11 min read

—

A practitioner guide to the documents, process phases, and AI automation techniques used by institutional CRE acquisition teams.

You are reviewing a proposed multi-tenant office acquisition three weeks before the scheduled close. The rent roll shows 87% occupancy. Two days into the data room, your analyst flags four leases where the stated square footage does not match the ALTA/NSPS survey. Until those leases are re-abstracted and cross-referenced against the survey, you cannot confirm whether the income figure in the offering memorandum is accurate.

That is commercial real estate due diligence at its most unforgiving: a single discrepancy across hundreds of documents can shift the underwriting materially. Institutional acquisition teams routinely process thousands of pages of title reports, environmental assessments, lease abstracts, and operating statements, all under deal-timeline pressure.

This article covers the core documents in a CRE due diligence checklist, explains how the review process is structured across deal phases, and examines where AI document extraction now fits into institutional workflows. Teams already using V7 Go's lease abstraction agent have reduced review cycles without adding headcount.

In this article:

The full CRE due diligence document checklist, organised by category

How institutional teams structure the review process across deal phases

Where AI extraction adds speed and where it does not replace legal judgement

How V7 Go automates the cross-referencing work that consumes analyst hours

AI for document processing

Automate CRE due diligence document review at scale

Get started today

The Commercial Real Estate Due Diligence Checklist

Due diligence documents in commercial real estate fall into five categories. Not every acquisition requires every item; a single-tenant industrial asset will have a shorter lease file than a 200-unit retail centre, but the categories remain consistent across property types. Missing documents are themselves information: they signal gaps that require resolution before closing.

Title and Ownership Documents

Preliminary title report. Issued by a title company, this lists all recorded encumbrances, easements, covenants, and liens against the property. The final title policy is the most important closing deliverable, but the preliminary report defines the diligence scope and identifies items requiring clearance.

ALTA/NSPS land title survey. The American Land Title Association / National Society of Professional Surveyors (ALTA/NSPS) survey maps the legal boundaries, improvements, easements, and access rights of the site. Discrepancies between the survey and the title report, or between the survey and lease premises descriptions, must be resolved before closing.

Deed and chain of title. Confirms the ownership history and identifies any breaks or disputes in the record of title.

Recorded easements and encumbrances. Utility easements, access agreements, and restrictive covenants that survive transfer and may affect the property's usability or financing terms.

Zoning certification and land use approvals. Confirms that the property's current use is legally permitted and that no outstanding violations exist. Non-conforming use status, where a property pre-dates current zoning, requires particular attention from counsel.

Existing title insurance policies. Review of prior owner policies can accelerate current-cycle underwriting and surface prior claims or exceptions not resolved in earlier transactions.

Environmental Due Diligence Documents

Phase I Environmental Site Assessment (Phase I ESA). A Phase I ESA is a desktop and site-inspection study identifying Recognised Environmental Conditions (RECs), meaning evidence or likelihood of past or present contamination, without soil or groundwater sampling. It is required by lenders and considered standard practice for any commercial acquisition.

Phase II Environmental Site Assessment. Required when a Phase I ESA identifies RECs. Involves physical sampling to quantify contamination levels and determine remediation scope and cost. A Phase II that yields a no-further-action letter from the relevant regulator substantially de-risks the acquisition.

Asbestos and lead-based paint surveys. Required for buildings constructed before 1980 in most jurisdictions. Identifies whether hazardous materials are present, in what condition, and whether abatement or ongoing management obligations apply.

Environmental remediation records and regulatory correspondence. If prior remediation has occurred, all agency correspondence, no-further-action letters, and monitoring plans should be in the data room. Incomplete remediation histories are a common deal complication.

Lease and Tenancy Documents

Lease review is typically the most labour-intensive part of a CRE acquisition. Each lease is its own negotiated contract; the income an asset actually generates depends on the precise terms of each agreement, not the summary in the offering memorandum. For a primer on how AI is changing this category of work, see our guide to AI in real estate.

Signed lease agreements and all amendments. The operative documents. Any amendment, side letter, or addendum can modify rent, term, permitted use, or termination rights. Missing amendments are among the most common data room deficiencies and frequently indicate discrepancies between the rent roll and actual lease terms.

Lease abstracts. Structured summaries of each lease's key commercial terms: base rent schedule, term, options to renew or terminate, permitted use, assignment and subletting provisions, and rent abatement periods. Abstracts should be verified against the executed leases — they are working documents, not authoritative sources.

