21 min read

—

AI for property appraisals promises faster valuations, richer insights, and new efficiencies, but it also raises important questions. This is your complete guide.

For decades, valuing a home meant long hours in the field and even longer ones back at the desk. An appraiser would drive to the property, measure every room, and carefully inspect each detail before heading back to the office to research comparable sales.

Only then could the real grind begin: combing through records and painstakingly entering every data point into spreadsheets and appraisal forms.

These methods, while thorough, were slow and sometimes inconsistent due to subjective judgments and limited data.

Things are beginning to look quote different. AI tools are now being used to automate everything from data collection and photo analysis to market forecasting and quality control.

Many appraisal professionals are asking fair questions. What tasks can AI realistically take over? Where does human oversight remain essential? And most importantly, will these tools compliment or erode the role of the appraiser?

In this article, we’ll explore:

The state of modern property appraisal

How AI is being used in property appraisal and valuation

Tangible benefits and risks

Best practices for using AI responsibly

The best AI tools for property appraisal

What the future may hold

AI for document processing

Automate appraisal document analysis at scale

Get started today

What is the Purpose of Property Appraisal?

The primary purpose of a property appraisal is to provide an objective, evidence-based opinion of a property’s current market value. Location, condition, size and comparable sales are all taken into consideration.

Appraisals give lenders, buyers, sellers, investors, and regulators a trusted reference point for making financial decisions, helping to:

Support fair lending and risk management

Establish market value for transactions

Settle legal and financial matters

Inform investment and portfolio decisions

Enable insurance and tax accuracy

An article about real estate appraisals from an October 10th, 1930 edition of the New York Times. The tools have changed, but the core principles of property appraisal have not.

As AI tools enter the workflow, the fundamental goal remains the same: provide an accurate estimation of value backed by transparent data and professional oversight.

Appraisals are important in nearly every aspect of a real estate deal, whether it is originating a loan, working out a loan, the decision to buy or sell a property and even bankruptcy.”

— Jay A. Neveloff

Modern Property Appraisals

Today’s appraisal process looks very different from the clipboard-and-calculator days. Digital data standards, and powerful AI tools are streamlining tasks that once took hours or days.

In the U.S, appraisal modernization efforts led by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac are accelerating this shift. One key innovation is the hybrid appraisal, where a trained inspector collects standardized property data using the Uniform Property Dataset, and a certified appraiser completes the valuation remotely.

Results showed that loans using AI-assisted hybrid appraisals had comparable quality and performance to traditional appraisals.

Hybrid models are only the beginning when it comes to the modernization of appraisals. AI is now touching every part of the appraisal lifecycle, from automated valuation models and computer-vision photo analysis to document processing and real-time market forecasting.

The sections that follow highlight the most impactful use cases and explain how these tools are enhancing accuracy, speed, and consistency while keeping the appraiser firmly in control.

AI Agents for Property Appraisal

AI agents are a great example of using AI for property valuation insights at scale. Unlike traditional software that follows fixed rules or scripts, these agents combine large language models, data access, and reasoning to perform dynamic, context-aware tasks.

They can read appraisal reports, interpret property data, analyze comparable sales, and even cross-check findings for consistency, all while following defined instructions and guardrails.

Modern platforms like V7 Go make it easy to design and deploy these agents. To learn more, read our blog What Are AI Agents and How to Use Them or check out the V7 Go Property Valuation Agent here.

AI Use Cases for Property Appraisal

Below are five core use cases where AI is already reshaping modern property appraisal and valuation. Each represents a distinct stage of the process where automation and machine learning deliver measurable gains in speed, accuracy, and compliance.

1. Automated Valuation Models (AVMs)

Automated Valuation Models are algorithmic systems that estimate a property’s market value using statistical and machine-learning techniques. They crunch data from comparable sales, property characteristics, and market trends to generate a value, often in seconds, without a physical inspection.

Mortgage lenders use AVMs for preliminary valuations, appraisal waiver decisions, portfolio monitoring, and as a “second opinion” alongside human appraisals. Online real estate portals also use AVMs to give consumers instant home value estimates.

They have been around for decades in basic forms, but modern AI has greatly increased their accuracy and usage.

