17 min read

—

A step-by-step framework covering six weighted dimensions, three thesis-based weighting profiles, a worked example, and an AI workflow that auto-populates scorecard fields from CIM documents.

A mid-market PE firm reviewing 200 CIMs a year has a consistency problem. The analyst who screens a deal on Monday is not the analyst who chairs the IC discussion two weeks later. The criteria the buyout team applies in Q1 are not precisely the same criteria they apply in Q4. By the time a promising deal reaches the investment committee (IC), the question is not always whether the business is attractive. Often the question is whether everyone on the team evaluated it against the same framework.

A deal evaluation scorecard fixes this. It gives every member of the deal team a shared reference point: the same six dimensions, the same weighting, the same 1–10 scale, applied consistently to every opportunity reviewed. Instead of debating whether a company is interesting, the conversation shifts to which dimensions score above threshold and which do not.

This guide covers the complete pre-deal scorecard framework used by PE practitioners: the six core dimensions, how to weight them for your investment thesis, a worked example with hypothetical scores for a mid-market industrial company, how to set pre-scorecard gate criteria that disqualify deals before scoring begins, and how AI can auto-populate scorecard fields directly from Confidential Information Memoranda (CIMs).

In this article:

What a PE deal scorecard is and how it differs from a portfolio monitoring scorecard.

The six dimensions every PE deal scorecard should cover, with scoring guidance for each.

How to weight the scorecard for buyout, growth equity, and distressed strategies.

A worked example: a hypothetical mid-market company scored across all six dimensions.

Pre-scorecard gate criteria that automatically disqualify a deal before scoring begins.

How AI auto-populates scorecard fields from CIM documents in five steps.

Five common deal scorecard mistakes and how to fix them.

AI for document processing

Auto-populate deal scorecards directly from CIM documents

Get started today

What Is a PE Deal Scorecard? (And What It Is Not)

A PE deal evaluation scorecard is a structured scoring framework that evaluates potential investment targets across a fixed set of weighted dimensions, converting the subjective assessment of a CIM or teaser into a comparable, repeatable score.

Each dimension is assigned a weight that reflects the firm's investment thesis, and an analyst scores the company 1–10 on each. The weighted total determines whether the deal advances to second-pass diligence or is passed.

That definition is worth pausing on, because it reveals what a deal scorecard is not.

A deal scorecard is not a due diligence checklist. Diligence checklists track whether specific documents have been received and reviewed. A scorecard evaluates the quality of what those documents contain. It is not an investment committee (IC) memo template, which is a narrative document prepared for a decision-maker audience. And it is not a legal or compliance review tool, which focuses on liability and risk exposure rather than investment attractiveness.

There is also a second, commonly confused type of scorecard that this article does not cover: the portfolio monitoring scorecard. A portfolio monitoring scorecard tracks key performance indicators (KPIs) for existing portfolio companies after acquisition: EBITDA improvement year-on-year, working capital changes, headcount efficiency ratios. That is a portfolio management tool, not a deal evaluation tool. Mixing criteria from both leads to evaluating new deals on post-acquisition metrics that cannot be measured from a CIM, which is one of the most persistent sources of scorecard failure in PE firms.

This article covers only the pre-deal screening scorecard: the framework applied to new targets at the top of the funnel, before significant analytical resources are committed.

