20 min read

—

Insurance regulators don't change the rules every week. But the documents proving you comply with them keep multiplying.

The NAIC coordinates 56 state insurance regulators, each of which can issue bulletins, adopt model laws on their own timeline, and revise filing requirements for forms already in circulation. A commercial insurer managing 150 program forms across 30 states doesn't face a compliance knowledge problem. The compliance officers understand what's required. The legal team can interpret new guidance. The problem is operational: hundreds of policy wordings, endorsement stacks, regulatory circulars, and audit evidence packages that someone has to read, compare against reference versions, and verify for currency continuously, not once at policy inception.

Manual document review doesn't scale to that volume. A compliance analyst reviewing policy forms for regulatory accuracy processes roughly 8 to 12 complex policies per day. A missed deviation in boilerplate exclusion language doesn't surface until a market conduct exam. Market conduct exams pull files from the past three years. By the time the finding arrives, the same gap has repeated across dozens of renewals.

The consequences are not theoretical. A regulatory fine for a missed mandatory form filing can reach six figures. A pattern finding in a market conduct exam can trigger a consent order restricting a line of business. A data handling gap discovered during a breach investigation can produce costs (legal, remediation, reputational) that dwarf the review process that would have caught it.

AI document review doesn't change what insurance compliance requires. It removes the extraction, comparison, and flagging work that currently prevents compliance reviewers from applying judgment at scale. This article explains what that looks like in practice, what to look for in a compliance automation tool, and how the technology is being deployed in insurance operations today.

In this article:

What insurance compliance involves and why document review is its central operational challenge

The five core regulatory requirements and the document types each one generates

Why the compliance document bottleneck is structural, not a staffing problem

How AI agents handle policy wording review, endorsement tracking, regulatory change monitoring, and audit readiness

What separates compliance automation tools that work in regulated industries from those that don't

AI for document processing

Automate compliance document review across every policy

Get started today

What is insurance compliance?

Insurance compliance is not a single obligation. It's a continuous intersection of state licensing requirements, financial solvency mandates, data privacy regulations, anti-money laundering obligations, and, increasingly, AI governance frameworks. For an insurer operating across 30 states, that intersection generates thousands of regulatory touchpoints per year. For an MGA building a program for a Lloyd's syndicate, it generates them across jurisdictions that share no common regulatory floor.

The core of regulatory compliance in insurance is not difficult to define: maintain appropriate licenses, honor filed policy terms, report financial conditions accurately, protect policyholder data, and apply consistent underwriting criteria. What's difficult is proving it, continuously, across every policy in force, every document in the file, and every regulatory update as it arrives. Proof requires documents. Documents require review. Review at scale requires either a very large compliance team or a more efficient process.

Most insurers have neither enough reviewers nor a more efficient process. They have a compliance framework that works in theory and a document review operation that falls short in practice. Not because the framework is wrong, but because the volume of documents required to prove compliance has grown faster than the teams reviewing them.

Compliance ownership spans multiple functions. Compliance officers set the framework and monitor for gaps. Legal counsel interprets new regulatory guidance and advises on material changes. Actuaries certify financial ratios and reserve adequacy. Underwriting teams execute within approved guidelines, applying criteria that have to match filed forms. Claims handlers process losses under policy terms that someone has to verify are still current and consistent with the approved wording. When one of those handoffs breaks down, usually because a document didn't get reviewed. The result is a regulatory finding that traces back to a process failure, not a knowledge failure.