Zillow’s popular Zestimate AVM reports a nationwide median error of only ~1.8% for homes that are on the market. This level of accuracy approaches that of human appraisals for many standard properties, and shows what large-scale machine learning models can achieve.

Going forward, we can expect AVMs to become steadily more accurate as they tap into richer datasets and more advanced AI techniques.

Limits to AVMs

Zillow itself acknowledges its estimates are not a substitute for an appraisal. Unique or high-end properties, or those in rural markets with few comps, can confuse AVMs. And an AVM can’t personally inspect a home’s interior or neighborhood nuances, so it might misvalue a house that has unseen damage or special features.

AVM estimates are always most accurate for properties that are similar in nature and condition to those around them.

These models need extensive, representative data to perform well, and quality is critical.

Policy and Regulation – “The AVM Rule”

The growing reliance on AVMs has prompted regulators to set quality control standards. In June 2024, U.S. federal agencies adopted an Interagency Rule on AVMs that requires anyone using AVMs in credit decisions to maintain robust controls.

This rule outlines five key requirements for AVMs:

Ensure a high level of confidence in the estimates produced;

Protect against the manipulation of data;

Seek to avoid conflicts of interest;

Require random sampling testing and reviews; and

Comply with applicable nondiscrimination laws.

In the UK, RICS’s upcoming standard will require appraisers to keep records of AI testing and data sources and to inform clients when an automated model is used.

All this governance may sound like extra work, but it ultimately builds trust in AI-assisted valuations.

2. Computer Vision for Property Condition

While AVMs handle the “number-crunching” of comparable sales and market data, another challenge in appraisals is assessing a property’s condition and features.

This has traditionally required human eyes on site to identify things like a new kitchen vs. a dated one, a well-maintained roof vs. one with damage, or whether a home’s quality is “Average” or “Good” by appraisal standards.

AI is helping to close this “condition gap” through computer vision.

