16 min read

—

How value-add real estate investors are using AI to extract rent rolls, abstract leases, and accelerate NOI uplift modelling from offering memoranda.

The rent roll tells you whether the deal works. Everything else is context.

A value-add real estate deal arrives as a stack of documents: a 40-page offering memorandum (OM) with the rent roll embedded as a PDF table, individual lease documents for each tenant, and an executive summary quoting in-place rents that may not match the underlying unit data. Before a single figure goes into your underwriting model, someone has to extract it.

At one deal, that is four to eight hours of analyst time. At 30 to 50 offering memoranda per quarter (the volume a mid-sized acquisition team needs to source two or three actionable deals), manual extraction is the constraint that determines how many opportunities you can actually evaluate.

Artificial intelligence tools have changed what is possible at this stage. Rent roll extraction from PDF tables, lease abstraction, below-market lease identification, and structured data output to financial models are problems AI tools can now solve. But most software marketed as "AI for real estate" targets property management, market data, or portfolio reporting. Fewer tools address the document-heavy analysis workflow that is central to value-add investing.

This article maps the value-add investment strategy, the five-stage analysis workflow it demands, and the AI tools built for each stage.

In this article:

What value-add real estate is and how it compares to core and opportunistic strategies

The investment strategy spectrum from core to opportunistic, with a returns and risk comparison table

The five-stage value-add analysis workflow: from OM screening to risk assessment

The best AI software for value-add real estate investment analysis, evaluated by functional fit

How V7 Go automates rent roll extraction, lease abstraction, and below-market lease identification

Answers to common questions about value-add real estate strategy and deal analysis

AI for document processing

Automate rent roll extraction and NOI modelling workflows

Get started today

What Is Value-Add Real Estate?

Value-add real estate is a commercial property investment strategy that targets assets with identifiable operational or physical inefficiencies. Investors acquire properties at below-stabilised value, implement targeted improvements (renovations, lease-up, management restructuring) and exit at a higher valuation once net operating income (NOI) increases.

The thesis is straightforward: the gap between what a property earns today and what it could earn under disciplined ownership is the return opportunity. Identify that gap correctly, price it into the acquisition, execute the business plan, and the exit cap rate applied to a higher NOI produces the return.

Value-add real estate refers to commercial properties acquired below their stabilised value where targeted capital improvements, operational changes, and leasing activity will increase net operating income and therefore asset value. The "value" is the spread between current income and income potential.

In commercial real estate (CRE), the most common value-add plays are:

Below-market rents in expiring leases. In-place rents trail market rents by 20 to 35 percent, and leases expire within the hold period. Re-leasing to market drives the NOI uplift that validates the acquisition price.

Deferred maintenance. A physically sound building with visible deterioration: dated lobbies, aging HVAC, deferred roof work, suppressing occupancy or preventing rent growth. Capital expenditure (CapEx) unlocks repositioning.

Mismanaged operations. Properties with above-market operating expenses or persistent vacancy caused by poor leasing effort rather than weak demand in the submarket.

Lease-up plays. Newly built or recently repositioned assets at 65 to 80 percent occupancy where stabilisation is the primary value creation event.

Return expectations for institutional value-add strategies typically target 12 to 20 percent levered internal rate of return (IRR), a 1.5 to 2.5 times equity multiple (EM), and a hold period of three to seven years.

Core, Core-Plus, Value-Add, and Opportunistic: The Investment Strategy Spectrum

Value-add occupies the operational improvement middle ground of the CRE risk-return spectrum. Understanding where it sits clarifies both what the strategy demands analytically and how it differs from adjacent approaches.

Strategy | Risk profile | Target IRR (levered) | Hold period | Occupancy at entry | Value creation lever |

|---|---|---|---|---|---|

Core | Low | 6–9% | 7–10 years | 95%+ | Income protection; lease renewal |

Core-Plus | Low-Medium | 8–12% | 5–8 years | 90–95% | Minor CapEx; market rent roll-up |

Value-Add | Medium | 12–20% | 3–7 years | 70–90% | CapEx and leasing uplift; lease-up execution |

Opportunistic | High | 20%+ | 3–7 years | <70% or development | Redevelopment; entitlement; ground-up construction |

Value-add works because it occupies the middle band of the risk-return spectrum where the conditions for active management are right. There is enough occupancy and in-place cash flow to support acquisition financing, but enough rent roll inefficiency to generate the NOI uplift the acquisition price requires. Core strategies protect income. Opportunistic strategies build assets from structural distress or entitlement. Value-add does something more specific: it finds commercial real estate assets where the income is real but underperforming, and brings it in line with what the market supports.

