17 min read

—

A fund close lands thirty signed convertible notes in the data room over 72 hours. Each comes from a different investor in the seed syndicate. Each carries slightly different terms — different valuation caps, different discount rates, different maturity dates. Someone on the legal or fund ops team needs to extract those terms, reconcile them against the cap table, and log the results before the LP close. Manually, that is 25 to 45 minutes per note, no audit trail, and a real chance of a transcription error that distorts every dilution model built on top of it.

This article explains the key terms AI extracts from convertible notes, where those terms appear in the document structure, and how VC teams process multiple notes in the time it once took to review one. It is a technical and operational guide for legal and fund operations professionals managing document workflows around fund closes, not a primer on investment strategy or term negotiation. For broader context on AI adoption in venture finance, see our guide to using AI in private equity and venture capital.

In this article:

Why convertible notes create disproportionate review burden at scale

The six key terms AI extracts from every convertible note, and where to find them

The five-step AI extraction workflow for a fund close portfolio

What AI automates and what still requires analyst judgement

How V7 Go handles convertible note parsing across a full portfolio

AI for document processing

Pull cap, discount, and maturity from 40 notes fast

Get started today

What Makes Convertible Notes Difficult to Review at Scale

Convertible notes look simple: eight to twenty pages, a handful of defined terms, and a conversion mechanism most associates have reviewed dozens of times. The standard NVCA form is familiar. The problem is not any single note. It is what happens when thirty of them arrive during a syndicate close on different law firm paper, each with subtly different term structures, and someone needs to reconcile all of them before the LP close window closes.

In a seed round syndicate, a fund can receive fifteen to fifty individual convertible notes. Some will use the NVCA template. Others will be on YC-adjacent forms. A handful will be on custom law firm paper that rearranges sections, renames defined terms, or buries key provisions in exhibits. The document structure familiar from the first note is not necessarily the structure found in the fifteenth. A reviewer who builds a mental model from the first document they open will apply that model to notes it was not designed for.

The reconciliation challenge compounds at scale. A fund reviewing forty notes where terms drift cannot rely on the same mental model for each document. One carries a 25 per cent discount rate, another an MFN clause, a third an unusual maturity extension provision. An AI contract review agent reads each document independently against a standardised extraction schema. A manual reviewer is working from memory and pattern recognition under time pressure, with no systematic check that their mental model fits the document in hand.

The downstream risk is material. A mislogged valuation cap distorts every dilution model built on top of it. Series A investors running AI-assisted due diligence will find the error. Cleaning up a cap table discrepancy after a priced round is in progress is far more disruptive than catching it at fund close. The "messy cap table" flag in Series A due diligence almost always traces back to a data entry problem in an earlier convertible note round, not to bad deal terms.

The Six Key Terms AI Extracts from Every Convertible Note

Most of the legal and economic risk in a convertible note portfolio concentrates in six terms. Understanding how to extract key terms from convertible notes consistently, across forty different law firms' document styles, is where AI earns its place in fund operations. Three of the six terms appear in standardised positions across most NVCA-derived templates. The other three drift in structure between law firms and require the AI to read more deeply into the document body. Here is what each term means, where to find it, and what makes it harder to extract consistently than it first appears.

Valuation Cap

The valuation cap sets the maximum company valuation at which a convertible note converts to equity. At the next priced round, if the company's pre-money valuation exceeds the cap, the note converts as though the valuation equalled the cap, giving early investors a proportionally larger ownership stake than Series A participants who paid the full price. If the cap is $8 million and the Series A pre-money is $20 million, the note converts at $8 million, not $20 million. That gap is the economic core of the instrument.

Typical range at pre-seed and seed stage: $3 million to $15 million. The extraction challenge is that the cap is usually defined as a named term in the definitions section, not on the cover page. Custom law firm templates may bury it in a definitions exhibit several pages into the document. AI reads the full document and identifies the cap regardless of where it sits in the structure, returning the value with a citation to the specific clause and page number.

Discount Rate

The discount rate gives the note holder a percentage reduction on the price per share at conversion, relative to new investors in the priced round. A 20 per cent discount means the note converts at $0.80 per share when Series A investors pay $1.00. Typical range: 10 to 25 per cent, with 20 per cent being the market standard. The discount rate is the fallback conversion mechanism when the valuation cap does not bind, for example when the company's valuation at the priced round is lower than the cap.

