High throughput fund

screening.

Independent pre-transaction fund pricing at population scale. For secondaries underwriting, primary diligence, and NAV finance.

Every fund commitment, every secondary bid, and every NAV facility is priced off marks that have never been independently tested. We describe a high throughput screening platform, built on a portfolio company knowledge graph, that extracts structured valuation primitives from thousands of fund documents per quarter and returns defensible pricing inputs, every figure traceable to source, before transactions close.

01 / Background

The pricing step nobody runs.

Private capital AUM has crossed $13 trillion. Every commitment, LP stake, and NAV facility in the market is priced off numbers written by individual GPs on reporting templates, and those numbers are almost never tested against what other holders of the same companies reported in the same quarter. The input to the largest private transactions in the world is the output of a single unreviewed assay.

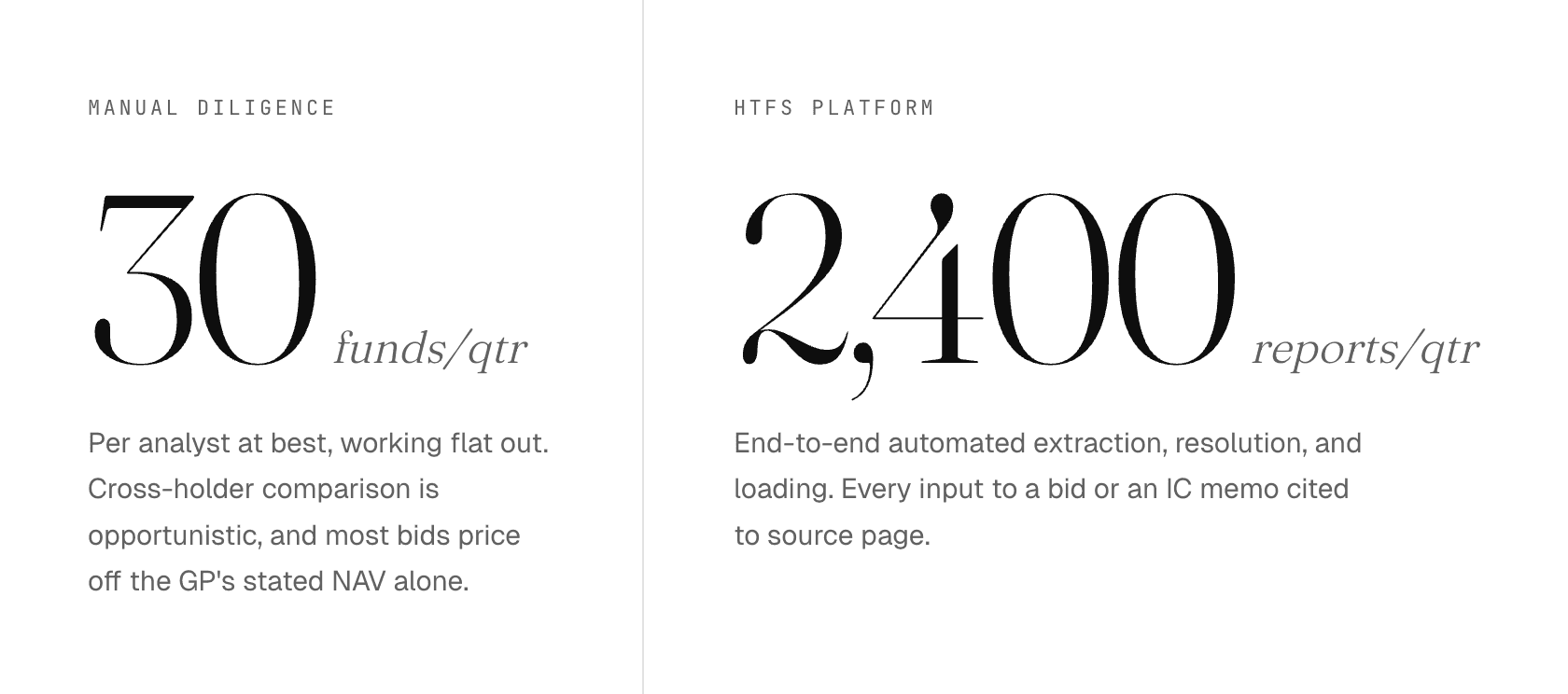

The reason is mechanical: the data lives in unstructured PDFs, and a good diligence analyst can price twenty to thirty funds per quarter working flat out. Secondaries houses, allocators, and lenders routinely transact on marks they have sampled rather than screened. For any given portfolio company, cross-holder dispersion is wide, persistent, and almost entirely unmeasured at the point of sale.

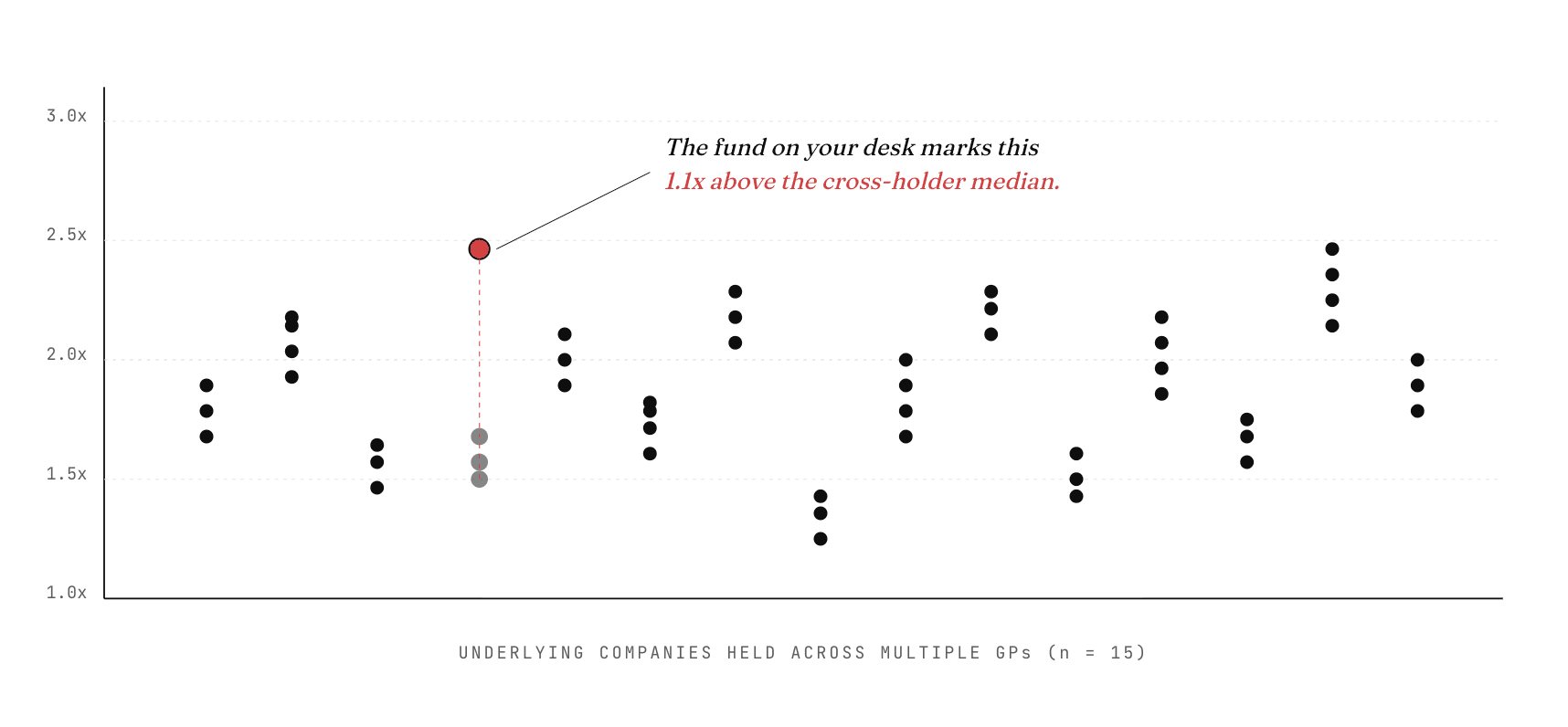

Fig. 01 / Cross-holder mark distribution at reference quarter. Each column shows what multiple independent GPs said the same company was worth on the same date. The red point sits above the cross-holder median by a margin that changes how an incoming LP stake should be bid.

