19 min read

—

The CIM arrives on a Thursday afternoon. It is 120 pages. Your IOI is due Monday morning. Somewhere inside a confidential information memorandum written by the company's own advisors to present the business at its absolute best, you need to find the information your investment committee actually cares about: what you are paying, why it is worth it, and what could go wrong.

That is the central problem with CIM private equity work. The document is not designed for you. It is designed to get you to bid.

The CIM-to-IC memo is one of the most time-intensive tasks in a deal team's workflow. A mid-market firm reviewing 80 to 100 CIMs per year (and closing one deal) cannot afford to spend 13 to 18 analyst hours on each review. Most firms don't. They skim, flag the obvious red flags, and move on. That means the average CIM review covers perhaps 20 to 30 percent of the document. The sections that don't make it into the initial scan can include the ones that matter most.

AI does not make this problem disappear. But it changes the economics fundamentally, if implemented correctly. The difference between an AI tool that produces a fast wrong answer and one that produces an auditable right answer comes down to how the workflow is structured, not which model sits underneath it.

This guide covers the complete picture: what a CIM actually contains and why it doesn't map directly to what the IC memo requires; how to build the section-by-section translation; where the manual process breaks down at volume; and how a properly structured AI workflow handles the extraction, synthesis, and flagging that takes an analyst the better part of two days.

In this article:

The structural difference between a CIM and an IC memo: why you can't just summarize one into the other

A section-by-section mapping from CIM to IC memo, with what the analyst must add at each step

Where the manual workflow fails at deal volume — and what that costs

How a structured AI workflow handles the CIM-to-memo process end to end, with source-grounded extraction and management projection flagging

AI for document processing

Extract CIM data into your IC memo automatically

Get started today

What a CIM actually contains : what the IC memo requires

A CIM is a sell-side document. Every line in it was written, reviewed, and approved by someone whose job is to make the business look as attractive as possible to potential buyers. That is not a criticism—it is the document's purpose. The banker's job is to run a competitive process and maximize value for the seller. The CIM is the opening argument.

An IC memo is a buy-side document. It goes to your investment committee to support a decision: proceed, pass, or proceed with conditions. Its purpose is the opposite of the CIM's. It must interrogate, challenge, and pressure-test what the seller's document presents. Where the CIM emphasizes market opportunity, the IC memo quantifies competitive intensity. Where the CIM shows management projections, the IC memo shows your own base case, upside, and downside scenarios. Where the CIM describes risk factors in the most favorable light available, the IC memo identifies the ones that could actually kill the deal or the return.

The document you receive and the document you must produce are philosophically opposed. That gap is where analyst hours go.

A standard mid-market CIM typically covers eight or nine sections: a business overview, the market opportunity, management team biographies, historical financial performance, projected financials (the management case), growth strategy, risk factors, and transaction overview. Some add detail on operations, customer concentration, or technology infrastructure. The total length runs from 80 to 150 pages for established businesses, longer for complex situations with multiple segments or international operations.

The IC memo that comes out the other side is typically 5 to 20 pages, depending on your firm's template. But the compression is misleading. The memo does not summarize the CIM. It evaluates it. That evaluation requires information that is not in the CIM at all: your own IRR analysis, your market data, your views on management credibility, your comparable transactions, your assessment of which growth levers are credible and which are aspirational.

You can read more about the mechanics of CIM review in deal screening workflows. The core point for this article is that the CIM-to-IC memo process is not a summarization task. It is a translation and synthesis task. The analyst must read, extract, challenge, supplement, and structure. AI that treats this as a single-step summarization will produce something that looks like an IC memo and reads like a CIM.

