19 min read

—

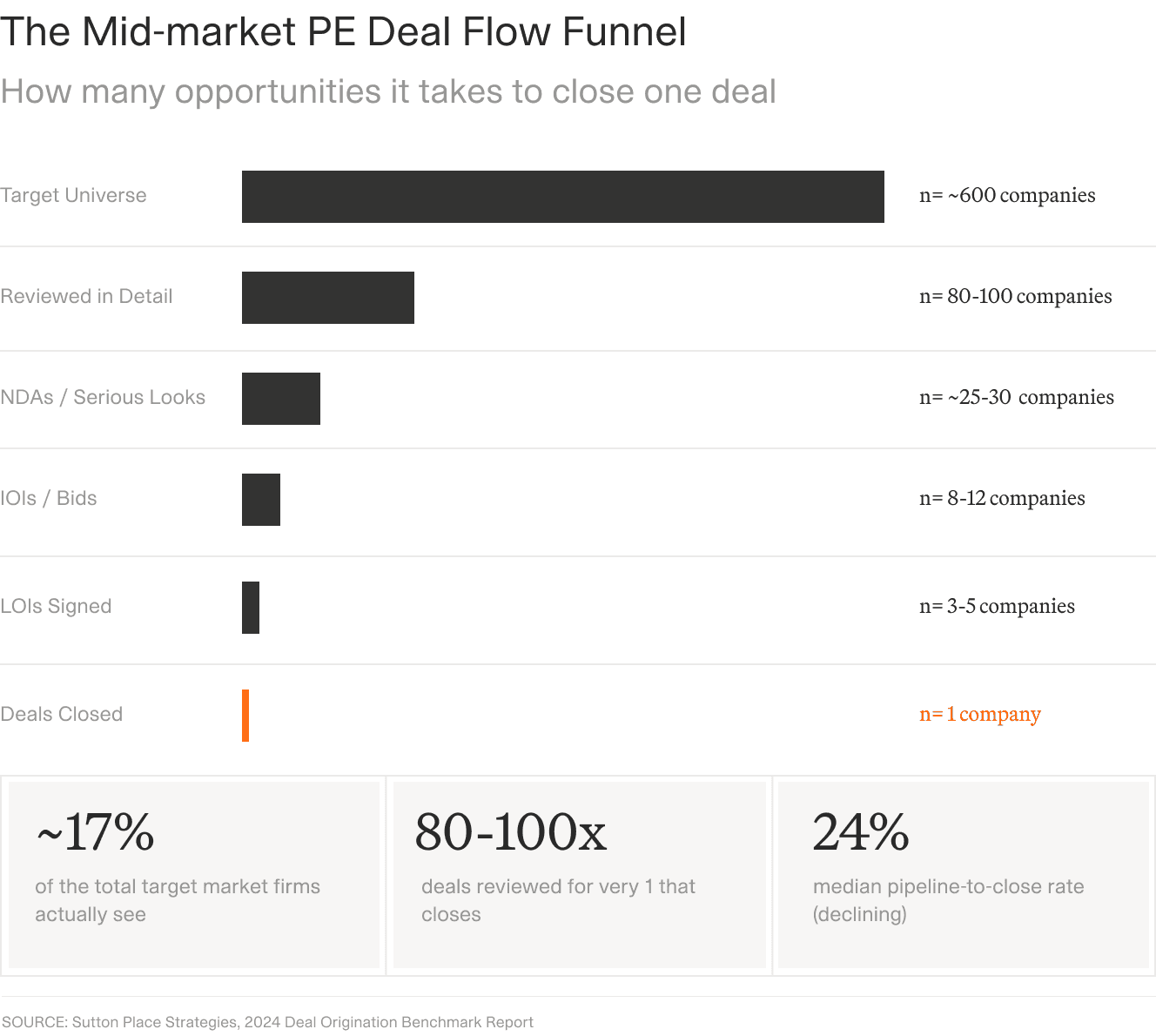

A mid-market buyout fund reviewed 97 confidential information memoranda (CIMs) last year. They passed on 96. That ratio is not a failure: it is how the private equity due diligence process is supposed to work. According to Sutton Place Strategies, deal teams review 80 to 100 opportunities for every deal they close, and the median pipeline-to-close rate has been declining for three consecutive years.

The question is not whether to run due diligence (DD) on every opportunity. It is how to do it thoroughly when the economics of the pipeline make thoroughness structurally difficult.

Two approaches now exist. The traditional approach assigns each document type to a specialist: accountants spread the financials, lawyers review the contracts, consultants model the market. Workstreams run in parallel for four to eight weeks while analysts sample what they can under time pressure. The AI-assisted approach deploys agents that review every document at consistent depth, extract structured data, surface red flags, and produce first-draft outputs that analysts then refine.

This article covers both. It explains what private equity due diligence actually involves, where the traditional process breaks down under volume and time pressure, and where AI changes the economics of document-heavy work. Firms already using AI in finance are discovering that the biggest gains are in coverage, not just speed. For an overview of how AI agents work more generally, our AI agents guide walks through how they work.

In this article:

What private equity due diligence is, how it is structured, and what deal teams actually do across four to eight weeks of a confirmatory process.

The five core types of due diligence: financial, commercial, legal, operational, and technology, with key documents and red flags for each.

Where the traditional process breaks down, and why 10 to 20 percent data room coverage is a structural problem rather than an analyst failure.

How AI changes each stage of the diligence process, with specific time benchmarks, and what it cannot replace.

The document workflows where AI delivers the largest time savings, and how to build an AI-enhanced process your deal team will actually use.

AI for document processing

Cut due diligence document review time in half

Get started today

What Is Private Equity Due Diligence?

Private equity due diligence is the structured investigation of a target company before a firm commits capital. A complete DD process examines the financial health, commercial position, legal obligations, operational capacity, and technology infrastructure of the business. Its purpose is not to confirm the investment thesis but to stress-test it: to verify that the growth assumptions are defensible, the risks are manageable, and the value creation plan survives contact with the actual business.