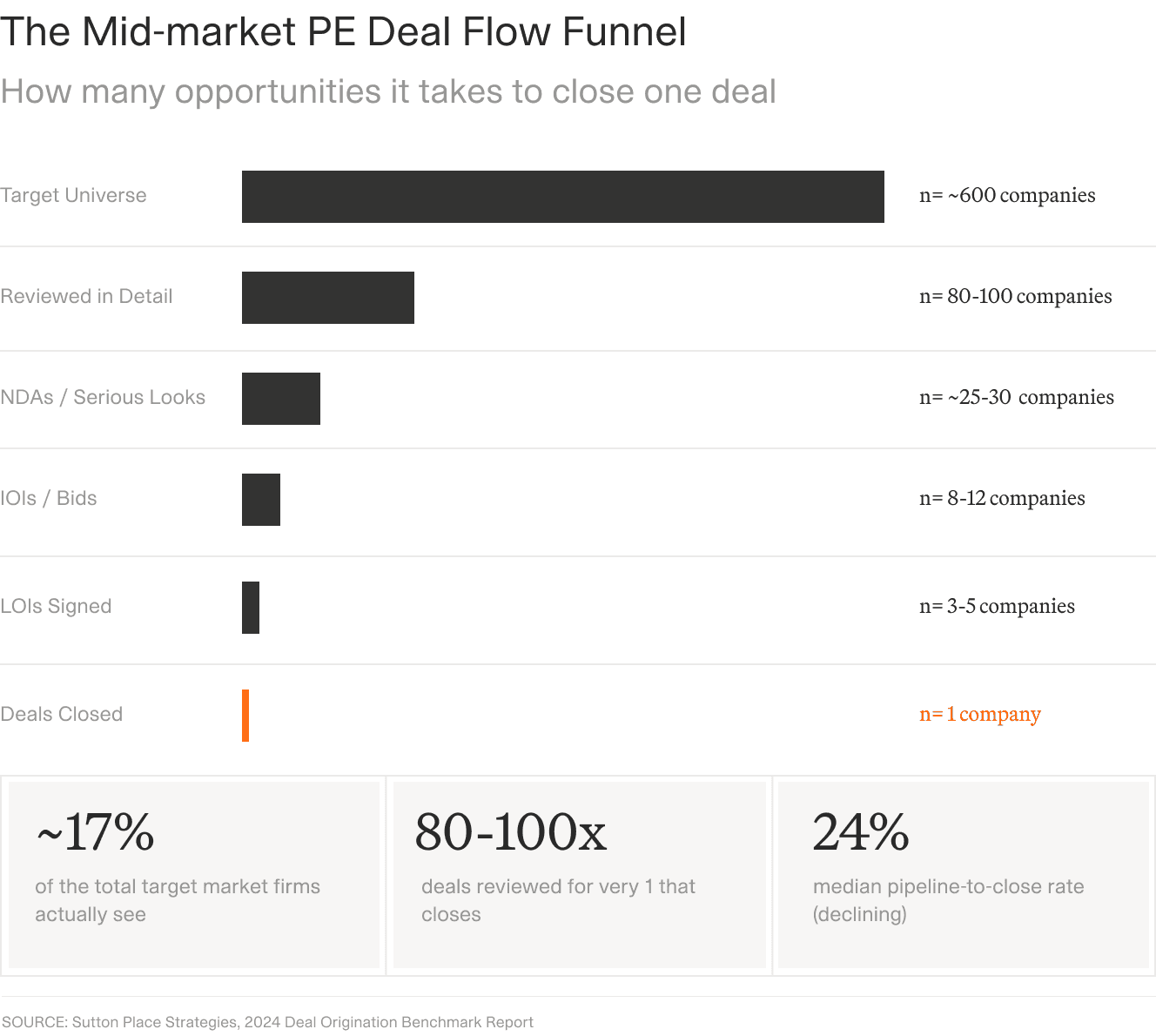

The deal funnel shows why a standardised evaluation scorecard matters. With 80–100 deals reviewed per close, applying consistent investment criteria at the screening stage is the difference between a structured selection process and an informal one.

The 6 Dimensions of a PE Deal Scorecard

Most PE firms use between four and eight dimensions. Six is the practitioner standard because it covers the full investment thesis without creating scoring fatigue or forcing analysts to populate overlapping fields for every deal. The six dimensions below appear consistently across buyout, growth equity, and distressed PE frameworks.

1. Financial Quality

Financial Quality is the foundation of any PE deal scorecard because it determines whether the business has the earnings profile to support an acquisition. The key data points are: normalised Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA) and the Quality of Earnings (QoE) adjustments required to reach it; revenue growth rate over the trailing three years and the consistency of that growth; gross margin profile and whether margins are expanding or contracting; cash conversion cycle and free cash flow quality; and leverage capacity, typically assessed as debt service coverage relative to normalised EBITDA.

Scoring guidance: a company with EBITDA margins consistently above 20%, revenue growing at 10–15% annually with no single year below 5%, and no single customer representing more than 15% of revenue would score 8 to 9 out of 10. A company with margins below 10%, flat or declining revenue, or QoE adjustments reducing reported EBITDA by more than 20% would score 3 to 4. Build a reference deal for each tier to calibrate scoring consistently across your team.