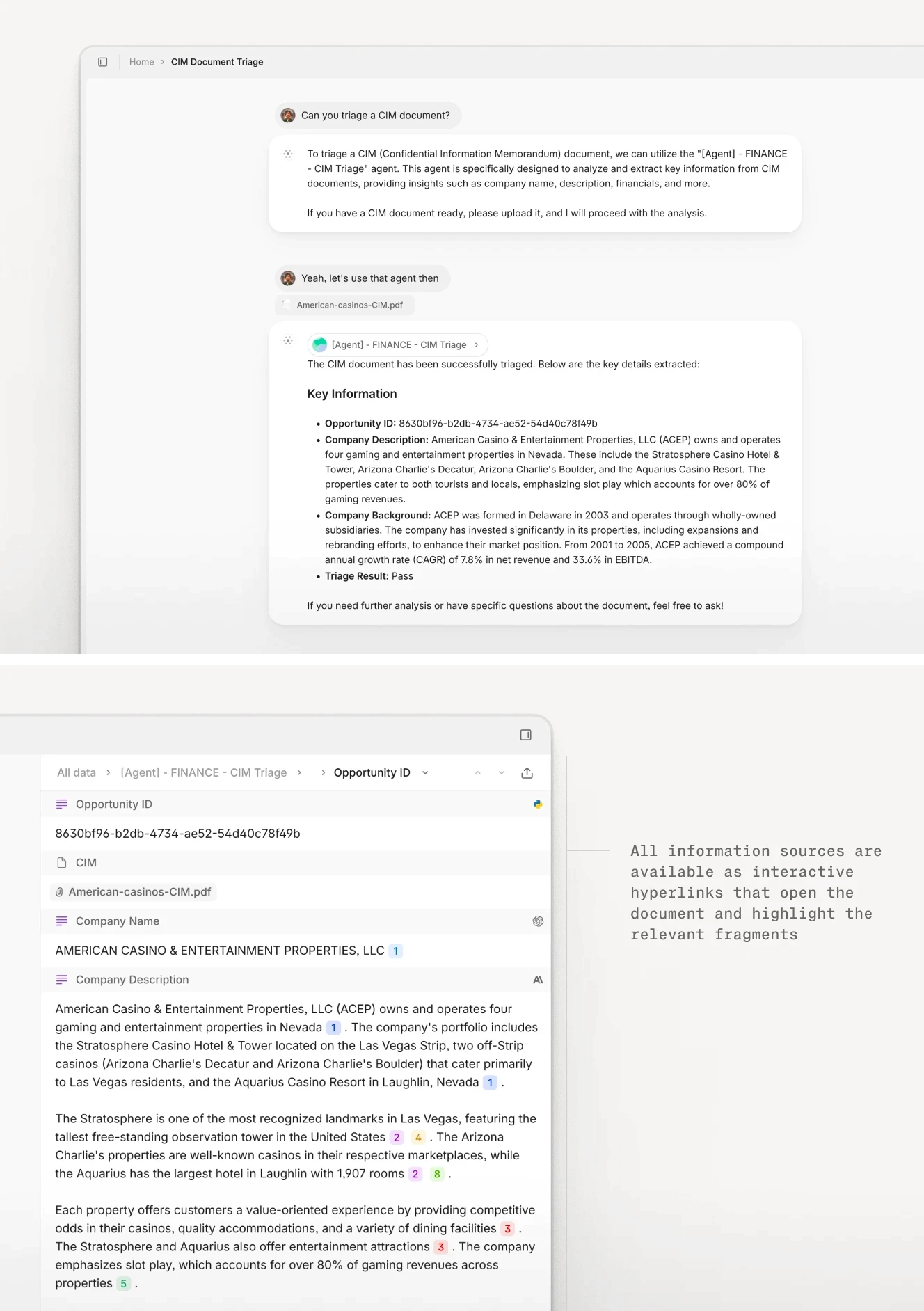

A structured AI triage of a CIM extracts the critical fields an analyst needs to form an initial view, not a summary of what the document says, but an evaluation of whether it passes screening criteria.

The CIM section mapping: how each section feeds the IC memo

The gap between the CIM and the IC memo is navigable if you treat it as a structured translation rather than a linear read-and-write. Each section of a CIM has a corresponding section in the IC memo; the correspondence is never one-to-one. The analyst must bridge the gap between what the CIM provides and what the IC memo requires.

The table below maps the standard CIM sections to their IC memo counterparts, with a column for what the analyst must add at each step.

CIM section | What it argues | IC memo section | What the analyst must add |

|---|---|---|---|

Executive summary | Best-case framing of the business | Investment thesis | Your firm's conviction and fit against fund criteria |

Market opportunity | Large TAM, favorable dynamics | Market analysis | Competitive intensity, disruption risk, structural durability |

Historical financials | Revenue, EBITDA on management's basis | Financial analysis | Quality of earnings flags, adjustments, recurring vs. non-recurring |

Management projections | Optimistic base case | LBO / returns model | Your own base, upside, downside; entry multiple and IRR scenarios |

Management team | Credentialed, experienced leaders | Management assessment | Key person risk, succession, track record against prior projections |

Growth strategy | Organic and M&A growth levers | Value creation plan | Which levers are credible, which require assumptions you wouldn't make |

Risk factors | Risks presented as managed or minimal | Key risks | Material risks the CIM underplayed or omitted |

Each row in that table represents a specific analyst task. But the tasks are not equal in complexity or time required. Three sections account for the majority of the work and are the most important to get right.