Due diligence in private equity is the process of independently verifying the claims made in a CIM, validating the assumptions behind an investment thesis, and surfacing the risks that management presentations are unlikely to disclose.

Most deal teams describe it in two phases. Exploratory diligence runs before a Letter of Intent (LOI) is signed. Its purpose is to identify deal-breakers: revenue concentration so severe it changes the valuation, legal liabilities that were not disclosed, a technology stack that cannot scale. If exploratory diligence surfaces a deal-breaker, the process stops. If it does not, the firm signs an LOI and enters confirmatory diligence.

Confirmatory diligence runs four to eight weeks for a mid-market buyout and involves multiple parallel workstreams. Financial advisors run a Quality of Earnings (Q of E) analysis. Lawyers review every material contract. Operations consultants assess the management team. IT specialists audit the technology architecture. Each workstream produces its own deliverable, and the deal team synthesises them into an investment committee (IC) memo.

The data room sits at the centre of all of it. A typical mid-market buyout data room contains 3,000 to 10,000 documents: financial statements, board minutes, customer contracts, employment agreements, IP filings, regulatory correspondence, and dozens of other document types. Everything a buyer needs to verify is in there, somewhere.

Source: Sutton Place Strategies 2024 Deal Origination Benchmark Report.

The Five Core Types of Due Diligence in Private Equity

Each DD workstream has a different scope, different document set, and different output. Understanding them separately matters because AI affects each differently, and the time savings are not evenly distributed. The legal and financial workstreams, which are most document-intensive, see the largest gains. The operational workstream, which is most judgment-intensive, sees the smallest.

DD type | Primary focus | Key documents | Red flags to surface |

|---|---|---|---|

Financial | Earnings quality, cash flow, balance sheet integrity | Financial statements, management accounts, Q of E report | Revenue concentration, EBITDA add-back anomalies, working capital swings |

Commercial | Market position, customer base, competitive dynamics | CIM, customer contracts, market research, sales pipeline data | Customer concentration, churn risk, undefended market position |

Legal | Contracts, compliance, IP, litigation exposure | Corporate records, material contracts, IP filings, regulatory correspondence | Undisclosed liabilities, restrictive covenants, regulatory exposure |

Operational | Team, processes, scalability | Org charts, process documentation, HR data, management bios | Key person risk, supply chain fragility, process gaps |

Technology | Systems architecture, cybersecurity, technical debt | IT architecture diagrams, security audits, software licences | Legacy system dependency, data privacy exposure, integration costs |

Financial due diligence

Financial diligence examines the income statement, balance sheet, and cash flows across three to five years of history. Its central deliverable is the Q of E report: an independent analysis of the sustainability and quality of the target's earnings, prepared by accounting advisors, identifying earnings before interest, taxes, depreciation, and amortisation (EBITDA) adjustments that distinguish recurring from one-time items.

A Q of E does not simply restate the management accounts. It questions every adjustment management has made to reported EBITDA, assesses the quality of revenue recognition, and stress-tests working capital normalisation. In deals where EBITDA has been aggressively adjusted, this workstream often determines whether the deal proceeds at the agreed valuation or requires renegotiation.

Beyond Q of E, financial diligence validates the financial model: are the growth assumptions consistent with historical performance? Is working capital modelled correctly? Are there off-balance-sheet obligations the management accounts do not capture?

Commercial due diligence

Commercial diligence examines the investment thesis from the outside in. It asks whether the market supports the growth case and whether the target's competitive position is defensible. A typical commercial workstream covers market sizing and competitive analysis, customer concentration assessment, churn and renewal rate analysis, and pricing power evaluation.

The primary source material is the CIM, but a thorough commercial review also examines customer contracts, sales pipeline data, and independent market research. Customer concentration is the most common commercial red flag in mid-market deals: a business where two clients represent 60 percent of revenue is a different risk profile from one where no single client exceeds 8 percent.

Legal due diligence

Legal diligence reviews every material contract, IP filing, regulatory record, and employment obligation. Lawyers look for undisclosed liabilities, restrictive covenants that limit what a new owner can do with the business, IP ownership ambiguities, pending or threatened litigation, and regulatory exposure. This workstream typically produces the longest document list in any data room.

In a large data room, a legal team may need to review hundreds of contracts. Standard practice is to prioritise: senior lawyers focus on the most material agreements, associates handle the rest, and some documents are skimmed or deferred. That prioritisation is where coverage gaps emerge.

Operational due diligence

Operational diligence evaluates the team, processes, and infrastructure. It asks whether the business can sustain three to five times growth without adding proportionate headcount and whether the management team that built the business can execute the value creation plan. Key questions: who are the critical dependencies, what happens if the chief executive leaves, how scalable are the operational processes, and is there cultural alignment with the buyer's model?

This workstream is the most qualitative of the five. Analysts review org charts, management bios, and process documentation, but the real assessment happens in management interviews and reference calls. AI can assist with background research and document extraction but cannot replicate the judgment required to evaluate a management team.

Technology and IT due diligence

IT diligence has grown in importance as software systems underpin more business operations. It covers the technology stack, cybersecurity posture, data privacy compliance, and integration costs. Legacy system dependency and technical debt are the most common IT red flags in mid-market deals. A business running customer data on a 15-year-old ERP faces integration costs that belong in the valuation model, not in the risk register.

Where the Traditional DD Process Breaks Down

The traditional process was built for a world where deals move slowly and data rooms are small. Neither condition holds in mid-market private equity today.

The first structural problem is volume. A typical mid-market data room contains 3,000 to 10,000 documents. Deal teams, working with four to six advisors across parallel workstreams, can realistically review 10 to 20 percent of the total at the depth the decision requires. The remaining 80 to 90 percent is either sampled quickly, skimmed by a junior associate, or deferred until after the LOI, when time pressure is greater.