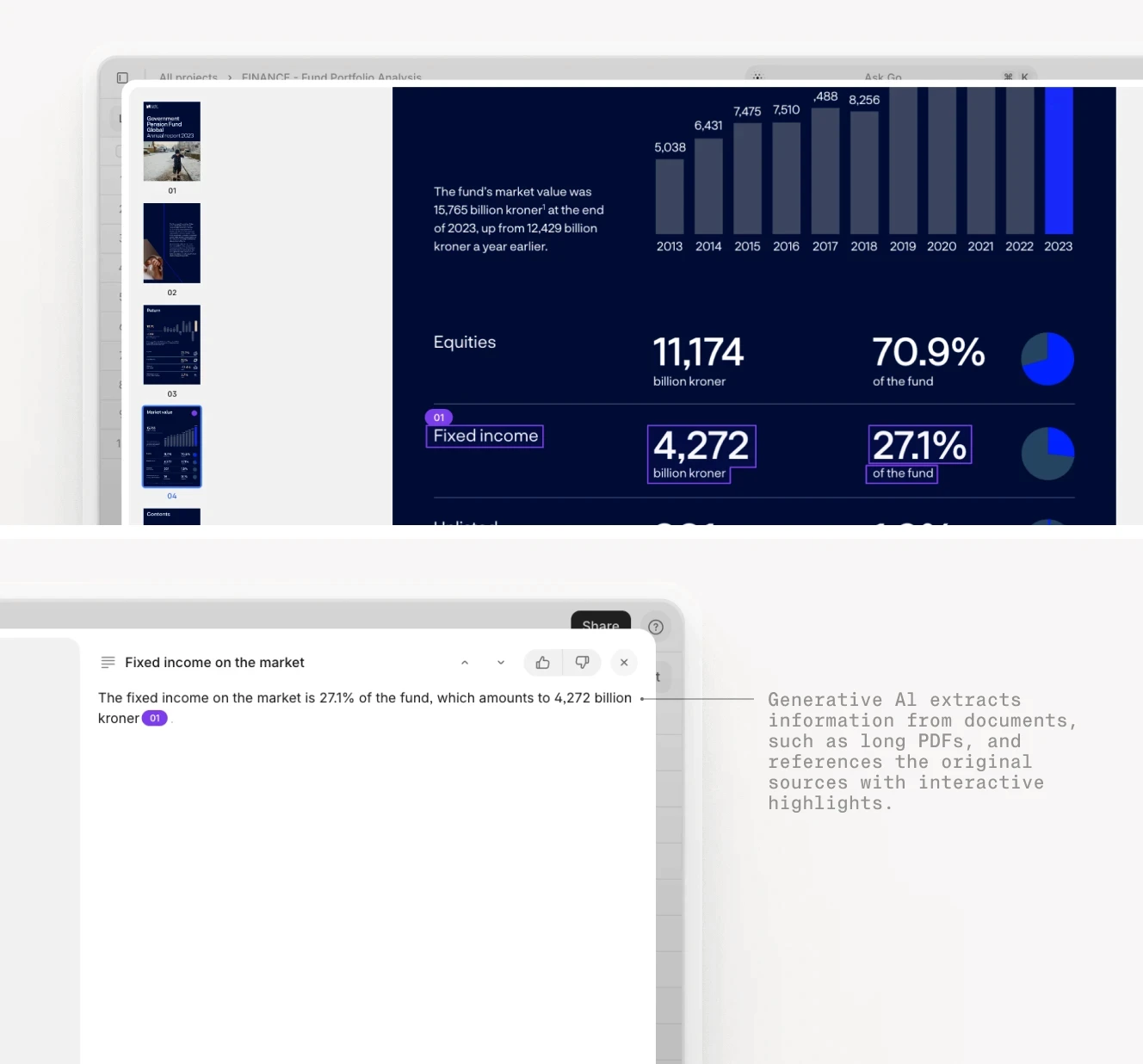

The AI Policy Analysis Agent is one example of how the review layer between document receipt and compliance decision can be automated without removing the human judgment that regulated decisions require.

Document intake workflows process incoming submissions in discrete stages: classification, extraction, comparison, and routing, rather than as a single undifferentiated review task.

The core insurance compliance requirements

Five distinct obligation types govern regulatory compliance for most insurers and MGAs. Each generates its own document categories, review cadences, and failure modes. Understanding them separately matters because conflating them produces compliance programs that address everything in general and nothing specifically enough to prevent findings.

Licensing and market conduct

Every line of insurance, in every state, requires an admitted or surplus lines license. License applications require filing documentation with each state's Department of Insurance. Changes in business model, ownership, product line, or geographic scope can trigger new filing requirements. Renewal cycles generate their own submissions. Market conduct exams, which states use to audit insurer behavior in the field, can pull policy files, claims files, complaint logs, and underwriting records going back three years.

For an insurer adding a new product line or entering a new state, licensing compliance alone generates hundreds of document submissions before the first policy is written. For an insurer facing a market conduct exam, the document production requirement can run to tens of thousands of records, assembled on a regulator's timeline rather than the insurer's own schedule. Manual document retrieval under that pressure is where compliance gaps tend to surface.

Data privacy obligations

Insurers handle some of the most sensitive personal data any business collects: health history, financial condition, driving behavior, criminal records, and in life insurance, biometric information. The California Consumer Privacy Act covers California policyholders. Fifteen-plus other states have enacted comparable privacy laws with varying carve-outs for insurance-specific data. The EU's GDPR applies to any international cedant or reinsurer relationship involving EU-resident data.

Each regulation specifies different retention limits, consent requirements, data subject rights, and breach notification timelines, all of which have to be implemented in policy language, operational procedure, and claims handling workflow. The compliance obligation is not understanding the rules in the abstract. It's maintaining documentation that proves the rules are being followed for each policyholder, each data category, and each third-party data sharing arrangement in the insurer's operations.

AML and KYC obligations

Life insurers, premium finance providers, and MGAs handling international business face anti-money laundering obligations under the Bank Secrecy Act. Know-your-customer checks are required for high-value annuity purchases, certain commercial lines programs, and premium finance arrangements over defined thresholds. The documentation requirements, which include customer identification, beneficial ownership verification for entity policies, and suspicious activity monitoring, parallel banking AML requirements, with the added complexity that insurance transaction patterns differ from banking norms in ways that standard AML frameworks don't address.

An international cedant relationship, for example, can generate a KYC documentation requirement involving multiple jurisdictions, beneficial ownership chains across several entities, and source-of-funds verification for premium payments, each of which requires documentary evidence that the MGA or insurer must maintain and produce on request.