2. Thesis Fit

Thesis Fit evaluates whether the target matches the fund's mandate on sector, geography, size, and ownership structure, and whether it aligns with the firm's specific investment thesis. A UK mid-market buyout fund with a mandate of £20–80m EBITDA businesses applies a different Thesis Fit rubric from a pan-European growth equity fund targeting £5–20m revenue software-as-a-service companies.

Beyond mandate screening, Thesis Fit asks whether the target's value creation story aligns with the capabilities the PE firm brings. A fund with strong operational improvement expertise in B2B services should weight Thesis Fit heavily on the operational lever, not just the sector. Funds with tight mandates often assign 25–30% weight to this dimension; generalist funds weight it lower, typically 15–20%.

3. Market Position and Competitive Moat

Market Position evaluates the quality of the business's competitive standing: market share and whether it is growing or declining, barriers to entry (intellectual property, switching costs, network effects, exclusive distribution contracts), supplier and customer concentration risk, and end-market dynamics (growth rate, cyclicality, regulatory tailwinds or headwinds).

Scoring guidance: a company with 15% market share, four active patents, and a long-term exclusive distribution agreement with a major industrial group scores very differently from a company with the same market share but no IP, commodity pricing, and three customers representing 60% of revenue. The competitive moat is more important than the market share percentage in most PE investment criteria frameworks.

4. Management Team Quality

Management Team Quality evaluates leadership across three axes: experience (sector track record, prior PE-backed company experience, prior exits), depth (whether value is concentrated in the founder/CEO or distributed across the second and third tier), and alignment (commitment to the exit timeline and compatibility with the PE firm's operating style).

A frequently overlooked scoring criterion is coachability. PE-backed growth requires management to accept external input on strategy, reporting standards, and operational practices. A high-performing but rigid team that resists board-level direction may score lower on this dimension than a mid-tier team with a demonstrated willingness to operate inside a PE framework. This is particularly relevant for first-time PE-backed businesses where management has never worked with a financial sponsor before.

5. Value Creation Potential

Value Creation Potential reflects what the specific PE firm believes it can do with the business, not just what the business is today. Organic growth levers include pricing headroom, new geographic or product markets, and capacity expansion. Inorganic potential includes identified bolt-on acquisition candidates that could accelerate the investment thesis. Operational improvement opportunities include margin expansion through procurement optimisation, working capital improvement, and overhead rationalisation. Technology and digital transformation investments that unlock scale are increasingly relevant across industrial and business services sectors.

A company that looks mediocre on Financial Quality may score 8 or 9 out of 10 on Value Creation Potential if the PE firm has a directly applicable operational playbook. This is where thesis-based scoring creates genuine differentiation from a generic evaluation framework: the same target company scores differently for different buyers, as it should.

6. Exit Route Clarity

Exit Route Clarity evaluates the realism of the exit plan within the fund's target hold period, typically three to seven years. The minimum requirement for a score above 5 out of 10 is at least two credible exit routes: at least one strategic acquirer with a documented history of buying comparable businesses, and either an active secondary buyout market or a plausible initial public offering (IPO) pathway. The dimension also incorporates comparable transaction multiples, the macro sensitivity of exit valuations in the sector, and whether the exit story relies on EBITDA multiple expansion or on operational value creation.

How to Weight Your Scorecard for Your Investment Thesis

The most common scorecard mistake in PE firms is distributing weights equally across all six dimensions, giving each roughly 17% weight. Equal weighting ignores that different investment strategies have fundamentally different primary value drivers. A buyout fund and a growth equity fund looking at the same target company should reach different conclusions if they apply thesis-appropriate weights, which is correct, because they are evaluating different value propositions.

The table below shows three illustrative weighting profiles. These are starting points for calibration, not prescriptions. Every firm should adapt weights to its own mandate, sector expertise, and historical deal data.

Dimension | Buyout (control) | Growth equity | Distressed / turnaround |

|---|---|---|---|

Financial Quality | 30% | 15% | 20% |

Thesis Fit | 20% | 25% | 15% |

Market Position | 15% | 25% | 15% |

Management Team | 15% | 20% | 25% |

Value Creation Potential | 10% | 10% | 20% |

Exit Route Clarity | 10% | 5% | 5% |

Total | 100% | 100% | 100% |

The buyout weighting logic: buyout firms rely on existing cash flow to service acquisition debt — the business must already generate reliable earnings, which is why Financial Quality receives 30% weight. Exit Route Clarity is weighted at only 10% because buyout targets typically have established secondary buyout markets and identifiable strategic acquirer pools.