Phrasing varies across legal documents: "discount rate," "conversion discount," and "purchase price discount" all appear in live instruments. When both a valuation cap and a discount rate apply, the note holder receives whichever results in the lower conversion price. AI must recognise this dual-mechanism structure and flag it rather than extracting only one term. Missing it produces an incorrect picture of the investor's economic position at conversion.

Maturity Date

The maturity date is when the note is due for repayment or automatic conversion. Typical range: 18 to 36 months from issuance. In well-structured NVCA notes, the maturity date appears on the cover page. In custom forms, it may appear only as a calculated period: "18 months from the Effective Date," which requires the AI to locate the effective date before computing the absolute maturity date. Either approach produces the same result; the extraction logic must handle both.

Portfolio-level monitoring matters here. A fund managing forty convertible notes across three vintage years needs a centralised view of which notes approach maturity, not forty separate calendar entries maintained manually. For how maturity monitoring integrates into fund-level reporting, see the V7 Go LP analysis use case.

Interest Rate and Interest Accrual Method

Convertible notes carry annual interest on outstanding principal, typically 6 to 8 per cent. At conversion, interest accrual capitalises into additional shares rather than being paid in cash. The accrual method (simple versus compound) affects the final share count at conversion. Simple interest is the market standard; compound interest appears in some older or non-standard instruments and produces a higher balance at conversion than the same rate applied simply.

AI extracts both the rate and the accrual method, flagging notes where compound accrual applies. The difference becomes material at conversion: a $500,000 note at 8 per cent over 30 months produces a different share count depending on whether interest compounds annually or accrues only on the original principal. A portfolio that mixes simple and compound interest notes will produce inconsistent conversion share counts even at identical interest rates.

Qualified Financing Trigger

The qualified financing is the specific funding event that triggers automatic conversion of the note into equity. It is typically defined as a new equity round raising at least a minimum dollar threshold in a single closing, commonly $1 million to $2 million, though the threshold varies note by note across the same syndicate. The definition may also include conditions on the type of securities issued, the identity of the lead investor, or the minimum number of participants in the round.

This is one of the most important terms to standardise across a portfolio. If two notes in the same round define the qualified financing threshold differently, a priced round may trigger conversion in one note but not the other, creating a split cap table event at Series A. AI surfaces these inconsistencies before the priced round, not during it, when the window to resolve them without disrupting the close is already closed.

MFN Clause and Anti-Dilution Provisions

The MFN (Most Favoured Nation) clause entitles early note holders to adopt better terms if the company subsequently issues a note or SAFE with a lower cap or higher discount. Anti-dilution provisions protect investors if new shares are issued below the conversion price. Both clauses carry significant consequences when they appear, and both are easy to miss in a fast-moving fund close.

A human reviewer under time pressure can overlook an MFN clause buried in a miscellaneous provisions section on page fourteen. AI reads the full document on every pass. The clause is equally likely to be flagged whether it appears on page three or page seventeen. For a fund that issued notes across twelve months and subsequently closed a SAFE round at better terms, identifying which early note holders hold MFN rights is a legal obligation, not an optional audit step.

Term | Where it appears | Typical format | Extraction complexity |

|---|---|---|---|

Valuation cap | Definitions section or Section 1 | Dollar figure | Low |

Discount rate | Definitions or conversion mechanics section | Percentage | Low |

Maturity date | Cover page or Section 1 | Date | Low |

Interest rate | Cover page or recitals | Percentage | Low |

Qualified financing threshold | Definitions section | Dollar figure and criteria | Medium |

MFN clause | Miscellaneous or investor rights section | Clause reference | High |

Anti-dilution provisions | Investor rights or conversion mechanics | Clause reference | High |

Where Manual Review Breaks Down: The Fund Close Scenario

The economics of manual review work at five notes. At thirty notes, the risk profile changes entirely. At fifty notes across multiple rounds and vintage years, data entry errors move from possibility to probability.