Financial and actuarial reporting

The NAIC's Insurance Regulatory Information System ratios are the primary solvency benchmark for state regulators, tracking twelve financial ratios across the statutory financial statements. Risk-Based Capital calculations require actuarial certification and must be recalculated when the business mix or reinsurance structure changes significantly. Annual statement filings, the statutory equivalent of a Form 10-K, must reconcile internal records across dozens of schedules, each of which references figures from underlying policy and claims records.

Reserve adequacy opinions, loss development triangles, and reinsurance recoverables are reviewed by state examiners looking for signs of financial distress or reserve manipulation. The document volume for a single annual statement cycle runs to thousands of pages. The accuracy requirements leave no margin for inconsistencies between related schedules. Those inconsistencies, in a manual process, typically originate from records that weren't synchronized across departments.

AI and algorithmic governance

The NAIC's AI Model Bulletin, adopted in December 2023 and now incorporated into regulatory guidance in multiple states, requires insurers to ensure that vendor AI systems used in underwriting or claims decisions don't produce discriminatory outcomes against protected classes. Colorado's SB 21-169 requires documented bias audits for any insurance AI system using external consumer data. California and Connecticut are at various stages of comparable rulemaking.

For any insurer using an automated underwriting scoring model or claims triage tool, compliance now includes documenting what the model does, how it was validated against bias metrics, what controls prevent disparate impact, and how those controls are monitored over time. That documentation obligation sits on top of the existing regulatory stack. It doesn't replace any of the licensing, financial reporting, or data privacy requirements that already apply.

An AI system evaluating an insurance request against document contents, representing the type of workflow that now falls under AI governance requirements in states adopting NAIC-aligned AI regulation.

The document review bottleneck in insurance compliance

The cost of insurance compliance comes from document volume and variability, not from the difficulty of the regulations themselves. Most compliance officers understand what the regulations require. The problem is proving compliance, at scale, without missing anything.

Consider a mid-size commercial lines insurer with 150 active program forms. Each form carries a base policy document, an average of 12 endorsements, and state-specific variations for 20 states. That's roughly 36,000 individual document versions in active circulation. Renewal season means reviewing a meaningful fraction of them for regulatory currency: have any endorsement approvals lapsed? Has a state updated the required language for a data-sharing disclosure? Has the AML threshold for suspicious transaction reporting changed since the last renewal cycle?

A compliance analyst working at full speed reviews 8 to 12 complex policies per day. At that rate, reviewing a quarter of the active policy library for a single renewal window would require four analysts working exclusively on form review for three months, before accounting for new submissions, regulatory updates, or the annual statement cycle that overlaps with Q4 renewals.

Manual review at that volume produces three failure modes, not one. First, inconsistency: different analysts apply different levels of attention to the same boilerplate exclusion language, so one reviewer flags a deviation that another treats as within tolerance. Second, coverage gaps: under time pressure, reviewers skip endorsements they've seen before, which is exactly where outdated language accumulates across renewal cycles, because it's the language nobody thinks to check. Third, bottlenecks: renewal windows concentrate document volumes that exceed capacity. Reviews get compressed, sequenced, or deferred, each of which opens a window where unreviewed documents are in active circulation.

The structural economics of manual compliance review don't improve with scale. A regulatory fine for a missed mandatory form filing can reach six figures in states with aggressive enforcement postures. A consent order triggered by a pattern finding in a market conduct exam can restrict a line of business for years while the remediation plan is negotiated and implemented. The cost of thorough manual review, analyst hours, supervisor review, QA sampling, doesn't scale to cover the risk exposure it's supposed to manage.

That gap is the specific problem that AI document review addresses. Not the compliance judgment calls, which remain with the compliance team. The extraction, comparison, and flagging work that precedes those judgment calls.

Insurance documents arrive in varied formats, scanned forms, PDFs, mixed-format broker submissions. Consistent review across format variability is the baseline requirement for compliance automation.

How AI automates insurance compliance document review

AI agents handle the extraction, comparison, and flagging steps that precede compliance judgment. That is a different claim than "AI does compliance", and the distinction is not semantic. In a regulated industry, compliance decisions carry personal and organizational accountability. The AI's role is to ensure that those decisions are made with complete, accurate information rather than on the basis of what a fatigued analyst happened to catch at hour seven of a document review session.

The practical scope of what AI handles in insurance compliance is straightforward: reading documents and comparing their contents against reference standards. Policy wording review. Endorsement version tracking. Regulatory change impact analysis. Audit evidence assembly. Each of these tasks is mechanical and voluminous. None of them requires judgment. All of them are currently consuming compliance team capacity that would be better directed at the decisions that do require judgment.

Policy wording review

Policy wording review is the clearest application for AI automation in insurance compliance, not because it's intellectually difficult, but because it's mechanical and high-volume. An AI agent can compare every clause in a submitted policy form against the approved reference version, flag deviations with exact page and line citations, and classify findings by severity in the time it takes a human reviewer to read the coverage definitions section of a single policy.