The distinction from opportunistic is frequently misunderstood. Opportunistic returns above 20 percent come from development risk, entitlement risk, or heavy structural redevelopment — not from leasing up an existing rent roll. A property at 50 percent occupancy with structural obsolescence is opportunistic. A property at 80 percent occupancy with leases 25 percent below market is value-add commercial real estate. The analytical workload for each is completely different.

Value-add acquisitions are, at their core, a document analysis problem. The investment thesis lives in the rent roll, the lease expiry schedule, and the terms of each individual lease. Read those documents correctly and the modelling follows. Miss a co-tenancy clause or misread a below-market lease lock, and the business plan fails before the first renovation begins.

The Value-Add Investment Analysis Workflow

Most articles about AI for real estate describe tools for market data or portfolio reporting. None maps the specific analytical workflow a value-add acquisition requires at the deal level. Here is the five-stage process, from OM receipt to risk-adjusted return estimate.

Stage 1: Offering Memorandum Screening

The OM is the entry point for every deal. It contains the rent roll snapshot, in-place NOI, property condition summary, and market context. The screening question is whether the gap between in-place rents and market rents is large enough, and whether leases are short enough, to support a viable value-add business plan.

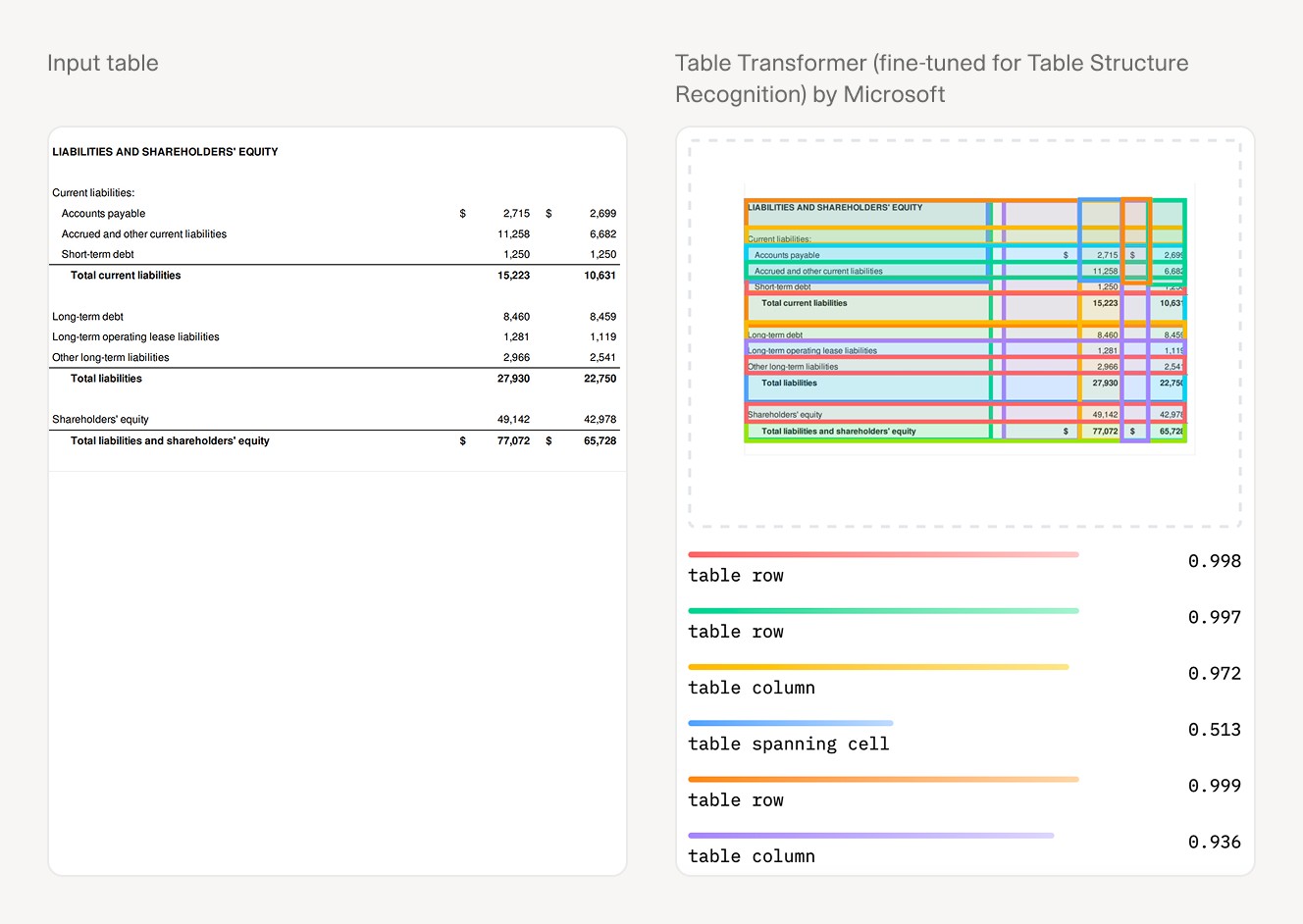