The growth equity weighting logic: growth equity firms are acquiring future earnings growth in an expanding market. They discount current Financial Quality and weight Market Position and Thesis Fit heavily because the bet is on Total Addressable Market (TAM) expansion and the firm's capacity to accelerate it. A company with thin margins today but a defensible position in a growing market scores well under this profile.

The distressed weighting logic: turnaround success is almost entirely a management execution question. The Management Team dimension receives 25% weight because without the right leadership and an aligned PE partnership, operational recovery is unlikely regardless of the underlying asset quality. Value Creation Potential also receives a higher weight (20%) because the entire investment thesis depends on the firm's ability to unlock it.

Scoring calibration is as important as the weighting itself. For each dimension, anchor the scale with at least three exemplar deals: a reference deal that scored 3 out of 10, one at 6, and one at 9. Run calibration sessions quarterly, where the deal team independently scores the same reference deal and compares results. Divergence of more than two points on any dimension signals that the rubric needs tightening before the next evaluation cycle begins.

Building the Scorecard: A Worked Example

The following example applies the buyout weighting profile to a hypothetical target company: ProSeal Group, a UK mid-market manufacturer of industrial protective coatings with £38m revenue and £8.4m normalised EBITDA. The purpose is to illustrate how the scorecard converts CIM data into a structured evaluation rather than to reflect any real company or transaction.

Dimension | Weight | Score (1–10) | Weighted score | Key evidence from CIM |

|---|---|---|---|---|

Financial Quality | 30% | 8.0 | 2.40 | 22% EBITDA margin; 11% 3-year revenue CAGR; no single customer above 18%; three years audited financials |

Thesis Fit | 20% | 9.0 | 1.80 | Exact mandate match (£5–15m EBITDA, UK industrial, owner-managed); aligns with firm's operational improvement thesis |

Market Position | 15% | 7.0 | 1.05 | 8% UK market share; four active patents; exclusive 5-year supply contract with a major infrastructure group |

Management Team | 15% | 7.5 | 1.13 | CEO 12 years sector experience, one prior exit; CFO 6 years in post; second tier thin (two of four director-level roles vacant) |

Value Creation Potential | 10% | 8.5 | 0.85 | Three identified bolt-on acquisition targets in adjacent regions; pricing headroom estimated at 8%; margin expansion available through procurement consolidation |

Exit Route Clarity | 10% | 7.0 | 0.70 | Two strategic acquirers with documented acquisition history in sector; secondary buyout market active at 7–9× EBITDA |

Total | 100% | N/A | 7.93 / 10 | Recommendation: proceed to second-pass diligence |

At 7.93 out of 10, ProSeal Group would advance to second-pass diligence under most buyout team thresholds (typically set between 6.5 and 7.5). The scorecard surfaces the primary risk of second-tier management thinness in the first read of the CIM — before an analyst spends three weeks on financial modelling. The key question generated for the management presentation: how does the business plan to fill the two vacant director-level roles, and is there succession depth for the CFO position ahead of a transaction?

Pre-Scorecard Gates: When to Disqualify Before Scoring

Not every deal that arrives should reach the scorecard. Pre-scorecard gate criteria are hard disqualifiers: conditions that, if present, mean the deal should not consume analyst time on dimension scoring. They protect the scorecard from being applied to opportunities that have already been implicitly rejected on fundamental grounds.

The following conditions should trigger an automatic pass at the gate stage, before any dimension is scored:

Hockey-stick revenue projections with no historical precedent. If the CIM projects 40% revenue growth in years 4 and 5 but shows 5% average growth over the prior three years, the projection is not credible without a structural explanation. Disqualify and request a revised financial model with documented assumptions before proceeding.

Unresolved material litigation exceeding 5% of estimated enterprise value (EV). Litigation at this scale creates valuation uncertainty that scoring cannot adequately capture. Place the deal on hold until a legal opinion is received.

Customer concentration above 50% in a single customer without a long-term contracted relationship. This level of concentration makes the business value functionally dependent on one renewal decision, a structural risk that cannot be meaningfully scored on a 1–10 dimension scale.

