Knowledge work automation

19 min read

—

Investor relationship management is the discipline most fund managers build too late — after they have already lost commitments they did not know they were losing.

The pattern is familiar. Six months into a fundraise, the IR team is tracking 50 conversations that feel like they are progressing. The LP at the state pension fund says they are still reviewing. The family office says the timing is not quite right. Three months later, both decline. The fund manager assumes timing. The real reason, in both cases, is that another fund in the same allocation review was faster, more organized, and responded to due diligence requests in four days instead of twelve.

According to Preqin's 2024 Global Alternatives Report, the median time from fund launch to first close is 14 months for private equity funds, and 18 months for first-time managers. The length is partly structural. But a significant portion comes from a fixable problem: most fund managers have no systematic way to qualify limited partners before investing significant time in them, no pipeline visibility to see where conversations are stalling, and no document workflow to respond to diligence requests at the speed institutional LPs now expect.

This article covers the full investor relationship management system for fund managers: from LP sourcing through lead scoring and diligence to subscription documents and post-close reporting, with particular focus on the document-heavy stages where AI is now compressing timelines by days, not hours. For a broader view of how generative AI applies across finance workflows, that article covers the full range of use cases beyond fund management specifically.

In this article:

The difference between investor relationship management and investor relations, and why confusing them costs fund managers months

The five stages of a fund manager's investor pipeline, with stage-specific activities and documents

LP lead scoring: a scoring framework for qualifying limited partners before committing significant IR time to them

DDQ automation, subscription document processing, and how AI handles the document workflows that stall most fundraises

AI for document processing

Automate DDQ responses without sacrificing accuracy

Get started today

What investor relationship management actually covers

Investor relations and investor relationship management sound like the same function. They are not.

Investor relations (IR) is a post-close function. Once LPs have committed capital and the fund has held a first close, IR handles ongoing communication with those investors: quarterly performance letters, capital call notices, distribution notices, annual general meeting materials, and ad-hoc LP inquiries. IR is relationship maintenance. The LPs are already in the fund.

Investor relationship management (also called investor pipeline management) is the pre-close function. It is the system for identifying potential limited partners, qualifying their fit, moving them through a fundraising funnel, managing the due diligence process, and getting them to a signed subscription document. It is LP acquisition.

Most fund managers use the same tool, or no formal tool at all, for both. The result: a team using a quarterly-reporting platform to track first meetings with institutional allocators they have never spoken to, with no pipeline visibility, no qualification criteria, and no way to see which LPs are progressing and which ones are stalling politely.

The distinction matters in practice. When an institutional allocator at a state pension plan sends a due diligence questionnaire with a two-week response window, the fund needs a system to produce that response quickly, track what has been sent, and follow up efficiently. That is not the same workflow as drafting a quarterly LP letter. IR tools do not solve it. A pipeline system does.

The five stages of a fund manager's investor pipeline

A systematically managed investor pipeline has five stages. Each has different activities, different documents, and different dropout rates. Most fund managers have informal versions of these stages. Formalizing them is what makes the pipeline visible and manageable.

Stage 1: source

LP sourcing is the prospecting stage. The fund identifies potential investors from placement agent networks, allocator databases, referrals from existing LPs, conference contacts, and introductions through co-investors or advisors. At this stage, records are thin: institution name, contact, basic mandate. Volume is high. Quality is unknown.

The source stage requires a light data structure. Each record needs enough information to make a qualification decision, and nothing more. Fund managers who over-invest in building detailed profiles at the source stage are doing research that belongs in the engage stage, for LPs who have already passed qualification.

Stage 2: qualify

Qualification is where most sourced leads should be filtered out. A pension fund that allocates only to vehicles above $500 million is not a qualified lead for a $150 million debut fund, regardless of how warm the introduction was. A sovereign wealth fund with a mandate restricted to infrastructure and real assets does not belong in a private equity buyout pipeline.

Qualification decisions depend on five criteria: mandate fit, target ticket size, LP type, investment geography, and decision timeline relative to the fund's close schedule. LP lead scoring, covered in the next section, formalizes these criteria into a consistent ranking system.

Stage 3: engage

Engaged LPs have passed qualification. The engagement stage involves formal outreach: pitchbook delivery, fund strategy presentation, and first formal meetings. This stage also serves as a secondary filter. LP responsiveness during engagement, the depth of their questions, and their willingness to schedule a formal review call all signal genuine interest versus polite pipeline participation.

Fund managers who skip this filter commit the same error at the engage stage that they committed at the source stage without a qualification framework: distributing their time equally across LPs of very different quality.

Stage 4: diligence

Diligence is the most document-intensive stage. LPs request access to the fund due diligence package: the private placement memorandum, audited financial statements, track record documentation, portfolio company performance data, team bios, and compliance materials. They send due diligence questionnaires. Institutional LPs often conduct a separate operational due diligence review covering the manager's infrastructure and controls. Site visits and reference calls may follow.

This stage stalls fundraises more than any other because it depends entirely on the fund's ability to respond to LP requests quickly and completely. Speed matters: an LP allocation committee that meets quarterly will move to the next fund in their review if the current fund's DDQ response is still outstanding when the meeting comes around.

Stage 5: commit

The commit stage begins when an LP issues a soft circle (an informal intent to invest) and ends with a signed subscription document and funded commitment. It involves subscription document review, KYC and AML document collection, side letter negotiation, and final legal approval. The limited partnership agreement governs the fund terms that all LPs agree to at commitment, and any LP-specific modifications are negotiated as side letters to the main LPA.