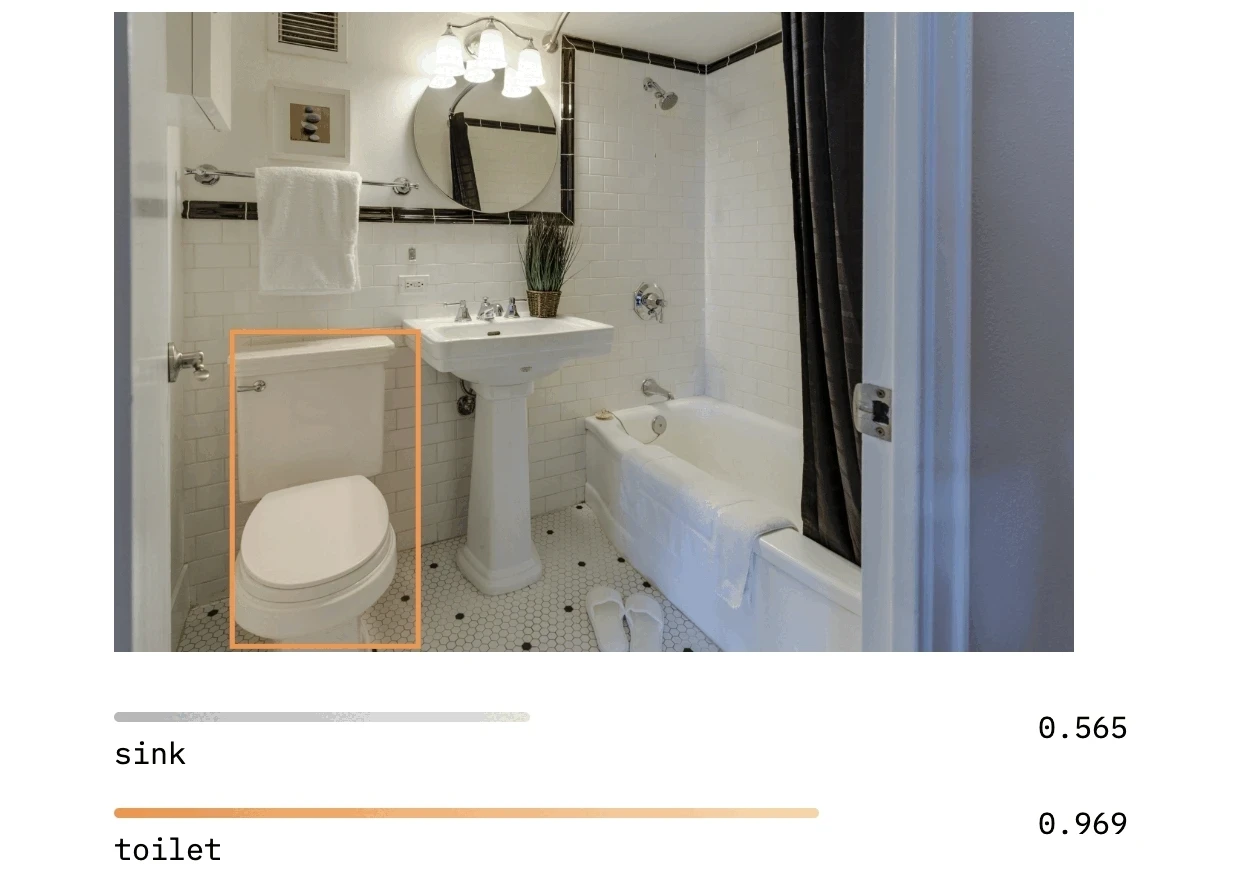

Computer vision for inspections

Modern appraisals involve a lot of photos, both of the subject property and comparable homes. It’s not uncommon for an inspector to take 30-50 interior and exterior photos of a single house.

Computer vision models can automatically detect property features. Does the kitchen have granite countertops? Is there a crack in the foundation wall? What is the architectural style?

They can also judge property condition from images, scoring things like curb appeal, interior condition, or quality of materials.

Photo quality and coverage for reporting

An AI vision system can verify that all required photos in an appraisal report are present (front, sides, street, all key interior rooms) and clear (not too dark or blurry.)

This prevents a common issue where a lender or AMC finds an appraisal incomplete due to missing or poor photos, requiring a second visit.

“No one likes it when borrowers are inconvenienced more than once for an appraiser or data collector to enter their homes and take more photos. This new technology eliminates the possibility of leaving the property site with poor-quality pictures or incomplete data collection.”

— Tony Pistilli, Appraisal Buzz

Avoiding misrepresentation or errors in condition ratings.

A recent white paper analyzed over 1,200 appraisals with AI and found a significant risk in 1 out of every 3 appraisals related to condition or quality adjustments that didn’t match the home’s actual state.

By using computer vision to evaluate photos, lenders and appraisers can catch these issues early. The AI might flag, for instance, that the subject property’s photos show a renovated kitchen, yet the appraisal didn’t adjust for condition, or conversely that a comp was rated “Excellent” despite photos suggesting deferred maintenance.

Armed with those alerts, a reviewer can ask the appraiser to justify or correct the report before the loan is made, reducing risk and keeping the human-in-the-loop.

Geospatial imagery

AI can be used to scan aerial and satellite images for property features. Does the house have solar panels? Is there overgrown vegetation indicating poor maintenance?

This can be done on millions of homes continuously, providing insurers and lenders with up-to-date condition data even without an in-person inspection.

You can learn more about computer vision in our blog, What Is Computer Vision? [Basic Tasks & Techniques]

