13 min read

—

A mid-market PE firm receives 200 to 300 Confidential Information Memoranda (CIMs) per year. Fewer than 5% result in a closed deal. But every CIM that reaches the deal team still requires a preliminary investment memo before anyone decides whether to pursue or pass. Producing that memo manually takes four to eight hours of analyst time. At 200 CIMs per year, that is 800 to 1,600 analyst hours spent on preliminary documents alone, before a single hour of full due diligence begins.

This article covers the CIM to Preliminary Investment Memo (PIM) step specifically. Not the final investment memo produced after full due diligence; that is a later and heavier document. The PIM is the internal screening memo produced within 48 to 72 hours of receiving the CIM, used to present the opportunity to the Investment Committee (IC) for a go-no-go decision. AI compresses that production time from six to eleven hours to under three. This guide explains how, step by step.

For a broader view of how machine learning fits into private equity deal workflows, see the linked article. Here we focus narrowly on the CIM-to-PIM step: what the documents contain, where the manual process breaks, and how AI-assisted workflows handle it correctly.

In this article:

What a CIM is and who receives it on the buy side

What a Preliminary Investment Memo contains and how it differs from the final IC memo

Why manual CIM-to-PIM conversion is a deal velocity problem

A five-step AI workflow for CIM analysis and PIM generation

What to evaluate when selecting an AI tool for this workflow

AI for document processing

Turn a 200-page CIM into a memo in two hours

Get started today

What Is a CIM in Private Equity?

The Confidential Information Memorandum (CIM) is a 50 to 200 page document prepared by the target company's investment bank and distributed to qualified potential acquirers after NDA execution. It is the sell side's primary marketing document: a structured overview of the business designed to generate competitive bids. Typical sections cover the executive summary, company history, products and services, management team, market analysis, three to five years of financial performance, and growth opportunities.

The PE buy-side analyst is the recipient of the CIM, not its author. This matters because most AI content about CIM analysis is written for investment bankers summarising a CIM to produce a sell-side teaser. That is a different workflow: a different audience, a different output, a different time constraint. The buy-side PE analyst receives the CIM and must produce an internal document for their own deal team: the Preliminary Investment Memo.

PE firms and other financial sponsors receive CIMs for two reasons. Either a bank has run a formal sale process and invited the firm to participate, or a proprietary deal source has provided CIM-equivalent documentation for a less-contested transaction. In either case, the analyst's job is the same: read the document, extract what matters, and produce an IC-ready screening memo within 48 to 72 hours.

What Is a Preliminary Investment Memo and What Does It Contain?

The Preliminary Investment Memo (PIM), sometimes called an initial investment memo, investment screening memo, or deal screening memo depending on the firm, is the first internal document the deal team produces after initial CIM review. It is presented to the IC for screening approval: the decision to commit analyst resources to full due diligence, or to pass.

The Four-Document Private Equity Deal Workflow

The PIM sits at a specific point in the deal document lifecycle. Understanding where it falls clarifies why it is the highest-impact point for AI intervention:

Document | Stage | Produced by | Purpose | Typical length |

|---|---|---|---|---|

Teaser | Pre-NDA | Sell-side banker | Anonymised deal marketing overview | 1–2 pages |

CIM | Post-NDA | Sell-side banker | Detailed business overview for buyers | 50–200 pages |

PIM | After CIM review | PE buy-side analyst | Internal IC screening memo | 30–40 pages |

Final Investment Memorandum (FIM) | After full due diligence | PE deal team | Final IC approval memo | 50–100 pages |

The four-document PE deal workflow. The PIM sits between CIM receipt and full due diligence commitment: the go-no-go decision gate that determines whether the firm invests analyst weeks into a deal.

The PIM is lighter than the FIM by design. It is based primarily on the CIM rather than full diligence findings. Its purpose is not to make the final investment decision. It is to determine whether the opportunity is worth investigating at all.