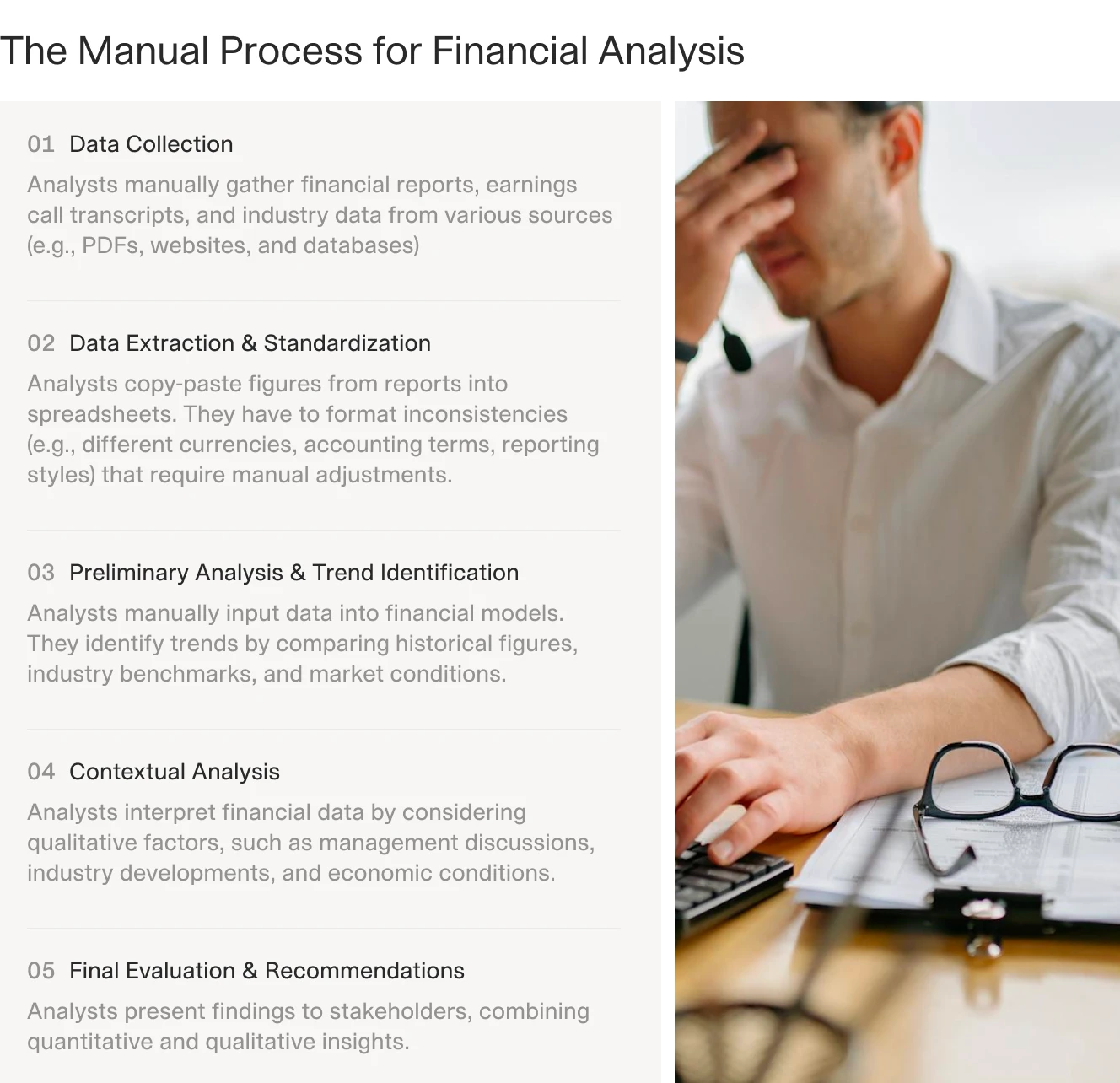

The standard VC fund close workflow looks like this: term sheet agreed, note executed, signed PDF arrives in the data room, someone logs the key terms into the cap table tool or an internal spreadsheet. The person doing the logging is often a junior analyst or a paralegal working under time pressure. They are copying numbers from a PDF into a spreadsheet, one note at a time, with no automated check that what they entered matches the source document.

