10 min read

—

The build vs. buy question for LLM agents in private markets has a false assumption buried inside it: that those are the only two choices.

They aren't.

PE and VC firms evaluating AI for deal screening, CIM review, DDQ completion, and IC memo preparation face three distinct paths. Build custom agents from scratch. Buy purpose-built point solutions designed for specific workflows. Or configure a platform that handles the AI infrastructure while your team handles the domain logic. Each path suits different kinds of work, and the wrong match costs more in ongoing maintenance, operational constraints, and vendor lock-in than it saves in initial deployment speed.

The firms making this work in 2026 are not the ones that adopted AI earliest. They are the ones that matched the right path to each workflow in their fund.

This guide maps the LLM agent platform decision against seven common private markets workflows. It covers what each path actually costs beyond the initial build, which workflows belong on each path, and four criteria for evaluating a platform if the configure option is where you land.

In this article:

The three real paths for LLM agents in private markets: build, buy, and configure

When building a custom agent makes sense: the hidden ongoing costs that change the math

A decision matrix mapping seven PE and VC workflows to the right path

Four criteria for evaluating an LLM agent platform in a deal-sensitive, regulated environment

How V7 Go fits the configure path for private markets teams

AI for document processing

Configure AI agents for PE workflows without building from scratch

Get started today

Build vs. buy LLM agents in private markets: the three actual paths

Most build vs. buy frameworks assume two options because that is how software procurement worked before AI platforms existed. You either hired engineers to build something or you bought a vendor's product. For LLM agents in private markets, there is a third option that sits between those two, and it is where most PE and VC teams end up when the workflows in question are bespoke but the fund does not have a software engineering department.

Path 1: Build from scratch

Building a custom LLM agent means your engineers design the prompt architecture, integrate with foundation models via API, build the retrieval and document parsing layer, define the output schema, and maintain the entire stack as models evolve. It makes sense for one specific profile: genuinely proprietary analytical logic that creates competitive advantage, a stable process over a three-to-five-year horizon, and engineering resources committed to owning the system long term. Most private markets firms do not fit this profile. The engineering resources required to maintain a custom AI system are the same resources that could be building portfolio analytics, LP portal tooling, or fund administration infrastructure.

Path 2: Buy a purpose-built point solution

Purpose-built tools for private markets AI have proliferated. Several cover specific workflows, such as deal pipeline enrichment, financial statement spreading, and basic CIM summarization, with pre-configured templates and subscription pricing. Bain's annual Global Private Equity Report tracks where PE technology spend is concentrating across workflow categories, and is worth reading before narrowing a shortlist. Purpose-built tools work well when the workflow is sufficiently standardized that the vendor's template matches your process. They fail when your IC memo format reflects fifteen years of firm-specific investment thesis framing that no vendor has bothered to productize.

Path 3: Configure on an agent platform

A modular approach combines AI infrastructure provided by a platform with domain logic your team defines. You configure what the platform extracts from a CIM, how to structure DDQ answers, and what output format feeds your IC review process. The platform handles model access, document parsing, output formatting, and the tooling your team uses to review and iterate. Non-technical team members can adjust the logic without waiting on a vendor's product roadmap or modifying code.

Where AI tools for private equity sit across the build, configure, and buy spectrum. Bespoke workflows like IC memo preparation and LPA analysis consistently map to the configure path.

When building a custom LLM agent makes sense

Building is appropriate for one specific scenario: workflows with genuinely proprietary analytical logic that creates competitive advantage, that will remain stable over a multi-year horizon, and where your fund has engineering capacity to own the system. That describes fewer than 10 percent of the AI use cases PE and VC operations teams are actually running.

The leadership transition problem

The most common mistake smaller PE and VC funds make is building a custom agent around the capabilities of one engineer or analyst, and then discovering 18 months later that person has moved to a portfolio company or a competing fund. What remains is a system that works until something breaks. Nobody on the team knows how to fix it, and the documentation exists only in the departing employee's head.