02 / Throughput

Pricing capacity against the deal clock.

Every private market transaction runs on a clock. Secondaries bids close within days, primary allocations clear IC inside a defined window, and NAV facilities are sized against a quarter-end mark. The question is not how many funds a team can price in principle, but how many they can price before the deadline.

03 / Platform Design

The discovery analogy, made literal.

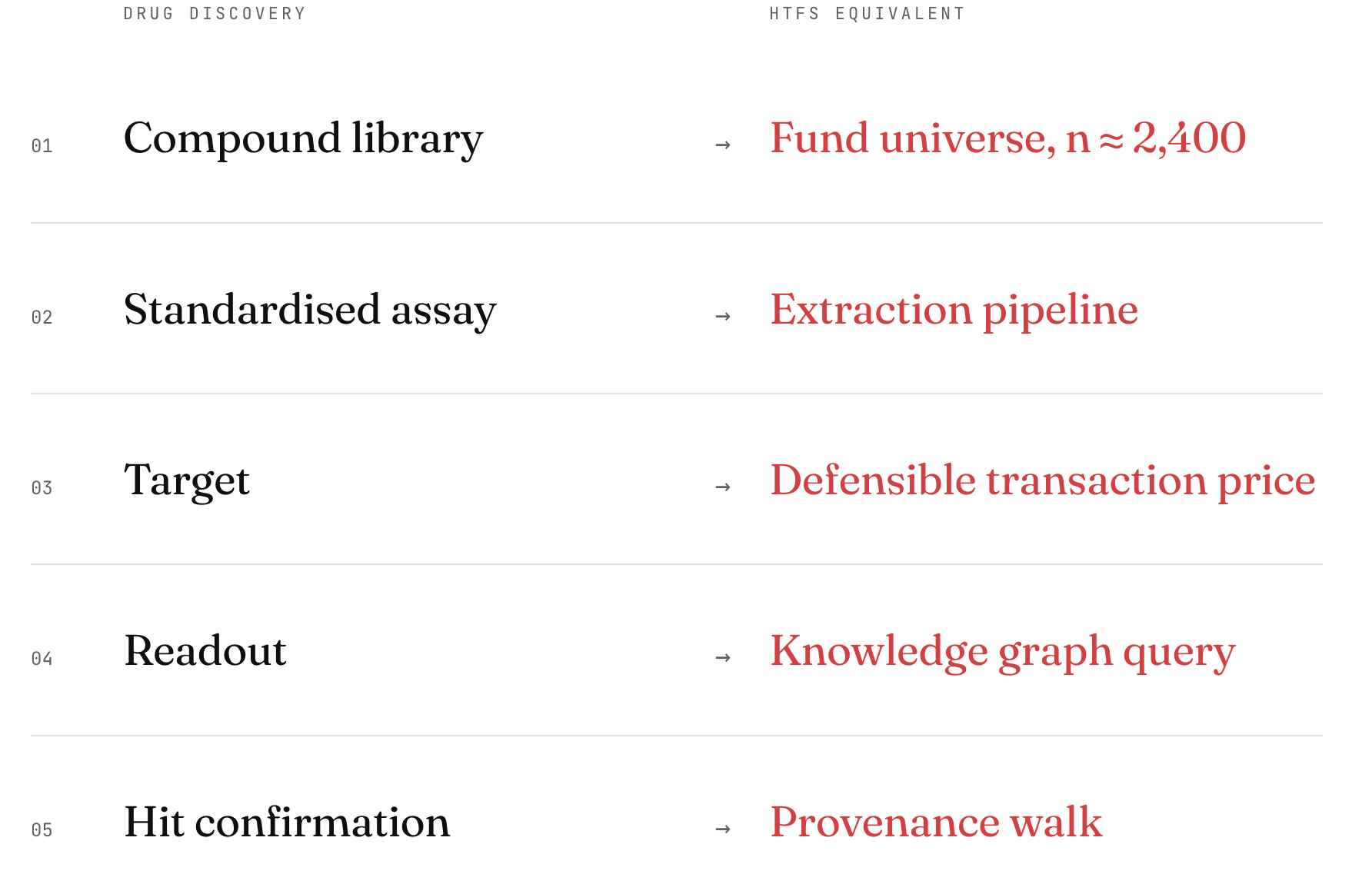

The platform is structured like an early-stage drug discovery campaign: a library of candidates, a standardised assay, a defined target, a readout that filters for hits, and a confirmatory step before anything advances. Pre-transaction fund pricing is the screening step, and the fund on your desk is the compound under test.

04 / The Graph

A relational ontology of private markets.