The time cost is real. Each convertible note takes 20 to 45 minutes to review manually. A 40-note fund close consumes 13 to 30 hours of paralegal or analyst time. No source citations. No audit trail. No way to verify, six months later, whether the logged valuation cap matches the signed note. That is not a workflow with known risk — it is a process that holds together until it does not.

The compounding risk is structural. A reviewer who logs a valuation cap incorrectly creates an error that propagates through every dilution model built on top of that figure. Cap table tools do not validate against the source document. They trust what was entered. The error persists until a new set of counsel reviews the original instruments at Series A, at which point the close timeline is already constrained and the cost of correction is highest.

The manual financial analysis workflow: five sequential steps, each compounding the error risk of the previous one. For convertible note portfolios at fund close, the extraction and standardisation step accounts for the majority of total review time and produces no audit trail.

There is also the MFN tracking problem. A fund that issued notes over twelve months and then subsequently issued instruments with better terms needs to know which early note holders have MFN rights that entitle them to adopt those terms. If that data is not logged and monitored, the answer depends on someone remembering to check, or on Series A counsel finding it during due diligence.

How AI Parses Convertible Notes: A Five-Step Extraction Workflow

AI extraction of convertible note terms is not a keyword search against a known document position. It is a structured pipeline that classifies each document, maps its section structure, extracts terms with source citations, normalises values across the portfolio, and produces a structured output for cap table integration. The five steps below describe how that pipeline works in practice, and why each step is necessary for reliable data extraction at scale.

Step 1: Document Ingestion and Pre-Processing

The pipeline begins with the signed PDF. AI models read the full document, not just the first page or the defined terms section. For PDFs generated from a word processor, this is straightforward text extraction. For PDFs that are scanned images (common with older instruments or documents signed on paper), an Optical Character Recognition (OCR) layer runs first to produce machine-readable text. The output of this step is a clean, searchable text representation of the full document, regardless of the original PDF's quality or provenance. Consistency at ingestion is what allows all subsequent steps to operate on reliable input.

Step 2: Structural Classification

Before extracting any terms, the AI classifies the document structure. Is this an NVCA form, a YC-adjacent instrument, or a custom law firm template? Where are the sections? Where is the definitions block? Where do the conversion mechanics appear? Structural classification is what allows the extraction layer to know where to look in each specific document rather than running a search against the full text.

This is where the instinct to build a keyword-based extractor breaks down at scale. A search for "valuation cap" finds the term on a standard NVCA form. It misses a custom template that defines the same concept as "Company Valuation Ceiling" in a definitions exhibit, or buries the figure under a cross-reference to another clause. Structural classification allows the AI to identify the concept regardless of what the drafter chose to call it.

Step 3: Targeted Key Term Extraction with Source Citations

With the document structure mapped, the AI extracts each of the six key terms from its identified location. Each extracted value is returned with a source citation: the specific clause, section, and page number where the value appears in the original document. This source linkage is the audit trail that manual data extraction does not produce. Six months after a fund close, the extraction output can be reconciled directly against the original signed instrument without re-reading the document.

The extraction handles variant phrasing across legal documents. The same discount rate may be described as "a 20% discount," "a purchase price discount of twenty per cent," or a formula referencing a defined term elsewhere in the document. AI trained on a broad corpus of convertible notes handles these variants without requiring a separate rule for each phrasing pattern found in the wild.

Step 4: Cross-Note Normalisation

A portfolio of thirty notes produces thirty independent extraction results. Cross-note normalisation converts those results into a single comparison table: one row per note, one column per key term, all values in a consistent format. Dollar figures are normalised to the same currency and precision. Dates are expressed consistently. Percentages are formatted to match across notes that used different decimal conventions in their source documents.

Normalisation also surfaces the inconsistencies. Two notes with different qualified financing thresholds sit in adjacent rows of the same table. An MFN clause present in some notes but absent in others appears as a flag in the comparison. The portfolio manager sees the full picture across the fund close in a single view, not thirty separate documents reviewed in isolation across the course of a week.