Delays at the commit stage are expensive. An LP who has issued a soft circle but whose subscription documents are still in review three weeks later is a close that is not closed. Subscription document processing is not a legal formality. It is an operational workflow with a direct impact on close timing.

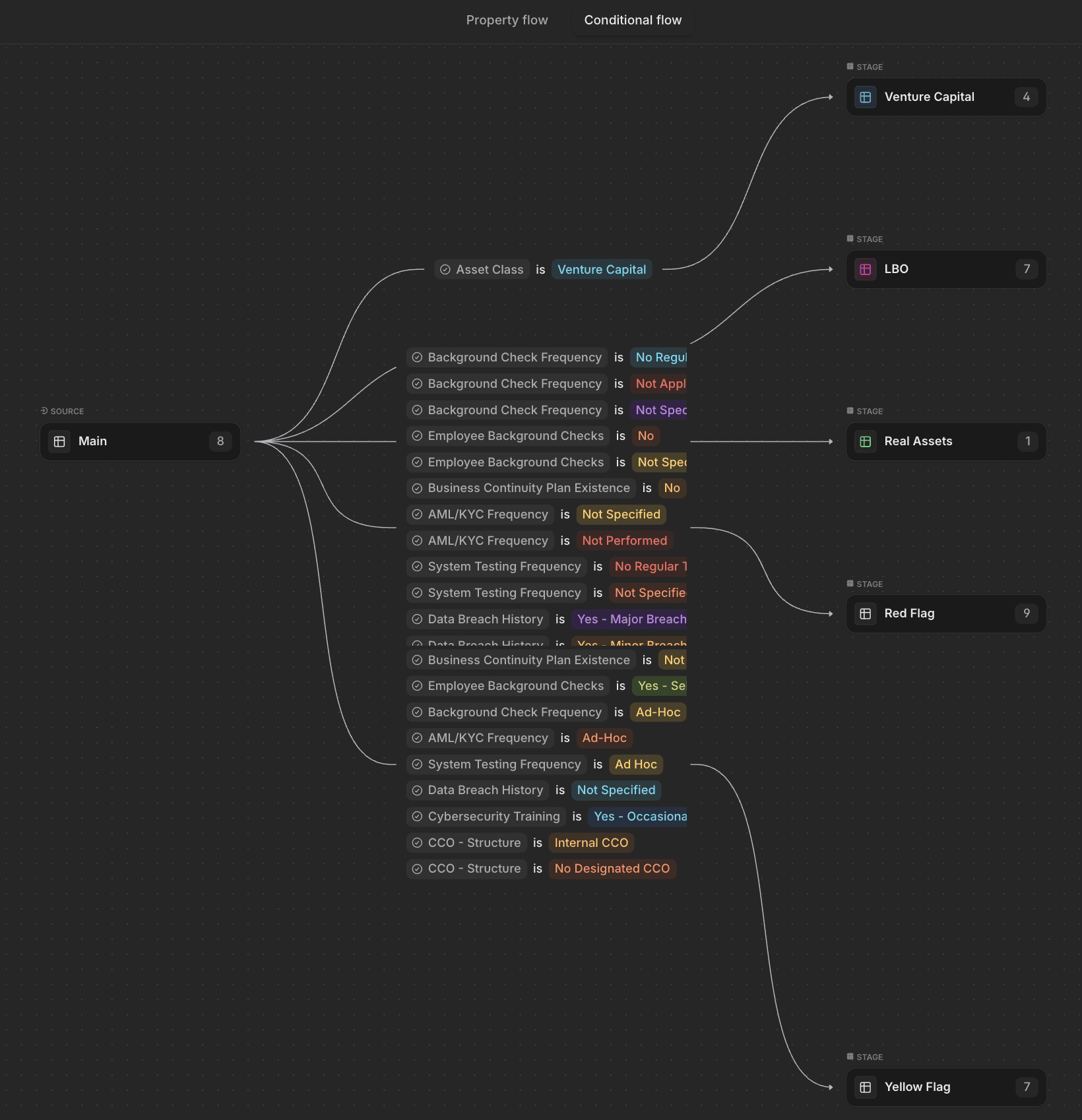

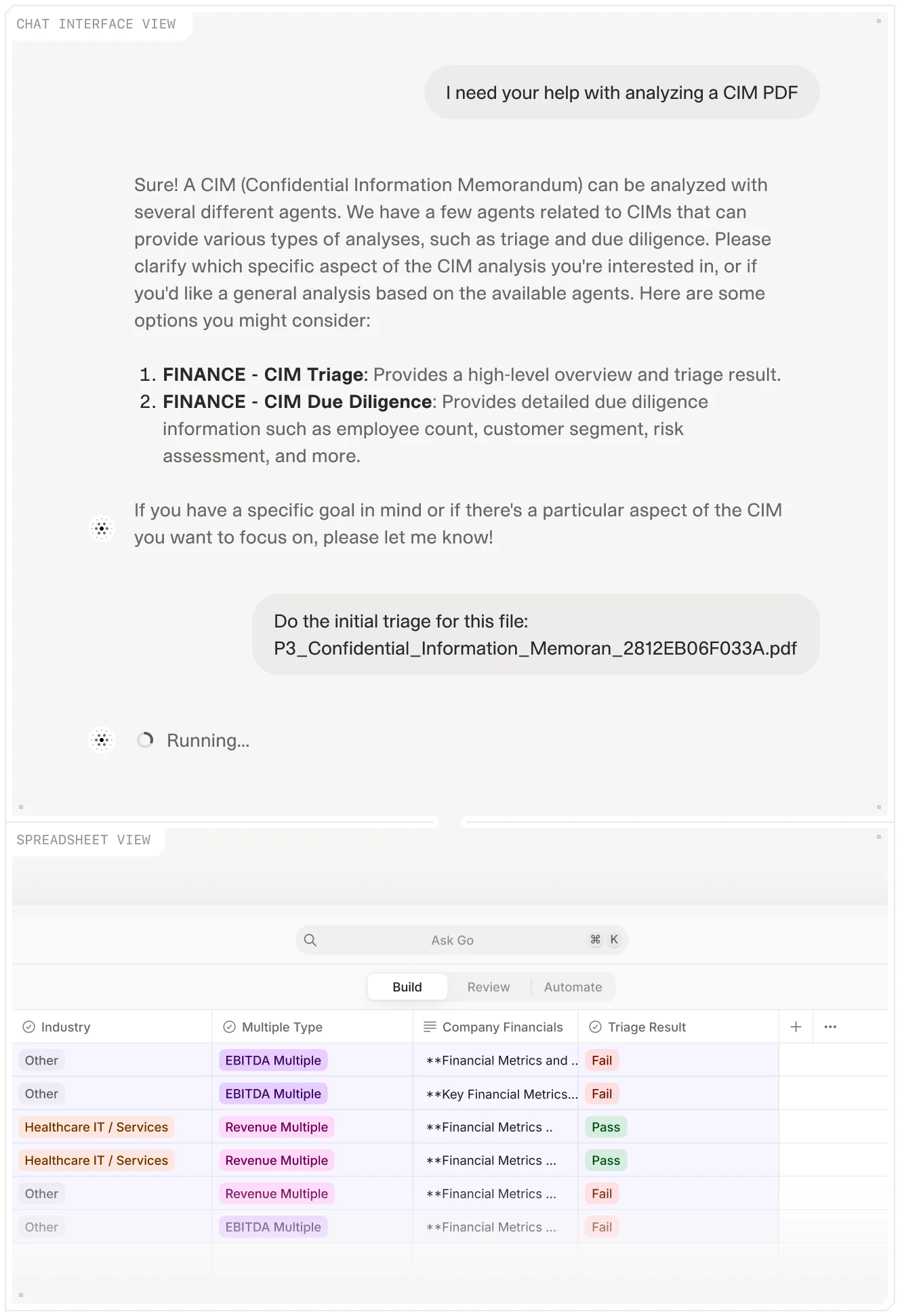

A workflow used by an AI operational due diligence agent

LP lead scoring: the qualification framework most fund managers skip

Lead scoring in an investor pipeline works the same way it does in enterprise sales: assign criteria-based scores to potential investors, rank them by fit and likelihood to close, and prioritize the team's time accordingly. Without it, every LP conversation gets roughly equal attention, which means the fund spends as much time on long shots as on genuine prospects.

Do fund managers actually need a formal scoring system?

They do.

A fund manager raising a USD 300 million buyout fund is typically in active conversation with 80 to 100 institutional allocators at any point in the fundraise. With two or three people managing LP relations, there is no way to service 100 LPs with equal attention. Something determines prioritization. The question is whether that something is a consistent, auditable framework or an implicit judgment call made differently by each team member. The scoring framework is better because it is consistent and can be reviewed when a qualified LP falls through the cracks.

Lead scoring criteria for limited partners

Five criteria account for most of the signal in LP qualification. Score each on a 0-to-3 scale, with 3 representing full alignment:

Mandate fit (0-3): Does the LP invest in this asset class, geography, fund stage, and strategy? A hedge fund allocator with a mandate limited to public equities does not belong in a private credit pipeline, regardless of AUM. Full alignment = 3. Partial but plausible = 1-2. No alignment = 0.

Target ticket size (0-3): The LP's typical commitment size versus the fund's target allocation range. A family office writing USD 2-5 million checks does not belong in the top tier of a fund seeking USD 30-50 million anchor commitments. Alignment within 20% of target = 3. Within 50% = 2. Outside range = 0-1.

Decision timeline (0-3): When does the LP expect to complete their allocation review relative to the fund's close schedule? An investment committee that meets semi-annually represents a high timeline risk for a fund targeting a close in six months. Timeline compatible = 3. Uncertain = 1-2. Incompatible = 0.

LP type and priority (0-3): Tier LP types based on your fund's strategy and target LP mix. For most institutional PE funds, pension funds and endowments score highest on stability and ticket size. Family offices score higher on speed and flexibility. Fund-of-funds introduce fee friction and score lower unless your LP mix specifically targets them.

Relationship warmth (0-3): An existing LP considering a re-up in a successor fund scores 3. A warm introduction from a co-investor or existing LP scores 2. A referral from a placement agent with an existing relationship scores 1. Cold outreach with no prior relationship scores 0.

Applying the scoring framework

A maximum score of 15 represents full alignment across all five criteria. Realistic top-tier leads score 11-15. The practical cutoffs for pipeline management:

12-15: Active pursuit. Assign a dedicated team member. Prioritize DDQ responses and meeting preparation within 48 hours of any LP request.