Standard PIM Sections

Most PE firms structure their preliminary memos around eight sections, though naming conventions vary by firm:

Executive Summary: deal overview, target company, preliminary valuation range, headline investment thesis

Company Overview: business model, products and services, customer profile, geographic footprint

Financial Summary: extracted revenue, Earnings Before Interest, Tax, Depreciation, and Amortisation (EBITDA), margins (three-year actuals), growth trajectory, key ratios

Market Analysis: industry size, growth rate, competitive dynamics sourced from the CIM market section

Investment Highlights: why this deal fits the firm's mandate (sector, size, growth profile)

Key Risks and Open Questions: material risks identified in the CIM; questions requiring diligence resolution

Mandate Fit Assessment: structured check against investment criteria: size, sector, geography, EBITDA threshold, holding period alignment

Recommended Next Steps: proceed to first-round bid, pass, or request additional information

This structure is what AI must populate from the CIM. Each section maps directly to content that exists somewhere in a 200-page document. But finding it, extracting it accurately, and organising it into the firm's format is the bottleneck.

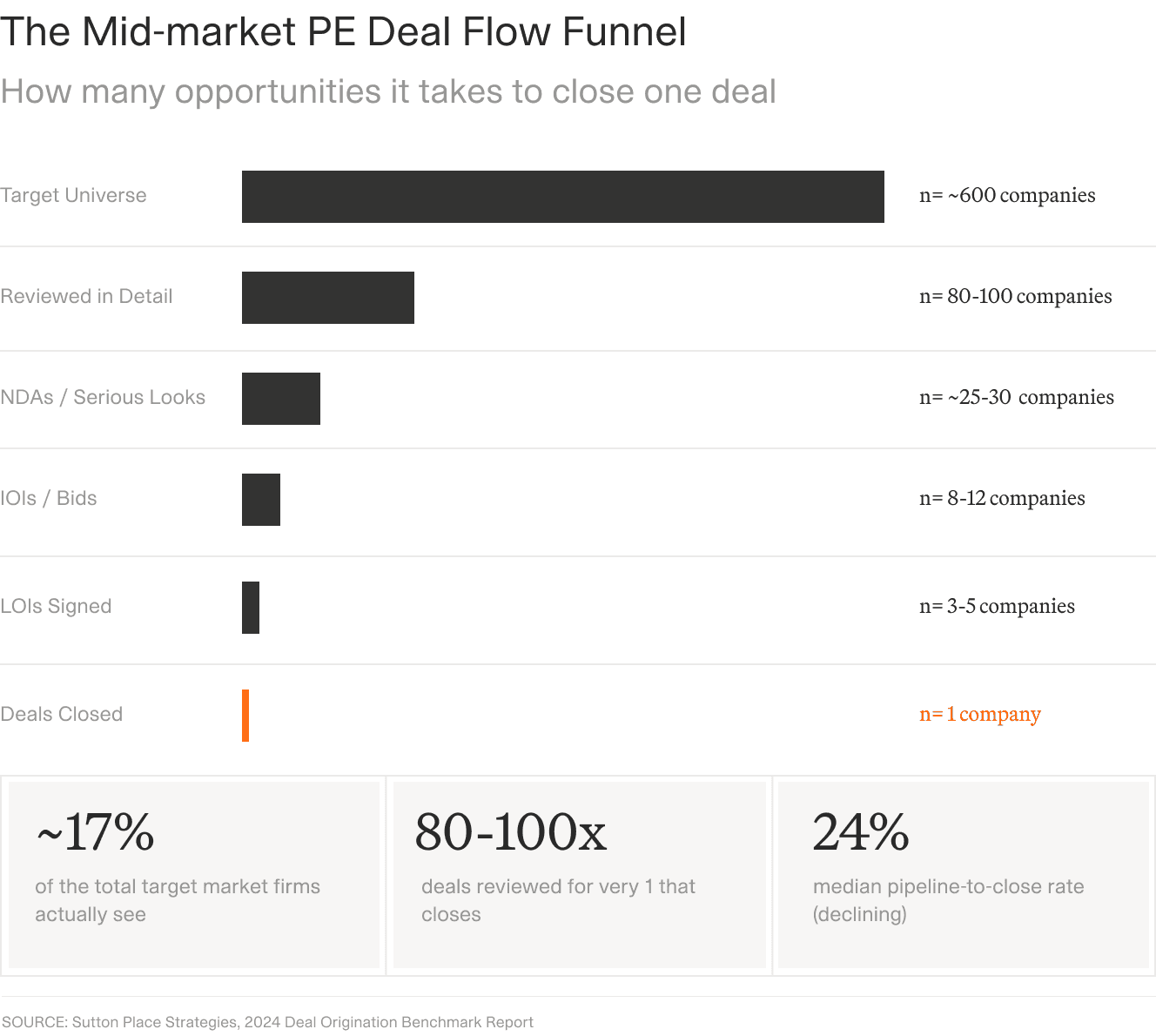

Mid-market PE firms review 80 to 100 deals for every closed transaction. Each one enters the CIM-to-PIM pipeline. At that volume, the time cost of manual preliminary memo production becomes structural, not incidental.

Why Manual CIM-to-PIM Conversion Is a Deal Velocity Problem

CIM data is unstructured. Financial tables are embedded in PDFs, not spreadsheets. Metrics are scattered across 200 pages without machine-readable labels. Revenue figures may appear in three different places with three slightly different numbers, and the analyst must determine which is the correct basis for the PIM.

The manual workflow looks like this: the analyst reads the full CIM, extracts 30 to 40 key data points into an internal template, writes narrative sections, formats the memo to the firm's standard, and sends it to a VP for review. At a firm processing 200 CIMs per year, each requiring six hours of analyst time, that is 1,200 analyst hours — roughly 30 working weeks, spent on preliminary documents before any full due diligence begins.