No audited financials for at least two years. Without audited accounts, normalised EBITDA cannot be established with confidence. The Financial Quality dimension cannot be scored accurately, which undermines the reliability of the entire scorecard output.

Management unwilling to commit to a full hold period. If the CEO has stated or implied an intention to exit within 12–18 months of transaction close, the value creation plan cannot be executed by the existing team. This creates a score floor on the Management Team dimension that will typically place the deal below any reasonable threshold regardless of scores elsewhere.

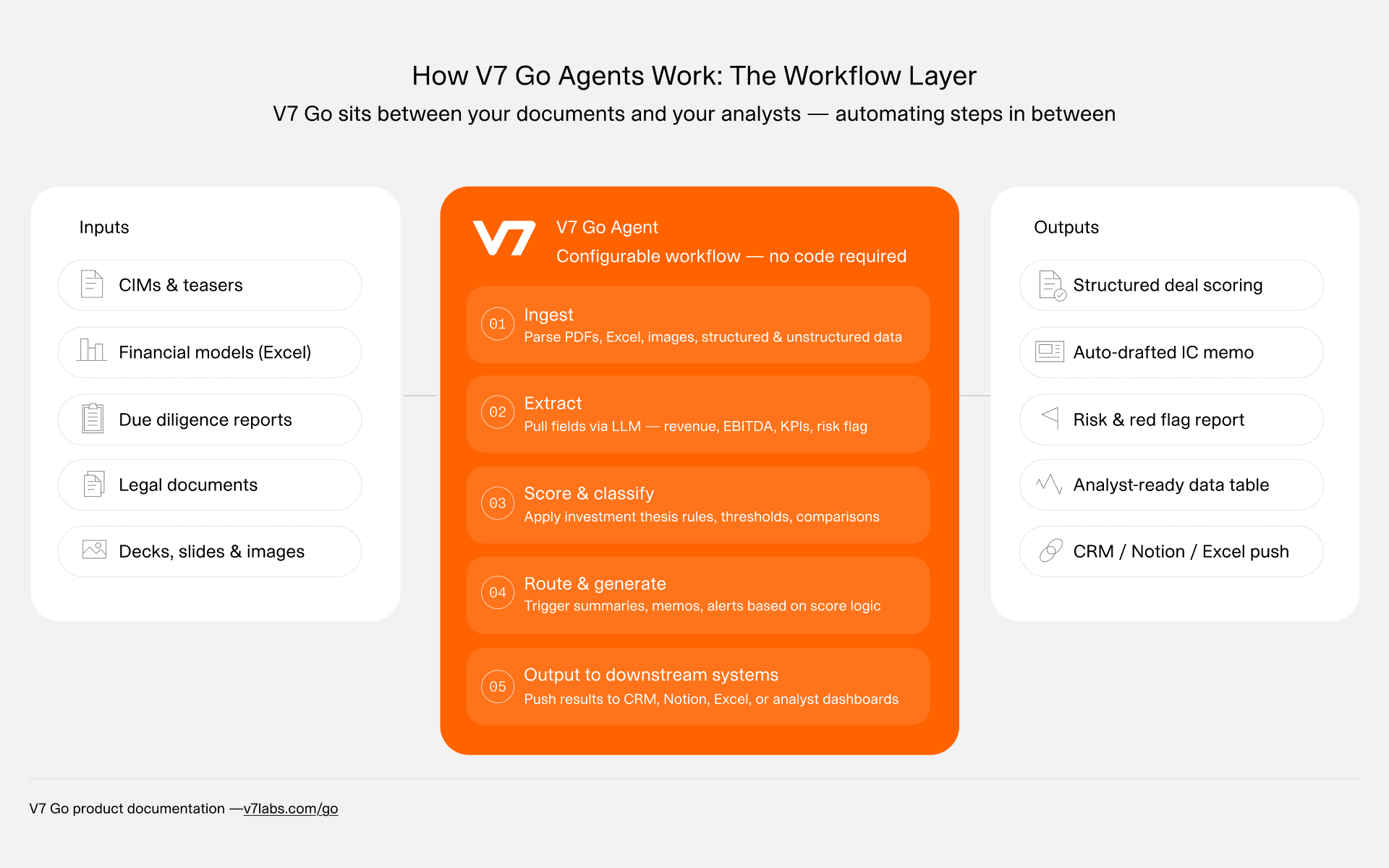

Review gate criteria against the CIM before opening the scorecard. The CIM to Screening Memo workflow in V7 Go checks gate conditions automatically at document ingestion, surfacing disqualifiers before any analyst begins scoring.