8-11: Monitor and maintain. Light-touch outreach at fund milestones: new documents available, performance updates, portfolio company news.

5-7: Deprioritize for this fundraise. Track for future cycles if the LP's mandate may evolve.

Below 5: Remove from the active pipeline. Re-qualify if circumstances change.

This framework is not precise to the decimal point. Its purpose is to force a consistent conversation across the team about which LPs get time and which do not. Without it, the allocation of IR time defaults to whoever called most recently.

A formal LP scoring framework replaces ad-hoc prioritization with consistent, auditable criteria. This is especially important when a small IR team is managing 80 or more active conversations across a 14-month fundraise.

Why spreadsheet-based investor pipelines break before the second close

Excel is where investor pipeline management goes to stall. Nearly every first-time fund manager starts with a spreadsheet: LP name, contact, stage, notes, last follow-up date. It works for the first 20 relationships. By the time the pipeline reaches 60 active conversations across two or three team members, it breaks.

The failure modes are predictable. LP records fall out of sync between team members working in different versions of the file. Follow-up tasks depend on someone remembering to check the spreadsheet rather than being surfaced automatically. The DDQ log lives in a separate tab from the pipeline, so the person drafting diligence responses cannot see the full relationship history for the LP they're responding to. There is no scoring column because maintaining a scoring framework in a spreadsheet requires discipline that erodes within six weeks.

The cost: a mid-market buyout fund that loses two USD 10 million commitments because of slow DDQ responses or missed follow-ups typically does not know those commitments were lost to process failure. The LPs say timing was not right. The fund assumes the strategy was the issue. The real reason was operational, and it was fixable.

The fix is not necessarily an expensive purpose-built platform. It is a CRM that mirrors the pipeline stages described above, with task automation for follow-up sequencing, document tracking at the diligence stage, and a single shared record that every team member updates and reads from. The pipeline has to be the same pipeline for everyone on the team, or the coordination failures the spreadsheet created reappear inside the new tool. The following section covers how to build that structure and where AI addresses the document workflows that currently consume the most time during a fundraise.

Building the investor CRM and pipeline structure

The CRM should mirror the pipeline stages exactly. Not a generic contact management tool with custom fields retrofitted for LP tracking, and not a shared spreadsheet with stage columns renamed to look like a pipeline. The structure should make it impossible to open the dashboard without seeing immediately where every active LP sits and what action is required next.

Each LP record needs a core set of fields. Firmographic data covers LP type (pension, endowment, family office, fund-of-funds, UHNW), AUM, geography, investment mandate, and typical ticket range. Relationship history tracks the introducing party, prior fund exposure, attendance at fund events, and last substantive contact date. Pipeline status records the current stage, assigned team member, next required action, and expected decision date. Lead score captures the current aggregate with component breakdown so new team members can reconstruct the qualification rationale without a handover meeting. Document status tracks which materials have been sent, which diligence requests are outstanding, and what the current response timeline looks like.

The document status field matters more than most fund managers realize. It is not a separate tracking system from the LP pipeline. It is part of the same record. When an LP's DDQ response is two days overdue and there is no flag in the system, that is a relationship at risk. When the CRM surfaces the flag automatically, someone catches it before it becomes a lost commitment.

On tool selection: the investor CRM does not need to be a fund-specific platform. Several general-purpose CRMs are used successfully by fund managers, including Salesforce, HubSpot, Affinity, and Pipedrive, each configured with fund-specific pipeline stages and custom fields. The critical requirement is not the software: it is the field structure, the stage definitions, and the discipline to keep records current. A well-configured general-purpose CRM beats a poorly-used fund-specific platform every time.

One configuration decision that fund managers consistently underinvest in is the task automation setup. A CRM with pipeline stages but no automated task sequencing is a better spreadsheet, not a better system. When an LP moves into the diligence stage, the system should automatically create tasks: send the PPM update, confirm data room access has been granted, set a seven-day follow-up if no DDQ has been received. When a DDQ arrives, the system should flag the response deadline and assign the drafting task to the appropriate team member. This task layer is what converts a CRM from a record-keeping tool into a pipeline management system. Without it, the fund is still relying on people to remember what needs to happen next, which is precisely the failure mode that spreadsheets produce.

The document workflows that slow LP due diligence

The diligence stage is where fundraising stalls. Most of the slowness is not in the LP decision process. It is in the fund's ability to respond. Three document workflows account for the majority of the friction: DDQ responses, subscription document processing, and operational due diligence documentation. Each one is a candidate for AI-assisted automation.

DDQ response automation

The due diligence questionnaire process works like this: an LP sends a template, either the ILPA standard questionnaire, an AIMA-based template, or the LP's own proprietary format, containing 80 to 150 questions covering the fund's strategy, investment process, team, track record, risk management, compliance policies, and operational infrastructure. The fund must respond accurately and completely, typically within 10 to 14 days.

A fund with 40 active LP conversations in a 60-day window may receive 25 to 30 DDQs during that period. Many questions overlap across LP templates: different phrasing, same underlying inquiry. But because each LP's template is formatted differently, the overlap is not obvious, and the fund ends up reconstructing the same answer from scratch for each template.

The AI approach: build a fund knowledge base containing the strategy documents, compliance policies, track record data, team bios, and prior DDQ responses. When a new DDQ arrives, an agent reads each question, matches it against the knowledge base, and drafts a response. A compliance officer reviews and approves. The fund sends a complete, accurate response in two days instead of ten.