This is the leadership transition problem. GP turnover at funds with fewer than 20 investment professionals is real enough that succession planning for technology systems deserves the same attention as succession planning for managing partners.

What custom solutions require, continuously

Custom solutions require continuous investment to stay current as foundation models evolve faster than most PE fund engineering teams can track. GPT-4 prompts do not transfer cleanly to newer model generations without testing and adjustment. Chunking strategies optimized for 8,000-token context windows need rethinking at 200,000 tokens. Retrieval architectures built for one document type need redesign when your fund adds a new instrument class. None of this is unsolvable. All of it costs engineering time that a configurable platform absorbs on your behalf.

A decision matrix for seven private markets workflows

The right path varies by workflow. DDQ completion has standardized structure that both point solutions and platforms handle well. IC memo preparation is fund-specific enough that off-the-shelf templates rarely work without significant modification. The following maps seven common workflows to the recommended path, based on configurability requirements, document variability, and expected rate of change in the underlying process. For workflows where the configure path fits, see how V7 Go covers CIM review and DDQ automation in practice.

DDQ completion: Buy a point solution for ILPA-standard questionnaire formats. Configure for fund-specific DDQ variations that go beyond standard templates. Building is overkill for this workflow.

CIM review and extraction: Configure. Point solutions use rigid templates that break on non-standard layouts. A configurable platform lets your team define the extraction fields rather than adapting to the vendor's structure.

IC memo preparation: Configure. Generic IC memo templates do not capture fund-specific thesis framing. A buyout fund with sector concentration has different analytical requirements than a growth-stage generalist, and no point solution accounts for this.

Legal due diligence (LPA, SPA): Configure. Waterfall structures and governance clauses in limited partnership agreements vary enough across fund structures and jurisdictions that clause extraction requires configurable logic rather than fixed templates.

Financial statement spreading: Buy a point solution. Several purpose-built tools cover this workflow well at reasonable cost. Configuring a platform for financial spreading is viable but unnecessary when strong point solutions exist.

LP reporting: Configure for funds with non-standard LPA reporting requirements. Buy a point solution for standard LP update formats. Build only if your fund has a data science team and genuinely proprietary portfolio analytics methodology.

Deal screening: Build if your screening methodology is proprietary and differentiating. Configure for hybrid criteria mixing public data with fund-specific thesis filters. Buy for generic deal attribute matching against standard databases.

Four criteria for evaluating an LLM agent platform for private markets

Enough platforms now claim to serve private markets that selection criteria matter as much as the shortlist. For PE and VC firms specifically, four factors should drive platform evaluation above the usual feature comparison.

Data residency and no training on your deal information

Ask every vendor directly: does your platform use customer data to improve foundation models or fine-tune inference? What are the data residency options? Most off-the-shelf tools cannot answer this precisely at the pricing tier that emerging managers can afford. For a firm in a fiduciary relationship with LPs, operating under investment management agreements that govern data handling, this is not a secondary concern. It is the first question. Platforms routing deal documents through shared inference infrastructure with ambiguous contractual data handling are not appropriate for non-public, material information.

Configurability vs. template lock-in

Configuring your own extraction logic is fundamentally different from adapting your process to a vendor's template. Purpose-built solutions optimize for common cases. An IC memo format for a growth-stage generalist fund uses different analytical framing than one for a buyout fund with a sector-specialist thesis. A platform where your team defines the extraction fields, the output structure, and the review workflow will not require your investment professionals to change how they think about the analysis. A template-based tool will.

Source traceability for investment committee documentation

Every finding that flows into an IC memo, a due diligence report, or an LP update needs to trace to a source document and a specific page or section. Investment committee members ask where this comes from during deal review. LPs ask equivalent questions during fund audits and regulatory inquiries. An AI agent that produces conclusions without linking them to evidence creates a documentation gap that becomes visible at the worst possible moment. Traceability is infrastructure, not a differentiating feature.