How AI Automates Deal Scorecard Population in Private Equity

A mid-market PE firm that reviews 200 CIMs a year, each requiring 2 to 3 hours of analyst reading and data extraction before a preliminary scorecard can be produced, is spending between 400 and 600 analyst hours per year on pre-scorecard data entry. This time does not improve the quality of deal evaluation; it merely prepares the inputs. AI agents eliminate this bottleneck by reading CIM documents and extracting structured scorecard data automatically, at consistent quality across every deal reviewed.

V7 Go Agents process CIMs and deal documents through a five-step pipeline that produces a structured scorecard output, a flagged risk summary, and a data table ready for the IC memo.

The five-step AI workflow for deal scorecard automation works as follows.

Step 1: Ingest. Connect your data room, email inbox, or document repository to V7 Go. Supported formats include PDF (CIMs, teasers, management presentations), Word documents, and Excel financial models. Drop in your CIM exactly as it arrived: no reformatting, no template required. V7 Go ingests the full document set as-is.

Step 2: Extract. The Agent reads each document and extracts structured data for each scorecard dimension. For Financial Quality: normalised EBITDA, revenue growth rate, gross margin trajectory, and customer concentration are pulled from financial summaries and QoE tables. For Market Position: sector descriptions, market share claims, and competitive moat statements are extracted from the business overview section. For Management Team: founders' years of experience, prior exits, and ownership stakes are identified from the leadership pages. The extraction is traceable — every data point links back to the exact paragraph and page number in the source document, so analysts can verify any figure in seconds.

Step 3: Score. The extracted data is mapped against your firm's scoring rubric. The Agent applies the weighting profile your team has configured (buyout, growth equity, or a custom profile) and produces a preliminary score for each dimension. The score is a starting point for analyst review, not a replacement for it. Analysts see both the score and the extracted evidence that generated it, side by side.

Step 4: Flag. V7 Go automatically highlights gate conditions and red flags: customer concentration above the configured threshold, missing audited financials, revenue projections inconsistent with historical growth rates, management ownership below a threshold that suggests limited alignment. These surface at the top of the scorecard output before dimension scores are reviewed, so the most material risks are visible immediately.

Step 5: Output. V7 Go generates a structured scorecard brief: dimension scores, weighted aggregate, flagged conditions, and three to five key questions for the management presentation. This output can be loaded directly into the Dataroom to IC Memo workflow. A CIM that previously required 2.5 hours of analyst reading and data extraction now produces a preliminary scorecard in under 10 minutes per deal.

