24 min read

—

A guide to the best reinsurance software platforms for automating treaty management, claims processing, and risk analytics. We evaluate modern AI challengers and legacy incumbents, and show how AI agents are solving the data extraction gap.

If you ask a reinsurance operations manager where their treaty data lives, they might point to an expensive enterprise platform. Guidewire, SAP, or Oracle. But if you ask the analyst who actually processes the quarterly bordereaux at 9:00 PM on a Friday, they will point to a sprawling Excel workbook with 47 tabs, half of which are named "Final_v3_ACTUAL_USE_THIS."

This is the reality of reinsurance operations: despite $1.54 billion spent annually on reinsurance software, the industry's backbone remains a fragile mesh of manual data entry, scanned PDFs, and reconciliation spreadsheets. The global reinsurance software market is projected to reach $3.62 billion by 2033, growing at 9.8% annually, yet the core operational bottleneck remains largely unsolved. Getting data out of documents and into systems still requires humans as the bridge.

The problem is not a lack of software. The problem is that most reinsurance platforms are designed as systems of record, not systems of ingestion. They assume clean, structured data arrives from upstream. In reality, treaty agreements come as scanned images, adjustment notices are handwritten, and bordereaux arrive as PDFs with inconsistent formatting across 15 different cedents.

In this article:

The Core Challenge: Why reinsurance software fails at the data ingestion layer and where manual processes break down.

Platform Reviews: Deep dives into 10 leading reinsurance software platforms, from modern AI challengers to legacy incumbents.

Solving the Data Gap: How AI agents automate the extraction of treaty terms, claims data, and bordereaux reconciliation.

Implementation Guides: What to expect when migrating from legacy systems to a modern, AI-enabled stack.

AI for document processing

Automate treaty and claims document processing now

Get started today

The Core Challenge: Why Reinsurance Software Fails

To select the right software, you must first understand why so many implementations fail. The core issue is a fundamental misunderstanding of what reinsurance software is designed to do versus what the day-to-day workflow of a reinsurance operation actually requires.

The System of Record vs. System of Engagement

Most traditional reinsurance platforms are designed as systems of record. They are databases for storing treaty structures, premium calculations, and claims reserves. Their primary job is to be an immutable ledger of transactions.

However, the daily workflow of a reinsurance analyst is fluid and document-heavy. They deal with messy, incoming data streams: a cedent restating their loss ratio from Q2, a treaty amendment that splits coverage between two different layers, or a bordereaux file that arrives with inconsistent column headers across 12 different Excel formats.

The software assumes data arrives clean and structured. The reality is that 80% of the work happens before data enters the system. Manual extraction, validation, and reconciliation of documents consume analyst time before a single field gets entered into Guidewire or SAP.

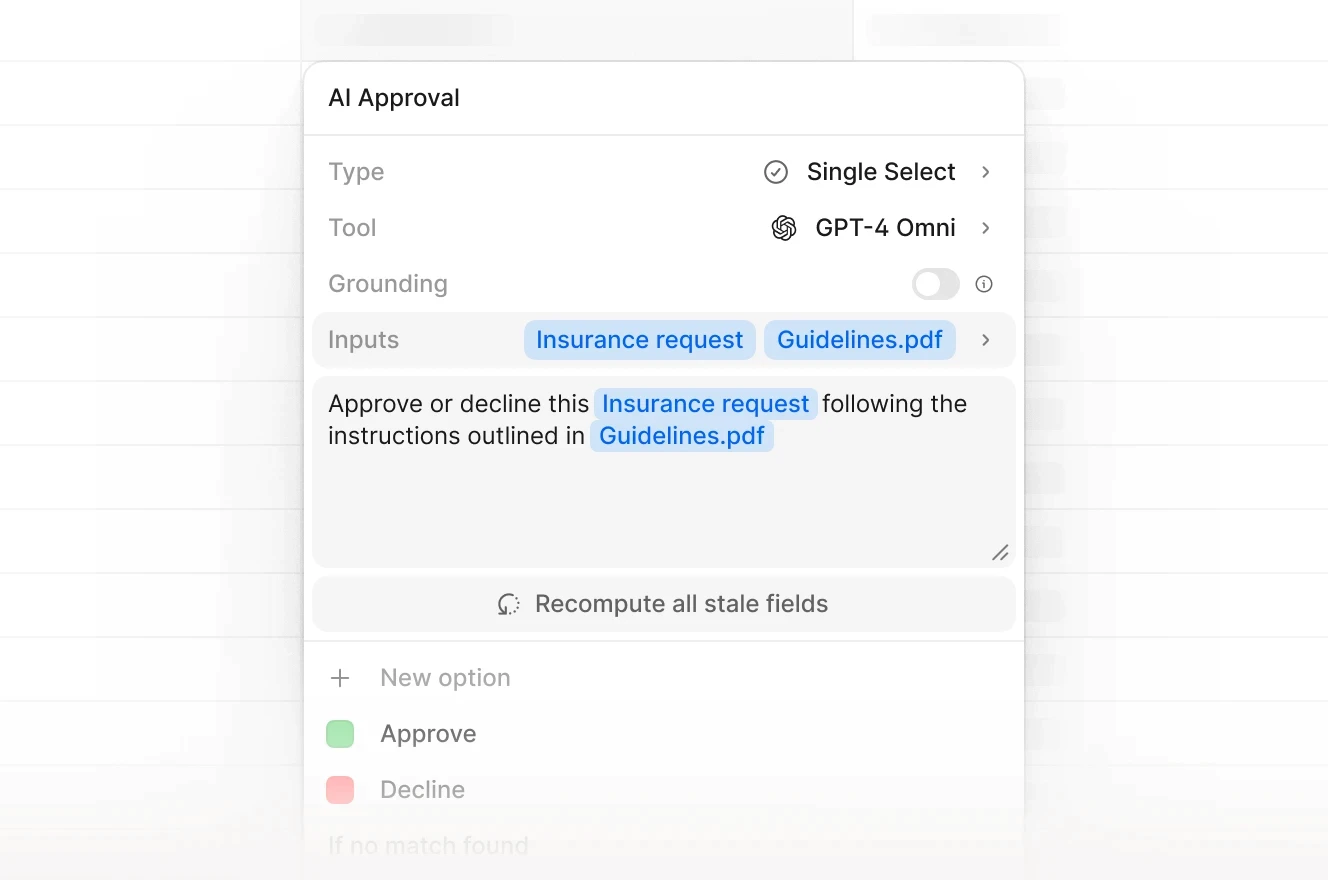

AI approval workflow for insurance requests. The example shows automated underwriting decisions with full audit trails.