For an MGA submitting programs to Lloyd's, that means every policy wording deviation is flagged before the submission reaches the syndicate's underwriting team. The underwriter sees a structured deviation report: specific clause, specific deviation, specific page reference. The compliance officer reviews exceptions and makes remediation decisions. Neither of them has read the full 90-page policy to get to that point.

For an insurer managing admitted forms across multiple states, AI policy wording review means that every form renewal is checked against the current filed version automatically. Deviations from the approved filing are flagged before they go into circulation, not discovered during a market conduct exam three years later. The Policy Analysis Agent handles this review layer for insurance-specific document types, including endorsement-heavy commercial programs that vary significantly by state.

Endorsement and amendment tracking

Endorsement stacks are where compliance problems accumulate without anyone noticing. An endorsement that modifies coverage terms gets added at policy inception. A renewal cycle adds a superseding endorsement but doesn't remove the original. Three years in, the policy file contains contradictory language that applies to a pending claim, and the claims examiner has to resolve the contradiction under pressure, with a claimant waiting and a coverage dispute forming.

The agent tracks endorsement version history across a policy lifecycle, identifies conflicting or superseding language within a stack, and flags policies where the endorsement sequence requires adjudication before renewal. The output is a prioritized list of file anomalies with source references, not a request for a compliance analyst to work through 300 policy files looking for version conflicts.

For MGAs managing multiple program endorsement families, automated endorsement tracking also surfaces the secondary compliance issue: endorsements approved for one program getting applied to another through copy-paste form assembly. The resulting form modifications were never approved by the producing carrier. That is a market conduct finding waiting to happen. Catching it before renewal is materially less expensive than addressing it during an exam.

Regulatory change monitoring

State Departments of Insurance and the NAIC publish regulatory updates on a rolling basis: new model law adoptions, bulletins modifying required form language, data call deadlines, filing fee revisions, and emergency regulatory guidance. Manual monitoring requires a compliance team member subscribing to alert services for each state where the insurer is licensed, reading the alerts, understanding their scope, and mapping their impact to the insurer's specific form library and program mix. Across 30 states, that's a substantial portion of a compliance officer's working time, for a task that produces no output except a list of things to do next.

An agent ingests regulatory updates as structured inputs, cross-references them against the insurer's active form library and program portfolio, and produces a prioritized impact report: which specific forms are affected, which filings are triggered, which deadlines apply, and which program managers need to be notified. The compliance officer reviews the report and allocates response resources. The state-by-state monitoring that produced the report took minutes instead of the better part of a workday.

For the NAIC AI Model Bulletin specifically, this kind of regulatory monitoring is directly applicable: new state adoptions of AI governance requirements affect any insurer using automated underwriting or claims tools in those states. Those adoptions trigger documentation and audit obligations that weren't previously required. An automated monitoring workflow ensures those obligations are identified as they arise, not six months later when someone asks whether the insurer has an AI governance policy for Colorado.

Audit readiness

Market conduct exams and internal audits share a common requirement: complete, organized evidence that a specific compliance obligation was met, for a specific policy or transaction, at a specific point in time. The exam notice arrives. The examiner specifies what they need. The compliance team has 30 days to produce it.

Manual evidence assembly under that timeline means locating documents across multiple systems, confirming that the versions being produced are the ones that were actually in force at the relevant time, and organizing them into a format the examiner can work through systematically. When the underlying records weren't maintained with an exam in mind, when they were created as operational documents rather than evidence, that assembly process is expensive and produces a package that the examiner may still find incomplete.

Agents maintain a continuously updated audit evidence trail as a byproduct of normal compliance workflow. Every policy reviewed generates a record of what was reviewed, when, and what was found. Every regulatory update processed generates a record of the impact analysis and the response. Every endorsement anomaly flagged generates a record of the finding and its resolution. When an exam notice arrives, the evidence package for the specified period is assembled from records that already exist, not constructed under deadline pressure from whatever operational records happen to be accessible.

Multi-step AI agent workflows chain document ingestion, extraction, comparison, and finding classification into discrete steps, each producing a structured output that the next step processes further.