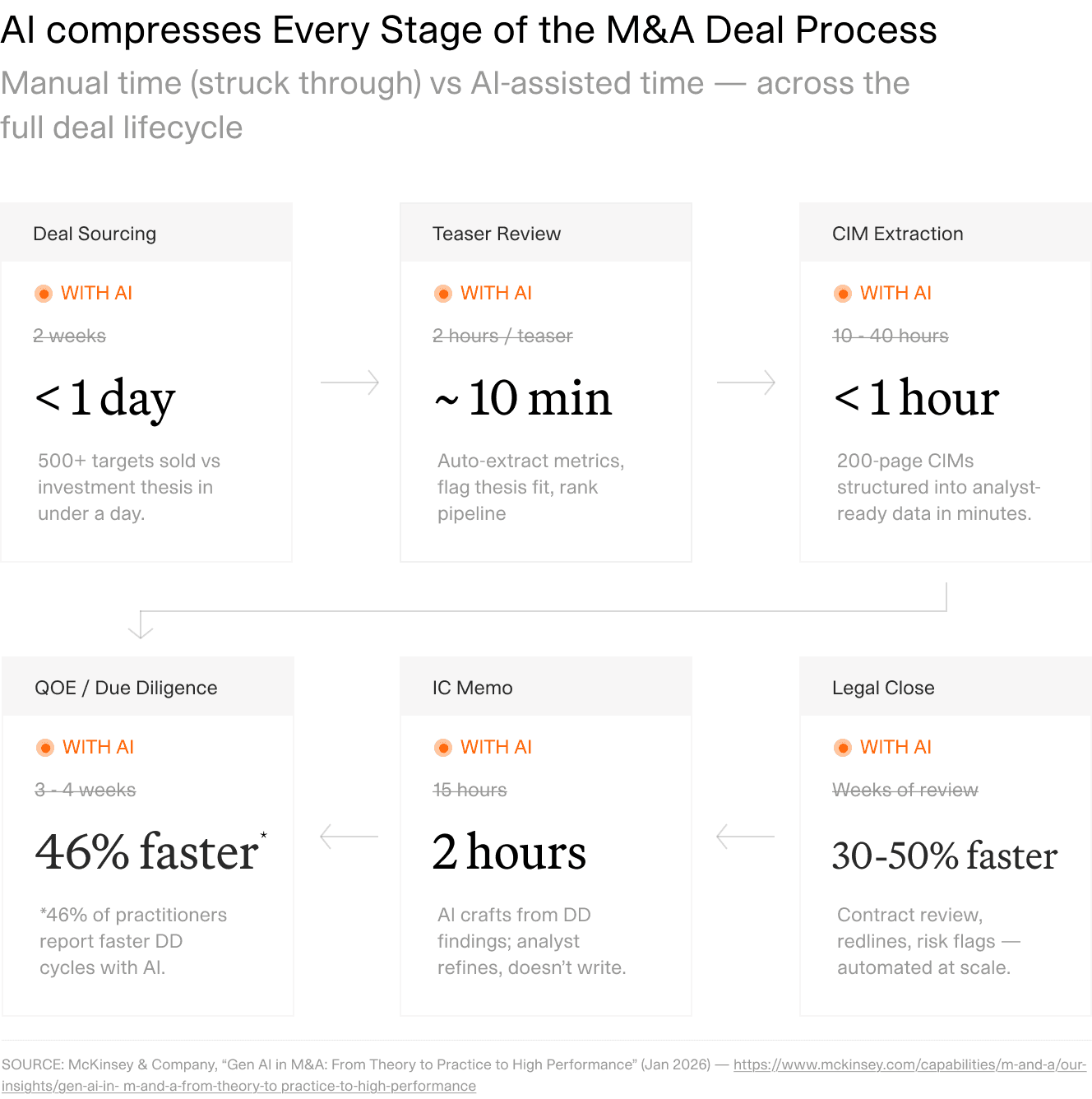

AI compresses every stage of the M&A deal process. CIM extraction, the manual data gathering that populates the deal scorecard, drops from 10–40 hours per document to under one hour.

The consistency benefit is as significant as the time saving. Every analyst, every sector, every deal type: the same six dimensions extracted against the same rubric. This changes the nature of IC review conversations. When all scorecard inputs are generated by the same extraction pipeline, the team focuses on evaluating the deal — not reconciling different interpretations of what the CIM said about customer concentration or revenue growth adjustments.

See how the AI Financial Due Diligence Agent populates deal scorecards from CIM documents, or explore the complete AI tools for data room analysis overview.

Five Common Deal Scorecard Mistakes

1. Using the same scorecard for every fund strategy. A buyout fund applying growth equity weights to a mature industrial business will systematically undervalue Financial Quality and overweight Market Position for companies that do not need TAM expansion to generate returns. Build thesis-specific weighting profiles and select the correct profile at the start of each deal assessment, before any scoring begins.

2. Too many dimensions with no weighting hierarchy. A scorecard with 10 or 12 dimensions at equal weights dilutes the evaluative signal. If every criterion matters equally, none of them matters decisively. Limit the scorecard to six to eight dimensions and accept that the weighting creates genuine trade-offs: a deal that scores high on Financial Quality but low on Exit Route Clarity should score differently from a deal with the inverse profile.

3. Scoring inconsistency across analysts. Without calibration anchors, two analysts scoring the same CIM on Financial Quality will regularly diverge by two to three points. This makes cross-deal comparison unreliable. For each dimension, define what a 3, a 6, and a 9 look like, using actual reference deals from the firm's own pipeline or existing portfolio. Run calibration sessions quarterly.

4. Confusing deal screening with portfolio monitoring. Applying post-acquisition KPIs to a deal at the screening stage produces scores that cannot be computed from a CIM. Maintain separate scorecards for separate purposes and make the distinction explicit when onboarding new deal team members.