Rent roll. A current snapshot of all tenants, occupied premises, contractual rents, lease expiration dates, and any pending rent abatements or free-rent periods. The rent roll is the primary financial summary of the asset's income; verifying it against the signed lease agreements is the core of tenancy review.

Weighted average lease term (WALT). WALT is the income-weighted average of remaining lease terms across all tenants. A high WALT indicates durable cash flow; a low WALT signals near-term re-leasing risk that should be reflected in underwriting assumptions and cap rate selection.

Common area maintenance (CAM) reconciliations. CAM is the mechanism by which tenants reimburse landlords for shared operating expenses. CAM provisions vary significantly between leases, and reconciliation records confirm whether tenants have been billed correctly and whether any disputes are outstanding or likely.

Tenant estoppel certificates. Signed by each tenant, estoppels confirm the key terms of each lease and certify that no defaults, rent credits, or side agreements exist outside the lease documents. Lenders typically require estoppels from tenants representing a threshold percentage of gross income before advancing funds.

Subordination, non-disturbance, and attornment agreements (SNDAs). SNDAs govern the relationship between tenants and any lender holding a mortgage on the property. Institutional tenants often require SNDAs as a condition of signing a new lease.

Guarantees. Personal, corporate, or letter-of-credit guarantees attached to individual leases. The enforceability of a guarantee depends on the creditworthiness of the guarantor, which should be separately verified.

Co-tenancy and exclusivity clauses. Retail leases frequently include co-tenancy rights, permitting rent reductions or early termination if an anchor tenant leaves, and exclusivity provisions, restricting the landlord from leasing to competitors of the protected tenant. These clauses can materially affect income stability and future leasing flexibility.

Financial and Operating Documents

Three to five years of audited operating statements. Actual income and expenses over multiple cycles, not pro forma projections. The spread between in-place income and underwritten income is a reliable signal of seller optimism; material differences require explanation before acceptance.

Current-year budget and variance report. Shows where actual performance is tracking against the current budget and identifies material unfavourable variances in operating expense categories that warrant follow-up.

Capital expenditure history. Documents what has been spent on capital projects over the past three to five years and what remains deferred. Deferred capital is a standard pricing negotiation lever.

Property management agreement. Fee structure, term, notice provisions, and any management company obligations that transfer to the buyer at closing.

Service and vendor contracts. HVAC maintenance, lift service, landscaping, security, and other contracts that run with the property. Contracts with unfavourable termination provisions may increase operating costs post-acquisition.

Utility bills and meter records. Confirms actual consumption patterns and identifies any utilities not separately metered or sub-metered to tenants, which represent a landlord cost exposure.

Insurance policies and claims history. Current property and liability insurance, plus any claims filed in the past three years. A pattern of repeated claims may indicate maintenance or structural issues.

Physical and Structural Documents

Property condition assessment (PCA). An independent engineer's report on the condition of the building systems and structure, typically including a ten-year capital expenditure reserve estimate. The PCA quantifies deferred maintenance and major system replacement costs.

Building plans and specifications. As-built drawings for the structure and mechanical, electrical, and plumbing systems. Required for lender underwriting and useful for estimating fit-out or repositioning costs.

Certificate of occupancy. Confirms the building is legally permitted for its current use. Missing or expired certificates can delay or prevent financing.

Outstanding permits, violations, and open inspections. Any unresolved code enforcement matters or building department violations carry over to the buyer. A title search typically captures recorded violations, but municipal databases should also be checked directly.

Lift and elevator inspection certificates. Current compliance documentation for any vertical transportation equipment, typically required annually in most jurisdictions.

Roof inspection reports. Condition assessment and estimated remaining useful life. Roof replacement is frequently the largest single capital item in a property condition assessment.

How the CRE Due Diligence Process Works

Institutional acquisition teams rarely review all document categories simultaneously. The process is typically phased to manage cost and prioritise potential deal-killers before committing to full review. For a broader view of how AI is changing due diligence across asset classes, see our article on AI due diligence.

Phase 1: Pre-LOI Preliminary Review

Before a letter of intent is submitted, the acquisition team reviews the offering memorandum, the rent roll, and any financial information provided by the seller's broker. The goal is to confirm whether the asset warrants deeper investigation and to identify obvious deal-killers: a significant environmental liability, a co-tenancy clause that could collapse the income, or title encumbrances that would prevent financing. This phase relies on broker-provided summaries and publicly available information, not a formal data room.