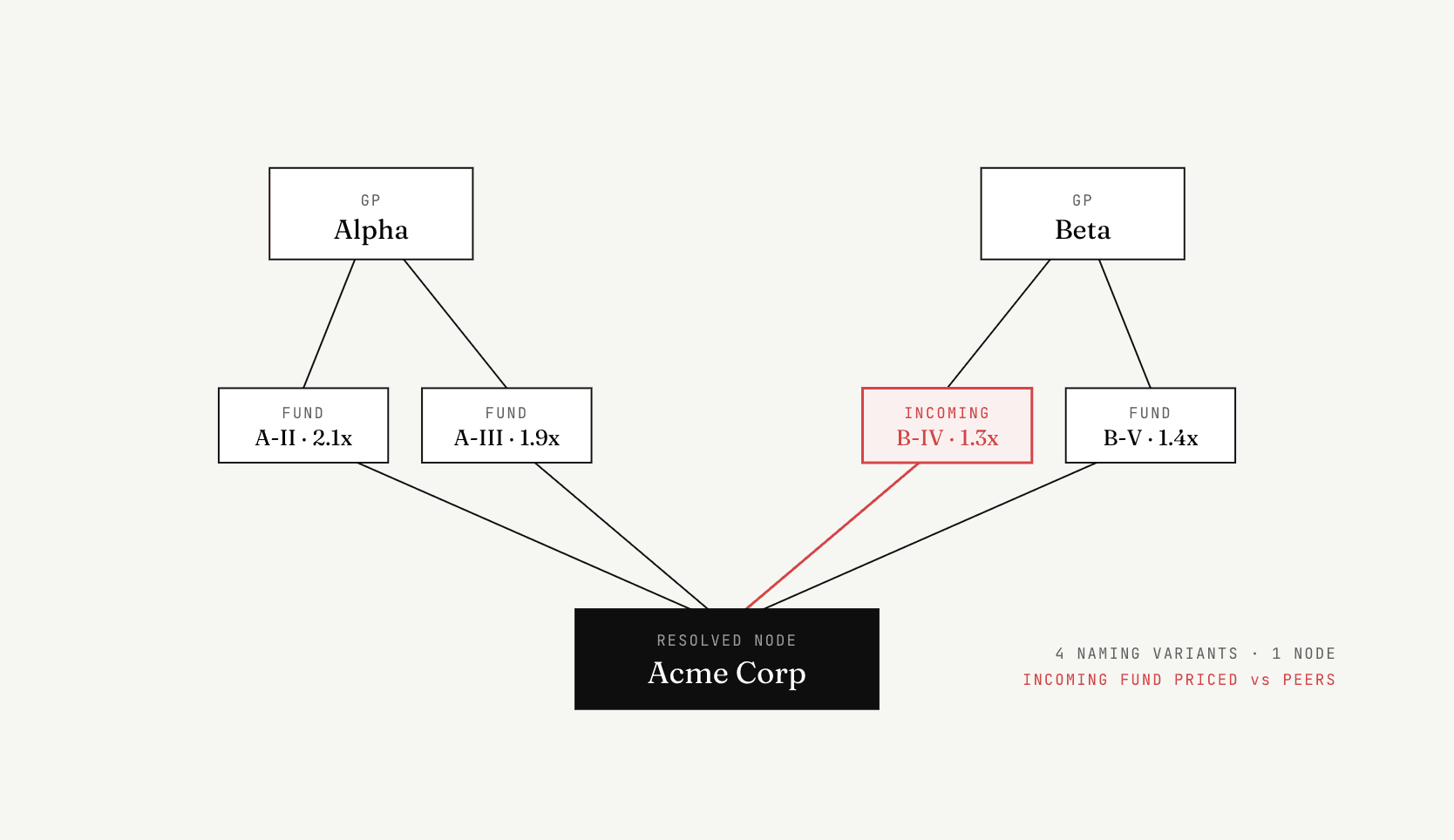

At the centre of the platform sits a knowledge graph. Nodes represent companies, GPs, funds, vintages, and sectors; edges encode holding, management, co-investment, and comparability. The hardest step is entity resolution, which collapses naming variants so that a single company held across six funds maps to one node. Without it, incoming funds cannot be priced against their peers.