5. Using the scorecard as a rubber stamp. The scorecard exists to determine which deals deserve analytical resources, not to justify a decision that has already been made informally. Apply gate criteria and the scorecard at the top of the funnel, before significant time is committed, and enforce the threshold consistently across all deal sources, including those referred by trusted relationships.

A consistent deal evaluation scorecard is one of the most impactful process changes a PE firm can make at the front end of its investment workflow. It replaces subjective, analyst-dependent assessment with a shared framework that every team member applies consistently, and that every IC member can interrogate directly against documented evidence.

The AI-automated version multiplies that advantage. From the first CIM read to the IC submission — every step of the pre-deal workflow runs on consistent, structured data. Preliminary scorecard fields are extracted by the same pipeline that feeds the diligence workstream and the IC memo, so the deal team spends its time on the analytical question (is this a good deal for our thesis?) rather than the operational one: did we all extract the same figures from the same document?

The result is a deal evaluation process that scales with deal volume without adding analyst headcount, and an IC discussion that starts from shared evidence rather than from reconciling different reads of the same CIM.

For a broader view of how AI is reshaping financial analysis workflows, see our guide to generative AI in finance. For the full AI due diligence workflow that sits downstream of the scorecard, from data room ingestion through to IC memo generation, the complete pipeline is covered in detail.

What is a deal scorecard in private equity?

A PE deal scorecard is a structured scoring framework that evaluates potential investment targets across a fixed set of weighted dimensions, typically four to eight. It converts the subjective assessment of a CIM or teaser into a comparable, repeatable score by assigning a numerical value (for example, 1 to 10) to each dimension, multiplying by the dimension's weight, and producing a total weighted aggregate. Every member of the deal team applies the same framework to every deal, making cross-deal comparison and IC preparation more consistent and efficient.

+

What are the key criteria for evaluating a PE deal?

The six criteria that appear consistently across PE practitioner frameworks are Financial Quality (normalised EBITDA, revenue growth, margins, cash conversion), Thesis Fit (mandate alignment, ownership structure, stage), Market Position (market share, competitive moat, concentration risk), Management Team Quality (experience, depth, exit alignment), Value Creation Potential (organic and inorganic growth levers, operational improvement), and Exit Route Clarity (realistic exit timeline, multiple exit paths, comparable transactions). Buyout firms weight Financial Quality and Thesis Fit most heavily. Growth equity firms weight Market Position and Thesis Fit. In both cases the weights should reflect the specific value creation thesis, not generic best practice.

+

How do you weight a PE deal scorecard?

Weights should reflect the primary value driver of your investment strategy. A buyout firm relying on existing cash flows to service acquisition debt typically assigns 30% to Financial Quality and 20% to Thesis Fit. A growth equity firm betting on market expansion typically assigns 25% each to Market Position and Thesis Fit. The most reliable approach is to identify the one or two dimensions that, if scored poorly, would cause you to pass on a deal regardless of all other scores, and assign those dimensions the highest weights. Calibrate the scale by anchoring each dimension with three reference deals representing scores of approximately 3, 6, and 9 out of 10.

+

What is the difference between a deal screening scorecard and a portfolio monitoring scorecard?

A deal screening scorecard evaluates new deal opportunities at the top of the funnel, before significant analytical resources are committed. It is applied to CIMs, teasers, and management presentations. A portfolio monitoring scorecard tracks KPI performance of existing portfolio companies after acquisition: EBITDA improvement year-on-year, working capital changes, headcount efficiency ratios. The two serve different purposes and must be maintained separately. Mixing criteria from both leads to evaluating new deals on post-acquisition metrics that cannot be measured from a CIM, or screening portfolio companies on deal-entry criteria that are no longer relevant to their current stage.

+

How many deals does a PE firm evaluate before investing in one?

AI agents can read CIM documents and extract the structured data required to populate each scorecard dimension automatically: normalised EBITDA and revenue figures from financial summaries, market share and competitive moat statements from the business overview, management team backgrounds from the leadership section, and concentration data from customer breakdown tables. This reduces the time to produce a preliminary scorecard from 2 to 3 analyst hours to under 10 minutes per CIM. Because the same extraction pipeline processes every document, every scorecard is structured identically, which makes cross-deal comparison and IC review faster and more reliable than when each analyst structures their notes independently.

+

How can AI help with deal evaluation in private equity?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.