Document processing

18 min read

—

Explore how AI is reshaping third-party administrator (TPA) software, automating complex insurance workflows, improving efficiency, and redefining the TPA-insurer relationship.

Third-party administrators (TPAs) are the operational powerhouses of the insurance industry, managing everything from complex claims processing to intricate benefits administration on behalf of insurers and self-insured organizations. They handle the demanding back-office work and enable insurers to focus on core functions like underwriting and risk management. The scale and complexity of these operations—spanning health, life, property and casualty (P&C) insurance, and retirement benefits—necessitate sophisticated software solutions.

Traditionally, TPA software has been crucial for managing claims, administering policies, and ensuring regulatory compliance. However, these legacy systems often struggled with unstructured data, limited automation capabilities, and adaptability challenges. Now, artificial intelligence (AI) is introducing a new era of efficiency and intelligence to TPA operations. Modern AI platforms, like V7 Go, are automating document-intensive workflows, speeding up decision-making, enhancing accuracy, and redefining the value proposition of TPAs.

This deep dive explores:

The limitations of traditional TPA systems and where they fell short.

How AI, including technologies like Intelligent Document Processing (IDP) and AI agents, is fundamentally reshaping TPA software and capabilities.

The evolving competitive dynamic between insurers and TPAs in an AI-driven landscape.

Join us as we unpack the current state and future trajectory of AI in TPA software, examining how this technology is not just optimizing processes but strategically repositioning TPAs within the insurance ecosystem.

AI for document processing

Automate complex insurance workflows with AI agents

Get started today

The Unseen Engine: Understanding the Role of TPAs in Insurance

A Third-Party Administrator (TPA) acts as an operational extension for insurance carriers or self-insured employers, managing administrative and claims-related functions under contract. Think of them as specialized service providers handling the complex, often labor-intensive machinery that keeps insurance policies running smoothly and claims paid accurately.

While they don't assume insurance risk themselves (that remains with the insurer or self-funded entity), their role is crucial across the insurance value chain. According to Investopedia, they bring specialized expertise, economies of scale, and technological capabilities that many insurers find more efficient to outsource than to build in-house.

The scope of TPA services is vast and touches nearly every corner of the insurance world:

Health Insurance and Employee Benefits

This is perhaps the most common area for TPAs. Health insurers frequently outsource claims processing, member enrollment, premium billing, eligibility verification, and customer service to TPAs. Employers who self-fund their health plans heavily rely on TPAs to administer these plans entirely, from managing provider networks and negotiating rates to processing claims and ensuring compliance with healthcare regulations like HIPAA and ERISA.

TPAs in this space might handle medical, dental, vision, and pharmacy claims, manage Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs), conduct utilization reviews, and handle pre-authorizations for medical procedures.

Life Insurance and Annuities

While less common than in health insurance, TPAs also play a role in the life and annuities sector. Insurers may outsource policy administration tasks such as application processing, premium collections, beneficiary management, and death claim processing. TPAs specializing in retirement services administer 401(k) plans, pension plans, and annuity contracts, handling record-keeping, participant communications, distribution processing, and compliance testing.

Property & Casualty (P&C) Insurance

In P&C lines—covering auto, homeowners, commercial property, general liability, and workers' compensation—TPAs often function as outsourced claims departments. They manage the entire claims lifecycle: receiving the first notice of loss (FNOL), assigning adjusters, investigating claims, determining coverage and liability, negotiating settlements, and managing payments.

Large corporations with significant self-insured retentions for liability or workers' comp often hire specialized TPAs to manage these claims programs globally. Some major TPAs like Sedgwick and Crawford & Company handle claims for numerous Fortune 500 companies and insurers worldwide. Their services can extend to litigation management (appointing and overseeing defense counsel), subrogation, and risk control services.

Specialty Programs and Other Services

TPAs also cater to niche markets and provide specialized services. This can include administering travel insurance claims, managing warranty programs, handling unemployment claims for employers, conducting premium audits, or providing forensic accounting services for complex financial claims. Essentially, any operational aspect of insurance that can be standardized and efficiently managed can potentially be outsourced to a TPA.

Why Insurers Partner with TPAs: The primary driver is efficiency and focus. By outsourcing administrative burdens, insurers can concentrate on their core competencies: underwriting risk, developing new products, and managing investments, ensuring operational elements are efficiently handled, as highlighted by financial services firm Cherry Bekaert. TPAs bring specialized expertise, standardized processes, and often significant cost savings through economies of scale. A TPA serving multiple clients can invest more heavily in technology and specialized personnel than a single insurer might justify for certain functions. This partnership model has fueled a massive TPA industry, projected to surpass $500 billion in the US by 2030.