The Monday Morning Reality

Here is what a typical reinsurance workflow looks like on Monday morning:

Documents and Artifacts: Scanned treaty agreements (often 200+ pages), handwritten adjustment notices from Lloyd's syndicates, legacy spreadsheets with re-keyed premium data, quarterly regulatory compliance PDFs that need to be parsed for specific clauses.

The Hack: In the absence of modern automation, teams resort to labor-intensive methods. They use outsourced BPO teams in India for data entry, perform VLOOKUPs across dozens of Excel sheets to reconcile bordereaux against treaty terms, and manually rekey data into core ERP systems like SAP. One reinsurance manager described their process as "a human OCR layer between the document and the database."

The Bottleneck: The critical issue is the reconciliation process. After month-end closures, teams spend 3-5 days reconciling premium bordereaux against treaty terms, cross-checking claims reserves against policy limits, and manually flagging discrepancies. Legal review adds another bottleneck. Treaty amendments require manual redlining, clause-by-clause comparison, and approval workflows that extend for weeks.

According to a Decerto analysis, adopting reinsurance automation processes can lead to an average 20% reduction in operational costs by reducing manual interventions. But most platforms do not automate the ingestion layer. They only automate what happens after data is already in the system.

The Modular Stack Approach

Leading reinsurance operations in 2025 are moving away from the all-in-one monoliths. Instead, they are building composable tech stacks that separate concerns:

The Intelligence Layer (Ingestion): Tools like V7 Go that reside at the top of the funnel. They read scanned treaty PDFs, extract data using intelligent document processing, visually verify it against source documents, and structure it into a clean format.

The Accounting Layer (Ledger): Traditional reinsurance platforms like Guidewire or SAP that receive the clean data and handle the heavy accounting logic. Premium calculations, reserve modeling, regulatory reporting.

The Visualization Layer (BI): Tools like Tableau, PowerBI, or specialized dashboards that present the final data to stakeholders. Underwriters, actuaries, and C-suite executives.

This modular approach reduces vendor lock-in and allows you to swap out components as technology improves. The critical glue holding this stack together is clean, structured data. By automating the ingestion layer, you ensure that every downstream system is fed with accurate, timely information.

The following video shows how an agent library provides pre-built workflows for different document types, from invoice processing to batch document analysis.

V7 Go's agent library showing pre-built workflows for invoice processing, OCR extraction, and batch document analysis.

Deep Dive: Comparing Reinsurance Software Platforms

To truly understand which software fits your operation, you have to look at how they solve the data ingestion problem. This is where the most operational friction occurs. The following breakdown covers 10 leading platforms in two categories: modern AI challengers and legacy incumbents.

Modern AI Challengers

These platforms are built with AI-first architectures, designed to automate the extraction and processing of unstructured reinsurance documents.

1. V7 Go

Website: https://www.v7labs.com/

Core Positioning: Best for leveraging advanced AI (OCR, LLMs, and multimodal capabilities) to automate extraction from complex, unstructured reinsurance documents.

Top 3 Features:

Advanced OCR for Scanned Treaty PDFs: V7 Go uses state-of-the-art optical character recognition to extract text from scanned treaty agreements, even when the documents are poor-quality images or handwritten notes. The system handles the 200-page treaty PDFs that arrive as scanned images from Lloyd's syndicates.

Agent Workflows: Pre-built agents like the Claims Intake Agent and Treaty Extraction Agent automate the parsing of bordereaux files, treaty amendments, and adjustment notices. Each agent follows a defined workflow: ingest document, extract fields, validate against schema, output structured data.

Integration of LLMs for Contextual Data Extraction: V7 Go uses large language models to understand the context of treaty clauses. The system flags non-standard terms and extracts key fields like coverage limits, retention amounts, and reinstatement provisions. Visual grounding shows exactly where each data point was found in the source document.

Pricing Model: Custom/Enterprise

What Users Say: Users praise high extraction accuracy and multi-agent workflows. One user noted that V7 Go reduced their treaty data entry time from 3 days to 4 hours. The learning curve is steeper for non-technical users, and pricing reflects enterprise positioning.