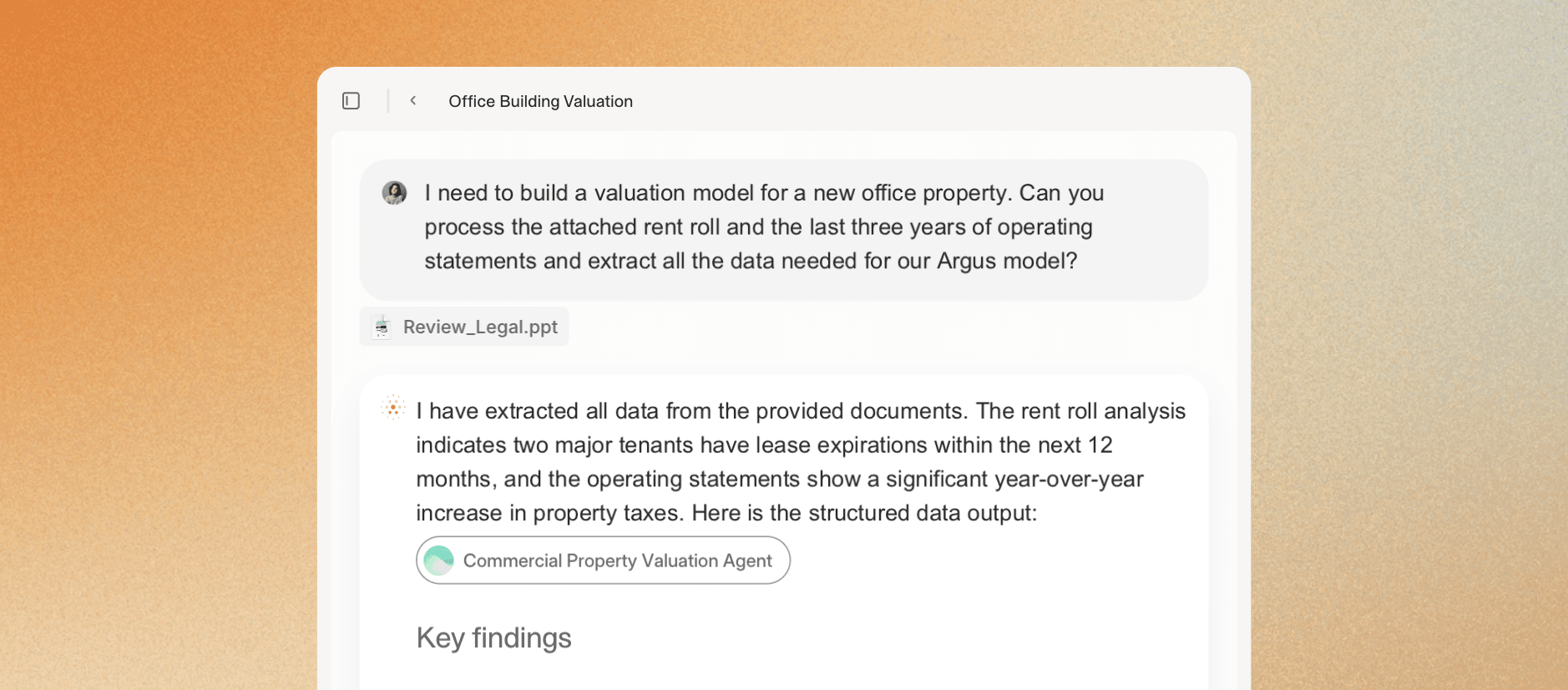

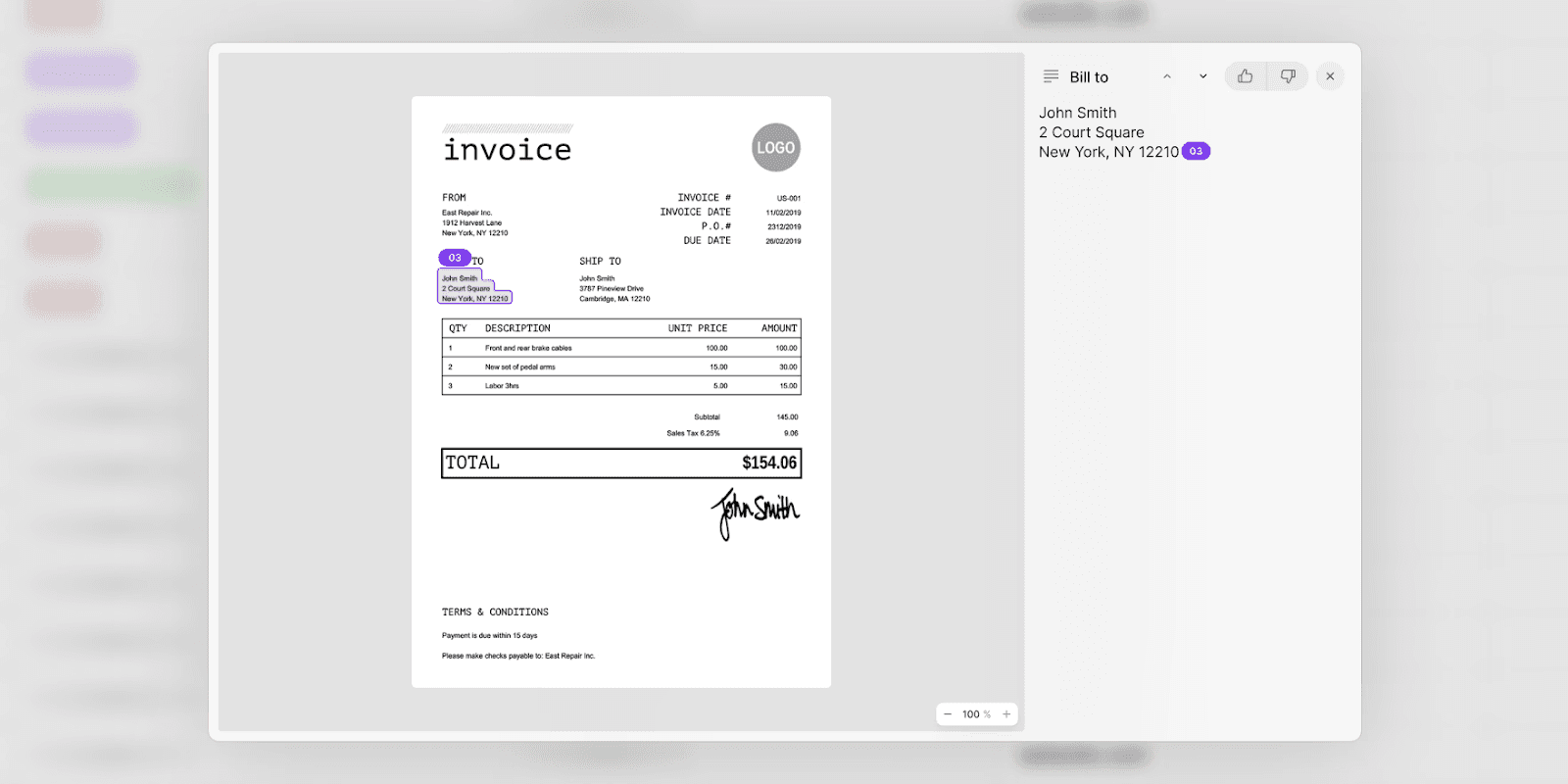

3. Document AI and Reporting Automation

In property appraisal, much of the work involves handling documents such as inspection reports, deeds, tax records, zoning permits, prior appraisals, and financial statements.

Traditionally, appraisers have manually reviewed these documents, pulled out key data by hand (square footage, lot size, building condition, prior sale history), and typed it into their report forms. This manual process is both time-consuming and error-prone: misreadings, typos, missing pages, or incomplete data are all common, and can lead to inaccurate valuations or extra work later for underwriters or lenders.

Leading Document AI platforms can automate extraction of structured data from all kinds of real-estate documentation. It can spot inconsistencies, flag missing or contradictory information, standardize inputs (so “sq ft” or “square feet” or “m²” get treated uniformly), and even read handwritten notes or scanned documents.

Given the variety of formats in the typical property appraisal workflow, multi-modal ingestion is vital for document automation.

V7 Go is purpose-built to automate your document workflows, seamlessly ingesting and analyzing documents of every type and format.

AI for Property Appraisal Report Writing

Appraisal reports are lengthy documents, typically 30+ pages including forms, narratives, photos, and certifications. Compiling and reviewing these reports is a time-consuming task in itself.

AI is streamlining the reporting process through automation of writing and quality checks.

Large language models are increasingly leveraged by appraisers to draft parts of the appraisal. For example, an appraiser can prompt an AI with data about a neighborhood and get a first draft of the “Neighborhood Description” or “Market Conditions” commentary.

This is akin to having a junior assistant who writes up an analysis which the appraiser then tweaks. The appraiser must always verify that the AI’s text is correct and compliant.