The Need for Specialized TPA Software

Handling the sheer volume and complexity of insurance administration tasks—processing thousands of claims daily, managing intricate policy rules, ensuring regulatory compliance across multiple jurisdictions, and communicating with numerous stakeholders—is impossible without robust, specialized software. Generic business software simply cannot cope with the unique demands of the insurance industry. TPA software is purpose-built to be the central nervous system of these operations.

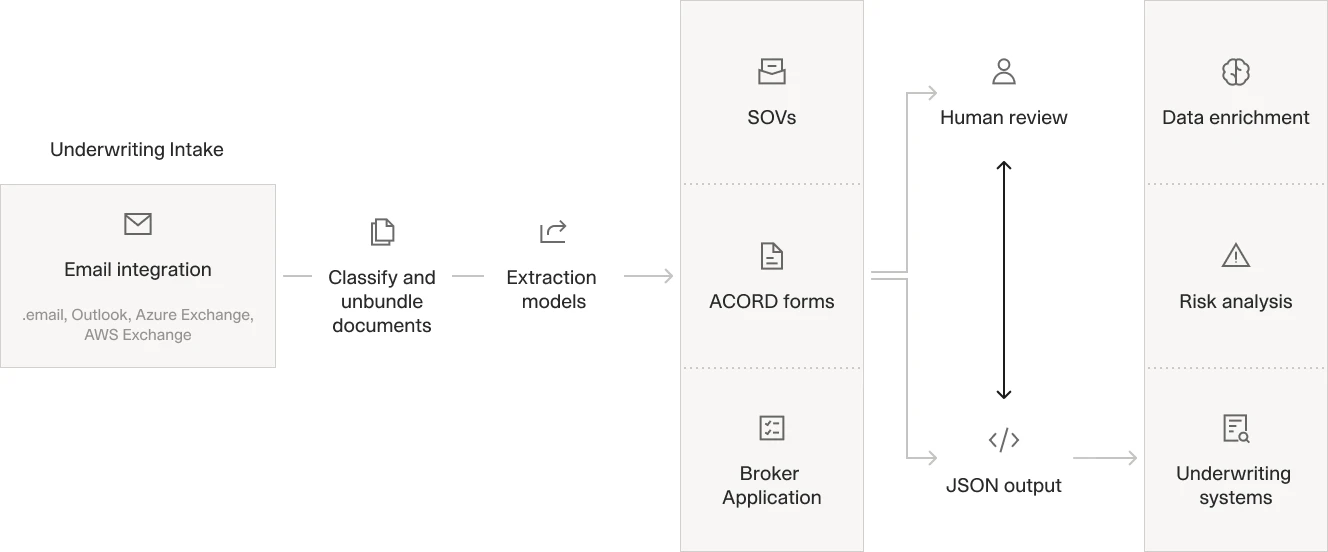

Modern TPA software integrates multiple steps, like document intake, classification, data extraction, and validation into seamless automated workflows.

Here’s why specialized software is non-negotiable for TPAs:

End-to-End Workflow Automation: TPA software automates the entire claims lifecycle, from FNOL intake and assignment to investigation, coverage verification, adjudication, payment processing, and reporting. Sophisticated rules engines can automatically adjudicate straightforward claims based on policy parameters and fee schedules, flagging only exceptions for human review. This drastically increases processing speed and consistency.

Structured Data Capture and Management: Insurance requires capturing vast amounts of specific data. TPA software provides configurable intake forms and structured data fields designed around industry standards (like ACORD forms or medical coding systems). This ensures data completeness and accuracy from the outset, reducing errors and follow-ups.

Integrated Communication and Collaboration: TPAs are communication hubs. Software facilitates this with built-in messaging, task management, automated notifications, and client/claimant portals. This keeps all stakeholders informed and ensures seamless collaboration between the TPA, insurer, claimant, providers, and legal counsel.

Centralized Document Management: Claims generate mountains of paperwork. TPA software acts as a central, secure repository for all related documents (policies, claim forms, medical records, legal correspondence, photos, etc.), linking them directly to the relevant claim file. Platforms like V7 Go even offer file repository features that function like a Virtual Data Room (VDR) for secure storage and AI analysis. This ensures easy access, version control, and auditability.