Fig. 02 / Pricing an incoming LP stake. The resolved node collapses naming variants across four holdings. The fund under evaluation is positioned against the peer distribution before a bid is entered.

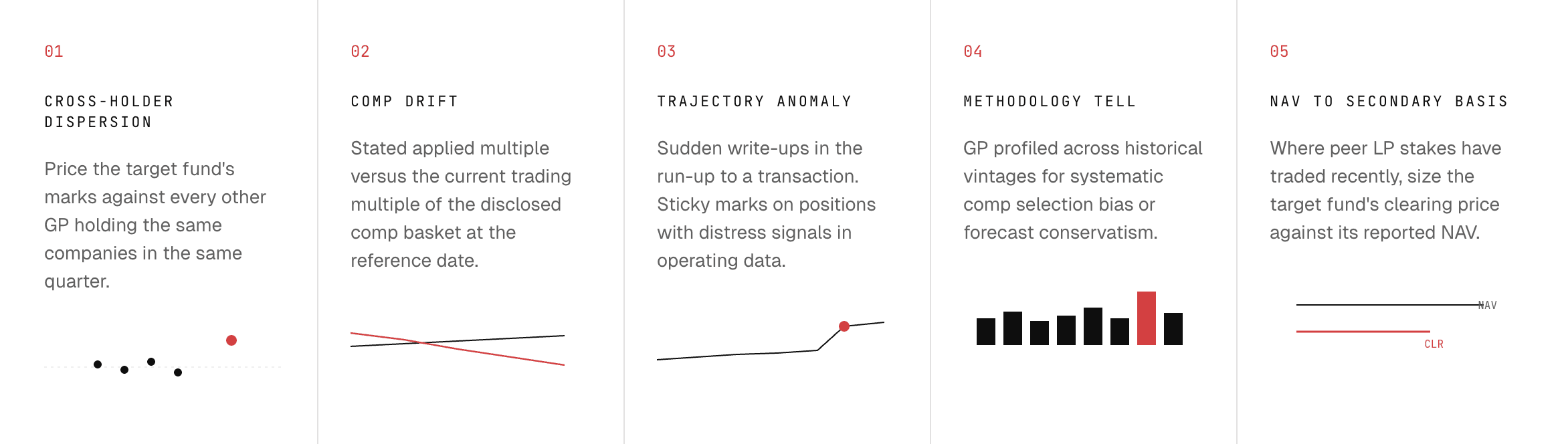

05 / Screens

Five primary endpoints.

Each endpoint is a quantitative rule that runs over the graph and returns a pricing signal on the fund under evaluation. A hit is a question raised, not a conclusion reached; the confirmation step lives in Section 06.

