounds descriptions, lot-and-block references, easement terms, and schedule exceptions. It cross-references the two documents and delivers a structured findings report for counsel review. For teams managing high transaction volumes, see how AI is reshaping real estate document workflows across the acquisition lifecycle.

V7 Go's Deed Analysis Agent reviews title commitments and ALTA surveys automatically — extracting exceptions, cross-referencing documents, and delivering a structured findings report. See the Deed Analysis Agent →

For teams doing AI-assisted lease abstraction alongside title review, the same extraction and cross-referencing infrastructure applies across both document types. The workflow investment in AI document review pays across the full due diligence stack, not just the title and survey package.

Every commercial real estate acquisition carries the same structural tension in title and survey review: the documents are consequential, the review window is short, and the cost of missing a material exception falls entirely on the buyer.

The process described above (Schedule B extraction, ALTA survey cross-referencing, issues list, T&S Memo, title objection letter) is the professional standard. The question is not whether to do it. The question is how fast it can be done reliably, at what cost, and with what consistency across a portfolio of simultaneous transactions.

AI handles the extraction and cross-referencing tasks that consume most of the time but require least of the judgment. Counsel spends their hours on the exceptions that require interpretation, negotiation, and strategic decision-making, not on confirming that 30 Schedule B-II items have been listed correctly.

V7 Go's Deed Analysis Agent processes title commitments and ALTA surveys, extracts exceptions and survey data, cross-references both documents, and delivers a structured findings report for counsel review. See the Deed Analysis Agent →

What is a title commitment in commercial real estate?

A title commitment is a written promise by a title insurance company to issue a title insurance policy, subject to the conditions and exceptions set out in its schedules. It is issued after the title search is complete and before closing. The commitment sets out what the title company requires before it will issue the policy (Schedule B-I) and what the eventual policy will not cover (Schedule B-II). In commercial real estate, the title commitment is typically the first title-related document delivered to buyer's counsel after the purchase and sale agreement is executed. It is not a guarantee of title quality — it is the title company's conditional offer to insure. The effective date is significant: defects recorded after that date are outside the scope of the title search and will not be covered by the eventual policy. Buyer's counsel must review the commitment promptly and raise objections within the contractual objection period.

+

What is the difference between a title commitment and a title insurance policy?

A title commitment is a preliminary document: the title company's conditional promise to issue a policy once the requirements in Schedule B-I are satisfied. The title insurance policy is the final contract of insurance, issued at or after closing once those conditions are met. The commitment identifies what will and will not be covered; the policy confirms the coverage actually issued. In practice, the exceptions listed in Schedule B-II of the commitment carry through into the policy. Any exception the buyer or lender does not successfully negotiate out of the commitment before closing will appear as a permanent limitation in the policy. This is why Schedule B-II review is critical — what survives those negotiations becomes a lasting limitation on the title insurance coverage the buyer and lender hold.

+

What is Schedule B in a title commitment?

Schedule B in a title commitment has two parts. Schedule B-I lists the requirements the title company must receive or have satisfied before it will issue the title insurance policy. Common B-I requirements include: payoff of existing mortgages, payment of delinquent taxes, delivery of corporate or partnership authority documents, execution of affidavits, and gap indemnities. Requirements are conditions to coverage; the policy will not be issued until they are met. Schedule B-II lists the exceptions to coverage: the matters the policy will not insure against. These include both standard exceptions (matters of survey, rights of parties in possession, unrecorded liens) and special exceptions specific to the property (recorded easements, deed restrictions, mechanic's liens, mineral rights reservations). Schedule B-II review is typically the most time-intensive part of a commercial real estate title commitment review, because every exception must be evaluated for its impact on the buyer's intended use and the lender's collateral position.

+

What is an ALTA survey used for in a CRE acquisition?

An ALTA/NSPS Land Title Survey serves two primary functions in a commercial real estate acquisition. First, it provides a detailed picture of the property's physical characteristics: boundary lines, improvements, easements, encroachments, access to public roads, flood zone designation, and setback lines. This is the information acquisition teams need to understand the property's actual condition on the ground, as distinct from how it is described in recorded instruments. Second, the ALTA survey is used to remove the standard survey exception from Schedule B-II of the title commitment. The standard survey exception excludes coverage for matters that a current, accurate survey would disclose. When the buyer delivers a conforming ALTA survey, the title company reviews it and, if no new issues are revealed, removes the exception from the eventual policy. This gives the buyer and lender title insurance coverage for boundary lines, encroachments, and easement locations, not just for recorded title defects. Most commercial lenders require an ALTA survey as a condition of the loan.

+

How long does a title and survey review take on a commercial real estate transaction?

The most common and most material red flags in a commercial real estate title commitment are: exception documents referenced in Schedule B-II but not provided with the commitment package (you cannot evaluate what you have not read); a legal description mismatch between Schedule A and the ALTA survey (signals a data error or a genuine boundary problem); a commitment effective date more than six months old (the title search may not reflect recent recordings); a gap in the chain of title (a period with no recorded conveyance that requires curative action); and a survey exception that remains in Schedule B-II despite delivery of an ALTA survey. In Schedule B-I, red flags include requirements calling for court orders to resolve disputes, pending lis pendens against the property, and missing authority documentation from the seller entity. In Schedule B-II, the most serious flags are easements that conflict with the buyer's intended use, active mechanic's liens, severed mineral rights with active development potential, and use restrictions that may prevent the buyer's planned improvements or operations.

+

What are the most common red flags in a commercial real estate title commitment?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.