Compliance and Reporting: The insurance industry is heavily regulated. Specialized software helps TPAs stay compliant by embedding regulatory rules, tracking deadlines (e.g., state-specific reporting requirements), enforcing data privacy protocols (HIPAA), and generating necessary compliance reports and audit trails. Built-in analytics tools also provide insights into operational performance, cost trends, and potential fraud indicators.

Legacy Systems: The Constraints of Traditional TPA Software

While essential, traditional TPA software platforms, particularly those developed in the late 20th or early 21st century, were often built on architectures that now show their age. Many TPAs operated (and some still do) on legacy on-premises systems or mainframe applications that, while functional, present significant limitations in today's fast-paced, data-rich environment.

Common constraints included:

Scalability Issues: Older systems often struggled to handle increasing data volumes or concurrent users without performance degradation. Scaling typically required costly hardware upgrades.

Manual Processes Persist: Despite digitization, many steps remained manual, particularly data entry from unstructured documents (scanned forms, emails). Integration between different modules or systems was often poor, requiring data re-entry and increasing error potential.

Lack of Interoperability: Legacy systems were often closed ecosystems, making it difficult to integrate with insurer systems, third-party data sources, or modern digital tools (like mobile apps or customer portals). Data exchange relied on cumbersome batch files.

Rigidity and Inflexibility: Adapting legacy systems to new insurance products, changing regulations, or evolving business processes was often slow and expensive, requiring custom coding rather than configuration. This led to inefficient workarounds outside the core system.

Security and Compliance Gaps: Older platforms often lacked modern security features (like robust encryption or granular access controls) and struggled to keep pace with evolving data privacy regulations and reporting requirements.

The migration to web-based and cloud/SaaS TPA platforms in the 2010s addressed some issues, improving accessibility, scalability, and integration capabilities through APIs. However, these platforms remained fundamentally rule-based. They could automate predictable processes but lacked the ability to interpret unstructured data, learn from patterns, or handle ambiguity—limitations that AI is now beginning to overcome.

▶ Watch: AI in Insurance – Key Use Cases & Workflow Examples

The AI Infusion: How Intelligent Automation is Improving TPA Software

Artificial intelligence is moving beyond hype and delivering tangible improvements in TPA operations. By embedding capabilities like machine learning (ML), natural language processing (NLP), computer vision, and generative AI, modern TPA software platforms are automating tasks previously thought to require human cognition. This isn't just about doing the same things faster; it's about enabling entirely new levels of efficiency, accuracy, and insight.

Key AI advancements include:

1. Intelligent Document Processing (IDP) Enhanced

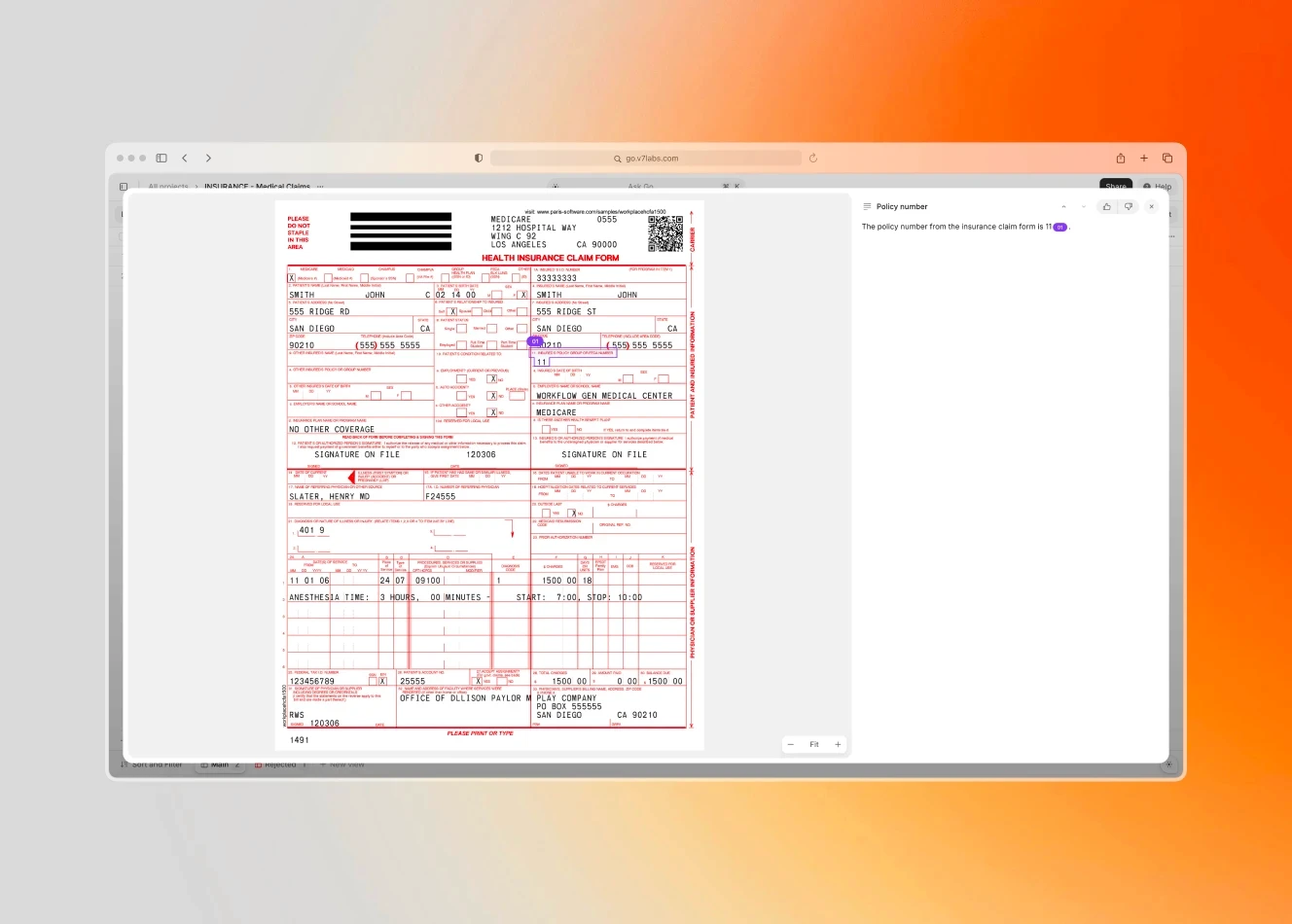

TPAs drown in documents. AI-powered IDP is the lifeline. Combining advanced Optical Character Recognition (OCR) with NLP and computer vision, these systems go way beyond text extraction. AI can read a complex medical report and extract diagnosis codes, procedure details, and treatment dates, even from narrative text or poorly structured formats. It can analyze images (like photos of car damage) or read handwritten notes on claim forms.

Platforms like V7 Go take this further by not just extracting data but also linking it back to the precise source location in the document (AI Citations), ensuring auditability. This drastically reduces manual data entry, accelerates intake, and improves data quality.

AI can accurately extract key identifiers like policy numbers from various claim forms, including scanned documents, improving TPA data accuracy.

2. Smarter Decision Support and Automation

AI moves beyond simple rule-based automation to provide intelligent decision support. Machine learning models trained on vast historical claims data can predict claim severity, identify potential fraud risks, or suggest optimal settlement amounts. For instance, AI can analyze initial claim information and predict the likelihood of litigation or prolonged disability in a workers' comp case, allowing for early intervention. These models once required extensive training or fine-tuning on custom datasets.

Today, however, even general-purpose Large Language Models can produce accurate insights—provided they’re given the right context as input. Thanks to expanding context windows, AI no longer needs to "know" everything; it just needs to understand the underlying mechanisms and patterns. Simple claims (e.g., minor auto damage validated by photos) can be auto-adjudicated with high confidence, freeing up human adjusters for complex cases requiring deeper AI underwriting analysis.

3. Proactive Fraud Detection and Prevention

AI systems are highly effective at identifying subtle patterns and anomalies indicative of fraud that might escape human reviewers. By analyzing claim data, provider billing patterns, and claimant history across large datasets, AI can flag suspicious activities—such as duplicate claims, upcoding of medical services, or networks of potentially collusive providers. TPAs leverage these AI tools to protect insurers and clients from significant losses.

4. Enhanced Customer and Stakeholder Experience

AI-powered chatbots and virtual assistants can handle routine inquiries (claim status, coverage questions) 24/7, providing instant responses and reducing call center volume. AI can also personalize communications and proactively update claimants on their claim progress. Sentiment analysis tools can monitor customer feedback to identify areas for service improvement.