A senior analyst reviewing an OM manually reads 30 to 60 pages, extracts the rent roll (often embedded as a PDF table rather than provided as a spreadsheet), calculates the weighted average rent gap, and forms an initial view on physical condition risk. That takes two to four hours per OM. At 30 to 50 OMs per quarter, manual extraction is the binding constraint on how many opportunities get a real look.

Stage 2: Rent Roll Analysis

Once a deal clears initial screening, the rent roll gets a detailed review. Key extractions: unit mix (bed/bath/type for multifamily; tenant/square footage/type for commercial), in-place rents, lease expiration dates, and current rent per square foot.

The core calculation is the weighted average rent gap: market rent minus in-place rent, multiplied by occupied square footage, summed across all units or tenants. This is the annual NOI uplift available if all below-market leases are reset to market on expiry. It is the primary upside metric against which the acquisition price is justified.

Red flags: in-place rents above market (downside risk on expiry, not upside), lease cliffs where more than 30 percent of the rent roll expires in the first 12 months (execution risk), and vacancy concentrated in a single large tenant (credit risk).

Stage 3: Lease Due Diligence

Each lease in the rent roll is reviewed for remaining term, renewal options and their pricing, rent escalation clauses, landlord versus tenant improvement obligations, exclusivity clauses in retail, and co-tenancy provisions. Each non-standard term affects the business plan and the timing of NOI realisation.

The highest-value flag at this stage is a below-market lease with a long remaining term and a renewal option exercisable by the tenant at the same below-market rent. This locks value: the NOI uplift cannot be realised until expiry, which may extend beyond the projected hold period and blow the return model.