From executive summary to investment thesis

The CIM's executive summary is the seller's lede. It leads with the business's best attributes: strong revenue growth, expanding margins, defensible market position, a management team with a track record. It is written to generate interest, not to inform an investment decision.

The investment thesis in the IC memo is a different document entirely. It has to answer your IC's actual questions: why this business, why now, why at this price, why us. It has to explain how the investment fits your fund's strategy and return profile. It has to state the core conviction: the one insight about the business that the market has not fully priced in.

The CIM gives you the raw material. The thesis is the analyst's judgment. AI can extract the executive summary, identify the key claims, flag which ones are supported by the financial data and which are not. The judgment about whether those claims add up to a compelling thesis belongs to the investor.

From historical financials to financial analysis

This is where the most common errors occur in both manual and AI-assisted workflows.

The CIM's financial section presents historical financials on a management basis. That often means adjusted EBITDA with add-backs that may or may not survive due diligence scrutiny. Revenue recognition policies may differ from how you model the business. One-time items may have a suspicious tendency to recur. Customer concentration and churn data may be buried in footnotes or absent entirely.

The IC memo's financial analysis must reconstruct what the actual financials look like on your basis: removing add-backs you don't accept, normalizing for one-time items, stress-testing the revenue growth rate against your market view. It must identify the quality of earnings questions that will drive the QoE workstream in due diligence.

That reconstruction requires reading the financial statements in the CIM closely, cross-referencing footnotes against the main tables, and applying your own judgment about which adjustments are credible. It is the section that takes the most analyst time and carries the most risk if shortcuts are taken.

From risk factors to material investment risks

No CIM has ever described its own risk factors as disqualifying. The risk section exists because buyers expect one, and because advisors have learned to present risks in the most favorable frame available. Customer concentration is "a diverse customer base with top clients representing 35% of revenue." Key person risk is "a founder-led business with a strong management team being developed." Technology disruption is "an industry that has historically been resilient to technological change."

The IC memo's risk section must call the question: is the customer concentration a genuine issue, and if it is, how does it affect the returns scenario? Is the management team actually ready to operate without the founder, or does that assumption require a new hire during the hold period? What does the technology disruption look like if a well-capitalized competitor enters in year three?

The analyst must read the CIM's risk language, identify where the framing is doing more work than the substance, and restate the risk in plain terms that the IC can evaluate. This is not a task that AI handles well without structure; structured AI can flag the gap between what the CIM says and what the financial data supports.

A structured CIM extraction workflow breaks the document into discrete sections: financials, key people, customer data, revenue breakdown, rather than producing a single unstructured summary.

Where the manual CIM-to-IC memo workflow breaks down

A careful, thorough CIM review and IC memo draft takes a senior associate 13 to 18 hours. That is the realistic estimate when the analyst is reading the full document, cross-referencing the financials, writing out the sections, and getting the memo to a state where a VP can review it without extensive revision.

Most of the time, that is not what happens.

At the volume mid-market funds operate (80 to 100 CIMs reviewed per closed deal, according to Sutton Place Strategies' 2024 Deal Origination Benchmark Report; a full 13-hour review of every CIM is not economically feasible. The math is simple: 100 CIMs at 13 hours each is 1,300 analyst hours per deal. Against a deal team of three associates, that is more than a year of full-time work for every deal you close. Firms compress the review. They skip sections. They rely on the executive summary. They triage on three or four headline metrics.

That compression has consequences. The financial section that was skimmed might contain the adjustment that changes your EBITDA basis by 20 percent. The risk factors section that was summarized in a paragraph might contain a customer concentration issue that surfaces in QoE and kills the deal six weeks later. The growth strategy that looked credible at a high level might, on close reading, depend entirely on an international expansion the company has never actually attempted.

The pipeline-to-close rate is declining. At 24 percent and falling (again per Sutton Place Strategies), the average fund is looking at more CIMs per close, not fewer. The review burden grows without a corresponding increase in deal team headcount. Something gives, and it is usually coverage depth.