5. Robust Compliance and Quality Assurance

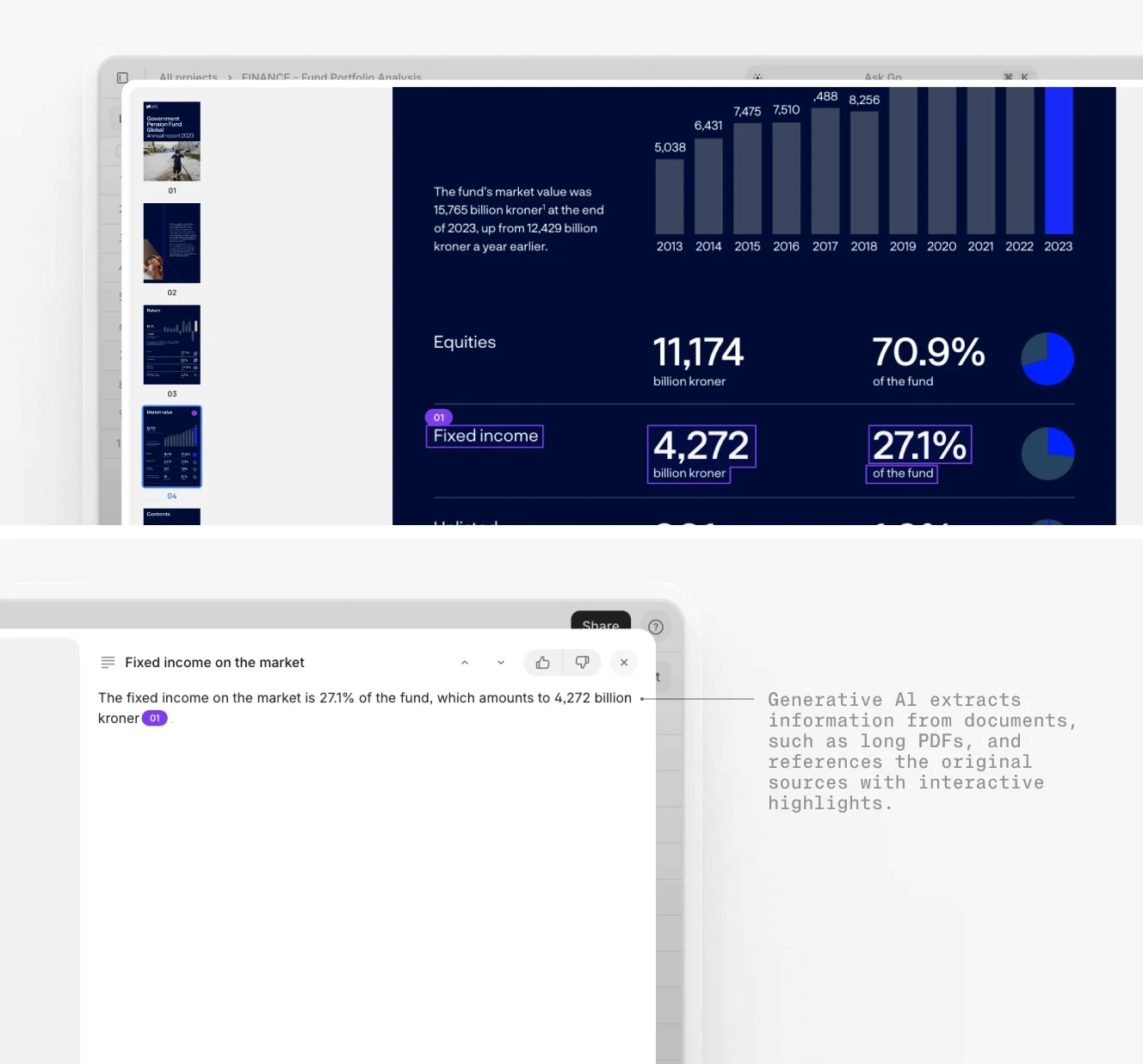

AI tools help TPAs navigate the complex web of regulations. They can automatically check claims against policy terms and regulatory requirements, ensure necessary documentation is present, and maintain comprehensive audit trails. AI can monitor 100% of transactions for compliance deviations, whereas human audits are typically sample-based. Features like V7 Go's source-linked citations enhance transparency and accountability.

Features like visual grounding and AI citations ensure extracted data can be easily verified against source documents, crucial for TPA compliance checks and audits.

6. Predictive Analytics for Strategic Insights

AI elevates TPA data from a record of past transactions into a source of predictive insights. By analyzing claim trends, cost drivers, and outcomes, AI can help TPAs advise insurers on underwriting adjustments, risk mitigation strategies, and reserve adequacy. This moves the TPA's role from purely administrative to a strategic partner, leveraging data to drive better overall insurance outcomes.