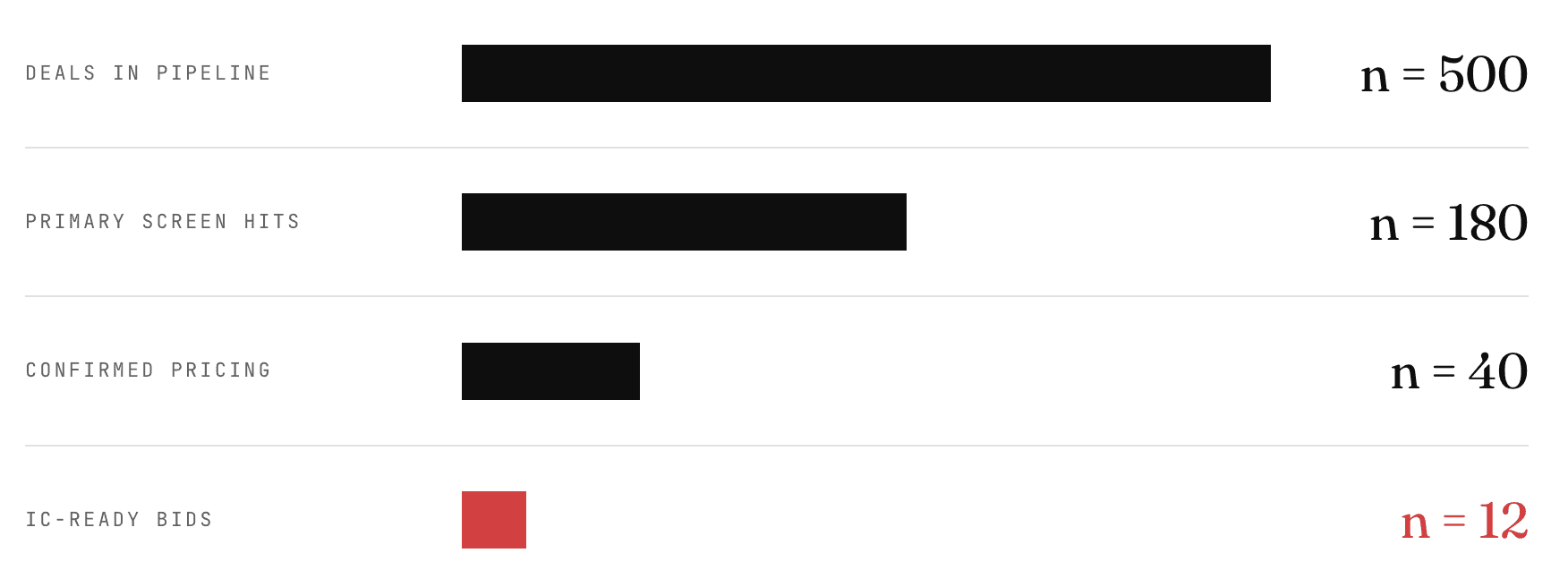

06 / Secondary Validation

Hit to bid.

Primary hits are not biddable on their own. Each flagged position is routed through a confirmatory workflow that reconstructs the valuation bridge and checks whether the signal survives a fully cited walk from cost to current mark. The analogue is a confirmatory dose response assay: its job is to filter false positives before anything reaches an investment committee or a bid letter.

Fig. 03 / Illustrative funnel for a secondaries underwriting team. Only a small fraction of primary hits survive provenance-backed validation, which is by design.