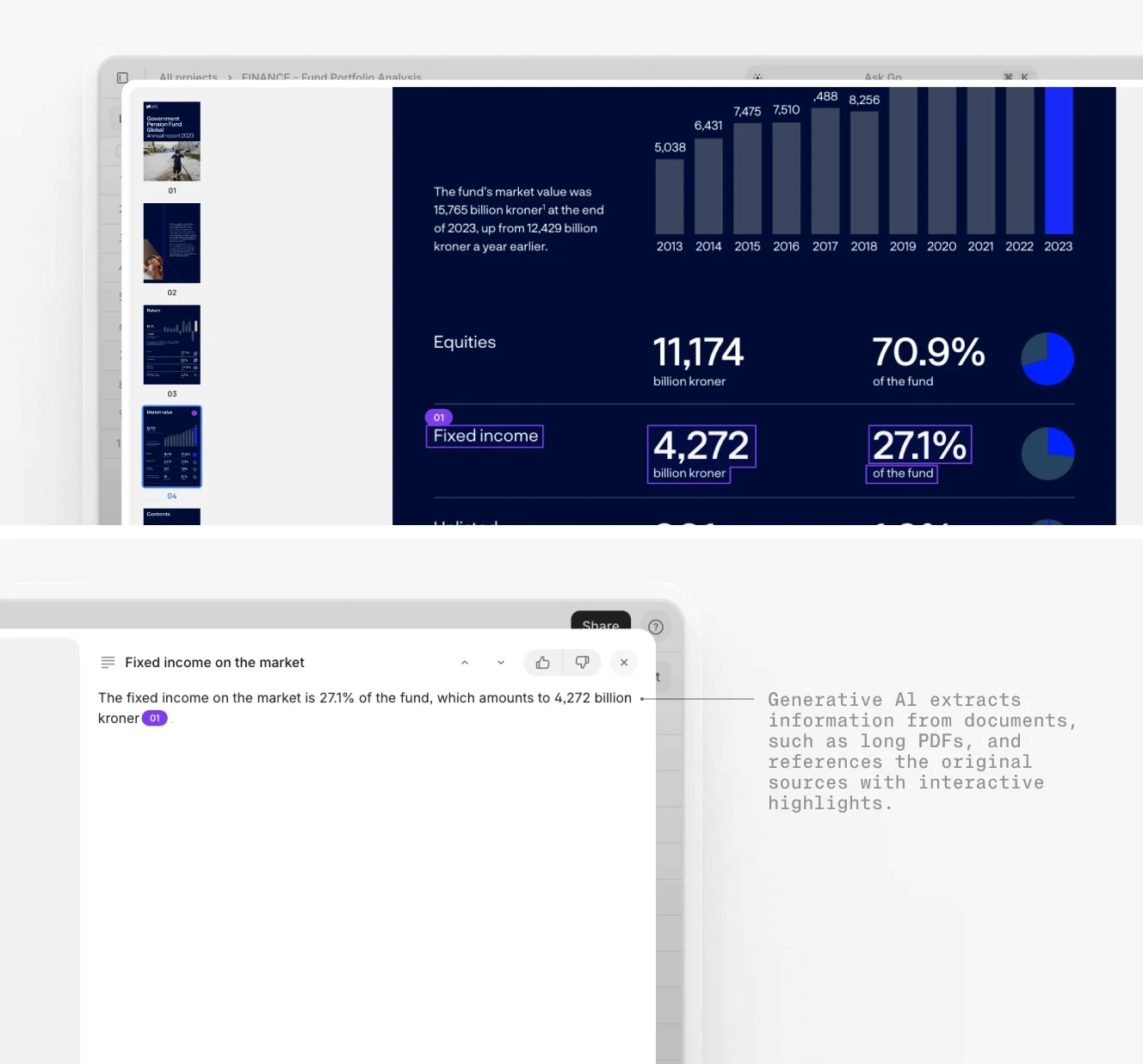

AI extracts fund data and marks the exact source location. Citations trace back to specific document pages for audit trails.

2. CyberCube Analytics

Website: https://www.cybercube.com/

Core Positioning: Best for cyber risk analytics and predictive modeling within the reinsurance space, particularly for underwriting cyber exposure.

Top 3 Features:

Cyber Risk Quantification: CyberCube specializes in cyber risk quantification, providing detailed exposure analysis for reinsurance portfolios. The platform models potential cyber events and their financial impact across a book of business.

Predictive Analytics: Uses machine learning to forecast loss scenarios and stress-test treaty structures against cyber-specific catastrophic events.

Data Visualization Dashboards: Interactive dashboards that allow underwriters to explore risk concentrations and scenario analyses. Particularly useful for understanding cyber aggregation risk.

Pricing Model: Custom pricing

What Users Say: Users appreciate the depth of risk insights, particularly for cyber reinsurance. Integration with legacy systems can be complex, and the platform is specialized for cyber risk rather than general reinsurance operations.

3. FIS Reinsurance Manager

Website: https://www.fisglobal.com/

Core Positioning: Source-independent reinsurance system that automates reinsurance programs regardless of your policy and claims administration system.

Top 3 Features:

Source-Independent Architecture: FIS Reinsurance Manager operates independently of your policy administration system. It ingests data from multiple upstream sources, which solves a common pain point for organizations running heterogeneous tech stacks.

Automated Cession Processing: Handles automatic cession calculations for proportional and non-proportional treaties. The system processes facultative certificates, obligatory treaties, and retrocession arrangements in a single workflow.

Audit Trail and Compliance: Every transaction is logged with full traceability. The platform generates regulatory reports and maintains the documentation required for financial audits and Solvency II compliance.

Pricing Model: Custom/Enterprise

What Users Say: Users value the platform's independence from policy admin systems. The implementation requires dedicated IT resources, and customization cycles can extend beyond initial estimates.

4. Verisk Touchstone Re

Website: https://www.verisk.com/

Core Positioning: Catastrophe modeling analytics for reinsurance, helping underwriters quantify and manage the loss potential of reinsurance contracts and portfolios.

Top 3 Features:

Complex Reinsurance Structure Modeling: Models potential losses for common and unique reinsurance structures. The system calculates AAL, EP curves, TVaR, and other standard metrics from multiple loss perspectives.

Integration with Catastrophe Models: Access to Verisk's suite of over 110 risk models. Underwriters can assess how their portfolio responds to diversified views of risk, including third-party and in-house models.

Real-Time Portfolio Management: Export maps, charts, and tables into customized reports. The platform integrates analytics into back-end rollup and reporting systems for real-time portfolio management.