Spotlight on V7 Go: An Example of Advanced AI for TPAs

Platforms like V7 Go exemplify how AI is being applied to complex TPA workflows. V7 Go uses multimodal AI (processing text, images, etc.) and AI agents to automate tasks like AI insurance claims processing and due diligence. It can ingest entire claim files (regardless of length or format), analyze unstructured text, cross-reference information across documents, and generate structured outputs with verifiable citations back to the source material. Its Knowledge Hub feature allows secure storage and AI analysis of large document repositories. This type of platform shifts TPA software from being a system of record to an intelligent system that actively assists in processing and decision-making.

AI platforms like V7 Go allow TPAs to build custom workflows using intuitive interfaces, combining different AI models and tools without extensive coding, improving TPA software capabilities.

The AI Tightrope: Insurer In-Housing vs. TPA Partnership

The rise of powerful, accessible AI tools creates a fascinating tension in the insurer-TPA relationship. For decades, TPAs thrived by offering scale and specialization that insurers found costly to replicate internally. Now, AI potentially lowers the barrier for insurers to bring some administrative functions back in-house, challenging the traditional outsourcing model.

The Insurer's Dilemma: Automate Internally or Leverage TPA Innovation?

From an insurer's perspective, AI presents a compelling case for insourcing. If sophisticated AI platforms can automate large portions of claims processing or benefits administration with fewer human resources, why continue paying TPA fees? The technology potentially makes building an efficient internal administrative function more feasible and affordable than ever before, as discussed by experts at Insurance Thought Leadership. Insurers might also desire more direct control over customer data, operational processes, and the strategic insights derived from claims data.

The TPA's Opportunity: Becoming an AI Strategic Partner

Conversely, forward-thinking TPAs see AI not as a threat, but as a powerful enabler to deepen their value proposition. By aggressively adopting AI, TPAs can achieve unprecedented levels of efficiency, accuracy, and speed, often surpassing what an individual insurer could achieve alone. They can offer these enhanced services at competitive prices, potentially strengthening the case for outsourcing. Furthermore, AI enables TPAs to move beyond transactional processing and offer higher-value services, such as advanced analytics, predictive risk modeling, and proactive loss prevention consulting. TPAs that demonstrate strong capabilities leveraging AI can position themselves as indispensable innovation partners.

The Rise of Hybrid Models and Intensified Competition

The outcome is unlikely to be a simple win/lose scenario. We are more likely to see a spectrum of approaches: Some large insurers with significant IT resources may invest heavily in building their own AI administration platforms. Others may opt for hybrid models, insourcing certain functions while partnering with tech-forward TPAs for specialized services or leveraging the TPA's AI platform under strict governance agreements. Smaller or specialized insurers may continue to rely heavily on TPAs, but will demand greater technological sophistication and demonstrable AI capabilities.

This dynamic will undoubtedly intensify competition within the TPA market itself. TPAs slow to adopt AI risk being undercut by nimbler, tech-savvy competitors—including new entrants leveraging AI-native platforms from day one. Large incumbent TPAs like Sedgwick are already investing heavily in AI (e.g., their 'Sidekick' application) to maintain their edge. The pressure to innovate with AI is immense.

Ultimately, AI empowers both insurers and TPAs. The configuration of how this power is deployed—whether through in-house systems, outsourced partnerships, or collaborative ecosystems—will likely vary depending on strategic priorities, capabilities, and market segment. The constant, however, is the imperative to leverage AI effectively to remain competitive.

Navigating AI Adoption: Perspectives from TPAs, Insurers, and Regulators

The integration of AI into TPA software and operations creates distinct opportunities and challenges for different players in the insurance ecosystem. Understanding these perspectives is key to navigating the ongoing changes effectively.

The TPA Viewpoint: Adapt or Perish

For TPA firms, AI is both an existential threat and a massive opportunity. Those that embrace AI can fundamentally enhance their service offerings:

Operational Excellence: AI tools like IDP and automated workflows allow TPAs to process higher volumes of claims and administrative tasks faster, more accurately, and often at a lower cost per transaction. This efficiency is critical for maintaining competitiveness.

Enhanced Value Proposition: Beyond efficiency, AI enables TPAs to offer sophisticated analytics, predictive insights, and proactive risk management services, moving them up the value chain from administrators to strategic advisors.

Scalability: AI platforms allow TPAs to scale their operations more easily to accommodate new clients or fluctuating volumes without linearly increasing headcount.