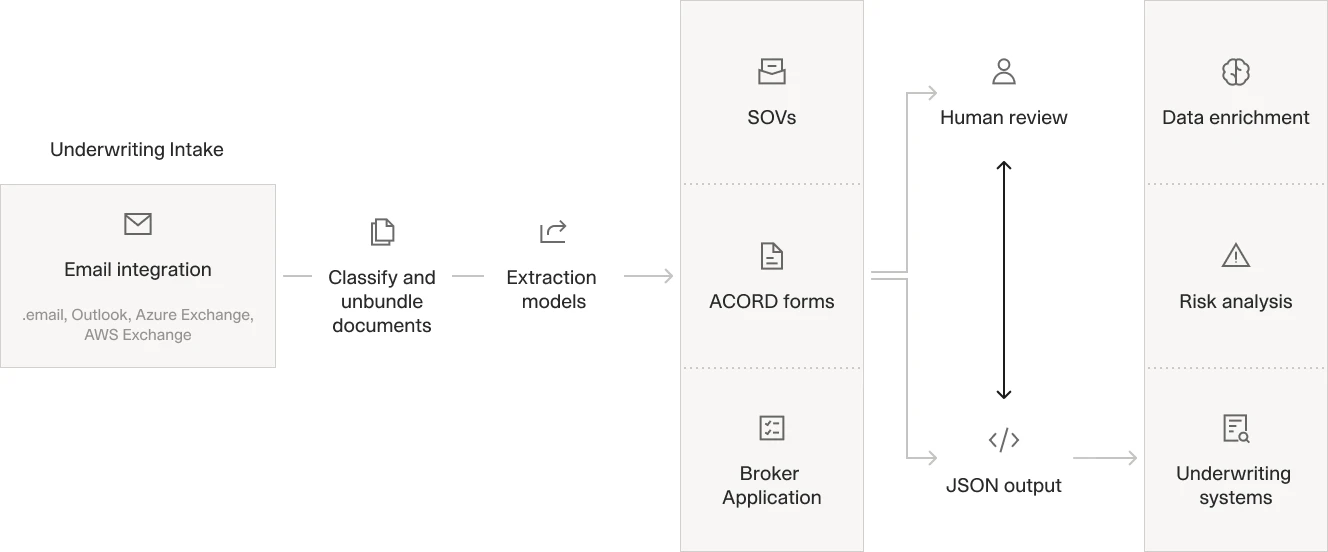

The following video shows V7 Go processing insurance operations document workflows, including submission processing and statement of values reconciliation at Lloyd's and reinsurance scale:

V7 Go processes insurance document bundles: submission processing drops from 30 minutes to 30 seconds at an international reinsurer, and statement of values reconciliation from 4 hours to 7 minutes at a Lloyd's syndicate.

What to look for in compliance automation software

The vendor market for "compliance automation" spans a wide range of tools: document tagging utilities, regulatory alert aggregators, form comparison tools, and multi-step AI agent workflows. Most insurers need the latter. But the marketing for all of them uses the same vocabulary. Here is what actually distinguishes tools usable in regulated compliance environments from those that aren't.

Source traceability is the threshold requirement

A compliance officer cannot act on an AI output they cannot verify. "The AI identified a deviation in the exclusion language" is not a compliance finding. "Page 47, paragraph 3 of submission 2024-08-182 uses language that differs from approved form IM-2022-14 in the following specific way, and here is the exact text from both documents" is a compliance finding. Any tool that produces the former without the latter cannot be used for regulated compliance work, regardless of what the rest of the feature set looks like. When a market conduct examiner asks how a deviation was identified and addressed, "the AI flagged it" is not an acceptable audit response.

Document variability matters more than processing volume

Insurance documents arrive in every format: clean PDFs, TIFF scans from legacy imaging systems, Excel schedules, mixed-format broker submissions, and email attachments with no consistent naming convention. A system that performs well on clean digital PDFs but fails on scanned endorsements, which is a large portion of what mid-size commercial lines operations actually process, is not a compliance automation system. It is a document viewing tool with a language model attached. Evaluate any vendor against a sample of your actual submission quality, not their demonstration documents.

Coverage rate matters more than processing speed

A review that catches 95% of form deviations in 30 seconds is less useful than a review that catches 100% of them in 5 minutes. Compliance is not a domain that accepts systematic misses in exchange for throughput. The 5% of deviations that are missed consistently will be the ones a market conduct examiner finds, because examiners are specifically trained to look for patterns that suggest systematic underreporting. Ask vendors for precision and recall metrics on document types comparable to your own, not speed benchmarks measured on their reference test sets.