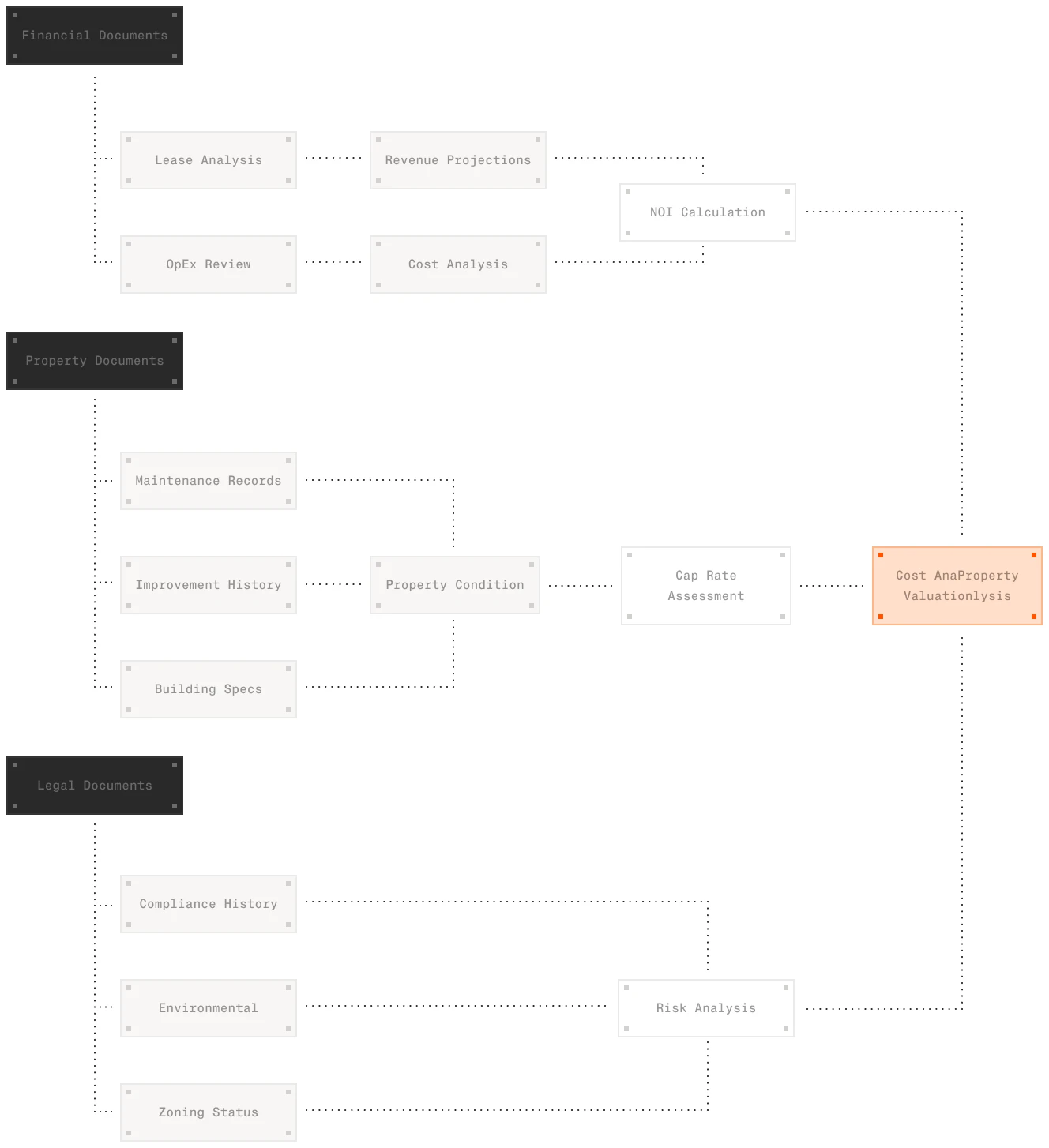

Stage 4: NOI Uplift Modelling

With a structured rent roll and abstracted lease terms, the analyst builds the proforma. Inputs: stabilised rents at market, projected absorption timeline, CapEx budget, and operating expense assumptions. Output: year-three stabilised NOI applied to an exit cap rate to estimate exit value, back-solved for levered IRR.

This is where Argus Enterprise does its job. But Argus requires structured inputs. If the rent roll arrived as a PDF and the leases as individual documents, someone has to structure those inputs first. That extraction step is where most analyst time in value-add underwriting actually goes.

Stage 5: Risk Assessment

Three risk categories dominate value-add analysis. Vacancy risk: what if absorption is slower than modelled? CapEx risk: is contractor pricing locked, and what is the contingency assumption? Market risk: does the submarket rent growth forecast from CoStar or Cherre support the stabilised rent assumption?

Market intelligence from platforms like CoStar informs the rent growth input. The lease review informs execution risk. The OM analysis sets the starting conditions. Each stage feeds the next, which is why an error at Stage 1 or 2 compounds through the entire model.

Best AI Tools for Value-Add Real Estate Investment Analysis

Most software marketed as "AI for real estate" targets property management, investor reporting, or market intelligence. Fewer tools address the deal-level document analysis workflow central to value-add investing. The following evaluates the platforms relevant to the five-stage process above, positioned by what they actually do.