However, adoption requires significant investment in technology and talent. TPAs must retrain staff to work alongside AI, develop new skills in data science and AI governance, and potentially overhaul legacy systems. They also face the challenge of demonstrating transparency and reliability to insurer clients, ensuring that AI processes are auditable and compliant. TPAs that fail to adapt risk becoming commoditized or bypassed altogether.

The Insurer Perspective: Control, Cost, and Partnership

Insurers evaluating their TPA relationships in the age of AI face several strategic considerations:

Cost vs. Control: Does the efficiency gain from a TPA's AI investment outweigh the potential cost savings and control benefits of bringing functions in-house with their own AI solutions?

Technological Capability: Can the insurer realistically build and maintain an AI administration operation that matches or exceeds the TPA's capabilities, considering the required investment and expertise?

Strategic Partnership: Is the TPA merely processing transactions, or are they leveraging AI to provide valuable strategic insights and innovative services that the insurer cannot easily replicate?

Governance and Oversight: How can the insurer ensure adequate oversight, compliance, and accountability when critical administrative functions are managed by a TPA using complex AI algorithms? This requires robust governance frameworks and clear contractual agreements.

Insurers will likely demand more from their TPAs – greater transparency, demonstrable ROI from AI, deeper data integration, and a move towards more collaborative, partnership-based relationships.

The Regulator Angle: Ensuring Fairness, Transparency, and Accountability

Insurance regulators are focused on ensuring that the adoption of AI in claims and administration does not harm consumers or compromise market stability. Key concerns include:

Algorithmic Bias: Ensuring AI models do not perpetuate or introduce biases that could lead to unfair claim denials or discriminatory practices.

Transparency and Explainability: Requiring that decisions made or supported by AI can be explained in understandable terms, especially when challenged by consumers. Black box algorithms are viewed with skepticism.

Data Privacy and Security: Ensuring that the vast amounts of sensitive claimant data used to train and operate AI systems are handled securely and in compliance with privacy laws.

Accountability: Clarifying that insurers remain ultimately responsible for the outcomes of processes outsourced to TPAs, even when those processes involve AI.

Regulators are actively developing frameworks (like the NAIC AI Model Bulletin) to guide responsible AI adoption. They expect insurers and TPAs to implement robust governance, testing, validation, and monitoring processes for their AI systems. Failure to do so could result in significant regulatory scrutiny and penalties.

Security and compliance certifications like SOC 2, ISO 27001, GDPR, and HIPAA are essential considerations when choosing AI platforms for handling sensitive insurance data.

The path forward requires collaboration. Insurers need to clearly articulate their expectations regarding AI use by TPAs. TPAs need to proactively demonstrate the reliability, compliance, and value of their AI investments. Regulators need to provide clear guidelines while allowing room for innovation. Navigating this complex interplay successfully will be crucial for all stakeholders.

Conclusion: The Augmented TPA – Advancing Insurance Administration

The integration of artificial intelligence is undeniably reshaping the landscape of third-party administration in insurance. What was once a field defined by manual processes and siloed legacy systems is rapidly evolving into a domain driven by intelligent automation, predictive analytics, and data-driven insights. AI is not merely optimizing existing TPA functions; it is fundamentally redefining the capabilities and strategic importance of TPAs within the broader insurance ecosystem.

AI TPA software offers tangible benefits: drastically reduced processing times, enhanced accuracy in data extraction and decision-making, proactive fraud detection, improved compliance adherence, and superior customer experiences through personalized communication and faster resolutions. Platforms like V7 Go demonstrate the potential of AI to handle complex, unstructured data and automate intricate workflows, changing document-heavy processes into streamlined, intelligent operations.

However, this technological advancement also introduces new complexities. The competitive tension between insurers potentially insourcing administrative functions and TPAs leveraging AI to become indispensable partners is reshaping industry dynamics. TPAs must innovate continuously to prove their value, moving beyond transactional efficiency to offer strategic insights and advanced analytical services. Insurers, in turn, must carefully evaluate the costs, benefits, and risks of different AI adoption models, ensuring robust governance and oversight regardless of whether functions are managed internally or outsourced.

Critically, the human element remains central. AI capably handles repetitive tasks and analyzes vast datasets, but it cannot replicate the empathy, nuanced judgment, and complex problem-solving skills of experienced insurance professionals. The most effective model is one of AI augmentation, where technology empowers claims adjusters, benefits administrators, and TPA staff to focus on higher-value activities, handle exceptions, and provide the essential human touch in customer interactions.