Step 5: Structured Output and Downstream Integration

The final step produces the structured output: a JSON or CSV record with one entry per note and all key terms as fields, ready for import into Carta, Airtable, or any cap table tool that accepts structured data. Each record includes a reference back to the source document and the specific clause that was extracted. If a term is absent from the document, the system flags the empty field for analyst review rather than defaulting to zero. A missing value and a zero-value are not the same thing, and an extraction pipeline that conflates them produces incorrect cap table data.

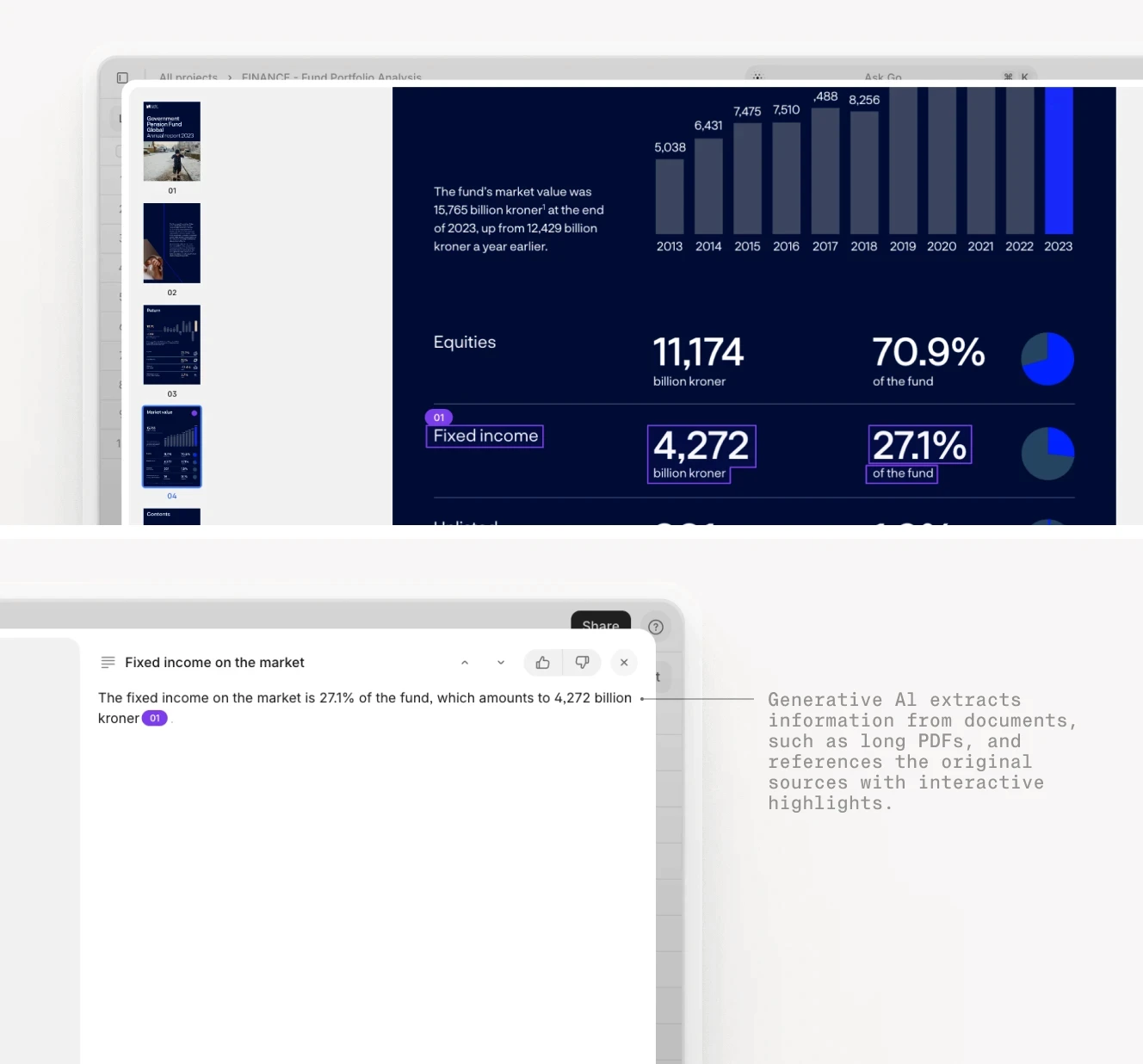

AI highlighting and extracting financial metrics from a fund document, with each extracted value linked back to its source for verification. The same principle applies to convertible note term extraction: every value in the structured output carries a citation pointing to the clause it came from.