Automated Completeness Checks

Before an appraisal report is delivered, it goes through internal review to catch any omissions or errors. Did you forget to add the interior floor plan sketch? Did you leave the reconciliation comment blank?

AI can automate a lot of this quality control. For instance, an AI system can scan the appraisal and the attached data to ensure that every required field is filled and consistent. If the form says the roof is “Composition shingle” but the addendum narrative mentions “metal roof,” that inconsistency could be flagged.

Lenders and regulators also have lists of forbidden phrases or requirements (for example, Fannie Mae doesn’t want to see subjective terms like “pride of ownership” in the report). AI can easily be trained to highlight any such phrases for removal.

Audit Trails and Explainability

Using AI in reporting also allows for better audit logs. Each suggestion or automated section can be recorded, showing how the report was built.

This is useful for governance. If later someone asks “how did you arrive at this comment or value?” There is a trace of the data fed into the AI, the output given, and any changes made by the human appraiser.

Citations in V7 Go

V7 Go is built for explainability, with visual grounding that shows exactly where your AI found its information. This allows for instant verification of generated responses, reduces hallucinations, and makes QA easier than ever.

Every step taken by an AI agent, every query, and every result is logged. You have a complete, accessible and transparent audit trail for compliance and internal review.

4. Risk & Fraud Detection

AI is increasingly used to detect anomalies and potential fraud in the appraisal process before loans close.

While these fraud flags can include anything from income misrepresentation to identity theft, appraisal valuation fraud (inflating value to get a bigger loan) is a perennial concern.

The goal of AI in review is to direct attention to the riskiest cases. Every appraisal can be scanned, and those with warning signs get a human in-depth review.

Anomaly Detection in Valuations

One straightforward application is comparing an appraised value to a model estimate or to statistical norms for that neighborhood.

Lenders usually have internal tools that score appraisals on risk. Modern versions use machine learning to combine many factors, such as the appraiser’s track record, the property specifics, comparable selection, and market trends, to predict the likelihood an appraisal is overvalued.

Those with high-risk scores get flagged for in-depth review.

A submission is automatically flagged in V7 Go

Consistency and Comparables Analysis

AI can also scrutinize the chosen comparable sales in an appraisal. It also can check if there were other recent sales nearby that the appraiser didn’t use but that might be more similar.

For example, if two comps are identical in quality but the appraiser gave one a big condition adjustment and not the other, that inconsistency could be a red flag. While there are legitimate reasons to exclude certain comps, those appraisals may get an extra look for possible bias or manipulation.

Image and Document Forensics

Another risk area is the integrity of the photos and documents themselves. There have been fraud cases where an unscrupulous actor reused photos from a different house or digitally altered images to hide defects.

AI-based image recognition can compare photos against databases of known images to ensure the photos actually match the property address and aren’t stolen from elsewhere. It can sometimes detect if an image has been edited or staged, for instance, signs of Photoshop in pixel patterns.

Even things like comparing the date/time stamps in photo metadata against the reported inspection date can be automated.

Patterns of Collusion or Bias

AI can also look at aggregate patterns, which is useful for regulators or large lenders auditing many appraisals. If a certain appraiser or brokerage always comes in 20% higher than AVM values in a certain neighborhood, that pattern might indicate inflated valuations or pressure to hit target values.

Conversely, if certain areas see systematic undervaluation, that can be spotted too. The PAVE task force in the U.S. is concerned with discriminatory appraisal bias; AI analysis can help reveal if properties in minority neighborhoods consistently get more conservative valuations than similar homes in white neighborhoods.

Such findings can then be addressed through training or policy changes.

5. Market Forecasting & Live Insights for Valuation

A property’s value today is one thing, but what about tomorrow?

Appraisers and investors are always looking at market trends to judge whether prices are rising, stabilizing, or declining. Traditionally this relies on expert opinion and lagging indicators. AI offers a way to bring more data-driven forecasting into property valuation, by analyzing real-time signals and big-picture trends that humans struggle to synthesize.

We are not so brazen as to believe that we can perfectly calibrate valuation; determining risk and return for any investment remains an art not an exact science.