Phase 2: Full Data Room Review

Following an executed letter of intent and negotiated diligence access, the full data room opens. The team works systematically through each document category, assigning specialists to their areas: environmental consultants for Phase I ESA review, counsel for title and lease analysis, engineers for the property condition assessment. The rent roll is verified against signed lease agreements and discrepancies are logged as open items requiring resolution before closing. Most acquisition timelines allow 30 to 60 days for full data room review, though competitive processes compress this window considerably. A well-organised data room, structured by document category with consistent naming conventions and all amendments filed alongside the primary lease, materially accelerates this phase; disorganised data rooms add days to the timeline regardless of team capacity.

Phase 3: Exception Resolution and Price Adjustment

Diligence findings feed directly into deal negotiation. Environmental RECs may result in escrow holdbacks or seller remediation obligations. Lease document gaps, including unsigned amendments, missing estoppels, and undisclosed side letters, affect the certainty of projected income and can support price adjustments or additional representations and warranties in the purchase agreement. Capital deficiencies identified in the property condition assessment are similarly quantifiable and negotiable. The final step is confirming that all open items are resolved or addressed contractually before the due diligence period expires.

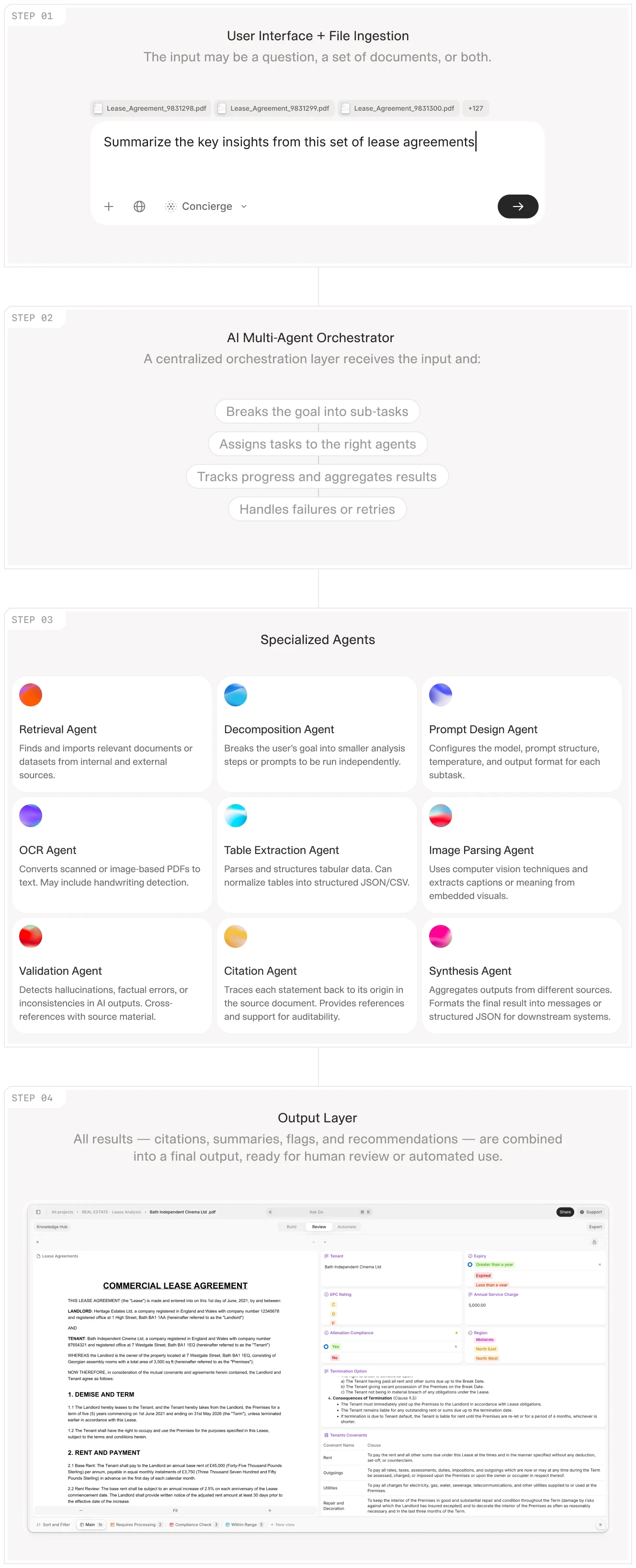

How AI Automates CRE Due Diligence Document Review

AI document extraction addresses a specific bottleneck in CRE due diligence: the time analysts spend reading, abstracting, and cross-referencing documents that follow predictable structures. Commercial leases, property condition assessments, and environmental reports share common field types (term dates, rent schedules, defined premises, identified conditions) that can be extracted systematically at scale.