The answer most firms have tried first is better templates and checklists. Build a standard CIM triage model, train associates to use it, review for consistency. This helps at the margin. It does not change the hours-per-document equation. A 120-page CIM does not get meaningfully shorter because your template is better.

The CIM to screening memo workflow is the point in the deal pipeline where AI has the clearest and most immediate impact — not because AI makes better judgments, but because it can do the coverage work that human teams cannot afford to do at volume.

How AI automates the CIM-to-investment memo workflow

The common failure mode is to treat a CIM as input for a single summarization prompt. You upload the PDF, ask the AI to produce an IC memo, and get back something that looks right on first read: organized, coherent, covering the main sections. Then you look at the financial tables and notice that the revenue figure is wrong by $40 million. Or you ask where the EBITDA margin figure came from and the AI cannot tell you. Or the risk section reads like a restatement of the CIM's own risk language rather than an independent assessment.

Single-prompt AI produces a fast output at low accuracy. It is not a workflow. It is an autocomplete for documents.

A structured AI workflow is a different thing. It breaks the CIM-to-memo task into a sequence of discrete steps, each with a defined input, a defined output, and a defined method. Each step is verifiable. Each output traces back to a source.

Ingest and parse

The first step is document ingestion: converting the CIM PDF into a parsed, structured representation that the AI can work with accurately. This is not just text extraction. A CIM contains tables, footnotes, charts, and financial statements that are formatted for human reading, not machine parsing. A chart showing revenue by year may carry more information than the prose paragraph describing it. A footnote two pages from the table it qualifies may change the interpretation of the entire row.

Accurate ingest requires document understanding: the ability to maintain the relationship between tables, footnotes, and text across a document that may run to 150 pages. The quality of everything downstream depends on this step. Bad parsing produces bad extractions regardless of how good the model is.