The second problem is consistency. Different analysts apply different standards. A senior associate on their fourth deal has developed heuristics for what to flag. A junior on their first has not. When review is distributed across multiple advisors with different methodologies, the output is uneven. Something that a financial advisor would catch in the numbers might not trigger a flag from the operational consultant reading a different set of documents.

The third problem is knowledge. Traditional diligence is a snapshot. The findings from a deal reviewed two years ago do not automatically inform the review of a similar deal today. If the analyst who built the thesis has left the firm, the institutional knowledge goes with them. Every new deal starts from a blank slate: new data room, new documents, new team.

The fourth problem is time. Exclusivity periods are finite. Sellers push for speed. Competition from other bidders compresses timelines. A deal team that needs six weeks to run a thorough process but has four weeks to work in will compromise. Usually that compromise comes from data room coverage: fewer documents reviewed, more assumptions carried forward from the CIM, more reliance on management representations that have not been independently verified.

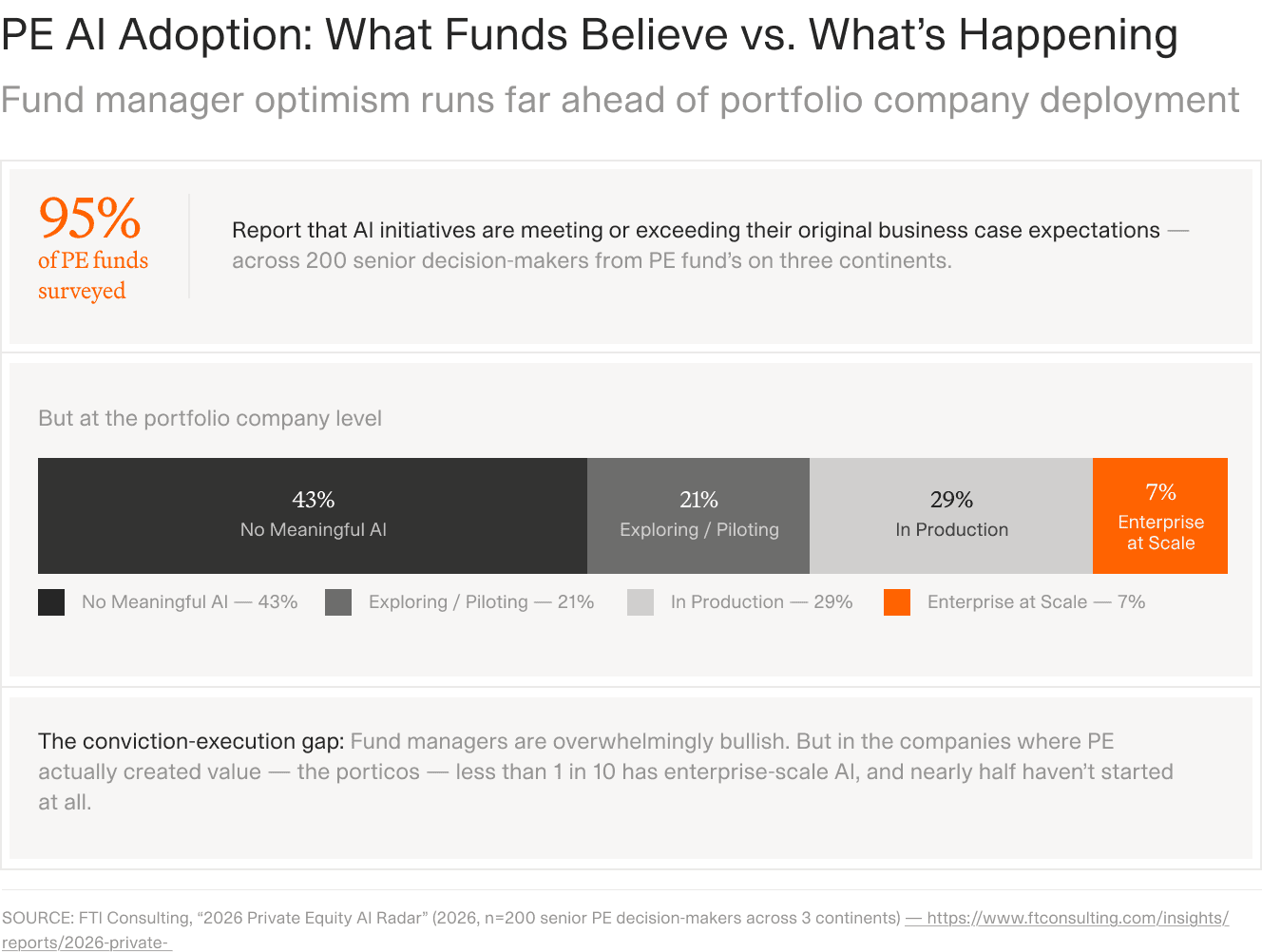

Source: FTI Consulting 2026 Private Equity AI Radar.

Research by FTI Consulting puts numbers to the gap: 95 percent of surveyed PE funds report AI initiatives are meeting or exceeding expectations, yet 43 percent of portfolio companies have no meaningful AI deployment, and only 7 percent are at enterprise scale. Senior decision-makers are bullish. The document-heavy workflows that actually consume analyst time have been slow to change.

The gap is not about willingness. It is about workflow design. Deploying a general AI assistant against a 10,000-document data room solves a different problem from deploying a configured workflow that extracts specific fields from specific document types, checks outputs against source citations, and produces a structured deliverable that integrates with the firm's IC memo process.

How AI Changes Each Stage of the PE Due Diligence Process

AI does not change what diligence requires. It changes who does the reading and how long it takes. The investment thesis still needs to be validated. The red flags still need to be surfaced. The documents still need to be reviewed. The difference is whether a human reads every page or an agent does, and what the human does with the time that frees up.