But there is a second, harder problem: deal speed.

PE deal processes are competitive. The team that gets to a non-binding Indication of Interest (IOI) first often has a negotiating advantage. A three-day delay in IC screening, because the preliminary memo is still being drafted, delays the IOI submission and signals to the bank that the firm is slow. In competitive auctions, that matters.

What Goes Wrong with Generic AI Tools for CIM Analysis

The obvious solution is to drop the PDF into ChatGPT or Claude and ask it to produce a memo. It creates a different problem.

Wrong. Generic large language models without source grounding will invent financial figures. Not occasionally. McKinsey's September 2025 analysis of ungoverned AI tools in due diligence found they generated peer sets that ignored business model nuances, surfaced cost estimates disconnected from operational realities, and hallucinated metrics from misinterpreted text. In the AI due diligence context, a fabricated EBITDA margin in a preliminary memo leads to a wrong IC screening decision, and potentially a wrong first-round bid.

Three other failure modes appear consistently:

Context window limitations. Standard models may not handle a 200-page CIM in a single pass. Chunking the document into segments introduces inconsistencies: the revenue figure in section one may not match the summary in section seven.

Data security. CIMs contain material non-public information. Uploading them to a non-approved AI platform violates the firm's AI usage policy and, in some cases, NDA terms. This is not a minor concern.

Template mismatch. Generic AI outputs a generic memo. PE investment committees expect the firm's own format, with their section headers, exhibit labels, and narrative style. A correctly structured PIM that looks wrong to the IC is still a problem.

The solution is not "don't use AI." It is using workflow-appropriate AI that handles document size, source grounding, and template customisation correctly.

How AI Automates the CIM-to-PIM Workflow: A Step-by-Step Breakdown

A properly configured AI workflow for CIM-to-PIM automation runs five sequential steps. The analyst's role shifts from data assembly to judgement and refinement, which is where the analyst's value actually lies.