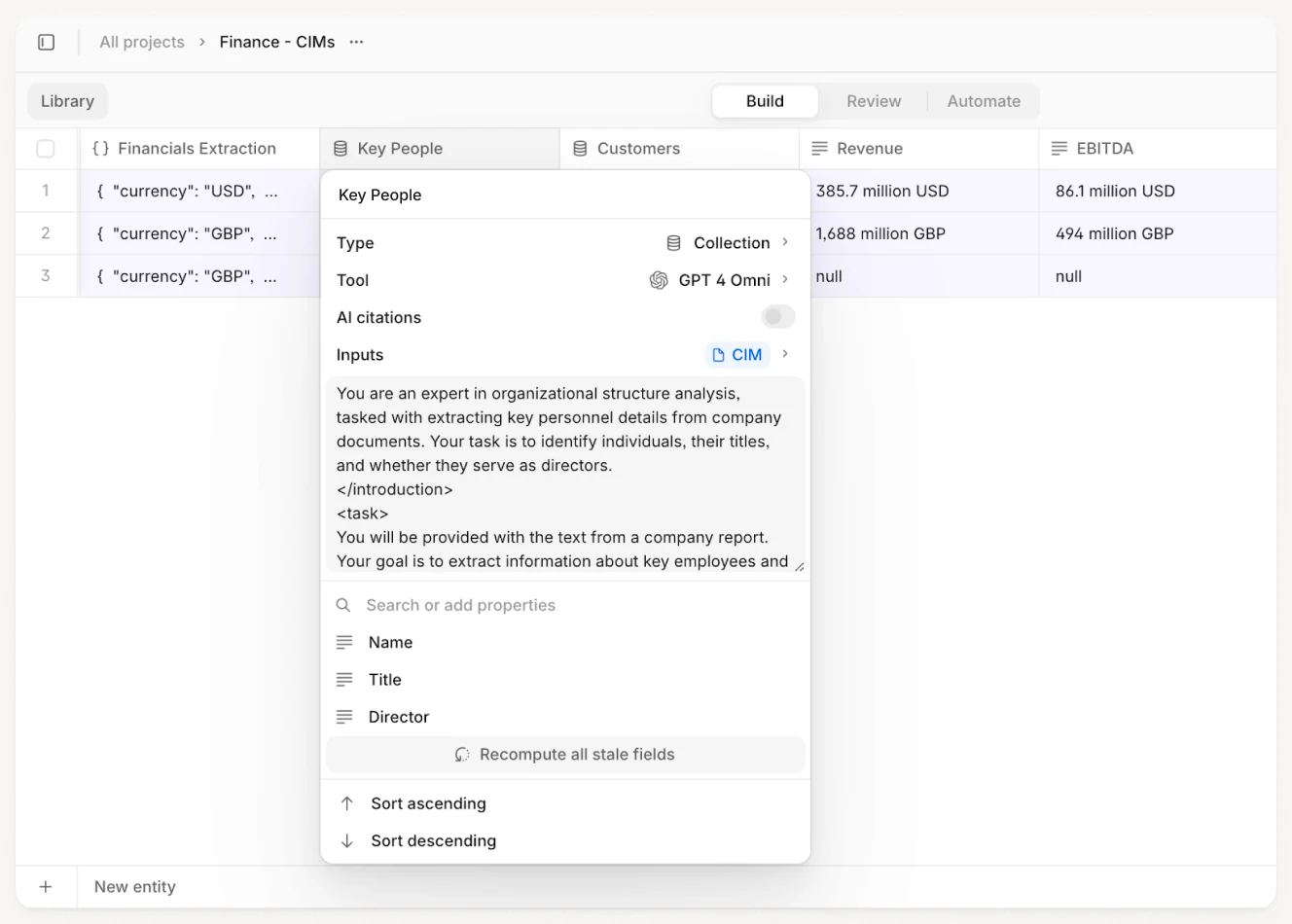

Extract structured data

The second step is extraction: pulling specific data points from the parsed document into a structured schema. For a CIM-to-IC memo workflow, the extraction schema maps to the memo template: revenue and EBITDA (on the CIM's stated basis), management projection assumptions, customer concentration data, key personnel, growth strategy claims, and risk factor language.