Human review checkpoints are a design requirement

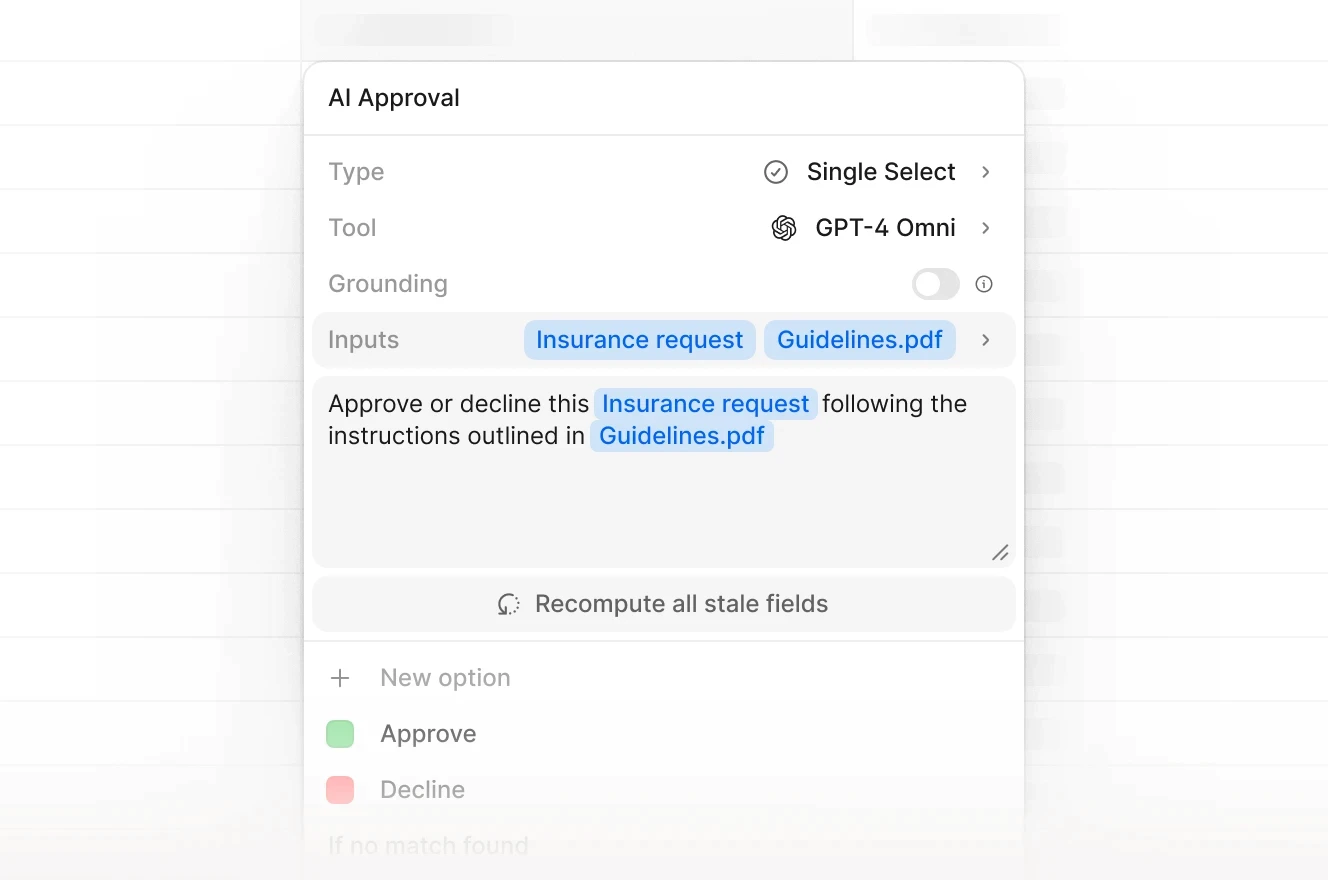

The appropriate architecture for insurance compliance automation is an AI workflow that flags, classifies, and organizes findings, with human compliance officers making the actual decisions about materiality, remediation, and regulatory response. Any tool framed as removing the compliance officer from that decision loop is misrepresenting what AI can reliably do in an environment where regulatory accountability is direct, personal, and documented.

Audit trail generation must be automatic

If producing audit-ready compliance records requires a separate export, formatting, or assembly step outside the normal compliance workflow, the tool is adding administrative work rather than removing it. Audit readiness should be a byproduct of ordinary compliance operations, records created during routine review, maintained in a format that can be produced without additional work when an examiner requests them.

Integration matters more than a standalone module

Insurance compliance does not happen in isolation from policy administration, claims systems, and regulatory filing platforms. A compliance automation tool that cannot pull policy data from the PAS, push findings into the workflow system, or receive regulatory updates from the alert service the compliance team already uses will create a parallel workflow that people work around rather than adopt.