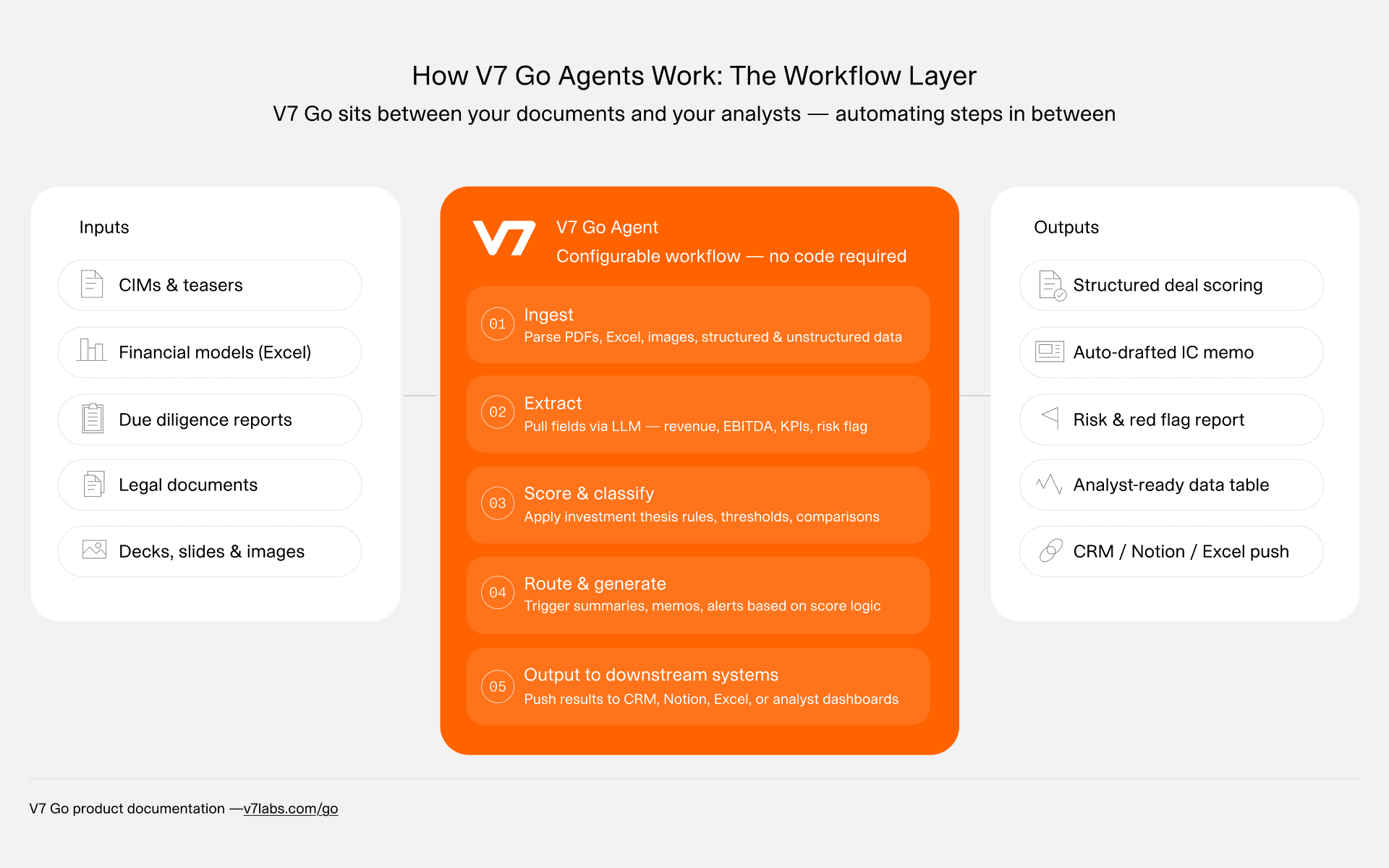

V7 Go

Best for: Document intelligence at the deal level — rent roll extraction from OM PDFs, lease abstraction, exception flagging, and structured data output for financial modelling.