Pricing Model: Custom/Enterprise

What Users Say: Verisk's catastrophe modeling is considered the industry standard for property catastrophe reinsurance. The platform excels at risk quantification but is specialized for catastrophe modeling rather than operational treaty administration.

5. Sapiens ReinsuranceMaster

Website: https://sapiens.com/

Core Positioning: Full operational control for large, multinational reinsurance programs with automated calculations and compliance management.

Top 3 Features:

Automated Calculations for Complex Contracts: Sapiens claims its platform can reduce processing times by up to 40%, enabling faster claim reconciliation and improved audit trails. The system handles sliding scale commissions, profit commissions, and loss corridor calculations automatically.

Multi-Currency and Multi-Line Support: Processes proportional and non-proportional reinsurance across all lines of business. The platform manages the complexity of quota share, surplus, excess of loss, and stop loss arrangements.

Third-Party Integrations: Connects with existing policy administration systems, claims platforms, and financial reporting tools via APIs. The platform supports data exchange with cedents in multiple formats.

Pricing Model: Custom/Enterprise

What Users Say: Users praise the breadth of functionality and deep integration capabilities. The platform's complexity requires dedicated training, and implementation timelines often extend to 6-12 months.

6. Appian Reinsurance Automation

Website: https://appian.com/

Core Positioning: Low-code platform for workflow automation that accelerates process modernization in reinsurance operations.

Top 3 Features:

Low-Code Development Environment: Allows business users to build custom workflows without extensive coding. Reinsurance teams can create bordereaux processing flows, approval chains, and exception handling without waiting for IT resources.

Bordereaux Automation: Appian's low-code reinsurance automation reportedly cuts manual errors by about 30% in claim processing workflows. The platform automates bordereau intake, validation, and follow-up actions by orchestrating AI, IDP, RPA, and system APIs.

Process Orchestration: Manages multi-step processes like treaty renewals, bordereaux reconciliation, and claims settlements. The system connects to cedent data sources automatically and reduces manual data transfer.

Pricing Model: Custom/Enterprise

What Users Say: Users value the flexibility and rapid deployment for creating tailored solutions. The platform requires significant customization effort, and users report a noticeable learning curve for building complex workflows.

Legacy Incumbents

These platforms are mature, enterprise-grade systems with broad adoption across the reinsurance industry. They excel at accounting and regulatory compliance but often struggle with data ingestion.

7. Guidewire Reinsurance Management

Website: https://www.guidewire.com/

Core Positioning: Enterprise-grade reinsurance management with broad industry adoption and extensive integration capabilities.

Top 3 Features:

Policy and Claims Administration: Guidewire provides end-to-end policy administration, from treaty setup to claims settlement. The platform manages the full lifecycle of a reinsurance agreement, including reinstatements and commutations.

Premium Calculations and Risk Analytics: Handles complex premium calculations, reinstatement provisions, and exposure modeling. The system calculates ceded premiums across proportional and non-proportional structures.

Extensive Integration Capabilities: Connects with existing policy administration systems, financial reporting tools, and third-party data providers. Guidewire's ecosystem includes pre-built integrations with major cedent systems.

Pricing Model: Custom/Enterprise

What Users Say: Users trust Guidewire for reliability and broad integration. Criticisms focus on high costs and time-consuming customizations. One user noted: "Guidewire offers strong functionality, but its heavy implementation and inflexible customization leave many of us stuck with workarounds."

8. SAP for Insurance

Website: https://www.sap.com/

Core Positioning: Best for companies needing deep ERP integration and end-to-end processing capabilities across the reinsurance lifecycle.

Top 3 Features:

Full Lifecycle Reinsurance Processing: SAP handles everything from treaty negotiation to claims settlement and financial reporting. The platform's strength is in connecting reinsurance operations to the broader financial ledger.

Advanced Analytics: Provides deep insights into portfolio performance, loss ratios, and reserve adequacy. The analytics layer connects directly to SAP's business intelligence tools.

ERP Integration: Integrates with SAP's broader ERP ecosystem, enabling financial consolidation across reinsurance and corporate accounting. This is particularly valuable for organizations already running SAP for general ledger functions.

Pricing Model: Custom/Enterprise

What Users Say: Users appreciate strong integration with existing ERP systems. The platform is noted for complex implementations and high total cost of ownership, particularly for organizations that are not already SAP shops.

9. Oracle Insurance Cloud

Website: https://www.oracle.com/

Core Positioning: Best for scalable cloud-based deployments and modern analytics in reinsurance operations.

Top 3 Features:

Cloud-Native Architecture: Oracle's cloud platform provides scalability and flexibility for growing reinsurance operations. The infrastructure handles peak processing loads during quarter-end reconciliation without requiring additional hardware.

Operational Dashboards: Real-time visibility into treaty performance, claims reserves, and premium bordereaux. Dashboards update automatically as data flows through the system.

Data Analytics: Integrates with Oracle's broader analytics suite, enabling advanced reporting and predictive modeling. The platform supports actuarial analysis and reserve forecasting.

Pricing Model: Custom/Enterprise

What Users Say: Users applaud scalability and modern cloud features. Challenges include implementation complexity and ongoing maintenance requirements. Oracle implementations typically require dedicated Oracle expertise on staff.

10. DXC Assure Reinsurance

Website: https://dxc.com/

Core Positioning: Integrated cloud-enabled solution for end-to-end reinsurance management across life, health, and P&C lines from both assumed and ceded perspectives.

Top 3 Features:

Full Reinsurance Lifecycle Support: DXC Assure Reinsurance manages all aspects of assignments and retrocessions, from technical processing to administrative and regulatory reporting. The platform is a modernized version of DXC SICS, a long-established reinsurance system.

Multi-Line Coverage: Supports all lines of business including life, health, and general/property and casualty. The platform handles both assumed reinsurance (as a reinsurer) and ceded reinsurance (as a cedent).