AI Extraction vs. Analyst Review: What to Automate and What to Verify

Not every term requires the same analyst attention after extraction. Standardised terms in predictable document positions (valuation cap, discount rate, maturity date) can be accepted from AI output with a spot-check review of the source citation. Non-standard provisions and those with significant legal implications need analyst review of the specific AI finding, not a full re-read of the document. The table below maps each term type to the appropriate post-extraction action.

Term or task | AI reliability | Analyst action required |

|---|---|---|

Valuation cap extraction | High | Spot-check against source citation |

Discount rate extraction | High | Spot-check against source citation |

Maturity date extraction | High | Spot-check; verify any calculated dates |

Interest rate and accrual method | High | Flag compound accrual notes for review |

Qualified financing threshold | Medium-high | Review threshold definition and triggers |

MFN clause identification | Medium | Review identified clause and its scope |

Anti-dilution provision analysis | Medium | Full analyst review of flagged provisions |

Cross-note consistency check | High | Review flagged discrepancies |

Legal interpretation and advice | Not applicable | Always requires legal counsel |

The pattern is consistent across term types: AI handles location, extraction, and normalisation. Analyst time concentrates on reviewing AI findings for unusual provisions and interpreting those findings in the context of the fund's specific situation, rather than reading every page of every document to find the information in the first place.

How V7 Go Automates Convertible Note Parsing

V7 Go processes signed convertible note PDFs in batch, extracts all six key terms with source citations, and outputs a structured comparison table ready for cap table integration or LP reporting. The workflow runs on a single agent configured to handle any convertible note template (NVCA, YC-adjacent, or custom law firm paper) without requiring a separate configuration for each format.

The agent ingests PDFs directly from a data room folder or a batch upload. For each document, it runs the five-step pipeline described above, returning a structured record with all extracted terms and their source citations. For a 40-note fund close portfolio, the agent completes the full extraction in under an hour. Analyst review time concentrates on the flagged provisions and cross-note inconsistencies that the comparison table surfaces, not on the extraction itself.