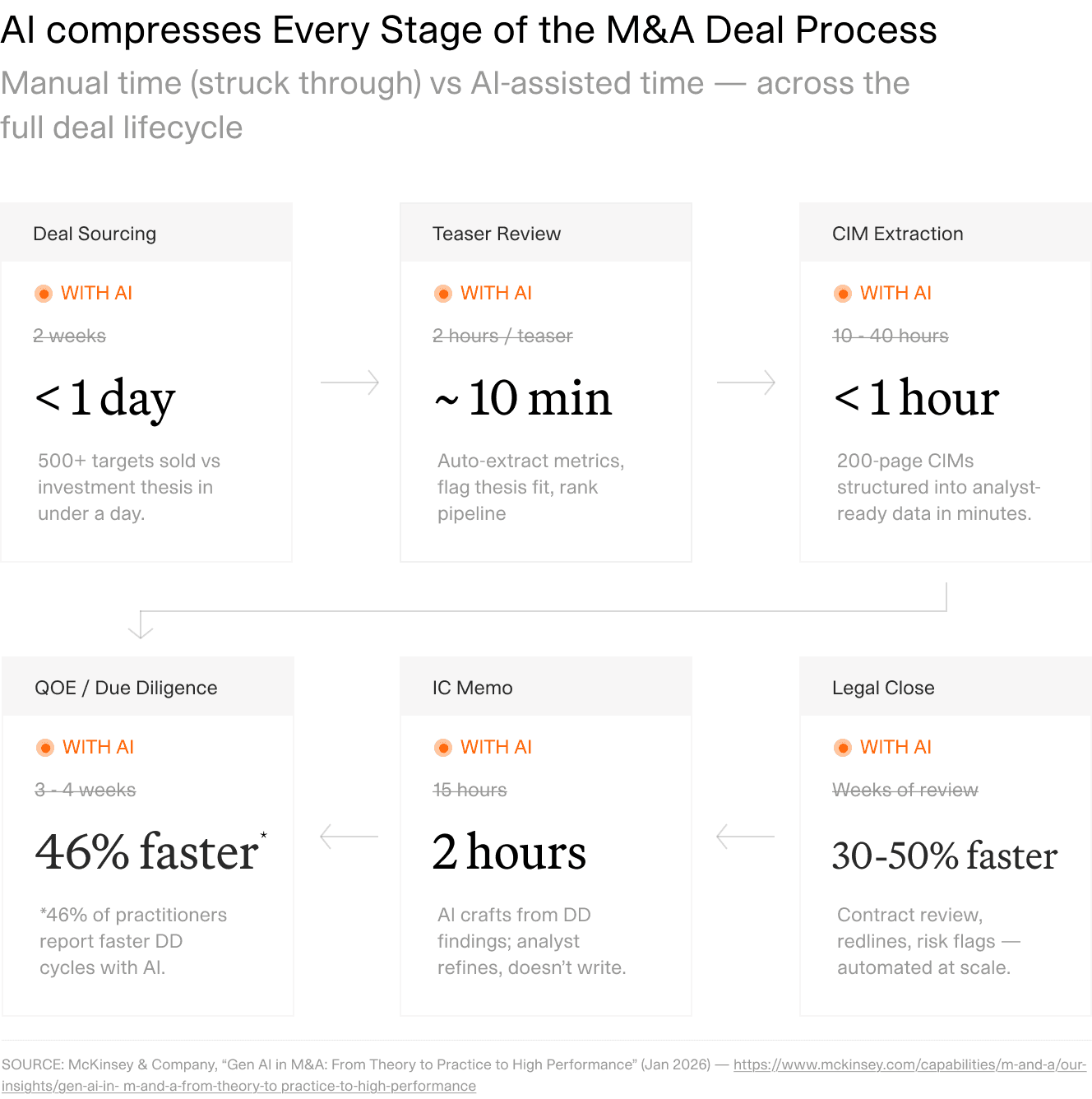

Source: McKinsey, Gen AI in M&A, January 2026.

Research by McKinsey on generative AI in M&A documents the compression across each deal stage: CIM extraction reduced from 10 to 40 hours to under one hour, Q of E and due diligence completed 46 percent faster with AI assistance, and IC memo drafting cut from 15 hours to 2 hours for the first draft. These gains compound across the full deal cycle, not just in one workstream.

DD stage | Traditional approach | AI-assisted approach | Reported time savings |

|---|---|---|---|

CIM screening | Analyst reads and summarises each CIM manually (3 to 5 hours per document) | AI extracts financial highlights, key metrics, and thesis-fit indicators in under one hour | CIM extraction: 10 to 40 hours down to under one hour |

Financial spreading | Accountants manually spread financials across periods (1 to 3 days per company) | AI extracts and structures data across all periods; flags inconsistencies between periods and management accounts | Financial spreading: 2 to 3 weeks to 3 to 5 days |

Legal contract review | Lawyers review clause by clause; senior review concentrated on highest-priority agreements | AI reviews 100 percent of the contract corpus; extracts key provisions, deadlines, and anomalies at consistent depth | Contract review: 4 to 6 weeks to 1 to 2 weeks |

Data room coverage | Teams sample 10 to 20 percent of documents under time pressure | AI reviews all documents at consistent depth; cross-references obligations across the full corpus | Full coverage replacing selective sampling |

IC memo drafting | Associates draft from notes; senior review and rewrite adds 10 to 15 hours | AI drafts from structured DD findings; analyst refines rather than writes from scratch | Initial draft: 15 hours to 2 hours |

The legal workstream shows the clearest time savings because the work is most directly document-dependent. A team reviewing 400 contracts in a data room used to face a binary choice: spend the time to review them all properly and miss the exclusivity window, or sample and accept the coverage gap. AI removes the binary. Every contract gets reviewed at consistent depth, key provisions get extracted to a structured output, and the senior lawyer reviews the flagged items rather than the corpus.

For financial diligence, the primary gain is in spreading and anomaly detection. An agent can extract revenue figures, EBITDA adjustments, and working capital metrics across five years of management accounts and flag inconsistencies between what management reported in the CIM and what the underlying financials show. The Q of E team still prepares the report. They start from an AI-extracted dataset rather than a blank spreadsheet.