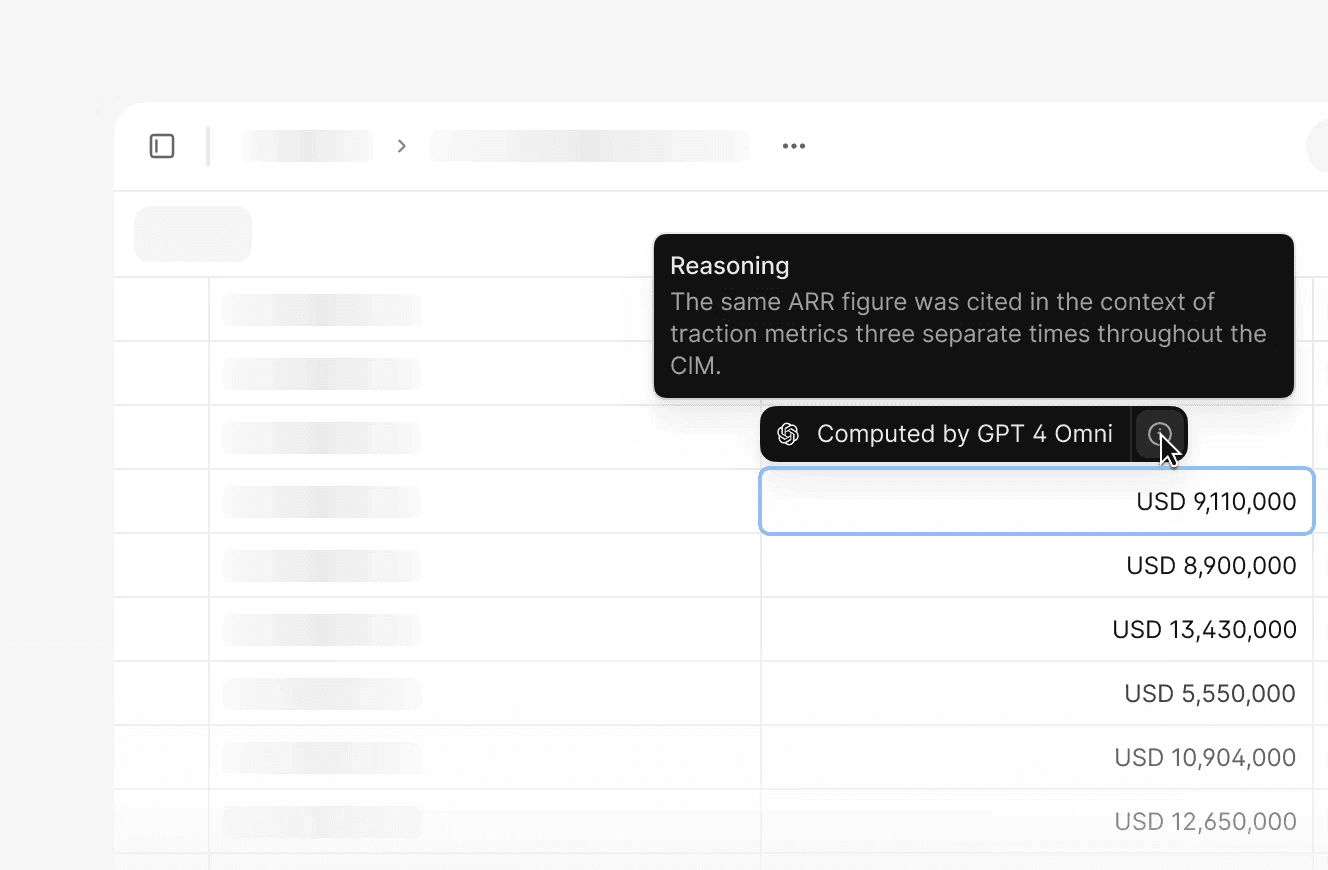

Each extracted data point must carry a source citation: which page, which table, which cell. Not because the AI might be wrong, though it might be, but because your IC will ask. "Where does this EBITDA figure come from?" is not an unanswerable question. It should take three seconds, not thirty minutes of re-reading the document.

This is also the step where AI consistently outperforms the manual process on coverage. A human analyst doing a timed CIM triage extracts perhaps 30 to 40 data points in two hours. A structured extraction workflow runs against the full document and produces 70 to 80 data points (with citations) in minutes. The coverage difference is not marginal. It is the difference between reading the document and skimming it.

Map to IC memo structure

Extraction gets the data out of the CIM. Mapping translates it into the structure your memo requires. This is where the section table from earlier becomes operationally useful: the AI needs explicit instructions about which CIM sections feed which IC memo sections, and what transformations apply at each step.

For the financial section, that means flagging the gap between the management EBITDA basis and a clean EBITDA basis, noting which add-backs appear and whether they are common or unusual. For the risk section, that means identifying where the CIM's stated risk language is contradicted by the financial data. Customer concentration risk described as "managed" deserves a flag if the top three customers represent 60 percent of revenue and that figure is buried in an appendix.

This mapping step cannot be done by a single prompt. It requires the AI to hold the CIM's content, the memo's structure, and the firm's own analytical standards in context simultaneously. This is precisely the kind of task that breaks down when you try to do it in one step.

Draft and structure

The draft step produces the prose that becomes the IC memo. This is the step people assume is the hard one for AI. In practice, it is the easy one. LLMs write fluent, structured prose. The challenge was always getting the underlying analysis right: the extraction, the mapping, the flagging. Once those outputs are accurate and source-grounded, drafting the memo sections is a relatively tractable task.

What matters is that the draft preserves source citations. Every claim in the memo should carry a reference to the underlying extraction, which in turn references the CIM page and table. The memo is a synthesis, but it should be a transparent one.

Review and flag

The final step in an AI-assisted workflow is not publication; it is review enablement. The AI's job is to produce an output that makes the analyst's review faster and more focused, not to eliminate the analyst. The output should flag: data points where the extraction was uncertain (ambiguous tables, conflicting figures), management projection assumptions that diverge significantly from industry benchmarks, and gaps where the CIM did not provide the information the memo template requires.

A well-structured workflow makes the reviewer's job clear: here are the 77 data points we extracted, here are the 8 that need your judgment, here are the 3 gaps you will need to fill from your own analysis or data room. That is a two-hour review task. The alternative is a two-day task: reading the full document and building the memo from scratch.

Source-linked extraction connects every output data point back to the specific passage in the source document. This is not optional for PE deal work: it is the baseline requirement for auditability.

The accuracy problem in PE deal work

Speed is the wrong thing to optimize for.

The V7 Go team tested single-prompt CIM extraction against a structured multi-step workflow on the same document. Single-prompt output: 35 data points, 37 percent correct, with a revenue figure off by $386 million. The structured workflow output: 77 data points, all source-auditable, with citations back to exact tables and pages in the source document. The single-prompt version was fast. It was also wrong in a way that would have been consequential at the point where it mattered most.

A $386 million revenue error does not stay inside the document. It flows into every downstream calculation: EBITDA multiples, LBO entry assumptions, returns projections. An IC memo built on a wrong revenue figure produces wrong recommendations.