API Framework and Partner Ecosystem: Integrates existing technologies through a full API framework. DXC provides a gateway to a partner ecosystem including insurtech innovation and third-party data providers.

Pricing Model: Custom/Enterprise

What Users Say: Swiss Re uses DXC's software and services, praising the ability to improve business processes. Users note that implementation requires commitment to the DXC ecosystem, and transitions from legacy DXC SICS installations can be complex.

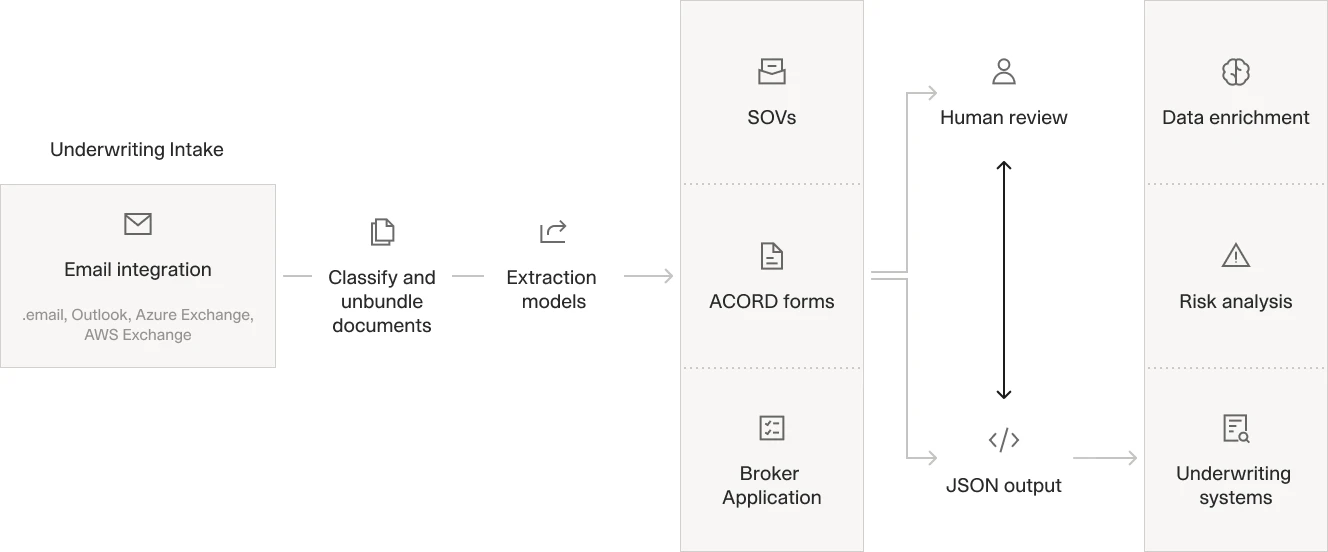

AI underwriting workflow: email classification, data extraction, and structured JSON output for downstream systems.

Solving the Data Gap: How AI Agents Automate Reinsurance Workflows

The core challenge in reinsurance operations is not the accounting logic. The accounting logic is solved. The challenge is the data ingestion layer. Most platforms assume data arrives clean and structured. In reality, treaty agreements come as scanned images, bordereaux arrive as PDFs with inconsistent formatting, and adjustment notices are handwritten.

This is where AI agents provide the most value. By automating the extraction, validation, and reconciliation of unstructured documents, AI agents eliminate the manual bottleneck that slows down every downstream process.

The Treaty Data Extraction Agent

A typical treaty agreement is 200+ pages of dense legal text, with critical terms buried in nested clauses. Extracting key fields requires reading every page and cross-referencing terms across multiple sections. Coverage limits might appear in Article 3.2, retention amounts in Schedule A, and reinstatement provisions in an amendment appended six months later.

An AI agent built with V7 Go automates this process. Here is the workflow:

Step 1: Document Ingestion. The agent receives a scanned treaty PDF via email or API integration. The system accepts documents from SFTP drops, email attachments, or direct uploads. Format variations across cedents are handled automatically.

Step 2: OCR and Text Extraction. V7 Go's advanced OCR engine extracts text from the scanned document, even when the image quality is poor or the text is handwritten. The system processes multi-column layouts, tables, and embedded schedules that break standard OCR tools.

Step 3: Contextual Field Extraction. The agent uses RAG (Retrieval-Augmented Generation) to understand the context of each clause. It identifies coverage limits by looking for phrases like "limit of liability" or "maximum indemnity" and extracts the associated dollar amounts. For ambiguous terms, the agent references the Knowledge Hub containing your organization's treaty templates and historical agreements.

Step 4: Visual Grounding. For every extracted field, the agent marks the exact location in the source document where the data was found. This provides full traceability and allows human reviewers to verify the extraction. Visual grounding turns a black-box extraction into an auditable process.

Step 5: Structured Output. The agent outputs a structured JSON file with all key treaty terms, ready to be imported into the reinsurance platform. Fields include treaty number, effective dates, coverage type, limits, retention, commission rates, and reinstatement provisions.

This workflow reduces treaty data entry time from 3 days to 4 hours. More importantly, it eliminates the risk of manual transcription errors. Every field is traceable back to the source document.

The following video shows a CIM due diligence workflow using Cases. The same approach applies to treaty extraction: documents enter, fields are extracted, and human reviewers verify the output.

CIM due diligence workflow showing Cases interface with extracted fields and entity analysis. The same pattern applies to treaty data extraction.

The Bordereaux Reconciliation Agent

Bordereaux files are the lifeblood of reinsurance accounting. They contain detailed premium and claims data from cedents, broken down by policy, coverage type, and geographic region. The problem is that every cedent sends bordereaux in a different format. Some use Excel, some use CSV, some use PDF tables with inconsistent column headers.