How V7 Go automates insurance compliance workflows

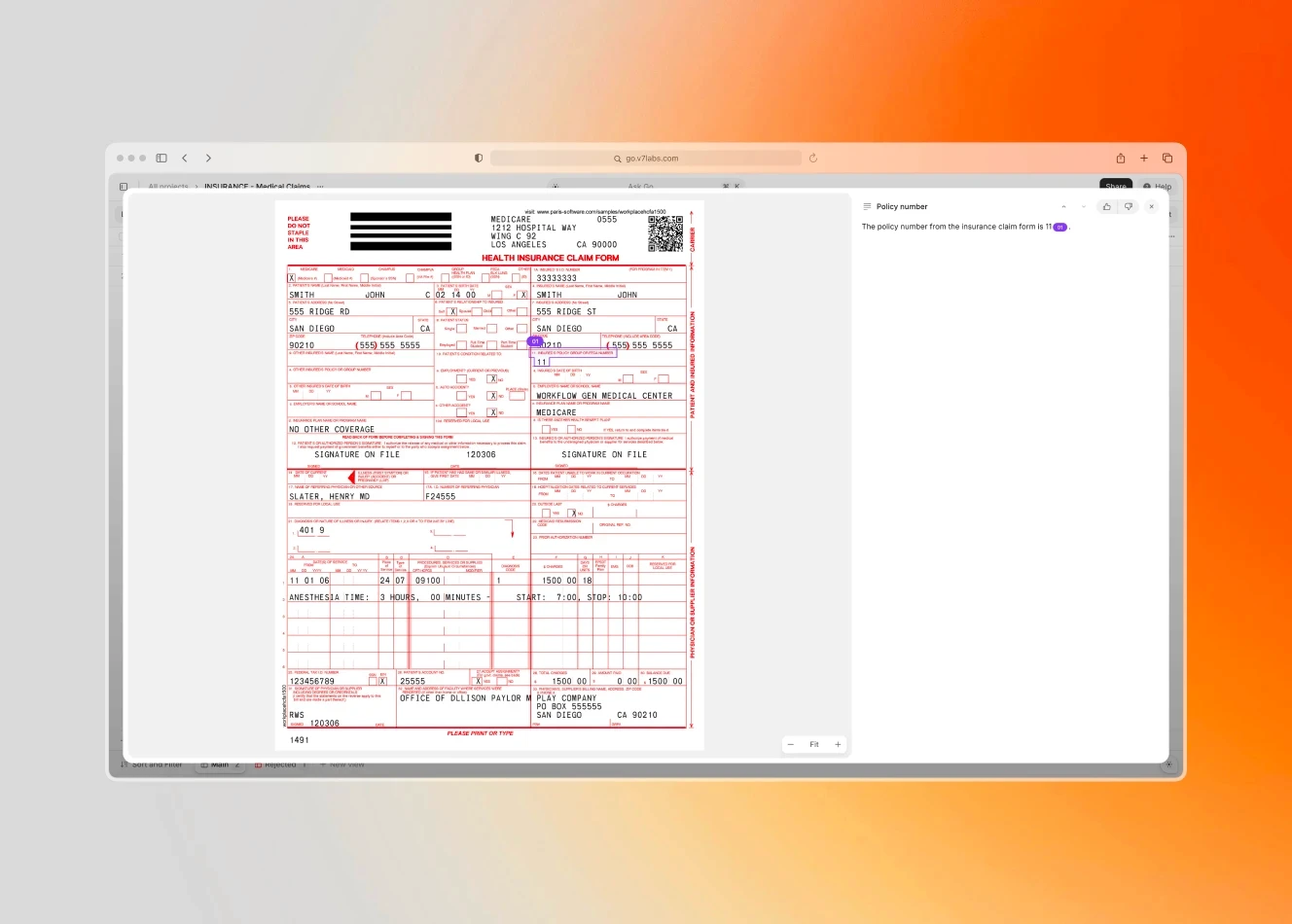

The specific case for V7 Go in insurance compliance is not processing speed, though the benchmarks are significant. The case is that every output is traceable to its source document, which is the functional prerequisite for using AI in regulated compliance work.

V7 Go's AI Citations feature, also called Visual Grounding, links every extracted clause, every flagged deviation, and every compliance finding directly to the exact page and passage in the source document. A compliance officer reviewing a V7 Go output clicks through to the specific location in the source policy in one step. In a context where "the AI said so" is not an acceptable audit response, that traceability is the functional difference between a tool that can be used for compliance work and one that produces outputs the compliance team still has to manually verify before acting on them.

The workflow architecture runs as a chain of discrete steps, not a single prompt producing a summary. A typical policy wording review in V7 Go proceeds as follows: ingest the submitted policy in whatever format it arrives, clean PDF, scanned form, mixed attachment, extract clause text with source page citations, compare each clause against the approved reference form, flag deviations with severity classification, and route the structured finding report to the compliance reviewer. Each step produces a structured output. Each output feeds the next step. The compliance officer receives a deviation report with direct source links, not a raw summary that requires independent verification before it can be acted on.

The benchmarks from V7 Go's insurance deployments give a sense of what this produces at operational scale. An international reinsurer reduced submission processing from 30 minutes to 30 seconds, a 60-fold reduction. A Lloyd's syndicate reduced statement of values reconciliation from 4 hours to 7 minutes. A third-party administrator reduced new claim file processing from 45 minutes to 1 minute. Those numbers describe the throughput change. The more important operational change is in consistency: when extraction and comparison are handled as a defined mechanical process, the error rate doesn't vary with analyst workload, document familiarity, or the time of day the review happens.

For organizations building a compliance automation stack, the Insurance Underwriting Agent and Policy Analysis Agent are starting points for the document review layer. The AI insurance underwriting guide covers how the same document processing architecture applies to the underwriting decision layer. This article focuses on the compliance and regulatory review workflows that run alongside underwriting and claims operations throughout the policy lifecycle.

V7 Go's Visual Grounding links every extracted finding to its exact source page and passage, providing the audit trail that compliance teams require before acting on any AI output in a regulated context.

Insurance compliance is a permanent feature of the industry, not a temporary problem awaiting a regulatory fix. The number of state insurance regulators is set by statute. The NAIC model law adoption process operates on its own timeline. AI governance requirements are accelerating, the states that haven't yet adopted NAIC AI guidance are watching the ones that have, and the trajectory is toward more documentation requirements, not fewer.

What changes with AI document review is the ratio between what compliance teams are required to do and what they can accomplish with the staff they have. Manual document review creates a hard ceiling on that ratio. More policies, more program forms, more states, more regulatory updates, and the ceiling gets lower because the same number of analysts has more ground to cover. AI document review removes the ceiling on extraction and comparison work, so compliance team capacity scales with the system rather than with headcount.