Speed of iteration after first deployment

First deployment is the easy part. The real test is how quickly your team adjusts the agent when conditions change: a GP revises how they want CIMs analyzed, a new jurisdiction introduces different waterfall structures, or the fund adds an instrument class to its mandate. Platforms where non-technical team members can modify the configuration matter more for long-term operational fit than platforms optimized for initial engineering speed.

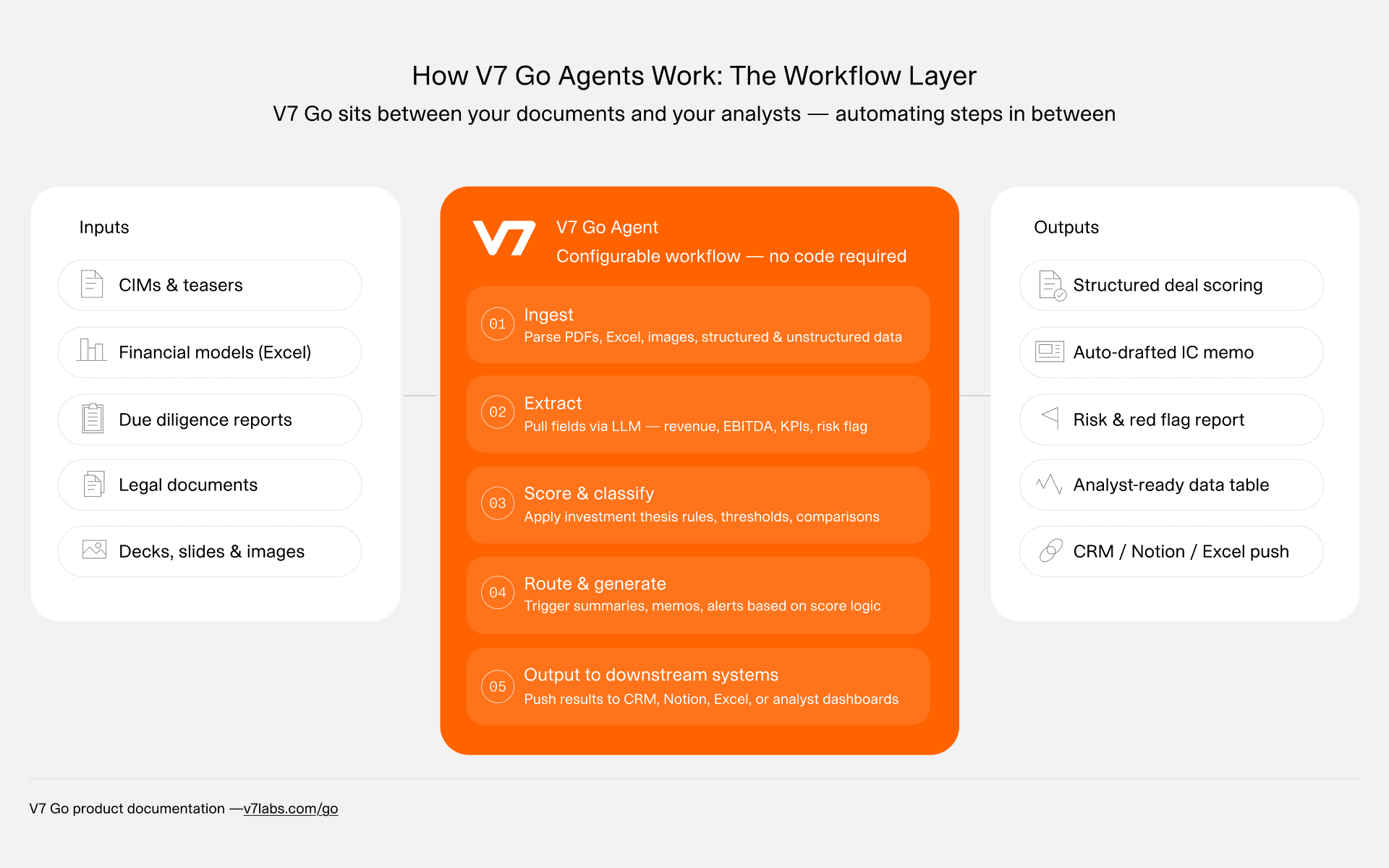

V7 Go's finance deployment benchmarks show CIM document processing at 35 structured data points per deal, compared to 77 manual steps in the equivalent analyst workflow. The reduction does not come from doing less analysis. It comes from extracting the same information more consistently, against a defined schema, with every finding traceable to its source. The workflow demonstration below covers both CIM extraction and DDQ completion:

V7 Go in a live finance deployment: CIM extraction across 35 data points vs. 77 in manual review, and DDQ completion benchmarked across 41 and 63 questions respectively.

How V7 Go fits private markets on the configure path

V7 Go is used by PE and VC teams specifically because it occupies the configure position: your team defines the extraction logic, V7 Go provides the AI infrastructure, and the output flows to your review process rather than into a vendor's fixed output format. Transacted's independent PE software directory lists V7 Go as suited for highly bespoke processes, which maps to the configure path as described in this article.

V7 Go's architecture: configurable extraction logic, Knowledge Hubs for persistent deal context, and AI Citations linking every extracted finding to its exact location in the source document.

The workflows PE and VC teams configure on V7 Go include:

CIM review: Configurable extraction across 35-plus data points per deal, with output structured for your IC review format. The CIM review automation handles deal documents at scale without requiring every CIM to match a vendor's expected layout.

DDQ completion: Structured extraction against fund-specific questionnaire formats. The DDQ completion use case covers both ILPA standard formats and LP-specific variations that point solutions cannot accommodate.

IC memo preparation: The investment memo generation automation pulls structured data from dataroom documents, organizes it against your fund's memo format, and links every section to its source.

LPA analysis: The LPA analysis agent extracts waterfall provisions, governance clauses, and fund-specific reporting requirements from limited partnership agreements, including documents with non-standard structures.

Two capabilities matter specifically for private markets context. AI Citations (Visual Grounding) links every extracted claim to the exact location in the source document, the page, the clause, and the specific sentence. This is the traceability that investment committee documentation requires. Knowledge Hubs store deal context persistently, so the analytical work done on a target company does not reset when a deal team member changes. For funds where analyst turnover is a recurring operational risk, this functions as institutional memory that does not leave when people do.

For a detailed view of how AI due diligence works across document types in a private markets context, including which workflows PE teams configure first, see the linked guide.

Technology decisions in private markets need a review cadence

The build vs. buy decision for LLM agents is not a one-time exercise. Foundation models improve on a schedule that does not align with fund cycles. The right path for DDQ completion in 2024 looks different in 2026 as models handle longer documents with greater accuracy and new purpose-built tools reach quality thresholds that make the configure path unnecessary for specific workflows.

A regular technology review, tied to fund launches, operational reviews, and hiring decisions rather than scheduled as a ritual, keeps the decision current. For teams on the configure path, this review is structurally easier. The platform absorbs model improvements automatically, and you iterate on configuration rather than rebuilding the system. For teams that built custom agents, a technology review often reveals that the maintenance cost now exceeds the original rationale for building.

The practical starting point: take the workflow that consumes the most analyst time and has the most predictable structure, run it on a configurable platform with a sample of real deal documents from the past 12 months, and compare the output quality against your current manual process before committing at scale. CIM review and DDQ completion are common first workflows because the document formats are relatively consistent and the extraction requirements are specific enough to configure clearly.

If you are evaluating V7 Go for private markets use cases, the AI due diligence agent is a reasonable starting point for understanding how the configure path works in practice.

How long does it take to build a custom LLM agent for private equity workflows?