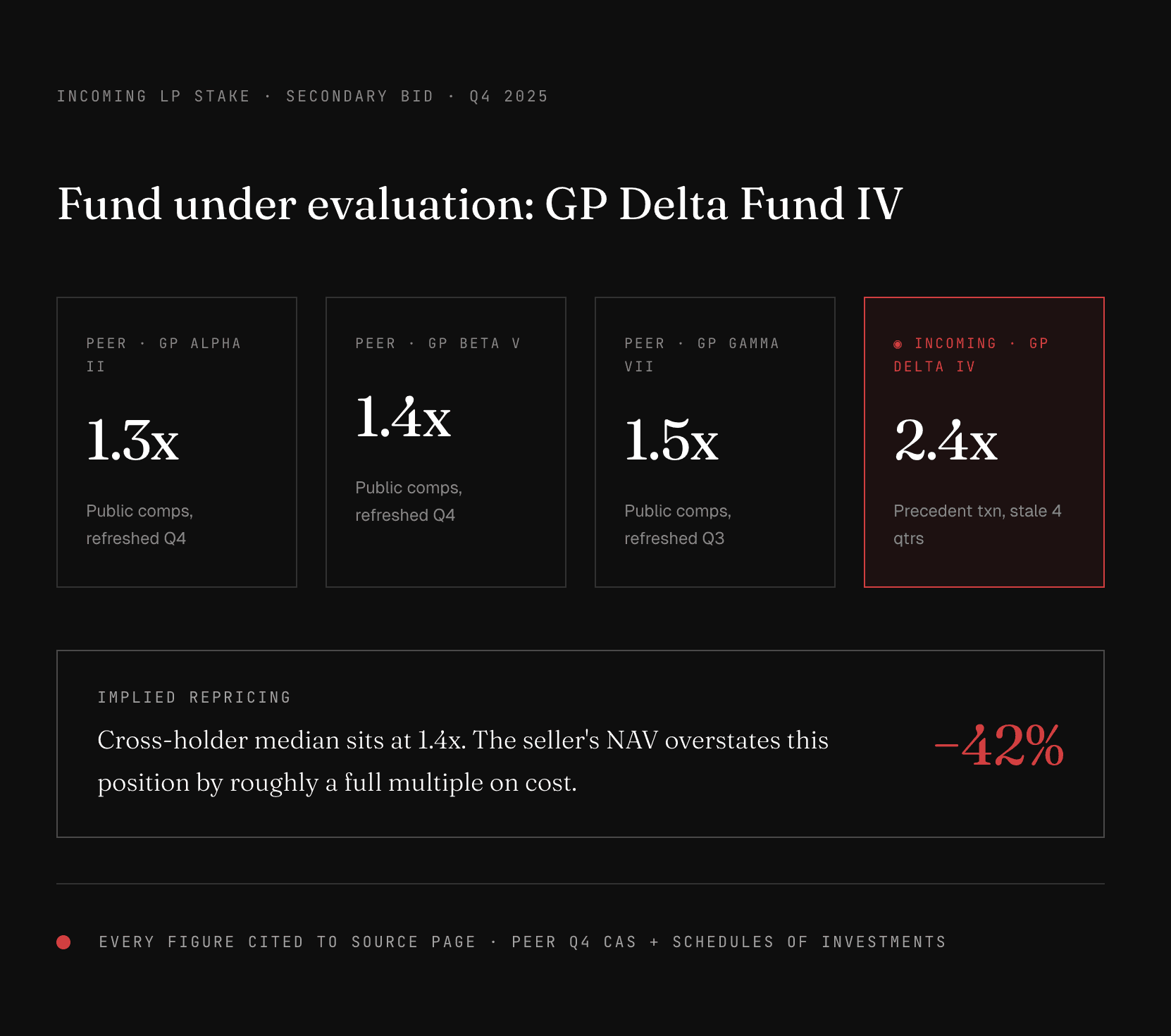

07 / Illustrative Pricing

A mark priced before a bid.

A secondaries buyer receives a call on an LP stake in a mid-market buyout fund. The seller's reference NAV implies a 2.4x mark on the largest position, and three other GPs hold that same company on the same reference date. The screen runs in minutes.