Teams using AI due diligence agents for document-intensive Q&A workflows report response times dropping from an average of 8 to 12 days to 2 to 3 days, with consistency improving because every answer draws from the same source material rather than being reconstructed from memory by whichever analyst happens to be available.

A structured fund data room with AI-assisted DDQ drafting compresses response time from 10 to 12 days to 2 to 3 days, enough to prevent the allocation committee timing problem that costs fund managers qualified LP commitments.

Subscription document processing

Subscription documents collect the information an LP provides at the point of commitment: investor entity type, commitment amount, beneficial ownership structure, representations and warranties, side letter elections, and KYC/AML documentation. A typical subscription document package runs 60 to 120 pages. In a fund closing with 30 LPs, the operations and legal teams are reviewing 1,800 to 3,600 pages of subscription materials in parallel, under close pressure.

Manual review of a single subscription document takes 45 to 90 minutes. The bottleneck is not reading speed. It is the need to extract specific fields from inconsistently formatted documents, catch exceptions and missing information, and route items requiring legal review without losing track of where each LP's package stands.

With AI: the agent ingests each subscription document, extracts structured fields (commitment amount, investor entity type, side letter elections, beneficial ownership chain, AML declarations), flags any field containing an exception or appearing incomplete, and routes flagged items to a legal reviewer. The reviewer focuses on the 15 percent of documents with actual issues rather than the full stack.

V7 Go is built for exactly this kind of workflow. Fund teams define the extraction schema once: the specific fields they need from subscription documents. The agent then processes every incoming document against that schema. Visual grounding links each extracted value back to its precise location in the source document, so the legal reviewer can verify without re-reading the full package. The structured data flows into the fund's CRM or fund administration system via API, closing the gap between document processing and pipeline tracking.