Reconciling bordereaux against treaty terms is a manual, error-prone process. Analysts spend hours cross-checking premium amounts, validating coverage limits, and flagging discrepancies. A single bordereaux file might contain 5,000 rows. Multiply by 30 cedents, and quarter-end becomes a reconciliation marathon.

An AI agent automates this process:

Step 1: File Ingestion. The agent receives bordereaux files via email or SFTP. The system monitors a designated folder and processes new files automatically. No manual download and upload required.

Step 2: Format Normalization. The agent uses AI data extraction to parse the file, regardless of format. It identifies column headers, maps them to standard fields (policy number, premium amount, coverage type), and normalizes the data into a consistent structure. A "Written Premium" column in one file becomes the same field as "Gross Premium" in another.

Step 3: Treaty Term Validation. The agent cross-references the bordereaux data against the treaty terms stored in the Knowledge Hub. It checks that premium amounts are within the agreed limits, that coverage types match the treaty scope, and that geographic regions are covered. For quota share treaties, the agent validates that the ceded percentage is applied correctly.

Step 4: Discrepancy Flagging. If the agent detects a discrepancy, it flags the issue and provides a detailed explanation. The flag includes the exact clause in the treaty that was violated and the specific row in the bordereaux that triggered the exception. Common flags include premium exceeding treaty limits, coverage outside treaty territory, and incorrect cession percentages.

Step 5: Automated Reconciliation Report. The agent generates a reconciliation report showing all validated records and flagged discrepancies. The report is formatted for human review and approval, with one-click navigation to source documents.

This workflow reduces bordereaux reconciliation time from 5 days to 1 day. It also improves accuracy. Every discrepancy is flagged with full traceability back to the source document and treaty clause.

The Claims Intake Agent

Claims processing in reinsurance is complex. A single claim may involve multiple layers of coverage, multiple cedents, and multiple treaty agreements. Extracting claims data from loss runs, FNOL (First Notice of Loss) reports, and adjustment notices requires reading dozens of documents and cross-referencing terms across multiple treaties.

An AI agent automates this process:

Step 1: Document Ingestion. The agent receives claims documents via email or API integration. Sources include cedent loss notifications, adjuster reports, and reserve updates.

Step 2: Claims Data Extraction. The agent extracts key fields: claimant name, loss date, loss amount, coverage type, policy number. For property claims, it extracts location, cause of loss, and building characteristics. For liability claims, it extracts claimant details, allegation type, and settlement status.

Step 3: Treaty Matching. The agent uses the Knowledge Hub to match the claim against the relevant treaty agreements. It identifies which treaties apply, what the coverage limits are, and what the retention amounts are. For layered programs, the agent calculates which layer is triggered based on the loss amount.

Step 4: Reserve Calculation. The agent calculates the reinsurance reserve based on the treaty terms and the loss amount. It accounts for retention amounts, coverage limits, and reinstatement provisions. For aggregate excess treaties, the agent tracks cumulative losses against the attachment point.

Step 5: Automated Claims Report. The agent generates a claims report showing the extracted data, the matched treaties, and the calculated reserves. The report is ready for human review and approval, with links to all source documents.

This workflow reduces claims intake time from 2 days to 4 hours. It also improves accuracy. Every reserve calculation is traceable back to the source documents and treaty terms.