Step 1: CIM Ingestion

Upload the CIM PDF, or the full data room package including a management presentation and any supplemental financial model outputs. The AI reads the full document in a single context pass. No chunking required for standard CIM lengths. Platforms that support multimodal ingestion handle scanned PDFs and image-heavy CIMs through optical character recognition, so a scanned 180-page document does not require manual pre-processing.

Step 2: Structured Data Extraction

The AI identifies and extracts the 30 to 40 data points a PIM requires: revenue (three-year actuals), EBITDA, margins, growth rates, customer metrics, geographic breakdown, management team, product and service description, market size estimates. Each extracted figure is linked to its source location in the CIM: the exact page, table, and paragraph where the figure appears. This source citation is not a convenience feature. It is the audit trail that makes an IC presentation defensible. "The AI said so" is not acceptable documentation. "Page 47, Table 3, footnote 2" is.

Step 3: Mandate Fit Check

The extracted data is compared against the firm's investment criteria: sector focus, enterprise value range, EBITDA floor, geographic constraints, holding period alignment. AI flags whether the deal meets, partially meets, or fails the mandate. This happens before any narrative is drafted. A CIM that fails the mandate check on deal size (for example, an enterprise value of $30M against a firm that does not invest below $75M) should be passed without consuming PIM production time at all. The mandate fit check is the triage gate that makes the rest of the workflow viable at 200 CIMs per year.

Step 4: PIM Draft Generation

For deals that pass the mandate check, the AI populates the firm's PIM template with extracted data and drafts narrative sections: investment thesis, company overview, market analysis, key risks. The draft uses the firm's section headers, formatting standards, and exhibit style. It reads like a first-pass analyst draft: structured, sourced, and approximately 80% of the way to the final document for a mandate-fit deal.

Step 5: Analyst Review and Refinement

The analyst reviews for accuracy, adds strategic judgement (management assessment, qualitative competitive positioning, gut-check on the investment thesis), corrects any extraction errors, and approves the final PIM for IC submission. This step still requires an hour or two. It is the step where the analyst's expertise actually matters.

Here is what the time comparison looks like in practice:

Step | Manual time | AI-assisted time |

|---|---|---|

CIM read and data extraction | 3–5 hours | 10–20 minutes |

Mandate fit assessment | 30–60 minutes | 2–5 minutes |

PIM draft (all sections) | 2–4 hours | 20–40 minutes |

Analyst review and refinement | 1–2 hours | 1–2 hours |

Total | 6–11 hours | 1.5–3 hours |

At 200 CIMs per year, a 65 to 75% reduction in PIM production time frees 800 to 1,000 analyst hours annually — roughly two full analyst years redirected from data assembly to deal judgement.