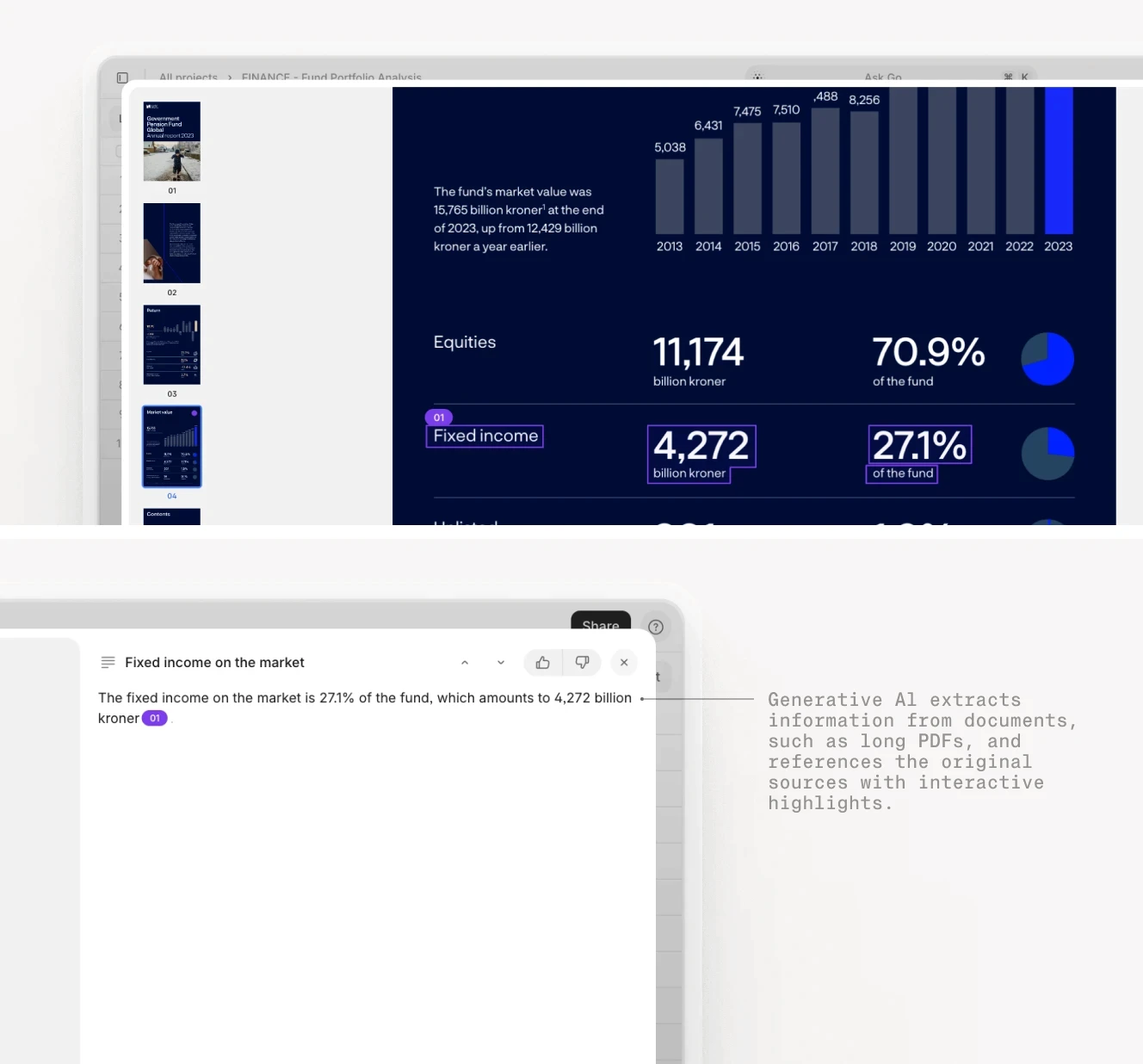

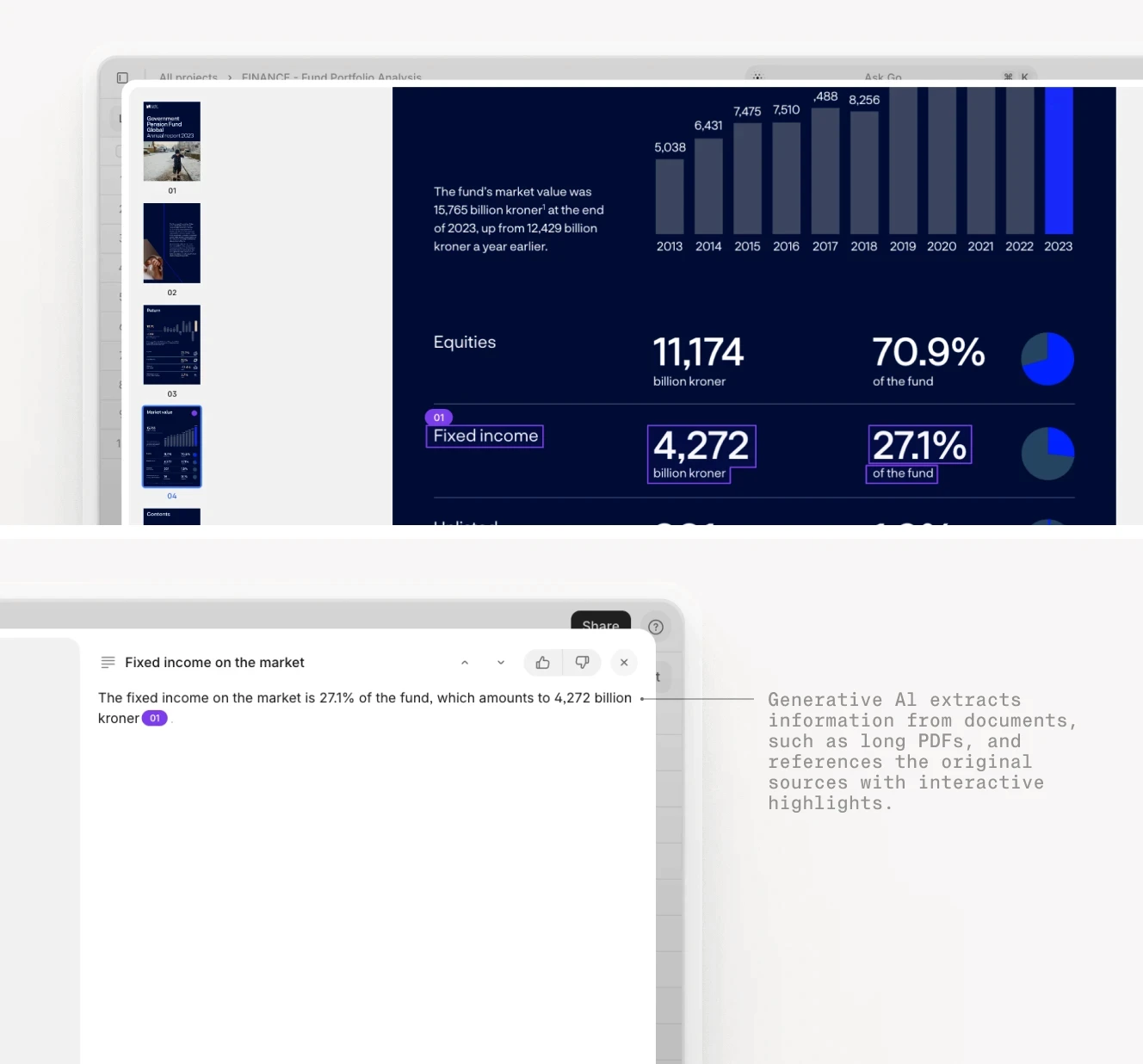

The following demonstration shows how V7 Go processes a document bundle and surfaces structured data with source citations:

V7 Go processing a fund document bundle with source citations: the same workflow fund managers apply to subscription document review, DDQ drafting, and ODD response preparation.

Operational due diligence documentation

Institutional LPs (pension funds, endowments, and insurance companies) typically require operational due diligence alongside investment due diligence. ODD covers the fund manager's infrastructure: valuation policies, custody arrangements, IT security, business continuity, and compliance controls. It generates a separate document request list with 30 to 60 line items, each requiring a specific document or attestation in response.

AI handles the same workflow here: ingest the ODD request list, match each item against the fund's operational documentation library, identify gaps (items with no matching document in the library), and surface which items require new documentation versus retrieval of existing materials. For fund managers running multiple concurrent closes across vehicles, the time saving compounds with each additional LP in the pipeline.

AI citation grounding ensures every data point extracted from fund documents traces back to its source in the original PDF, which is critical for LP reporting accuracy and compliance attestation.