The accuracy requirement has two components that are distinct. The first is extraction accuracy: did the AI pull the right number from the right place? The second is source traceability: can you verify that it did? A workflow that produces accurate extractions without source citations is difficult to trust. An analyst (or an IC member) cannot verify an AI output without knowing where it came from. That is not a philosophical point about AI trust. It is a practical workflow requirement.

There is a third component that is specific to CIM work: management projection handling. CIM financials are presented on a management basis. The AI must be configured to recognize that management projections are not historical fact: they are the seller's view of the future, and they should be extracted and labeled as such, not silently used as the basis for your returns analysis. A workflow that does not flag this distinction will produce an IC memo that presents the company's own optimistic assumptions as if they were analyst estimates.

Flagging management projections separately, and prompting the analyst to apply their own growth rate, margin, and terminal value assumptions, is one of the structural features that distinguishes a PE-grade workflow from a generic document summarization tool.

Source-grounded extraction shows the output value alongside the specific references in the CIM that support it. A PE analyst can verify the extraction in seconds rather than re-reading the document to find the source.

How V7 Go handles the CIM-to-IC memo workflow for PE teams

The dataroom-to-IC memo workflow in V7 Go is structured as a multi-step agent pipeline rather than a single extraction prompt. Documents are ingested through the platform's document parsing layer, which handles PDFs including financial tables, charts, and footnotes. Extraction runs against a configured schema: EBITDA, revenue, growth assumptions, customer concentration, management team, risk factors, with each output carrying a citation to the source page and table in the original CIM.

The AI due diligence agent can process the CIM alongside supporting documents: management presentations, historical financials, data room materials, and synthesize across sources rather than treating each document in isolation. When the financial statements in the data room contradict the EBITDA figure stated in the CIM, the workflow flags the discrepancy rather than silently choosing one or the other.

Each deal that goes through the platform feeds V7 Go's Context Graph: a persistent knowledge layer that stores the firm's view of every business evaluated, every sector analyzed, every investment considered. When a new CIM arrives in a sector the firm has reviewed before, the workflow can surface prior passes: what you looked at, what you concluded, which assumptions proved wrong. That institutional memory does not walk out the door when an analyst leaves. It compounds with every document the team processes.

The practical output is an IC memo draft structured to your firm's template, with extraction citations throughout, management projection sections clearly labeled, risk flags for gaps between the CIM's stated position and the underlying financial data, and a review checklist that tells the analyst exactly which judgments still belong to them.

V7 Go processes the full CIM in discrete stages: ingest, extraction, section mapping, and draft generation, with source citations at every step so the analyst review is targeted, not exploratory.

The AI investment analysis agent extends the same workflow to the screening phase: before a full CIM review, it produces a structured triage output that answers the first three questions an investment team asks when a CIM lands in the inbox. Does it fit our mandate? Does the headline financial profile pass our screening criteria? What are the two or three questions this CIM raises that we would need answered before taking it further?

Deal teams using this workflow typically handle the full CIM-to-IC memo process in two to three hours of analyst time rather than thirteen to eighteen. The hours saved are not the point. The coverage improvement is. A team that can review every CIM at full depth, rather than skimming 80 percent of the document and reading 20 percent carefully, catching things that get missed at volume. The risk factor buried in page 94. The revenue recognition policy in the footnotes. The customer that accounts for 40 percent of revenue and whose contract renews in eighteen months.

What changes on Monday morning

Start with a single deal. The CIM arrives Thursday. Under the manual workflow, an associate spends the better part of Friday and the weekend building the triage memo. By Monday, you have a memo that covers the sections the analyst had time to read carefully (probably the executive summary, the financials at a high level, and the management team).

Under an AI-assisted workflow, the extraction runs in the first hour. The analyst has a structured draft with 77 sourced data points, flagged management projection assumptions, and a list of eight decisions that require judgment before the memo is ready. The analyst spends Friday afternoon on those eight decisions. The draft that goes to the VP on Monday is more complete and more auditable than anything that could have been produced manually in the same time.

Now multiply that across a year. A mid-market fund reviewing 80 CIMs per deal closed, with each review saving ten hours of analyst time, recovers 800 hours per deal cycle. That is five months of full-time analyst capacity, redirected from document extraction and first-draft writing to the judgment-intensive work that actually differentiates investment decisions.