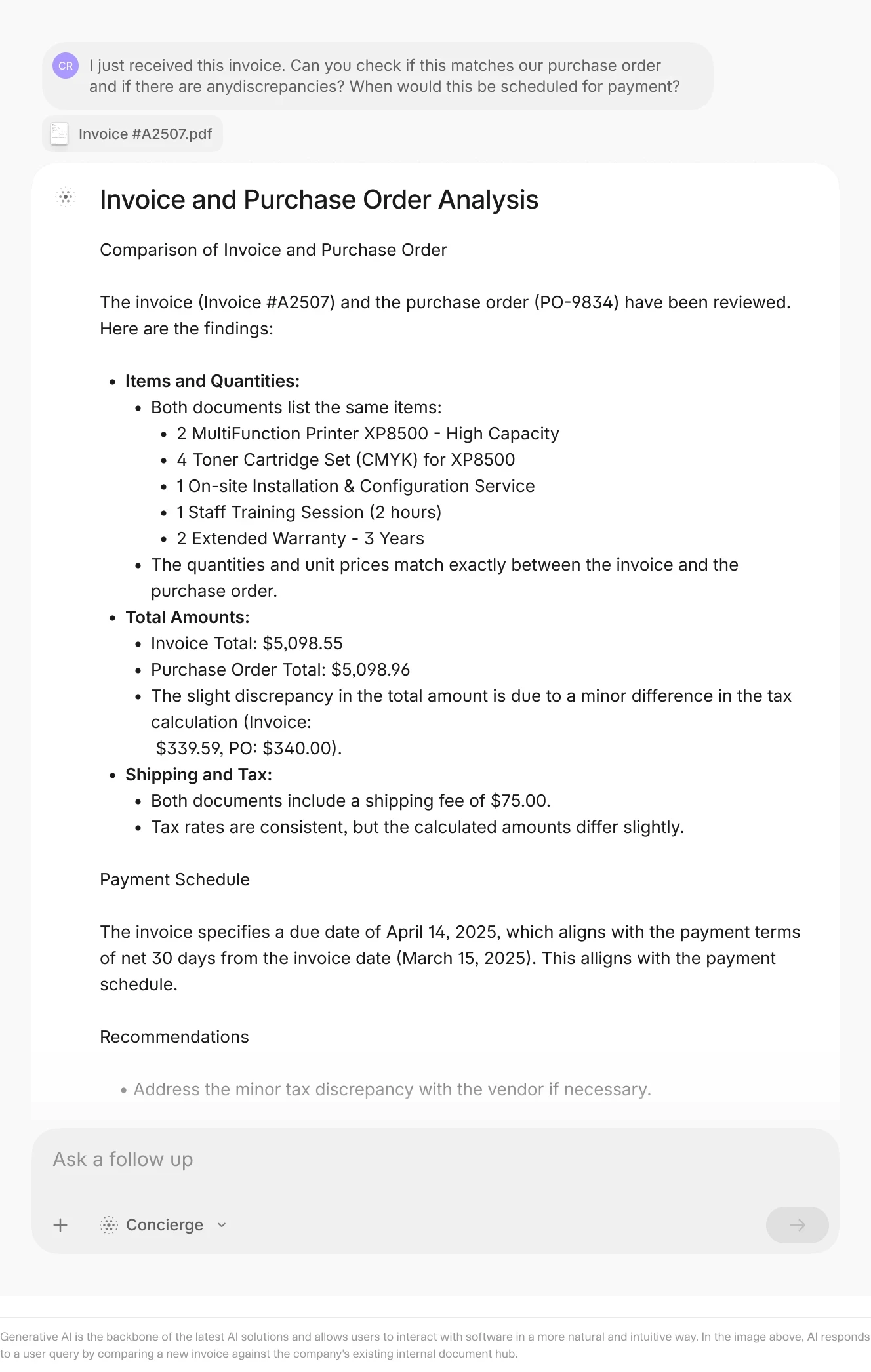

AI compares invoices to POs and flags mismatches for a 3-way match review. The same validation approach applies to bordereaux reconciliation.

Implementation Guide: Migrating to a Modern Reinsurance Stack

Migrating from a legacy reinsurance platform to a modern, AI-enabled stack is a complex process. It requires careful planning, stakeholder alignment, and a phased approach to minimize disruption.

Phase 1: Assessment and Planning (Weeks 1-4)

The first step is to assess your current state and define your future state.

Document Current Workflows: Map out every step in your current reinsurance workflows. Identify where manual processes occur, where data is re-keyed, and where bottlenecks exist. Common bottleneck areas include bordereaux ingestion, treaty data entry, and month-end reconciliation.

Identify Pain Points: Interview stakeholders. Underwriters, analysts, actuaries, IT teams. Understand their pain points. What takes the most time? What causes the most errors? What processes are most frustrating? In our experience, bordereaux reconciliation and treaty amendment tracking top the list.

Define Success Metrics: Establish clear success metrics for the migration. Common metrics include: time to process bordereaux (target: 80% reduction), error rate in premium calculations (target: below 1%), time to settle claims (target: 50% reduction), and cost per transaction.

Select Platforms: Based on your pain points and success metrics, select the platforms that best fit your needs. Consider a modular approach. An AI ingestion layer (like V7 Go), a core reinsurance platform (like Guidewire or SAP), and a visualization layer (like Tableau or PowerBI).

Phase 2: Pilot Implementation (Weeks 5-12)

The second step is to run a pilot implementation with a limited scope. This allows you to test the new platforms, identify issues, and refine your approach before rolling out to the entire organization.

Select a Pilot Use Case: Choose a high-value, low-risk use case for the pilot. Common choices include bordereaux reconciliation for one treaty type, treaty data extraction for renewal season, or claims intake for a specific line of business.

Configure the AI Agent: Work with your AI platform vendor to configure the agent for your specific use case. This involves defining the fields to extract, the validation rules to apply, and the output format. For treaty extraction, define fields like treaty number, effective date, coverage type, limits by layer, retention, commission structure, and reinstatement terms.

Integrate with Existing Systems: Connect the AI agent to your existing reinsurance platform via API. Ensure that data flows from the agent to the platform. Test the integration with sample documents representing the full range of formats you receive from cedents.

Run the Pilot: Process a sample set of documents through the AI agent. Measure the time savings, error rate, and user satisfaction. Collect feedback from stakeholders and refine the agent configuration. Expect 2-3 iteration cycles before the agent meets production quality standards.

Phase 3: Full Rollout (Weeks 13-24)

The third step is to roll out the new platforms to the entire organization.

Migrate Historical Data: Migrate historical treaty data, bordereaux files, and claims records from the legacy platform to the new platform. This is often the most time-consuming step, as it requires data cleansing, format normalization, and validation. Budget 4-6 weeks for data migration depending on volume.

Train Users: Provide training to all users. Underwriters, analysts, actuaries, IT teams. Ensure they understand how to use the new platforms, how to interpret the AI agent outputs, and how to escalate issues. Include hands-on exercises with real documents.

Monitor and Optimize: After the rollout, monitor the performance of the new platforms. Track the success metrics you defined in Phase 1. Identify areas for optimization and work with your vendors to refine the configurations.

Common Pitfalls to Avoid

Based on feedback from reinsurance operations managers, here are the most common pitfalls during a migration:

Underestimating Data Quality Issues: Legacy data is often messy, incomplete, and inconsistent. Budget extra time for data cleansing and validation. We have seen data migration timelines double when historical data quality is poor.

Ignoring Change Management: Users are resistant to change, especially when it involves replacing familiar workflows. Invest in change management. Communicate the benefits, provide training, and address concerns. Identify champions in each department who can support their peers.

Over-Customizing the Platform: Resist the temptation to customize the platform to match your legacy workflows exactly. Instead, adapt your workflows to take advantage of the new platform's capabilities. Customization increases implementation time and maintenance burden.

Skipping the Pilot: A pilot implementation allows you to test the new platforms, identify issues, and refine your approach before rolling out to the entire organization. Skipping the pilot increases the risk of a failed rollout.

Advanced Use Cases: Beyond Basic Automation

Once you have solved the data ingestion problem, modern reinsurance software opens up high-value capabilities that go beyond simple accounting.

Automated Treaty Compliance Monitoring

One of the most pressing demands from regulators and auditors is detailed compliance monitoring. If a treaty includes a clause that limits coverage to certain geographic regions, auditors want to know immediately if a claim falls outside that region.