Investor reporting as a retention tool for limited partners

Investor pipeline management does not end at first close. The LPs who committed are now the fund's ongoing investor base, and the quality of post-close communication determines re-up rates for successor funds. Investor reporting is the primary touchpoint, and it is worth treating with the same systematic discipline as the pre-close pipeline.

Quarterly LP letters, capital call notices, distribution notices, and AGM materials are the standard reporting cadence for most private equity and private credit funds. Each quarterly letter requires gathering performance data from portfolio companies, calculating fund-level metrics (IRR, MOIC, DPI, RVPI), and writing narrative commentary contextualizing the period's performance. For funds with 15 to 20 portfolio companies, this is a two to three week exercise every quarter.

AI compresses it. An agent ingests portfolio company financial statements, extracts performance data against a predefined schema, calculates fund metrics, and drafts the quarterly letter narrative. The investment team reviews, adjusts commentary, and approves. Letters reach LPs faster, and the investment team's time goes to portfolio company management rather than reporting production. For a detailed breakdown of this workflow, the AI investor reporting article covers quarterly letter generation, capital call processing, and LP communication automation in full.

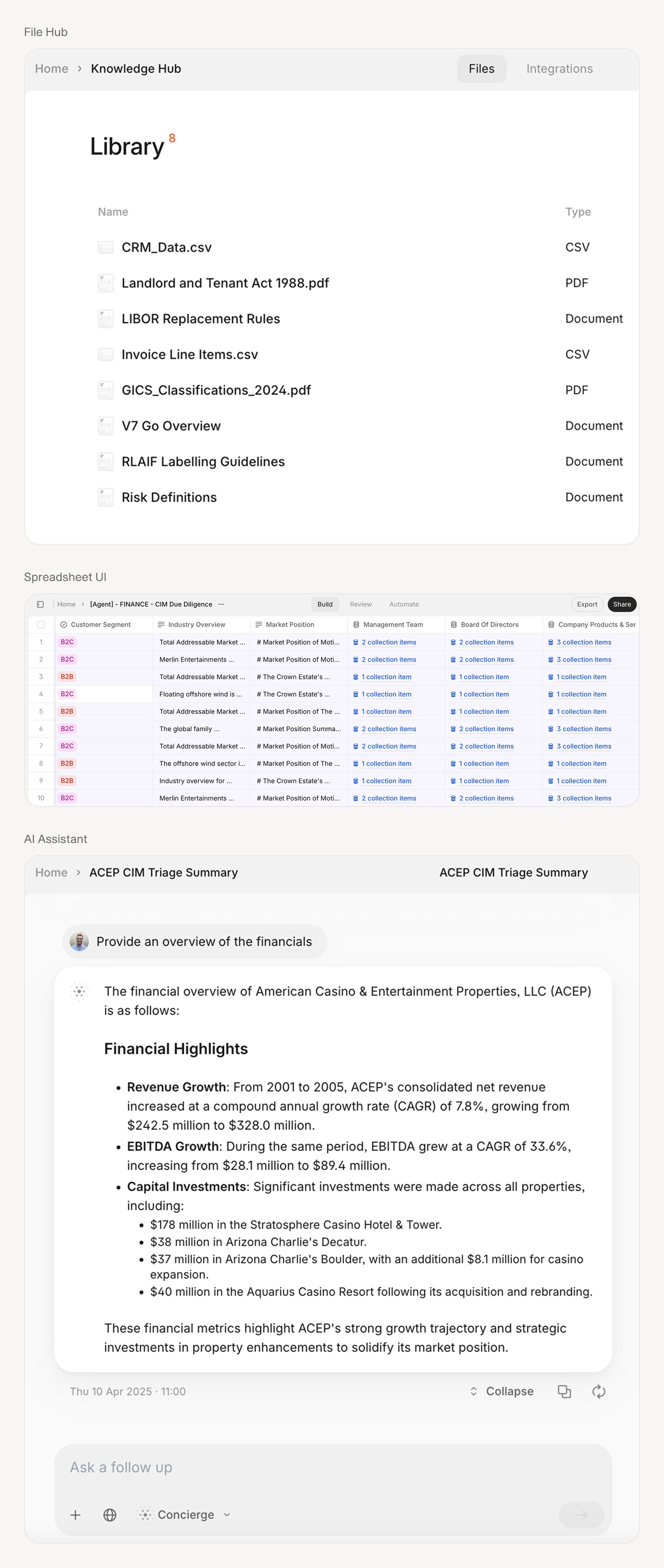

V7 Go's agent workflow for fund document analysis, from ingestion through structured extraction to review and output, applies consistently across the full LP lifecycle from diligence to quarterly reporting.

What a systematic investor pipeline looks like at scale

When a fund manager combines a structured investor CRM, a formal LP lead scoring framework, and AI-assisted document workflows, the fundraise changes in measurable ways. DDQ response time drops from ten to twelve days to two to three days. Subscription document review shifts from 45 to 90 minutes per LP to a review of flagged exceptions only. The investment team's time on quarterly reporting compresses from three weeks to four to five days.

More important: the team has pipeline visibility at every moment. Conversations that are stalling get surfaced automatically. High-score LPs receive prioritized follow-up. The fund closes faster not because the strategy changed but because the process stopped losing commitments it did not know it was losing.

The AI investment memo generation workflow sits within this broader system, alongside DDQ processing, subscription document review, and LP reporting. Building a pipeline system that manages all of these stages in one connected workflow is the work of the first months of any serious fundraise. The teams that build it before they need it close faster than the teams that build it while they are already behind.