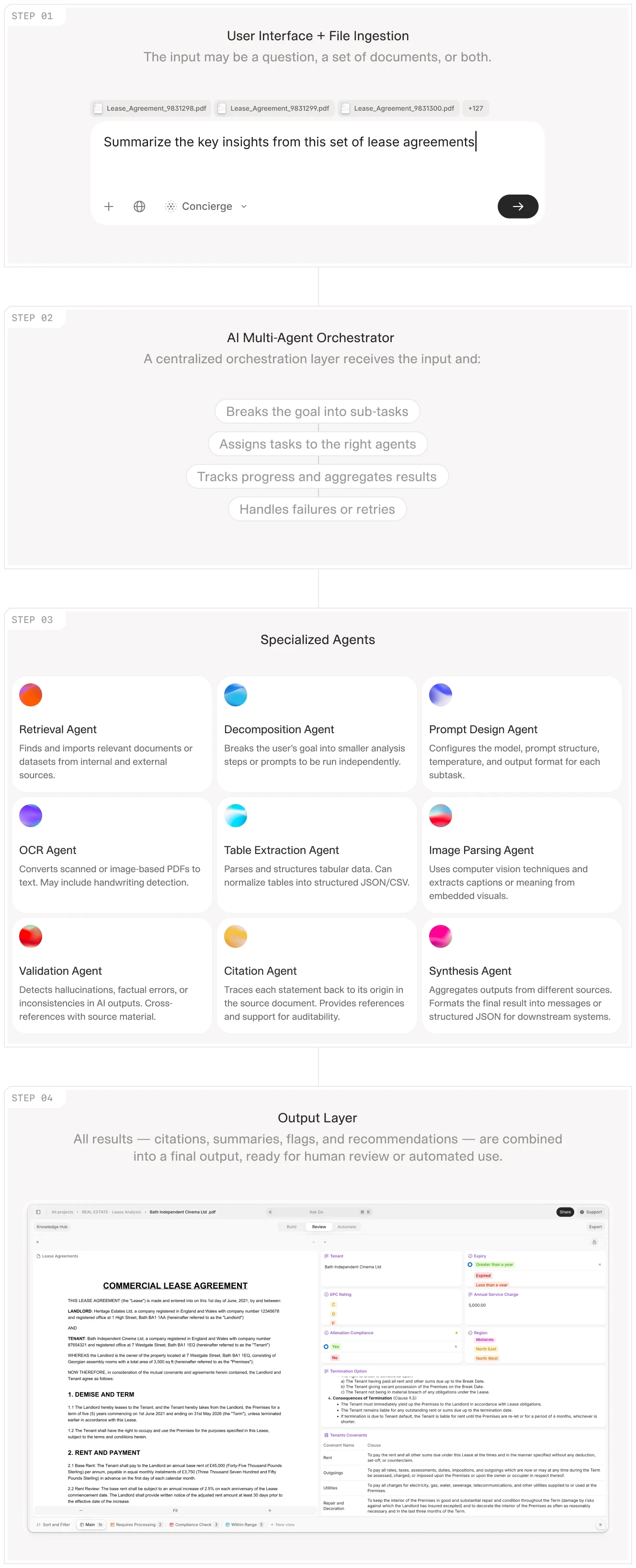

V7 Go is a document intelligence platform built for enterprise workflows processing high volumes of unstructured document inputs. In value-add deal analysis, it addresses the extraction bottleneck that precedes every proforma: reading OM PDFs, pulling embedded rent roll tables, structuring tenant-level or unit-level data, and abstracting individual lease terms across a full deal package.

What distinguishes V7 Go for value-add work is its ability to process documents as they actually arrive: PDFs with rent roll tables rendered as image layers, brokerage packages formatted inconsistently across deals, lease documents with non-standard clause structures. The output is structured data ready for Argus Enterprise or custom financial models, without manual rekeying.

Purpose-built agents for real estate include the AI Lease Abstraction Agent, the Commercial Lease Analysis Agent, and the Real Estate Investment Committee Memo Agent, which converts structured deal data into IC-ready outputs.

Argus Enterprise (Altus Group)

Best for: Building the detailed proforma once rent roll and lease data has been structured. The institutional standard for CRE cash flow modelling and exit valuation.

Argus Enterprise is the industry-standard underwriting tool for commercial real estate. It does not extract data from documents; it models data once that data has been structured and entered. For value-add acquisitions, Argus is the output layer: the platform where the NOI uplift thesis is tested against realistic absorption timing, CapEx phasing, and exit cap rate sensitivities.

Every serious value-add sponsor uses Argus for final underwriting. The question is not whether to use it but how to get reliable inputs into it faster. Document intelligence tools address the extraction step that Argus cannot handle.

CoStar and Cherre

Best for: Calibrating the market rent assumption that anchors the rent gap calculation; submarket vacancy data and rent growth forecasts for Stages 4 and 5 of the analysis.

The market rent figure in the rent gap calculation is only as reliable as the comp data behind it. CoStar provides transaction and lease comp data across all major CRE asset classes. Cherre aggregates property data across public records, operator inputs, and third-party market intelligence providers. Both are essential inputs for accurate NOI uplift modelling, but neither touches the document extraction problem at Stages 1 through 3.