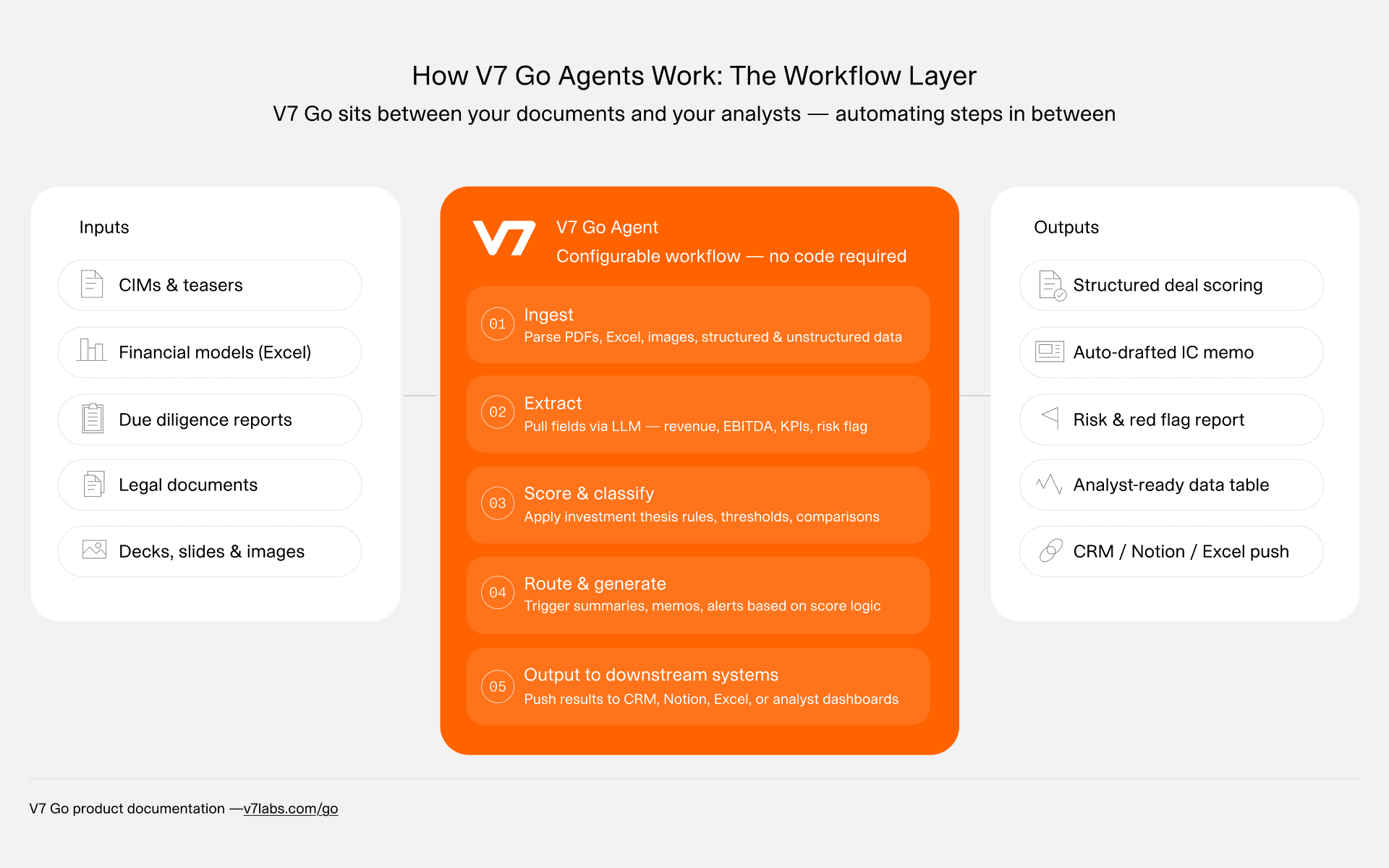

V7 Go agent architecture for document-based workflows. The same pipeline that handles CIM analysis and LP agreement review applies directly to convertible note portfolios: document inputs flow through a structured agent and produce downstream-ready structured outputs.

Every extracted value links to its source clause in the original signed document. Six months after the fund close, when a Series A data room request asks for all signed convertible note instruments and a reconciliation to the current cap table, the answer is in the extraction output rather than in someone's memory of which document they reviewed and when. The agent also supports recurring monitoring: scheduled runs flag notes approaching maturity or compare newly received notes against the portfolio-wide term distribution.

Your deal data stays private: V7 Go does not train on client documents. Enterprise deployment options include private model environments for funds with data residency requirements or existing security policies. To see how V7 Go handles convertible note portfolios end to end, visit v7labs.com/automations/convertible-note-agreements.

From Signed PDF to Structured Cap Table: What Good Looks Like

The fund close scenario at the start of this article is routine: thirty signed convertible notes, 72 hours, one fund ops team, and a close deadline. What varies is what the legal and fund operations team does with those documents after they arrive.

The manual approach produces a tracker that is probably mostly correct. The terms are logged, the cap table is updated, and the close proceeds. The error rate is low enough that most fund closes finish without incident. But "probably mostly correct" is not a foundation that survives Series A due diligence. It is not a foundation that tells you, six months later, which notes carry MFN rights that became relevant when you issued a SAFE at a lower cap. It is not a foundation that flags the three notes approaching maturity next quarter before those dates become a negotiating problem.

The AI-assisted approach produces something structurally different. Every extracted term links to its source clause in the original signed document. Every value in the comparison table is auditable. The monitoring layer flags approaching maturity dates, identifies new notes that differ from the portfolio standard on key terms, and produces output that integrates directly with your cap table tool without manual re-keying.

For VC funds managing 40 to 200 convertible notes across multiple rounds and vintage years, the operational case is clear. Data extraction that produces no audit trail is a liability embedded in every cap table and dilution model the fund relies on. AI-based data extraction at scale turns legal document review from a one-time manual event into a continuous, auditable record of every instrument in the portfolio.