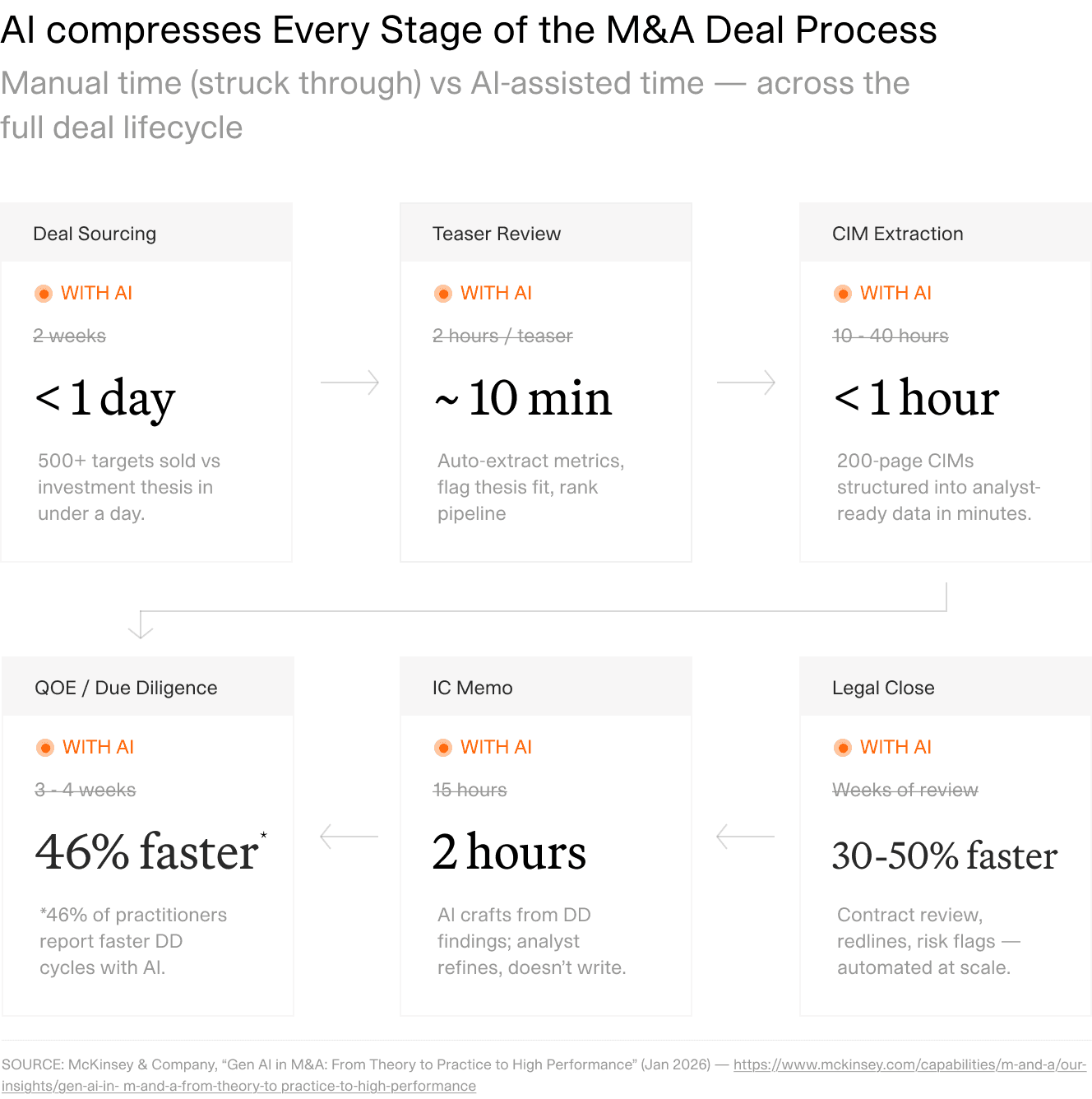

The V7 Go CIM analysis automation covers this full five-step sequence. For context on how this fits the broader deal workflow, the McKinsey January 2026 report on gen AI in M&A documents CIM extraction compressing from 10 to 40 hours to under one hour across the market, consistent with the step-level timing above.

AI compresses every major stage of the M&A deal process. CIM extraction, from 10 to 40 hours down to under one hour, is the highest-impact single step for PE buy-side teams. Source: McKinsey & Company, Gen AI in M&A, January 2026.

Key Considerations When Choosing an AI Tool for CIM-to-PIM Workflows

Not every AI tool that can summarise a document can run a CIM-to-PIM workflow reliably. PE deal teams evaluating options should test against six specific criteria, and source traceability is the one that most generic tools fail first.

Document size handling. Can the tool process a 200-page CIM in a single pass without chunking? Chunking introduces figure inconsistencies. Ask vendors specifically: what is the maximum document length, and how is it handled above that limit?

Source citation and audit trail. Does every extracted figure link back to its CIM page, table, and paragraph? IC reviewers and compliance teams need to verify assumptions. This is the non-negotiable criterion. If the tool cannot show you where it got the EBITDA figure, the tool is not appropriate for this workflow.

Data security and confidentiality. SOC 2 Type II certification; no data residency on vendor servers; compliance with the firm's AI usage policy. CIMs contain material non-public information and are distributed under NDA. The Sutton Place Strategies 2024 Deal Origination Benchmark Report documents deal teams processing 80 to 100 CIMs per close: at that volume, an insecure AI tool is a systematic compliance risk, not an isolated incident.