The firms that get this right are not using AI to go faster. They are using AI to go deeper. They are reviewing the full document rather than the first 30 pages. They are building IC memos that reflect the actual analysis rather than the analysis that was possible in 48 hours. They are catching the things that slow deals down or kill them in QoE: not because they are smarter, but because their workflow gives them coverage that was not economically available before.

The CIM will still be 120 pages. The IOI deadline will still be Monday morning. What changes is what you are able to do in between, and how much of it comes back to the analyst's judgment rather than their endurance.

If you want to see how V7 Go handles this workflow in practice, the data room analysis agent and the virtual data room AI guide cover the full due diligence context beyond the initial CIM review.

What is a CIM in private equity?

A Confidential Information Memorandum (CIM) is the primary marketing document a company's investment bank produces when running a sale process. In private equity, the CIM is the first substantive document a potential buyer receives after signing an NDA. It typically runs 80 to 150 pages and covers the business overview, market opportunity, management team, historical financial performance, management projections, and the proposed transaction structure. The CIM is a sell-side document written to present the business at its most attractive. Every section is designed to generate competitive interest and support a high valuation. For PE deal teams, the CIM is the raw material for the IC memo, but because its perspective is the seller's, the buyer must read it critically, identifying what the data actually supports versus what the framing implies.

+

How long does a CIM review take in private equity?

A thorough manual CIM review and IC memo draft takes a senior associate 13 to 18 hours. That estimate assumes reading the full document, cross-referencing the financial tables and footnotes, writing all IC memo sections, and producing a draft that a VP can review without major revision. In practice, most firms cannot sustain that time allocation at volume. A mid-market fund reviewing 80 to 100 CIMs per deal closed faces a straightforward math problem: 100 CIMs at 13 hours each is 1,300 analyst hours. Deal teams compress the review, covering 20 to 30 percent of the document in depth and relying on the executive summary for the rest. Structured AI-assisted workflows can complete the same extraction and drafting in two to three analyst hours, with fuller document coverage than the manual approach provides at volume.

+

What is the difference between a CIM and an IC memo?

A CIM is a sell-side marketing document produced by the target company's investment bank to present the business to potential buyers. An IC memo (Investment Committee memorandum) is a buy-side analytical document produced by the PE firm to support an investment committee decision. The two documents have opposite purposes. The CIM is designed to generate interest and justify a high valuation. The IC memo is designed to interrogate the same business and surface the risks that could affect the deal or the return. The CIM presents management projections as the financial story. The IC memo evaluates those projections against the firm's own base, upside, and downside scenarios. Converting one into the other is not a summarization task. It is a translation and synthesis task that requires extracting data from the CIM, supplementing it with external analysis, and reframing every claim in terms of what it means for the investment decision.

+

How does AI improve the CIM review process for PE teams?

AI improves CIM review by handling the extraction and structured drafting steps that account for most of the analyst time in a manual workflow. A structured AI workflow ingests the CIM, parses tables and footnotes accurately, extracts 70 to 80 data points with citations back to the source page and table, and maps those data points to the IC memo template. The result is an AI-drafted memo with sourced references that the analyst reviews and completes rather than builds from scratch. The improvement is not only speed: coverage depth increases significantly. A human analyst doing timed CIM triage extracts 30 to 40 data points in two hours and reads perhaps 20 to 30 percent of the document carefully. A structured AI workflow covers the full document, flagging customer concentration buried in appendix tables, revenue recognition policies in footnotes, and management projection assumptions that diverge from market benchmarks. These are the items that get missed at volume.

+

What makes a PE-grade CIM workflow different from generic document AI?

AI can produce a complete first draft of the IC memo, but the draft requires analyst input before it is IC-ready. The AI handles extraction, mapping, and structured drafting: the work that accounts for roughly 80 percent of the analyst hours in a manual workflow. What remains is the judgment layer: the investment thesis (why this business, why now, why at this price, why your fund), the analyst's own financial scenarios (base, upside, downside), the assessment of management credibility, and the determination of which risks are material versus manageable. These judgments cannot be automated because they require the investor's own market knowledge, fund criteria, and conviction. A well-structured AI workflow makes the judgment layer explicit: here are the extractions, here are the gaps, here are the decisions that belong to you. That is a two-hour analyst task rather than a two-day task, but it is still an analyst task.

+

Can AI produce the complete IC memo, or does it still require analyst input?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.