VTS

Best for: Managing leasing execution after acquisition closes. Tracks prospects, deal terms, and market comps across a commercial portfolio through the lease-up phase.

VTS is relevant post-close, not at underwriting. For value-add sponsors, it manages the leasing activity that drives the NOI uplift, tracking broker relationships, prospect pipeline, and deal progress against the proforma absorption schedule. It does not contribute to the deal analysis workflow prior to acquisition.

Blooma

Best for: First-pass underwriting automation at high deal volume. Generates rapid preliminary NOI and valuation estimates from structured data inputs and market feeds before a full Argus model is built.

Blooma complements Argus for sponsors screening large deal volumes who need a go/no-go signal before committing to full diligence. Less useful for detailed lease-level review or deals with complex tenant situations that require individual lease analysis.

ChatFin

Best for: Tracking actual versus proforma NOI across a stabilised portfolio; GL-level variance analysis post-acquisition.

ChatFin addresses performance monitoring once assets are stabilised, not deal-level underwriting. It answers "how is this asset performing against plan?" rather than "should we buy it?" Useful to asset managers running value-add portfolios through the execution phase; not relevant to acquisition teams evaluating new deals.

How V7 Go Accelerates Value-Add Document Analysis

Value-add real estate has been treated primarily as a modelling problem. Sponsors build detailed Argus models and write rigorous investment memos. But the inputs to those models come from PDFs that someone read by hand. V7 Go addresses the step that precedes everything else.

The document stack in every value-add deal

A typical value-add deal package contains one OM (30 to 80 pages, PDF), a rent roll (sometimes embedded in the OM, sometimes provided as a separate spreadsheet) and between five and fifty individual lease documents depending on asset type and tenant count. A commercial retail strip with 20 tenants carries 20 separate lease PDFs, each formatted differently, with option provisions buried in exhibits and riders.

Manual extraction across that document set takes four to eight hours per deal. At 30 to 50 OMs screened per quarter, that time cost has historically constrained deal capacity: a team can only evaluate as many opportunities as its analysts can process by hand. The analytical bottleneck is not judgement; it is data entry.

What V7 Go does at each stage

OM analysis: V7 Go reads the offering memorandum, locates the rent roll table whether in a typeset PDF, an image-rendered table, or a separate attachment, and extracts unit-level or tenant-level data including unit type, in-place rent, square footage, lease expiration date, and tenant name. The output is structured data, not a summarised paragraph. No manual rekeying required.

Rent gap calculation input: The structured rent roll output feeds a comparison against submarket comps to calculate the weighted average rent gap. V7 Go surfaces properties where the spread between in-place and market rent exceeds the threshold that justifies acquisition economics.

Lease abstraction: V7 Go reads each lease document and extracts term, rent, escalation schedule, renewal options and their pricing, landlord and tenant improvement obligations, exclusivity provisions, and co-tenancy clauses. The AI Lease Abstraction Agent processes multiple leases in parallel and outputs a normalised comparison table across the full rent roll.

Exception flagging: V7 Go automatically surfaces leases with terms that affect the business plan: below-market rents with long remaining terms, renewal options exercisable at current below-market rent, co-tenancy clauses that could void leases if an anchor tenant vacates, and near-term lease cliffs where more than 30 percent of the rent roll expires within 12 months of acquisition.

Stage 4 input: Structured rent roll and lease data output to a format compatible with Argus Enterprise or custom financial models. The analyst receives structured inputs and proceeds directly to proforma construction, skipping the extraction step. The Real Estate Cash Flow Modeling Agent connects directly to the structured rent data to feed the proforma.

At 30 to 50 OMs reviewed per quarter, the time recovered from automated extraction converts directly into deal capacity. A team that previously reviewed 10 deals thoroughly can review 30. The constraint shifts from data extraction to analytical judgement, which is where experienced real estate professionals add durable value. For acquisition teams evaluating V7 Go for CRE due diligence, the Dataroom to IC Memo workflow shows how document intelligence connects raw deal documents to investment committee output.

Frequently Asked Questions

What is a value-add real estate investment?

A value-add real estate investment is the acquisition of a property where identifiable operational or physical inefficiencies create a gap between current performance and stabilised potential. The investor acquires below stabilised value, implements targeted improvements including CapEx, lease-up, and management restructuring, and exits once NOI has increased at a valuation reflecting the improved income stream. Levered IRR targets are typically 12 to 20 percent over a three-to-seven-year hold period.