— Seth Klarman

Predictive Modeling for Prices

Real estate data often comes at low frequency, from monthly sales reports to quarterly indices. But AI models can be trained to forecast future price movements by feeding on a wide range of higher-frequency inputs:

Macroeconomic data (interest rates, employment, GDP growth)

Local economic indicators (job openings in the city, building permits, migration patterns)

Real estate market data (inventory levels, days on market, list-price-to-sale-price ratios)

Geospatial maps and satellite images (transit points, green spaces, highways)

Even less conventional data like social media sentiment or Google search trends for real estate.

By finding patterns in how these factors correlate with past price changes, the AI can predict, for example, that “homes in this zip code are likely to appreciate 5% in the next six months” or flag that a certain condo market is overheating and due for a correction.

AI can provide a more immediate and holistic view of property valuations, drawing from a wide variety of less obvious data points.

Reducing subjectivity

A common critique of appraisals is that the market condition adjustments or trend analyses can be subjective. Some appraisers might be pessimistic and undervalue in a rising market. Others might be too optimistic. If applied properly, AI forecasts can provide a more objective anchor.

Of course, forecasts are not crystal balls. AI predictions can be wrong, especially in the face of “black swan” events.

Human appraisers will still apply judgment to these insights. The role of AI here is to provide a data-rich perspective that helps appraisers and lenders make more informed decisions about risk. For instance, a lender might require stricter review on a loan in a city where AI predicts a downturn.

Benefits of AI-Powered Real Estate Appraisals

With these use cases we see AI woven through the entire appraisal process.

Next, let’s summarize what benefits this brings in practice, and then discuss the risks and how they can be managed.

Below are some of the key advantages:

Accuracy & Consistency: AI analyzes huge datasets to uncover patterns even seasoned appraisers might miss. Using the same criteria every time reduces human bias and delivers more evidence-based, defensible valuations (with ongoing checks to prevent bias in the data).

Speed & Scale: Tasks that once took days like collecting property data, finding comps, running calculations can be done in hours or minutes. Faster appraisals help loans close sooner and let firms handle more volume.

Cost Savings: Cutting manual work also reduces per-report labor costs and rework. Lenders save on rate-lock extensions and avoid costly buybacks caused by appraisal errors.

Transparency for Clients: Online AI valuation tools can help make market data visible to buyers and sellers, building trust. Clear visualizations and explanations help consumers understand how a value was reached.

Fraud Detection & Compliance: AI screens every appraisal for anomalies, deters bad actors, and flags potential bias or regulatory issues. Continuous monitoring strengthens fairness and protects lenders, communities, and borrowers.

That said, reaping these benefits depends on using AI correctly. Poor implementation or blind reliance on AI can introduce new risks.

Risks and Best Practices for AI in Property Appraisal

While AI offers many advantages, it also comes with risks and challenges that must be managed. Below we outline the key risks and the best practices to ensure AI is used responsibly in the appraisal process.

Key Risks

Risks appraisers need to be aware of when using AI include, but are not limited to:

Data Bias and Fairness Issues

AI models learn from historical data, which may reflect past biases or discrimination. If not addressed, a model could systematically undervalue homes in minority neighborhoods simply because those areas were historically undervalued due to bias, not true market factors

This is a serious risk because it can perpetuate inequity under the guise of algorithmic objectivity.

While machines crunching numbers might seem capable of taking human bias out of the equation, they can’t. Based on the data they are fed and the algorithms they use, automated models can embed the very human bias they are meant to correct.

— Rohit Chopra, Consumer Financial Protection Bureau

“Garbage In, Garbage Out”

AI is only as good as the data it’s using. Incomplete, incorrect, or unrepresentative data will lead to flawed valuations. For example, if an MLS feed has wrong square footage or missing renovation info, the AVM’s estimate will be off. If an AI vision system is trained mostly on mid-range homes, it might mis-evaluate a luxury property’s photos.

Over-reliance and Misapplication

There is a risk that users may place too much trust in AI outputs without understanding their limitations. An AVM might be very accurate on average but still make large errors in individual cases. If a lender blindly relies on an AVM for a property that has no good comparables, say a custom-built log mansion, they could severely misprice the loan.