Template customisation. Can the AI output to the firm's own PIM template, not a generic format? IC members expect the memo to look the way it always has. A correctly structured memo that uses the wrong headers or exhibit labels still requires significant reformatting.

Mandate fit check capability. Can the tool be configured with the firm's investment criteria so it automatically flags mandate alignment before drafting begins? This is the feature that makes the workflow viable at scale, not just faster but selective.

Accuracy and hallucination controls. How does the tool handle uncertainty? The right answer is: it flags low-confidence extractions for human review and cites sources for every output. The wrong answer is: it presents all outputs with equal confidence regardless of source quality.

How V7 Go Handles the CIM-to-PIM Workflow

V7 Go's CIM-to-PIM workflow covers all five steps described above in a single configured agent. The AI investment memo generation automation ingests the full CIM, extracts structured data with field-level source citations, runs the mandate fit check against configurable criteria, and populates the firm's PIM template.

The visual grounding capability is the specific feature that makes this IC-defensible. Every extracted figure (revenue, EBITDA, margin, deal size) is linked to the exact page, table, and cell in the CIM where it appears. Click on "EBITDA: $45M" in the PIM draft and see the table and footnote in the source document. That citation chain is not optional in PE. It is how the IC knows the preliminary memo is based on the document, not on the model's prior training.

Multi-document handling covers the full data room: if a management presentation accompanies the CIM, V7 Go extracts from both and cross-references figures before populating the PIM. V7 Go flags conflicting figures between documents for analyst review rather than silently resolving them.

For data security: V7 Go is SOC 2 Type II certified, uses end-to-end encryption, and does not train on client data. The McKinsey September 2025 analysis of AI-assisted due diligence identifies data governance as the primary barrier to AI adoption in PE. V7 Go's architecture is designed specifically to satisfy the compliance requirements of regulated financial firms.

The V7 Go agent is also configurable without code. Define the firm's investment criteria once (sector focus, enterprise value range, EBITDA floor, geographic constraints), and the mandate fit check runs automatically on every CIM processed. A firm receiving 200 CIMs per year can set up a triage layer that filters out non-mandate deals before a single hour of PIM production time is spent. V7 Go's finance workflow in practice shows CIM data extraction with field-level source citations, Due Diligence Questionnaire (DDQ) completion, and structured output for deal team review, all from a single agent configuration.

The CIM to screening memo use case page documents the full workflow configuration for PE deal teams. The AI due diligence agent covers the downstream step once a deal has passed IC screening and full diligence begins.

From Preliminary Memo to Deal Conviction

Star Mountain Capital, a specialist credit and private equity firm focused on the US lower middle market, processes deal flow at the pace that makes manual CIM-to-PIM production a genuine constraint. The workflow described in this article (structured extraction, mandate fit check, template-matched draft, analyst refinement) is the architecture that turns a 200-page CIM into a defensible IC screening memo in under three hours rather than over a workday.

The point is not speed for its own sake. A faster PIM means the IC screen happens in 48 hours rather than five days, the IOI goes out while the deal is still warm, and the analyst who would have spent Tuesday extracting revenue figures from page 47 of a CIM is instead developing the investment thesis that differentiates the firm's bid. That is where a deal gets won or lost — not in the data assembly.

What is a CIM in private equity?

A Confidential Information Memorandum (CIM) is a 50 to 200 page document prepared by a target company's investment bank and distributed to qualified potential acquirers after they have signed an NDA. It is the primary sell-side marketing document in a formal M&A sale process: a structured overview of the business designed to give financial sponsors and strategic buyers enough information to submit a preliminary bid. Typical CIM sections cover the executive summary, company history, products and services, management team, three to five years of financial performance, market analysis, and growth opportunities. The PE buy-side analyst is the recipient of the CIM, not its author. The investment banker who created it was working for the seller. The PE analyst's job, on receiving the CIM, is to review it and produce an internal screening document for their own deal team: the Preliminary Investment Memo, to decide whether to pursue or pass.