With an AI-enabled stack, this becomes a query. V7 Go can ingest the treaty agreements, extract the compliance clauses using LLMs, and feed a compliance monitoring system. Every claim is automatically checked against the treaty terms, and any violations are flagged for review. The system tracks territorial restrictions, coverage caps, and exclusion clauses without manual cross-referencing.

Predictive Loss Modeling

For reinsurance underwriters, risk lives in the loss forecasts. Predicting future losses requires analyzing historical claims data, understanding loss trends, and modeling catastrophic events.

This is a prime use case for intelligent document processing combined with predictive analytics. An AI workflow can ingest historical loss runs, extract claims data, and feed a predictive model. The model can then forecast future losses based on historical trends, catastrophic event scenarios, and treaty terms. The output is a loss forecast that updates automatically as new claims data arrives.

Automated Regulatory Reporting

Regulatory reporting in reinsurance is complex and time-consuming. Regulators require detailed reports on treaty structures, premium volumes, claims reserves, and solvency ratios. These reports must be filed quarterly or annually, and they require data from multiple systems.

An AI agent can automate this process. It extracts data from the reinsurance platform, the claims system, and the financial reporting system, and generates the regulatory reports automatically. This reduces the time to file reports from weeks to days, and it improves accuracy by eliminating manual data entry. For Solvency II reporting, the agent can extract the specific data points required by the regulation and populate the standard templates.

Financial analysis workflow: data collection, extraction, validation, analysis, modeling, and reporting. The same stages apply to reinsurance regulatory reporting.

The Future of Reinsurance Operations: Modular and Connected

The era of the all-in-one monolithic reinsurance platform is fading. The future belongs to modular, interconnected ecosystems where the best-in-class ledger (like Guidewire or SAP) connects with the best-in-class intelligence layer (like V7 Go) and the best visualization layer (like PowerBI).

This approach reduces vendor lock-in and allows you to swap out components as technology improves. The critical glue holding this stack together is clean, structured data. By automating the ingestion layer, you ensure that every downstream system is fed with accurate, timely information.

For reinsurance operations, the competitive advantage will not come from having the same software as everyone else. It will come from information advantage: the ability to ingest, synthesize, and act on unstructured treaty data faster and more accurately than the competition.

According to market research, cloud-based deployments account for 56% of new software implementations in 2024, reflecting a clear preference for scalable, cost-effective solutions. This trend will accelerate as AI agents become more sophisticated and as reinsurance operations demand more flexibility.

What Changes Monday Morning

If you take one thing from this article, here is what to do this week:

Pick one treaty family. Select a treaty type where you process the most documents or experience the most errors. Quota share treaties with high cedent volume are a good starting point.

Define 20 fields to extract. Document the specific fields you need from each treaty: treaty number, effective dates, coverage type, limits, retention, commission rates, territory, exclusions. Write acceptance criteria for each field.

Set up a 2-week pilot. Choose 3 cedents and run their documents through an AI agent. Measure extraction accuracy against your manual baseline. Sample 10% of outputs for QA.

Route outputs into your staging environment. Connect the agent output to a staging table in your reinsurance platform. Validate that the data flows correctly before pushing to production.

The key to success is not to replace your entire stack overnight. Start with a high-value, low-risk use case. Run a pilot, measure the results, and refine your approach. Then expand to other use cases, building a modular stack that fits your specific needs.

To see how you can automate the ingestion of your reinsurance data, from treaty agreements to bordereaux reconciliation, book a demo with V7 Go.

What is the difference between reinsurance software and insurance software?

Reinsurance software is designed to manage the transfer of risk from primary insurers (cedents) to reinsurers. It handles treaty structures, premium bordereaux, claims reserves, and regulatory reporting specific to reinsurance operations. Insurance software, by contrast, manages the relationship between insurers and policyholders: policy administration, claims processing, billing, and customer service. While there is some overlap in functionality, reinsurance software must handle more complex treaty structures, multi-layer coverage, and reconciliation of data from multiple cedents.

+

Can AI fully automate reinsurance operations?

No, and you should be cautious of anyone claiming it can. AI automates the data gathering, extraction, and reconciliation components. It removes the manual friction of getting data into the system. However, the strategic decisions remain human tasks: treaty negotiation, risk assessment, claims adjudication. AI agents are best used to handle the repetitive, high-volume tasks (like bordereaux reconciliation or treaty data extraction), freeing up human experts to focus on the complex, judgment-based work.

+

Is it safe to put sensitive reinsurance data into cloud-based AI software?

Yes, provided the vendor meets strict enterprise security standards. The industry standard is SOC 2 Type II certification. You should also look for ISO 27001 certification, GDPR/CCPA compliance, and encryption in transit and at rest. Enterprise-grade platforms like V7 Go include these protections by default. Additionally, many platforms offer on-premises deployment options for organizations with strict data residency requirements.

+

How long does it take to implement reinsurance software?

It varies by complexity. A cloud-native tool for a small reinsurance operation might take 4-8 weeks. A complex enterprise implementation with Guidewire or SAP often takes 6-12 months due to historical data migration, treaty structure configuration, and custom reporting. Deploying a specialized AI ingestion layer like V7 Go is much faster: often live in days for a pilot use case, with full rollout in 8-12 weeks.

+

What is the biggest challenge in reinsurance software implementation?

Pricing is typically customized to the buyer. For enterprise platforms like Guidewire, SAP, or Oracle, annual costs often range from $100,000 to over $500,000 for mid-sized reinsurance operations, plus significant implementation fees. Modular AI tools for data extraction like V7 Go are often priced on usage (volume of documents processed), offering a more scalable entry point for organizations that want to start with a specific use case and expand over time.

+

How much does reinsurance software cost?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.