What AI Still Cannot Do in PE Due Diligence

The question deal teams most often ask is whether AI replaces analysts. Wrong question. The right question is: which parts of diligence require human judgment, and which are document processing?

Management assessment cannot be automated. Evaluating whether a management team has the judgment, adaptability, and cultural fit to execute a value creation plan requires direct interaction, reference calls, and the pattern recognition that comes from having assessed dozens of management teams in comparable situations. AI can surface background information and flag inconsistencies between what management says and what the documents show. It cannot assess the quality of the thinking in the room.

Deal structuring requires negotiation intelligence. Co-investment rights, governance terms, management incentive packages, and earn-out mechanisms involve tradeoffs that depend on the specific counterparties, their objectives, and the history of the relationship. No model can substitute for the judgment of a dealmaker who knows the room.

LP governance and relationship context remain human. Deal decisions depend on LP preferences, fund strategy, and relationship history that are not captured in any document. An earn-out structure that works for one LP group may be unacceptable to another. This is judgment that does not compress.

Regulatory interpretation in novel situations stays with the lawyers. AI can flag regulatory risk based on patterns in the documents. It cannot interpret how a novel regulatory situation will play out or advise on the strategy for managing it.

AI removes the document work around the decision: the reading, the extracting, the cross-referencing, and the first-draft synthesis. The decision itself stays with the analyst.

This distinction matters for how AI is positioned in a DD workflow. Deal teams that use AI well treat it as the layer that produces first-pass intelligence: structured extractions, flagged anomalies, draft summaries. The analyst's job is to interrogate those outputs, validate them against source documents, and apply the judgment the model cannot replicate.

Document Workflows Where AI Has the Biggest Impact

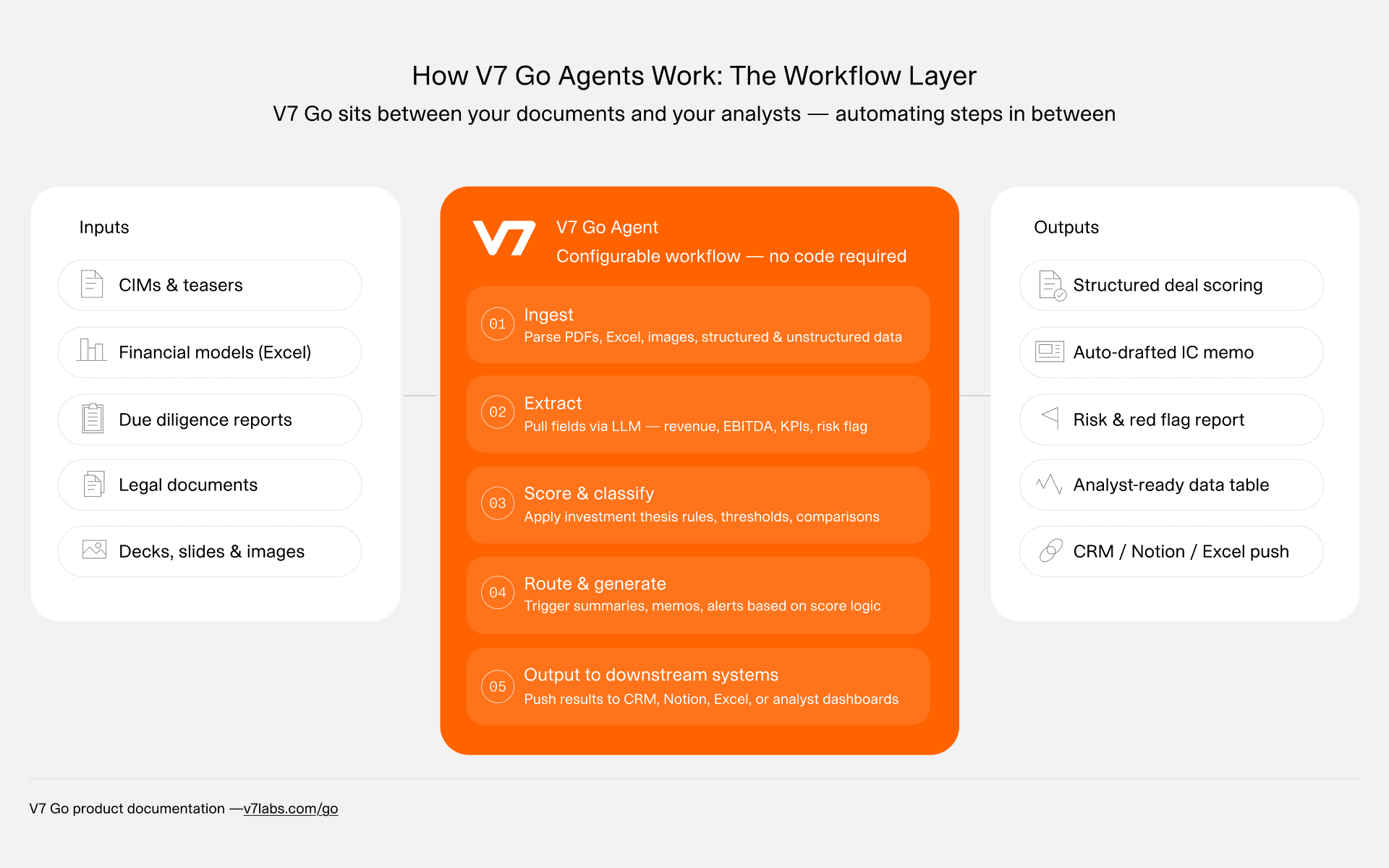

The documents that dominate diligence time are not the ones that require the most judgment. They are the ones that require the most reading. AI's contribution sits in that reading: covering the full document corpus at consistent depth, extracting specific fields, and surfacing what a human reviewer needs to examine more closely.