The technology is available. The question for most insurance organizations is which workflows to automate first, how to maintain the human review layer that regulated industries require, and how to build audit evidence practices that treat AI outputs as inputs to compliance decisions rather than as decisions themselves. The Claims Triage Agent and Insurance Document Ingestion automation are practical starting points for organizations beginning with high-volume, clearly bounded document workflows before extending automation into the compliance review layer.

What is insurance compliance?

Insurance compliance is the ongoing process of meeting the regulatory, contractual, and operational obligations that govern how insurance companies and managing general agents conduct business. It covers five primary areas: state licensing and market conduct requirements, data privacy regulations governing policyholder information, anti-money laundering and know-your-customer obligations, financial and actuarial reporting to state regulators, and AI governance frameworks for automated underwriting and claims tools. Compliance is not a one-time certification. It requires continuous monitoring of policy forms, regulatory updates, and operational practices across every state where an insurer is licensed. The central operational challenge is document review: proving compliance requires maintaining current, accurate records across thousands of policy forms, endorsements, and regulatory filings simultaneously. When compliance teams lack capacity to review those documents consistently, gaps accumulate in ways that only surface during market conduct examinations, regulatory audits, or coverage disputes.

+

What are the main insurance regulatory requirements in the US?

US insurance is regulated at the state level, with the NAIC coordinating model laws and standards across 56 jurisdictions. The main regulatory requirements fall into six areas. State licensing requires admitted or surplus lines status for each line of business in each state. Market conduct standards govern underwriting practices, claims handling, and consumer treatment. Financial solvency requirements include Risk-Based Capital calculations, NAIC IRIS ratio monitoring, and annual statutory financial statement filings. Data privacy rules under the CCPA and state equivalents cover policyholder data collection, retention, and sharing. Anti-money laundering obligations under the Bank Secrecy Act apply to life insurance, premium finance, and certain commercial programs. AI governance requirements under the NAIC AI Model Bulletin and state-level algorithmic bias laws in Colorado and other states complete the set. Each requirement generates distinct document types and review obligations that must be maintained continuously throughout the policy lifecycle.

+

How does AI help with insurance regulatory compliance?

AI helps with insurance regulatory compliance by handling the extraction, comparison, and flagging work that precedes compliance judgment, not by replacing that judgment. Specifically, AI agents compare submitted policy forms against approved reference wordings and flag deviations with exact source citations. They track endorsement stacks across a policy lifecycle to identify conflicting or superseding language. They ingest regulatory updates from state DOIs and the NAIC and identify which active forms and programs are affected. They maintain continuous audit evidence trails that produce the right documents when a market conduct examiner requests them. The key distinction is that AI handles mechanical document processing — reading 90-page policies to confirm exclusion language, cross-referencing state bulletins against active form libraries — while compliance officers make the actual decisions about materiality, remediation, and regulatory response. That division is what makes AI practically usable in regulated compliance environments where accountability for decisions is direct and personal.

+

What documents are involved in insurance compliance?

Insurance compliance involves several distinct document categories. Policy documents include base policy forms, endorsements, exclusion schedules, and state-specific form variations, each of which must match approved and filed versions. Regulatory filings include license applications and renewals, rate and form filings with state Departments of Insurance, and annual statutory financial statements. Underwriting records document the criteria applied to individual risks and must be available for market conduct review going back three years. Claims files include adjudication notes, reserve calculations, and payment records demonstrating compliance with policy terms and claims handling regulations. AML and KYC records include customer identification documents, beneficial ownership verifications, and suspicious activity monitoring logs. AI governance documentation — required by the NAIC AI Model Bulletin and state-level AI bias laws — includes model validation reports, bias testing results, and ongoing monitoring records for any automated underwriting or claims scoring tool. The compliance challenge is not having these documents. It is maintaining current, consistent versions across all of them and producing specific records on demand during regulatory examinations.

+

How does AI maintain an audit trail for insurance compliance?

Compliance risk and regulatory risk are related but distinct in insurance. Compliance risk is the internal operational risk that an insurer fails to follow its own procedures, filed policy terms, or stated underwriting guidelines. Those gaps emerge between what the insurer is supposed to do and what it actually does in practice. A policy form that deviates from the approved filing is a compliance risk. An endorsement stack with conflicting language is a compliance risk. An AML check that was supposed to happen but didn't is a compliance risk. Regulatory risk is the external risk that the regulatory environment changes in ways that affect how the insurer can operate: new solvency capital requirements, revised data privacy rules, AI governance mandates, or enforcement actions triggered by industry-wide regulatory scrutiny. Compliance risk is largely within the insurer's control. Better document review processes, consistent procedure execution, and automated monitoring reduce it materially. Regulatory risk is driven by external events, but its operational impact depends on how quickly the insurer's compliance monitoring identifies relevant changes and responds to them before deadlines pass. AI document review primarily addresses compliance risk by improving the consistency and coverage of internal document review; it also reduces regulatory risk exposure by automating the monitoring and impact assessment of regulatory changes as they are issued.

+

What is the difference between compliance risk and regulatory risk in insurance?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.