The system is worth building before you need it

Star Mountain Capital manages private credit and private equity investments where document-intensive deal and LP workflows are a daily operational reality. Their adoption of V7 Go for fund document processing reflects a pattern we see across fund managers building serious investor pipeline systems: the teams that build document automation before they are behind on a close outperform the teams that build it as a fire-drill response to a late-stage diligence request from an institutional LP with a hard deadline.

The investor pipeline described in this article is a connected system. Lead scoring decides which LPs receive dedicated IR time. The CRM tracks where each LP sits in the process. AI agents handle the DDQs, subscription documents, and ODD requests that the diligence stage generates. Reporting automation handles the quarterly LP communication cadence post-close. Each component is independently useful. Together, they eliminate the manual bottlenecks that extend the average fundraise by three to six months.

If your fund is currently managing LP diligence documents manually, or tracking a 60-LP pipeline in a spreadsheet that two team members are updating independently, the AI due diligence workflow is a practical starting point. Define the extraction schema for your most common LP document type, process your last ten DDQs through it, and measure the time difference. The outcome of that exercise tells you whether building the full system is worth the investment. In our experience with fund managers, it almost always is.

What is investor pipeline management?

Investor pipeline management is the pre-close system fund managers use to identify, qualify, and move limited partners from first contact to signed subscription document. It covers the full LP acquisition lifecycle: sourcing potential investors from allocator databases, placement agents, and referrals; qualifying their fit against the fund's mandate, target ticket size, and close timeline; managing engagement through pitchbooks and formal meetings; processing due diligence requests including DDQs and data room access; and handling subscription documents and KYC at the commit stage. It is distinct from investor relations, which is the post-close function of managing capital calls, quarterly reporting, distributions, and AGM communications for LPs who have already committed to the fund. Fund managers who conflate the two typically apply IR tools to pipeline problems and get the wrong results.

+

How does investor pipeline management differ from investor relations?

Investor pipeline management is the pre-close LP acquisition function. Its goal is to move potential limited partners from first contact to committed capital. Investor relations is the post-close LP communication function. Its goal is to maintain relationships with existing investors through regular reporting, capital call management, distribution notices, and annual general meetings. The activities, timelines, and document types involved are entirely different. IR tools are designed for relationship maintenance with a stable set of counterparties. Pipeline tools are designed for managing a funnel with high dropout rates, variable response timelines, and document-intensive qualification processes. Using an IR platform to manage a fundraise pipeline creates blind spots at every stage: no qualification criteria, no stage visibility, no document workflow, and no scoring framework. Most first-time fund managers discover this distinction the hard way, six months into their first fundraise.

+

What criteria should fund managers use for LP lead scoring?

The five most predictive criteria for LP lead scoring are mandate fit, target ticket size, decision timeline, LP type priority, and relationship warmth. Score each on a 0-to-3 scale. Mandate fit assesses whether the LP invests in the fund's specific asset class, geography, fund stage, and strategy. Ticket size compares the LP's typical commitment range against the fund's target allocation per LP. Decision timeline evaluates whether the LP's investment committee cycle is compatible with the fund's close schedule. LP type priority depends on the fund's target LP mix: for most institutional PE funds, pension funds and endowments score highest on stability; family offices score higher on speed. Relationship warmth ranges from 3 for an existing LP considering a re-up to 0 for cold outreach with no prior relationship. Total score ranges from 0 to 15. LPs scoring 12 to 15 receive active pursuit. Scores of 8 to 11 get light-touch maintenance. Below 8, deprioritize for the current fundraise cycle.

+

What documents are typically involved in LP due diligence?

LP due diligence involves several distinct document categories, each with different volume and processing requirements. The investment diligence package includes the private placement memorandum, audited financial statements, portfolio company performance data, track record documentation, and team bios. LPs then issue a due diligence questionnaire, either the ILPA standard template, an AIMA-based format, or a proprietary institutional questionnaire, covering strategy, investment process, risk management, compliance, and operations. Institutional LPs also conduct operational due diligence, a separate document-intensive process covering valuation policies, custody arrangements, IT security, business continuity, and compliance infrastructure. At the commit stage, subscription documents collect commitment amounts, entity structures, side letter elections, and KYC/AML materials. A fund closing with 30 LPs processes thousands of pages of these documents in parallel. AI handles the extraction and triage at each document stage, routing only exceptions and incomplete items to human reviewers.

+

How can AI help fund managers process investor documents faster?

Fund managers evaluating investor CRM options should look for five capabilities. First, customizable pipeline stages that mirror the fund's actual workflow: source, qualify, engage, diligence, and commit, each with distinct fields and task structures. Second, document status tracking integrated into each LP record, not in a separate system, so the full relationship context is visible alongside the diligence timeline. Third, automated task sequencing for follow-up actions, surfacing outstanding items rather than relying on team members to remember to check. Fourth, a lead scoring framework that can be configured to the fund's specific criteria and maintained across the full team without eroding over time. Fifth, API integrations with the fund's fund administration platform and document processing tools, so that data extracted from subscription documents and DDQ responses flows into the LP record automatically. General-purpose CRMs including Salesforce, Affinity, and HubSpot are used successfully by fund managers when properly configured. Purpose-built investor CRM platforms add fund-specific context but require the same configuration discipline to be effective.

+

What should fund managers look for in an investor CRM?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.