Building a functional custom LLM agent for a single PE workflow typically takes three to six months from scoping to deployment, assuming a team with relevant engineering experience. That timeline covers prompt architecture design, document parsing infrastructure, retrieval and chunking implementation, output schema definition, evaluation and testing against real deal documents, and initial deployment. It does not cover ongoing maintenance. The less obvious cost is what happens after deployment. Foundation models release major versions every six to twelve months. Each version requires testing against your existing prompts and often requires prompt reengineering to maintain output quality. Retrieval architectures optimized for shorter context windows need redesign as models extend to longer ones. For a fund without a dedicated AI engineering team, this ongoing maintenance burden is often the reason teams that initially built eventually migrate to a configurable platform, not because the custom agent did not work, but because sustaining it costs more than the alternative.

+

What does it cost to configure an LLM agent platform for private markets compared to building?

Configurable platforms for private markets typically price on a per-seat or usage basis, with implementation costs ranging from minimal for self-serve setup to a few weeks of implementation support for complex multi-workflow deployments. The total cost over a 24-month period for a team of five to ten users is generally lower than the engineering cost of building and maintaining an equivalent custom solution, particularly when you account for the time cost of prompt maintenance across model version releases. Building a custom agent requires either in-house engineering resources or contractor costs. A senior engineer with LLM experience costs roughly 150,000 to 250,000 USD annually in fully loaded compensation. A minimal custom agent build might require three to six months of that engineer's time, plus ongoing maintenance at ten to twenty percent of their capacity. At those numbers, a configurable platform covering the same workflows is cost-competitive from month six onward, and carries no single-engineer dependency risk.

+

What happens when the engineer who built a custom AI system leaves the fund?

This is the leadership transition problem, and it is the most underweighted risk in custom AI builds at smaller private markets firms. When the engineer or analyst who built and maintained the system moves to a portfolio company, a competing fund, or another role, what remains is a working system with no owner. The system functions until something breaks: a model API change, a document format the original code did not anticipate, a dependency that needs updating. At that point, the fund must either hire replacement engineering resources, contract an AI developer to audit and rebuild the system, or migrate to a platform. Configurable platforms avoid this problem because the system's logic lives in configuration that non-technical team members can read and modify. When a senior analyst who configured the DDQ completion workflow leaves, another analyst can review the configuration, understand what it does, and adjust it. The institutional knowledge stays in the system rather than leaving with the person.

+

What AI tools are PE and VC firms currently using for deal review and due diligence?

The current private markets AI landscape includes purpose-built point solutions for specific workflows, such as financial statement spreading, deal pipeline enrichment, and basic CIM summarization, alongside configurable agent platforms for bespoke processes. Point solutions from several vendors cover specific document types with pre-built templates. Configurable platforms including V7 Go serve funds with workflows that do not fit standard templates: IC memo preparation with fund-specific framing, LPA clause analysis, or DDQ formats with non-standard LP requirements. General-purpose AI tools such as ChatGPT, Claude, and Gemini are widely used for ad hoc research tasks but are not appropriate for systematic deal review at the workflow level. They lack structured output formatting, source traceability, and the access controls required for working with non-public deal information at scale. The distinction is between using AI for a single analyst's research versus deploying it as infrastructure for a repeatable fund operations workflow.

+

Should a smaller venture capital fund build or configure AI agents for deal operations?

The core question to ask every AI vendor: does your platform use customer data to train or fine-tune models? The answer should be a clear no, backed by contractual language in the data processing agreement. Follow-up questions: where is data processed, and in which cloud regions? Does deal document content transit shared inference infrastructure? What happens to document data after a query completes? For funds operating under investment management agreements that govern data handling, the contractual language matters as much as the technical architecture. Many off-the-shelf AI tools include language in their terms of service permitting use of customer interactions for model improvement. This is usually configurable at enterprise pricing tiers but not at lower ones. For funds handling non-public, material information, which describes most private markets deal documents, confirm data handling terms in writing before deploying any AI tool on live deal documents. The ILPA provides guidance on evaluating third-party technology providers in a limited partnership context at ilpa.org; their data governance frameworks are a useful starting reference for funds formalizing their AI vendor evaluation process.

+

How should PE and VC firms evaluate data security when deploying LLM agents on deal documents?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.