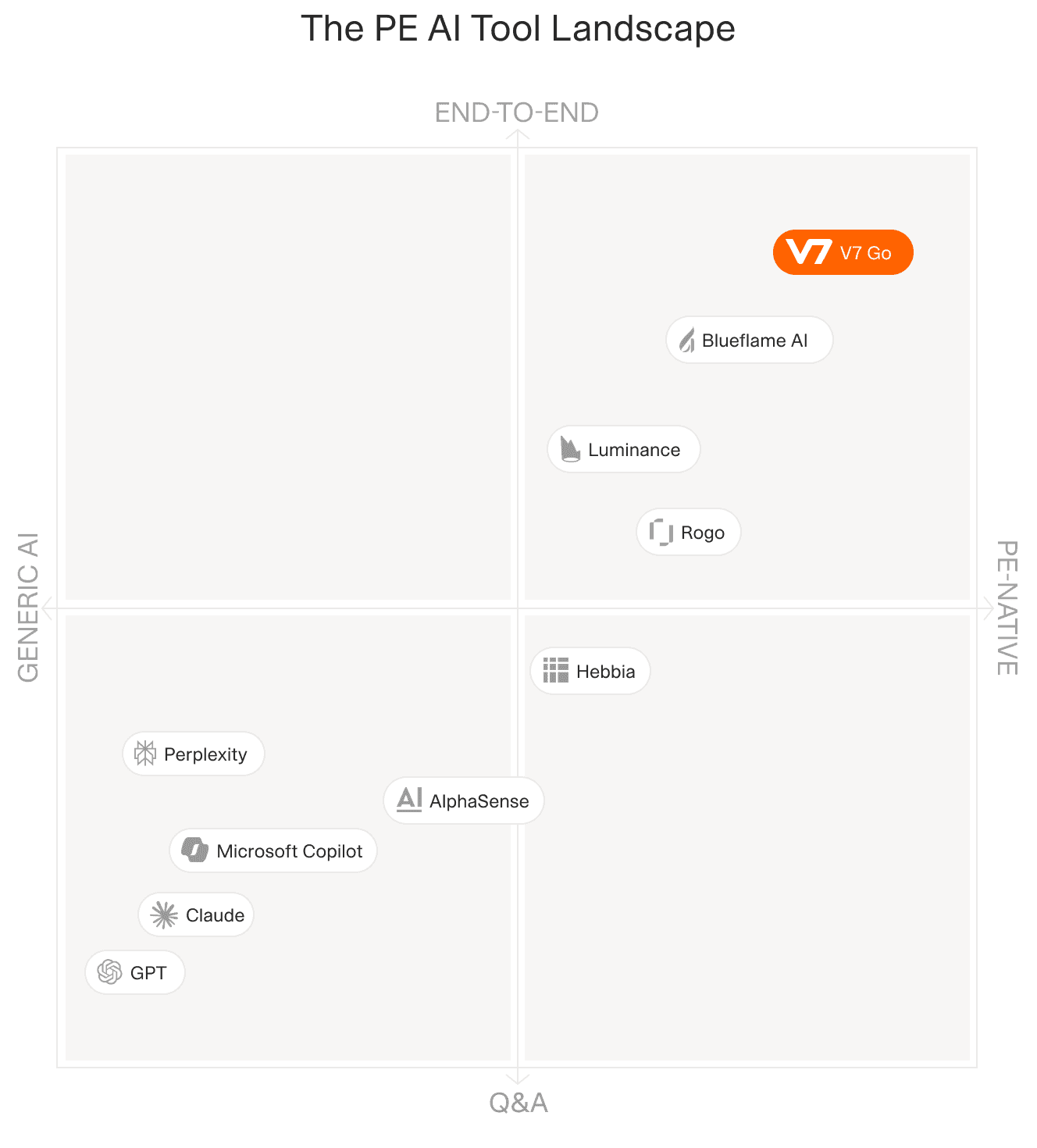

V7 Go was built for this layer of the DD process. Deal teams define what they need extracted from each document type: financial metrics from CIMs, obligation terms from contracts, risk disclosures from board minutes. The agent extracts that structure consistently across every document in the data room. The output flows directly into the firm's review workflow, with every extracted value linked to its source location in the original document for analyst validation. The AI Due Diligence Agent and CIM Review automation show specific workflow examples for each document type.

Document type | Traditional workflow | AI workflow |

|---|---|---|

Confidential Information Memorandum | Analyst reads and manually summarises (3 to 5 hours per document) | AI extracts financial highlights, management summary, key metrics, and thesis-fit indicators in under one hour |

Financial statements | Accountants manually spread across periods (1 to 3 days) | AI extracts and structures across all periods; flags inconsistencies between periods and versus management accounts |

Legal contracts | Lawyers review clause by clause; some contracts are sampled rather than fully read | AI extracts key provisions, deadlines, obligations, and anomalies from every contract at consistent depth |

Management presentations | Analysts manually note key data points; no systematic cross-reference with financials | AI extracts financial data and growth assumptions; cross-references against underlying financials automatically |

Board minutes | Sequential manual review; risk disclosures and related-party transactions may be missed | AI scans the full corpus for red flags, related-party transactions, and risk disclosures; flags anomalies for senior review |

Source traceability is not a secondary concern. In a regulated investment process, every figure in the IC memo and every risk assessment needs to point back to where in the source document it came from. Firms that have piloted AI-assisted diligence workflows report consistently that the first question from senior partners is not "can we trust the AI?" but "can we show where this came from?"

The AI Citations feature in V7 Go addresses this directly. Every extracted value links back to its exact location in the source document. An analyst reviewing an extracted EBITDA figure can click through to the page and line in the management accounts where that figure appears. This matters both for internal review quality and for the firm's ability to demonstrate the integrity of its diligence process to LPs.