What AI Extraction Produces

A configured extraction workflow takes a set of documents (signed leases, amendments, guarantees) and produces structured outputs: a table of base rent by tenant by year, a schedule of option exercise dates, a list of co-tenancy triggers and exclusivity restrictions. This is the same work an analyst performs by hand, at the speed of document processing rather than manual reading. For a 20-tenant retail property with an average lease length of 40 pages, the compression in review time is substantial.

Cross-Referencing as the More Valuable Output

Extraction alone is table stakes. The more commercially valuable capability is automated cross-referencing: confirming that what the rent roll states about each tenant matches what the executed lease actually says. Discrepancies between the two are where deal risk concentrates. An AI workflow that surfaces "Tenant C: rent roll shows $42 per square foot; lease shows $38 — verify amendment" identifies an issue that would otherwise require an analyst to trace the discrepancy manually through multiple documents.

How V7 Go Structures This in Practice

V7 Go's document review workflow processes a data room as a structured pipeline. Lease documents are extracted into a standardised field set, then cross-referenced against the rent roll and offering memorandum figures. The data room IC memo workflow consolidates findings into an investment committee memorandum format, reducing the time from data room access to internal committee presentation. For teams that need a complete extraction-to-memo pipeline, the AI real estate investment committee memo agent handles the full flow without custom development.

What AI Does Not Replace

AI extraction does not replace legal review. Identifying a co-tenancy clause is not the same as advising on whether it poses material risk to the transaction. Flagging a missing estoppel is not the same as negotiating its delivery. The value of AI in CRE due diligence is in compressing the document processing step, getting structured data out of unstructured documents quickly enough that qualified reviewers can concentrate on the decisions that require judgement rather than the reading that does not. Teams exploring this for acquisition analysis should look at V7 Go's offering memorandum analysis agent.

CRE due diligence does not become easier as deal volume increases. Each acquisition adds another data room, another set of leases to abstract, another rent roll to verify against the signed agreements. Teams that rely entirely on manual review reach a ceiling — defined by headcount and the hours available within the due diligence period.

The firms maintaining consistent review quality at higher deal volumes have typically introduced AI document extraction into their workflows. V7 Go's pre-built agents handle extraction and cross-referencing without custom configuration, allowing senior staff to concentrate on the exception resolution and negotiation work that determines deal outcomes.

For a broader view of how AI is reshaping document-intensive workflows across asset management, see our article on intelligent document processing.

What documents are required for commercial real estate due diligence?

Commercial real estate due diligence requires documents across five main categories. Title and ownership documents include the preliminary title report, ALTA/NSPS land title survey, deed, and recorded easements. Environmental documents include the Phase I Environmental Site Assessment and, where RECs are identified, a Phase II assessment. Lease and tenancy documents include all signed lease agreements and amendments, lease abstracts, the rent roll, tenant estoppel certificates, and SNDA agreements. Financial documents include three to five years of audited operating statements, the current budget, capital expenditure history, and service contracts. Physical documents include the property condition assessment, as-built drawings, certificate of occupancy, and any outstanding permit violations. The specific documents required vary by asset type: a single-tenant industrial building will require fewer lease documents than a multi-tenant retail centre. However, these five categories remain consistent across institutional CRE acquisitions regardless of asset class or geography.

+

How long is the due diligence period in a commercial real estate transaction?

The due diligence period in a commercial real estate transaction typically runs 30 to 60 days from the execution of a purchase and sale agreement, though this varies by deal type and complexity. Simple single-tenant transactions with clean title and a short lease file may close with a 21 to 30-day period. Complex multi-tenant assets or portfolios may require 60 to 90 days to allow for thorough data room review, delivery of tenant estoppels, environmental assessment, and engineering inspection. Competitive auction processes sometimes compress the due diligence window to 20 to 30 days to meet seller timelines, placing additional pressure on review teams. The length of the due diligence period is a negotiated term in the purchase agreement; buyers typically seek as long a period as market conditions allow. The period ends either when the buyer satisfies or waives all contingencies, or when a hard deadline triggers a default or deal termination.