+

What is a preliminary investment memo?

A Preliminary Investment Memo (PIM), also called an investment screening memo or initial investment memo depending on the firm, is the first internal document a PE deal team produces after reviewing a CIM. It is presented to the Investment Committee (IC) for a screening decision: commit analyst resources to full due diligence, or pass. The PIM is produced within 48 to 72 hours of CIM receipt, before any full diligence work begins. It runs approximately 30 to 40 pages at most PE firms, though some firms produce shorter 10 to 15 page screening memos for a first-pass review. Standard PIM sections cover an executive summary, company overview, financial summary (three-year actuals extracted from the CIM), market analysis, investment highlights, key risks and open questions, a mandate fit assessment, and recommended next steps. The PIM is lighter and faster than the Final Investment Memorandum (FIM), which is produced after full due diligence and is used to support the final IC approval decision.

+

What is the difference between a preliminary investment memo and a final investment memo?

The Preliminary Investment Memo (PIM) and Final Investment Memorandum (FIM) serve different decisions at different stages of the deal lifecycle. The PIM is produced immediately after initial CIM review, typically within 48 to 72 hours, and is used to support the IC's go-no-go decision on committing to full due diligence. It is based primarily on the CIM, management presentation, and any supplemental data room materials available at the time. It runs 30 to 40 pages and its purpose is triage: does this deal meet our mandate and warrant the resource commitment of a full diligence process? The FIM is produced after full due diligence is complete, weeks or months later, and is used to support the final IC approval decision on a specific acquisition at a specific valuation. It incorporates findings from management meetings, third-party quality of earnings analysis, legal diligence, operational assessment, and financial modelling. It runs 50 to 100 pages and must be comprehensive enough to support an IC vote. AI's highest-value role is at the PIM stage, because that is where the volume is highest and the time constraint is tightest.

+

How long does it take to review a CIM?

Manual CIM review by a PE analyst takes four to eight hours per document, depending on CIM length (50 to 200 pages), complexity of the business, and the analyst's familiarity with the sector. Producing the Preliminary Investment Memo from that review adds another two to four hours for drafting, formatting, and VP review prep, bringing the total CIM-to-PIM time to six to eleven hours per deal. With an AI-configured workflow, structured data extraction from a 200-page CIM takes 10 to 20 minutes rather than three to five hours. The mandate fit check takes two to five minutes rather than 30 to 60 minutes. A PIM draft with all sections populated takes 20 to 40 minutes rather than two to four hours. The analyst review and refinement step, which still requires human judgement, takes one to two hours regardless of AI involvement. Total AI-assisted CIM-to-PIM time: 1.5 to 3 hours, a 65 to 75% reduction versus the manual workflow. At 200 CIMs per year, that reduction represents 800 to 1,000 analyst hours saved annually.

+

Can AI generate a preliminary investment memo without hallucinating?

Only if the platform meets three specific conditions. First, SOC 2 Type II certification: this confirms the vendor has been independently audited for information security controls appropriate for handling sensitive commercial data. Second, no data residency on vendor servers and no training on client data. The CIM must not be retained, stored, or used to improve the vendor's models after your session. Third, the platform must be approved under your firm's AI usage policy. Most PE firms have implemented specific policies governing which AI tools may be used with confidential deal data, and CIMs are typically classified as material non-public information subject to NDA terms. Uploading a CIM to a non-approved AI platform is a compliance violation under most firm policies and, in some cases, a breach of the NDA signed with the investment bank. The practical test: ask the vendor for their data processing agreement and SOC 2 report before uploading a live CIM. Consumer AI tools and free-tier plans from any vendor are not appropriate for this use case, regardless of the underlying model quality.

+

Is it safe to upload a CIM to an AI tool?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.