The Context Graph: when AI carries institutional memory

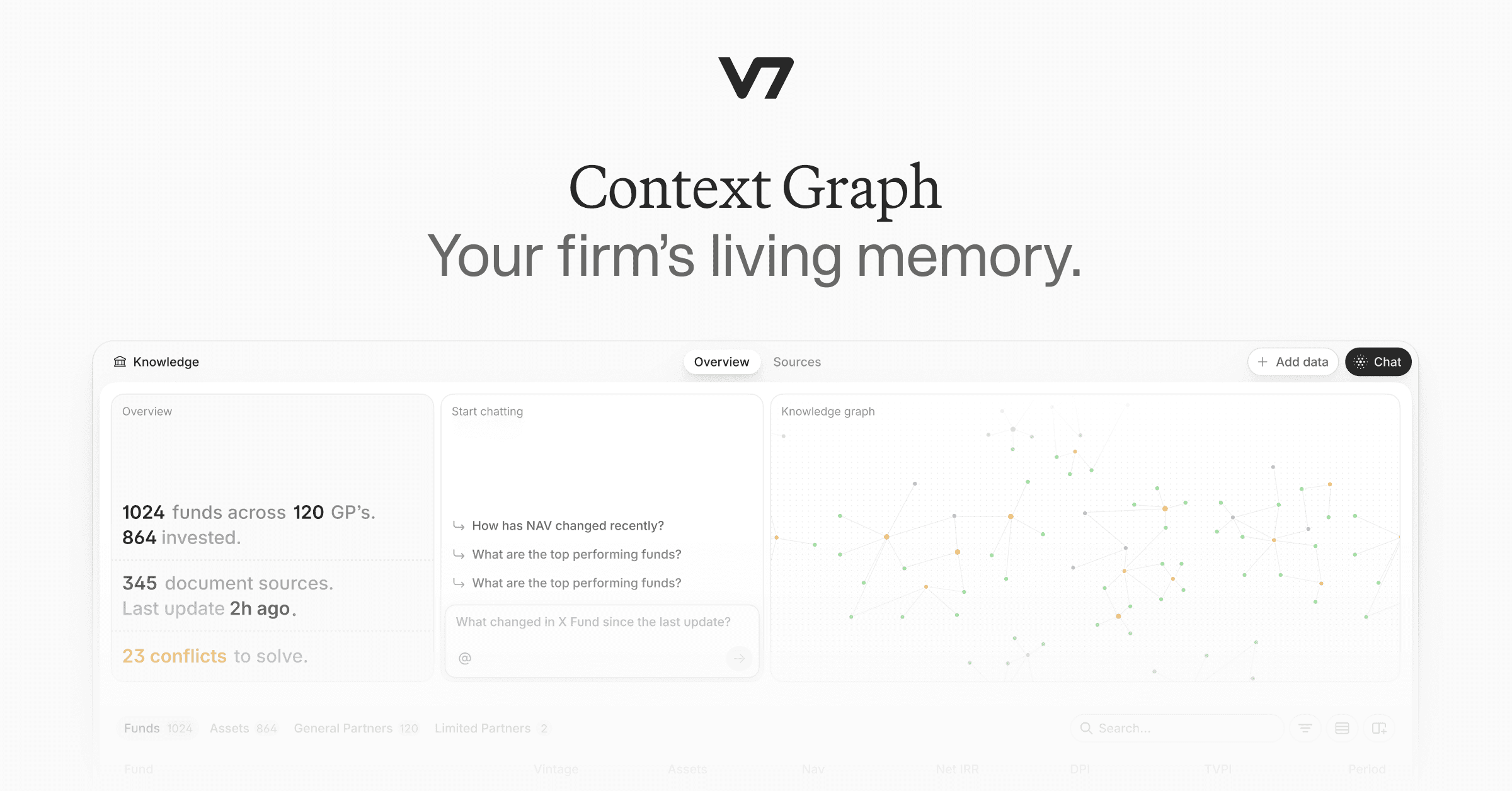

The data room is only part of the picture. A firm that has screened 400 companies in a sector over five years has accumulated more institutional knowledge about that sector than any individual analyst. Most of that knowledge does not survive in queryable form. It lives in old deal memos, prior committee decisions, and the heads of people who may have left the firm.

V7 Go Context Graph: querying the firm's full fund and entity history in natural language.

V7 Go's Context Graph changes this. It is a persistent, entity-resolved knowledge layer built on the firm's own data: every company evaluated, every deal considered, every GP relationship documented. When a new CIM arrives, the screening agent does not start from a blank slate. It queries the Context Graph to surface whether the firm has evaluated this company before, what the prior pass rationale was, which portfolio companies overlap with the target's customer base, and what the firm's view on the sector has been over time.

For firms managing 400 to 600 CIMs per year and passing on 98 percent of them, this is not a marginal improvement. It is structural. The knowledge that used to leave when an analyst left the firm now stays. A company that was evaluated two years ago and passed for specific reasons arrives again under new management: the firm's view of it is instantly available to the screening agent and the analyst reviewing the new book.

Most AI tools know everything about the world and nothing about your firm. Context Graph fixes the second part. The firm gets smarter with every document processed, every deal evaluated, every interaction logged. The knowledge belongs to the firm, not to the session or the analyst who ran it.

For the broader picture of how these workflows connect, see our AI in due diligence guide and the AI investment memo generation automation for the output end of the workflow.

Building Your AI-Enhanced PE Due Diligence Process

A useful AI diligence implementation starts with one question: which workstream has the highest document volume and the clearest output requirement? Start there, not with a platform-wide rollout.

For most mid-market deal teams, the answer is legal contract review or financial spreading. Both have large, consistent document sets, clear extraction requirements, and structured outputs that feed directly into downstream deliverables. Both are also areas where thoroughness is currently limited by time rather than judgment.

Define document extraction requirements for each document type before the data room opens: what fields do you need from every contract, every financial statement, every board minute?

Configure AI review for all legal and financial documents on day one of data room access, rather than waiting until time pressure forces prioritisation.

Run AI-flagged anomalies through senior analyst validation before they reach the IC memo: every extracted figure or risk flag should have a human sign-off in the review workflow.

Use AI for Q of E preparation: extract management-reported EBITDA, flag add-back categorisation, and surface inconsistencies between periods before the accounting advisor begins the formal report.

Review AI-extracted CIM data within 48 hours of receiving the book: the screening stage is where gains compound across the full pipeline.