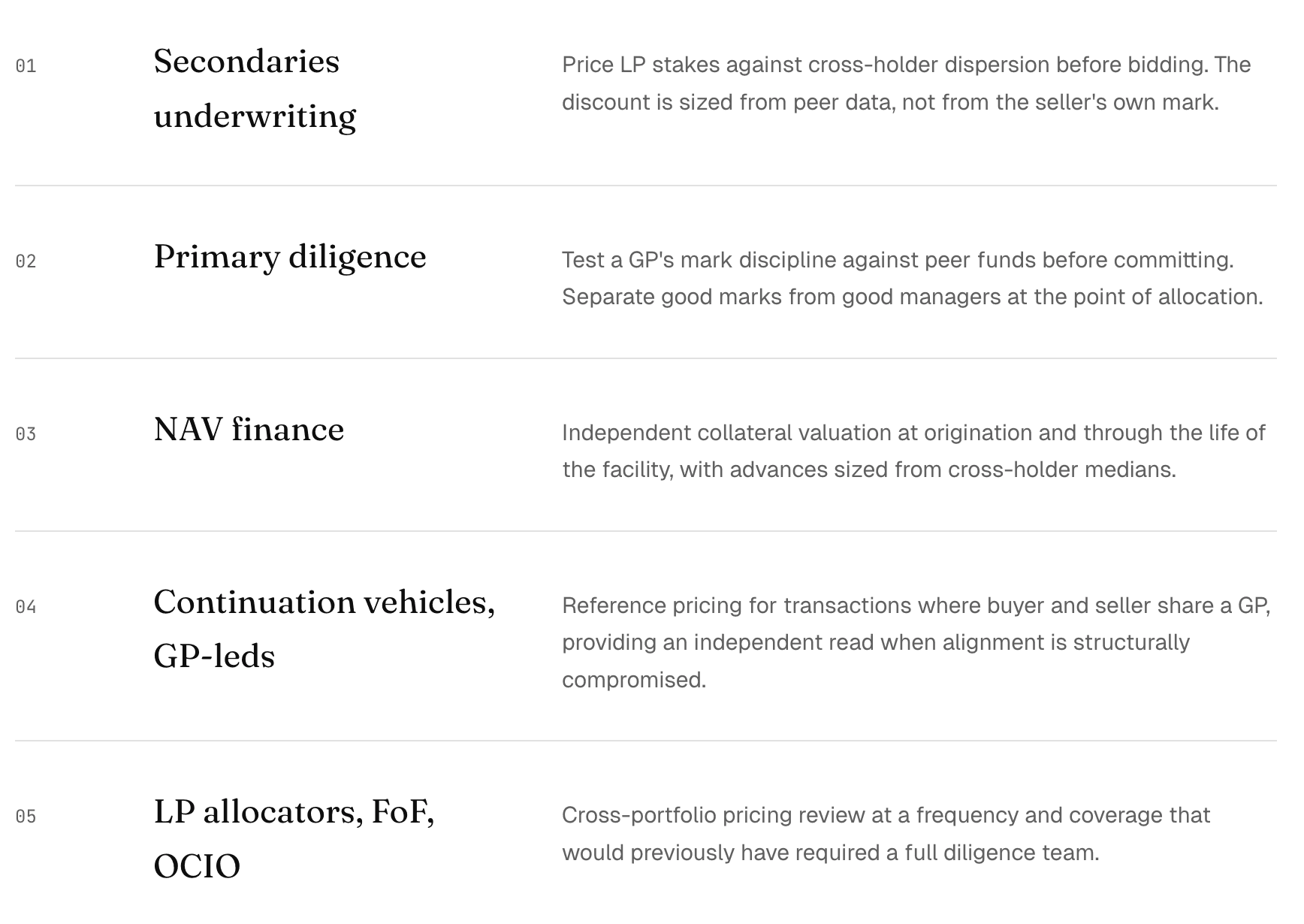

08 / Applications

Who this is for.

The Wedge

Provenance is the

product.

Any screen can generate a list. A defensible screen, where every number is traceable to a source page, clears the bar for a bid letter, an IC memo, or a lending decision. The platform is generative as well as diagnostic: each quarter's data enriches the graph and tightens the pricing baselines, so the assay gets more sensitive over time.