+

What is the typical due diligence period for commercial real estate?

The typical due diligence period for commercial real estate is 30 to 60 days, with 45 days as a common market standard for mid-complexity acquisitions. The appropriate length depends on the asset type, the data room quality, and whether specialist reports such as Phase I environmental assessments and property condition assessments can be ordered and received within the agreed window. Off-market transactions negotiated directly between buyer and seller often allow for longer periods, since there is no competing bidder pressure. Lender requirements can also extend the effective diligence window, particularly when bridge financing or agency lending requires its own underwriting and appraisal process. Teams that use AI document extraction for lease abstraction and rent roll verification can meaningfully compress the time spent on document review within a fixed period, allowing more time for legal review and exception resolution before the deadline expires.

+

What happens after the due diligence period ends?

When the due diligence period ends, the buyer either proceeds to closing or exercises a contractual right to terminate the purchase agreement. If the buyer is proceeding, all diligence contingencies are waived and the deposit typically becomes non-refundable. The final steps before closing include delivery of outstanding tenant estoppel certificates, resolution of any title exceptions, satisfaction of lender underwriting conditions, and preparation of closing documents. If the due diligence period reveals material issues that cannot be resolved through negotiation, the buyer may attempt to renegotiate the purchase price, request seller credits for identified deficiencies, or terminate the agreement and recover their deposit if the contract permits. In some transactions, outstanding diligence items are addressed through escrow holdbacks or post-closing obligations rather than causing a delay. Items discovered after the due diligence period ends are generally the buyer's responsibility.

+

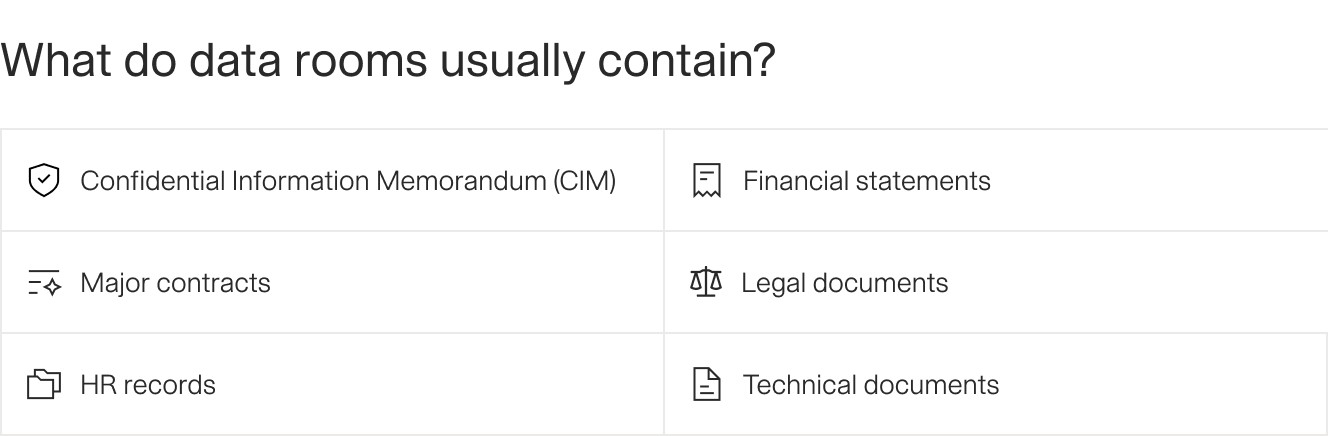

What is a data room in commercial real estate due diligence?

AI automates commercial real estate due diligence primarily through document extraction and cross-referencing. Extraction workflows process lease agreements, rent rolls, environmental reports, and operating statements, pulling structured data fields (base rent, lease term, WALT, CAM provisions, option exercise dates) into a standardised output format. Cross-referencing then compares extracted data across documents automatically, flagging discrepancies — where the rent roll reports a different rent figure than the executed lease, or where the ALTA survey boundary differs from the premises description in a tenancy agreement. These are the tasks that consume the most analyst time in a traditional manual review. AI does not replace legal review or judgement on material risks. It reduces the time spent on document reading and data organisation, compressing the period between data room access and substantive exception review. V7 Go offers pre-built agents for lease abstraction, rent roll verification, and investment committee memo generation that institutional teams can deploy without custom engineering.

+

How can AI automate commercial real estate due diligence?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.