Document your AI tooling for LP due diligence questionnaires: LPs are increasingly asking how firms use AI in deal evaluation and portfolio monitoring, and a clear answer demonstrates operational discipline.

The financial statement spreading automation and the Dataroom to IC Memo workflow are practical entry points for deal teams building their first configured workflow. They cover the highest-volume, most time-intensive document types and produce structured outputs that integrate directly into existing IC memo and deal-tracking processes.

The principle is straightforward. AI handles the reading. Your team handles the judgment. The ratio of reading to judgment in a typical diligence process is heavily weighted toward reading.

AI changes that ratio.

Deal teams that have deployed configured AI diligence workflows report consistently that the return on investment is not primarily in time saved on individual documents. It is in the quality of coverage across the full data room. When analysts review every contract at consistent depth rather than sampling, the risk of missing a material obligation drops substantially. When every CIM has been screened against the investment thesis in under an hour rather than over three days, the team can run a more disciplined pipeline without adding headcount.

V7 Go's approach to finance AI starts from how deal teams actually work: document-heavy inputs, structured outputs, source traceability at every step. If you want to see how it handles a specific document set relevant to your process, the place to start is the AI Due Diligence Agent configured for your document types and output schema, not a generic demo that does not reflect your actual workflow.

What is the private equity due diligence process?

Private equity due diligence is the structured investigation of a target company before a private equity firm commits capital. It runs across two phases. Exploratory diligence, conducted before a Letter of Intent is signed, aims to identify deal-breakers: structural risks, undisclosed liabilities, or investment thesis assumptions that the underlying data does not support. If exploratory diligence finds nothing material, the firm signs the LOI and enters confirmatory diligence. Confirmatory diligence runs four to eight weeks for a comprehensive buyout process and covers five parallel workstreams: financial, commercial, legal, operational, and technology. Each workstream produces a structured deliverable, and the deal team synthesises them into an investment committee memo. The data room, which typically contains 3,000 to 10,000 documents in a mid-market deal, is the primary source of documentary evidence for all five workstreams. The CIM is the starting point for commercial and financial assessment. Legal and operational workstreams pull from contracts, board minutes, and management records. Technology diligence draws on IT architecture documentation and security audit reports.

+

What are the five types of due diligence in private equity?

The five core types are financial, commercial, legal, operational, and technology. Financial diligence examines earnings quality, cash flow sustainability, and balance sheet integrity, with a Quality of Earnings report as the central deliverable. Commercial diligence assesses market position, customer concentration, competitive dynamics, and whether the investment thesis growth assumptions are defensible. Legal diligence reviews material contracts, IP ownership, regulatory compliance, outstanding litigation, and employment obligations. Operational diligence evaluates the management team, key person risk, process scalability, and cultural alignment with the buyer's model. Technology diligence covers the systems architecture, cybersecurity posture, technical debt, and integration costs. Each workstream involves a different set of advisors and a different primary document set, but all five typically run in parallel during the confirmatory phase. AI affects each workstream differently: legal and financial show the largest time savings because they are most document-intensive. Operational diligence, which depends on management interviews and reference calls, shows the smallest gains from AI assistance.

+

How long does private equity due diligence take?

A comprehensive confirmatory diligence process for a mid-market buyout typically runs four to eight weeks. The timeline varies with deal complexity, data room quality, and the breadth of advisory workstreams deployed. Exploratory diligence, conducted before LOI signing, usually runs two to four weeks for an initial assessment aimed at identifying deal-breakers. AI-assisted document processing has compressed the document-intensive parts of diligence significantly. Industry data shows financial spreading reduced from two to three weeks to three to five days, and legal contract review compressed from four to six weeks to one to two weeks for the document extraction and classification phase. These are not guarantees: they reflect industry-reported outcomes from teams that have configured specific extraction workflows for their document types, not generic AI deployments against unstructured data rooms. Under competitive auction timelines, where a seller pushes for exclusivity periods of four weeks or less, the ability to compress document review to days rather than weeks has a direct impact on deal quality and risk management.

+

What documents are required for PE due diligence?

Core documents span all five workstreams. Financial diligence: three to five years of financial statements, management accounts, board minutes with financial updates, and the Quality of Earnings report. Commercial diligence: the Confidential Information Memorandum, customer contracts, market research, and sales pipeline data. Legal diligence: corporate records, material contracts, IP filings, regulatory correspondence, employment agreements, and outstanding litigation records. Operational diligence: org charts, management bios, process documentation, and HR data. Technology diligence: IT architecture diagrams, security audit reports, and software licence agreements. A mid-market buyout data room typically contains 3,000 to 10,000 documents across these categories. The CIM, management accounts, and material contracts are consistently the highest-priority starting points, and they are also the documents where AI extraction delivers the most immediate time savings. Board minutes and regulatory correspondence are lower priority for initial review but are important sources of undisclosed risk and related-party transaction history that thorough diligence should not skip.

+

What is a Quality of Earnings report in private equity?

No. AI removes the document processing work that currently occupies a large fraction of analyst time: the reading, extracting, cross-referencing, flagging, and first-draft synthesis. It does not replace the judgment required to make investment decisions. Management assessment, deal structuring, LP governance, regulatory interpretation, and investment committee deliberation all require human judgment that AI cannot replicate. What changes with AI-assisted diligence is the ratio of reading to judgment in an analyst's working week. A significant proportion of current analyst time goes to document processing that is mechanical rather than analytical: spreading financial statements, reading and summarising contracts, checking figures against source documents. AI handles that layer. Analysts spend their time on analytical work: interrogating the outputs, validating the extractions, and applying the judgment the model cannot replicate. The most accurate framing is augmentation rather than replacement. AI handles the drudge work. The analyst handles the work that actually requires their expertise. Deal teams that position it this way, and build workflows around that division of labour, get substantially better outcomes than teams that either overautomate and lose oversight or underutilise AI and continue absorbing the document volume manually.

+

Can AI replace analysts in private equity due diligence?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.