What is the difference between core and value-add real estate?

Core strategies target stabilised, fully-leased assets with predictable income streams. Returns are income-driven at 6 to 9 percent IRR with minimal active management beyond lease renewals. Value-add strategies accept occupancy or operational risk in exchange for the upside of resetting a below-market rent roll to market rates, targeting 12 to 20 percent IRR through active CapEx programs and leasing.

What is the difference between value-add and opportunistic real estate?

Both strategies accept significant risk, but the source of risk differs. Value-add risk is operational: the thesis depends on leasing up vacant space or resetting below-market rents in an existing, functioning asset. Opportunistic risk is structural: the return requires development, entitlement, or major redevelopment where the asset does not yet exist in its target form. Opportunistic strategies target IRRs above 20 percent and typically carry longer execution timelines.

What makes a good value-add property?

The best value-add properties combine below-market rents with near-term lease expiry so the opportunity materialises within the hold period, strong submarket fundamentals that support the market rent assumption, manageable deferred maintenance within a CapEx budget the NOI uplift can absorb, and an identifiable lease-up path traceable to manageable factors rather than structural demand weakness.

What returns can you expect from value-add real estate?

Value-add commercial real estate strategies typically target levered IRRs of 12 to 20 percent, equity multiples of 1.5 to 2.5 times, and hold periods of three to seven years. These are targets, not guarantees. Actual returns depend on execution quality, submarket conditions during the hold period, and exit cap rate assumptions at the time of sale. Deals at the higher end of the return range carry more lease-up risk or require more significant CapEx programs.

How do you analyse a value-add real estate deal?

The five-stage process: offering memorandum review to identify the rent gap and confirm physical condition; rent roll analysis to quantify the weighted average rent gap and flag lease-expiry concentration; individual lease review to identify terms that restrict or extend the value realisation timeline; NOI uplift modelling to build the proforma from structured inputs; and risk assessment across vacancy, CapEx, and market assumptions. Accuracy at Stages 1 and 2 determines the reliability of everything that follows.

Real estate investment teams are already using document intelligence to change the economics of deal analysis, processing more offering memoranda, reviewing more leases, and building more proformas without adding analyst headcount.

The extraction bottleneck is a solvable problem. Explore V7 Go's real estate agents to see how acquisition teams are recovering analyst hours from rent roll extraction, lease abstraction, and OM review.

What is a value-add real estate investment?

A value-add real estate investment is the acquisition of a property where identifiable operational or physical inefficiencies create a gap between current performance and stabilised potential. The investor acquires below stabilised value, implements targeted improvements including CapEx, lease-up, and management restructuring, and exits once NOI has increased. Levered IRR targets for value-add strategies are typically 12 to 20 percent over a three-to-seven-year hold period.

+

What is the difference between core and value-add real estate?

Core strategies target stabilised, fully-leased assets with predictable income streams. Returns are income-driven at 6 to 9 percent IRR with minimal active management. Value-add strategies accept occupancy or operational risk in exchange for the upside of resetting a below-market rent roll to market rates, targeting 12 to 20 percent IRR through CapEx and active leasing.

+

What is the difference between value-add and opportunistic real estate?

Both strategies accept significant risk, but the source differs. Value-add risk is operational: the thesis depends on leasing up vacant space or resetting below-market rents in a functioning asset. Opportunistic risk is structural: the return requires development, entitlement, or major redevelopment. Opportunistic strategies target IRRs above 20 percent and typically carry longer execution timelines.

+

What makes a good value-add property?

The best value-add properties combine below-market rents with near-term lease expiry so the opportunity materialises within the hold period, strong submarket fundamentals supporting the market rent assumption, manageable deferred maintenance within a CapEx budget the NOI uplift can absorb, and an identifiable lease-up path traceable to manageable factors rather than structural demand weakness.

+

What returns can you expect from value-add real estate?

The five-stage process: offering memorandum review to identify the rent gap; rent roll analysis to quantify the weighted average rent gap; individual lease review to identify terms that restrict or extend value realisation; NOI uplift modelling to build the proforma from structured inputs; and risk assessment across vacancy, CapEx, and market assumptions. Accuracy at Stages 1 and 2 determines the reliability of everything that follows.

+

How do you analyse a value-add real estate deal?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.