Looking ahead, the TPA software market will continue to consolidate and evolve. TPAs that successfully integrate AI into their core operations, foster a culture of continuous learning, and build transparent, collaborative relationships with insurers and regulators will thrive. Those that cling to outdated models risk obsolescence.

Ultimately, the successful adoption of AI in TPA software hinges on a shared commitment to using technology responsibly to deliver better outcomes for all stakeholders—insurers, employers, claimants, and regulators. It's about harnessing the power of intelligent automation not just to cut costs, but to build a more efficient, accurate, transparent, and customer-centric future for insurance administration.

Ready to explore how AI can optimize your TPA operations or enhance your partnership with TPAs? Request a personalized demo of V7 Go to see how our AI platform can automate complex insurance workflows and deliver measurable results.

What specific AI technologies are most impactful for TPA software?

Several AI technologies are making a significant impact. Intelligent Document Processing (IDP) combines OCR with NLP and computer vision to extract and understand data from diverse documents like claims forms and medical records. Machine Learning (ML) is used for predictive analytics, such as forecasting claim severity, detecting fraud patterns, and optimizing reserves. Natural Language Processing (NLP) powers chatbots for customer service and analyzes unstructured text in adjuster notes or claimant communications. AI Agents orchestrate complex workflows, combining these technologies to automate multi-step processes like claim adjudication or compliance checks. Platforms like V7 Go integrate these, offering multimodal capabilities and verifiable outputs through features like AI Citations.

+

How can TPAs ensure compliance and ethical AI use?

Ensuring compliance and ethical AI use is paramount. TPAs should implement robust AI governance frameworks that include: Transparency and Explainability (using tools with features like AI Citations to understand AI decisions), Bias Detection and Mitigation (regularly testing models for fairness across demographic groups), Data Privacy and Security (adhering to regulations like HIPAA and GDPR, ensuring data anonymization where appropriate, and using secure platforms), Human Oversight (maintaining human review for critical decisions and complex cases), and Regular Audits (conducting internal and external audits of AI systems and processes). Collaborating with insurers and staying updated on regulatory guidance (e.g., NAIC guidelines) is also crucial.

+

What are the biggest challenges TPAs face when implementing AI?

TPAs face several hurdles: Legacy System Integration (connecting modern AI tools with older core systems can be complex and costly), Data Quality and Availability (AI models require large amounts of clean, relevant data, which may be siloed or inconsistent), Talent Gap (finding and retaining staff with expertise in AI, data science, and AI governance is challenging), Change Management (getting buy-in from staff and adapting existing workflows requires careful planning and communication), Cost of Investment (significant upfront investment in technology and training is often required), and Ensuring ROI (clearly defining use cases and measuring the tangible benefits of AI implementation).

+

How does AI change the skill set required for TPA professionals?

AI shifts the required skill set from manual data entry and routine processing towards higher-value activities. TPA professionals increasingly need: Data Literacy (understanding AI outputs, basic analytics, and data quality concepts), Tech Savviness (comfort working with AI tools, workflow automation platforms, and digital communication channels), Critical Thinking and Problem Solving (analyzing complex cases flagged by AI, handling exceptions, and making nuanced judgments), Compliance and Ethical Awareness (understanding the regulatory and ethical implications of AI use), and Communication Skills (explaining AI decisions to clients and stakeholders, and collaborating effectively in hybrid human-AI teams).

+

Can smaller TPAs realistically adopt and benefit from AI?

The future is likely one of augmentation, not replacement. AI will automate many routine administrative and claims processing tasks, leading to greater efficiency and accuracy. This will push TPAs to evolve, focusing more on complex claims management, strategic advisory services (leveraging insights derived from AI), specialized risk management, and providing enhanced customer experiences. The TPA-insurer relationship will likely become more collaborative, focused on shared data and innovation. TPAs that successfully integrate AI and demonstrate its value will thrive, while those slower to adapt may face consolidation or marginalization. AI proficiency will become a key differentiator in the TPA market.

+

What is the future outlook for the TPA industry in the age of AI?

Go is more accurate and robust than calling a model provider directly. By breaking down complex tasks into reasoning steps with Index Knowledge, Go enables LLMs to query your data more accurately than an out of the box API call. Combining this with conditional logic, which can route high sensitivity data to a human review, Go builds robustness into your AI powered workflows.

+

Casimir is a seasoned tech journalist and content creator specializing in AI implementation and new technologies. His expertise lies in LLM orchestration, chatbots, generative AI applications, and computer vision.