To apply the same workflow to your own convertible note portfolio, explore V7 Go for convertible note analysis.

What is a valuation cap on a convertible note?

A valuation cap is the maximum company valuation at which a convertible note converts to equity. If the startup's pre-money valuation at the next priced round exceeds the cap, the note converts as though the company were worth only the cap — giving the early investor a larger ownership percentage than new investors who paid the full price. Caps typically range from $3 million to $15 million at the pre-seed and seed stage, though later seed rounds in competitive markets can see caps above $20 million. The cap is one of the most economically significant terms in the note because it directly determines the investor's ownership stake at conversion. It is typically defined as a named term in the definitions section or Section 1, not always visible on the cover page. AI extraction identifies the cap regardless of where it sits in the document structure, returning the value with a citation to the specific clause and page number where it appears.

+

How does the discount rate work on a convertible note?

The discount rate is the percentage reduction on the price per share that a convertible note holder receives at conversion, relative to the price paid by new investors in the priced round. A 20 per cent discount means the note converts at $0.80 per share when new investors pay $1.00. When both a valuation cap and a discount rate apply, the note holder receives whichever results in the lower conversion price, which is typically the more economically favourable of the two. Typical discount rates range from 10 to 25 per cent, with 20 per cent being the most common market rate. The phrasing varies across legal documents: 'discount rate,' 'conversion discount,' and 'purchase price discount' all appear in live instruments. AI systems that extract discount rates must recognise all common phrasings and flag cases where dual conversion mechanisms apply, because those carry compounded economic implications for the investor at conversion and require careful reconciliation against the cap table model.

+

What happens when a convertible note reaches its maturity date?

At maturity, a convertible note must either convert to equity, be repaid in cash, or be extended by mutual agreement. If a qualified financing has occurred before or at the maturity date, the note converts automatically. If no qualifying round has closed, the company faces three options: negotiate an extension of the maturity date, repay the outstanding principal plus accrued interest in cash, or default if neither option is viable. Maturity dates typically fall 18 to 36 months from the note's issuance date. For a VC fund holding 30 to 50 notes across multiple vintage years, monitoring maturity dates manually is operationally intensive and error-prone. AI tools that extract maturity dates from convertible note portfolios allow funds to maintain a centralised view across all notes, receive alerts as maturity dates approach, and flag notes that may require renegotiation before a priced round closes. Mismanaged maturity dates are a common source of friction in Series A due diligence, typically discovered when new counsel reviews the original instruments under time pressure.

+

What is a qualified financing in a convertible note?

A qualified financing is the specific funding event that triggers automatic conversion of a convertible note into equity. It is typically defined as a new equity round that raises at least a minimum dollar threshold in a single closing — commonly $1 million to $2 million, though the exact threshold varies between notes. The definition may also include conditions on the type of securities issued or the identity of the investors participating in the round. The qualified financing clause is one of the most important terms to extract and standardise across a portfolio, because if two notes in the same syndicate define the threshold differently, a Series A round may trigger conversion in one note but not the other, creating a split cap table event during the priced round. VC legal teams use AI extraction to surface these inconsistencies across note portfolios before the priced round closes, rather than discovering them during due diligence when the timeline pressure is highest.

+

What is the difference between a convertible note and a SAFE?

Convertible notes carry annual interest on outstanding principal, typically 6 to 8 per cent. This interest is rarely paid in cash during the life of the note. Instead, it accrues over time and capitalises at conversion — meaning it is added to the principal balance, and the combined amount converts to equity shares. The accrual method affects the final share count at conversion. Simple interest, the market standard, calculates interest only on the outstanding principal each period. Compound interest, which is less common but appears in some older or non-standard notes, calculates interest on principal plus previously accumulated interest, resulting in a higher balance at conversion and additional dilution for the company. For fund operations teams reviewing a convertible note portfolio, standardising the interest accrual method field across all notes matters for accurate cap table modelling. A portfolio with a mix of simple and compound interest notes in the same vintage will produce different share counts at conversion even at identical interest rates, which complicates dilution analysis when the priced round closes.

+

What is interest accrual on a convertible note?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.