Likewise, appraisers using AI suggestions need to remain critical; the tool might suggest a wrong comp or a poor adjustment.

Misapplication can also mean using an AI or an AI-powered tool beyond the scope it was designed for. For instance, using a residential AVM for a commercial property would be inappropriate.

Regulatory and Legal Non-Compliance

The use of AI in valuations is coming under regulatory scrutiny. If an AI model’s decisions cannot be explained, that might conflict with appraisal standards that require rationale for adjustments and value conclusions.

There are also fair lending laws, and if an AI-driven valuation process results in disparate impacts on protected classes, lenders could face liability. The new Interagency AVM Rule explicitly requires compliance with nondiscrimination laws and regular testing. Failure to implement these controls could lead to penalties or having to pull AVMs from use.

V7 Go complies with leading privacy and regulatory requirements

Additionally, privacy laws (like GDPR in Europe) affect how you can use personal data in AI. If an AI tool uses data without proper consent, for example, scraping photos or social media posts, that could be a legal violation.

Firms must be careful to use trusted vendors and have agreements in place to protect the data.

Job Impact and Change Management

Appraisers and support staff might feel threatened by automation, leading to resistance or morale issues. If not handled well, this could result in underutilization of the AI tools (people might ignore the AI or use it incorrectly) and loss of valuable human expertise.

"Employee engagement is an investment we make for the privilege of staying in business"

— Ian Hutchinson

When teams are included in the process, given proper training, and shown how AI reduces repetitive work, attitudes shift quickly.

Best Practices for Responsible AI Use

These risks can be mitigated, and your AI implementation made more successful, through following some key best practices.

Build a Solid Data Foundation

Like a building, the best AI implementations rest on a strong foundation. Prioritize data accuracy, completeness, and diversity. Invest in cleaning data and establishing strict data entry standards.

Use multiple data sources to cross-verify (e.g., public records + MLS + homeowner-provided data) so the AI isn’t relying on a single potentially flawed source.

Regularly audit the data feeding your models to root out errors and update outdated info. Encouraging data diversity in model training helps the AI perform better across the board and avoid blind spots.

Ensure Transparency and Explainability

Use AI systems like V7 Go that can provide insight into how they arrived at a given result, or at least don’t operate as an inscrutable black box for critical decisions. For AVMs, this might mean models that output not just a value but also the top factors or comps influencing that value.

Treat your AI models as you would any critical process, with proper governance, validation, and periodic reviews. This includes random testing of outputs against actual sale prices to gauge accuracy (as the AVM rule requires).

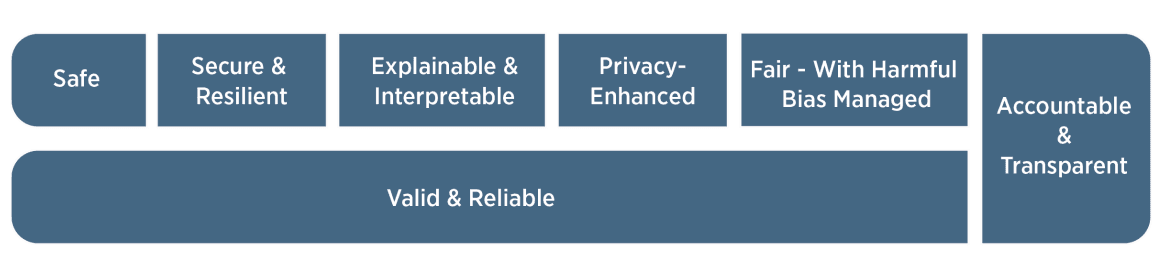

Using an established framework, such as the National Institute of Standards and Technology AI Risk Management Framework, is wise.

“Characteristics of trustworthy AI systems” from NISTs Artificial Intelligence Risk Management Framework (AI RMF 1.0)

RICS’s standard will require surveyors to have a basic understanding of their AI tools’ workings and limitations. Similarly, the CFPB has made clear that if a lender can’t explain an AI’s decision (e.g., why it gave a certain appraisal value or credit decision), they shouldn’t be using it.

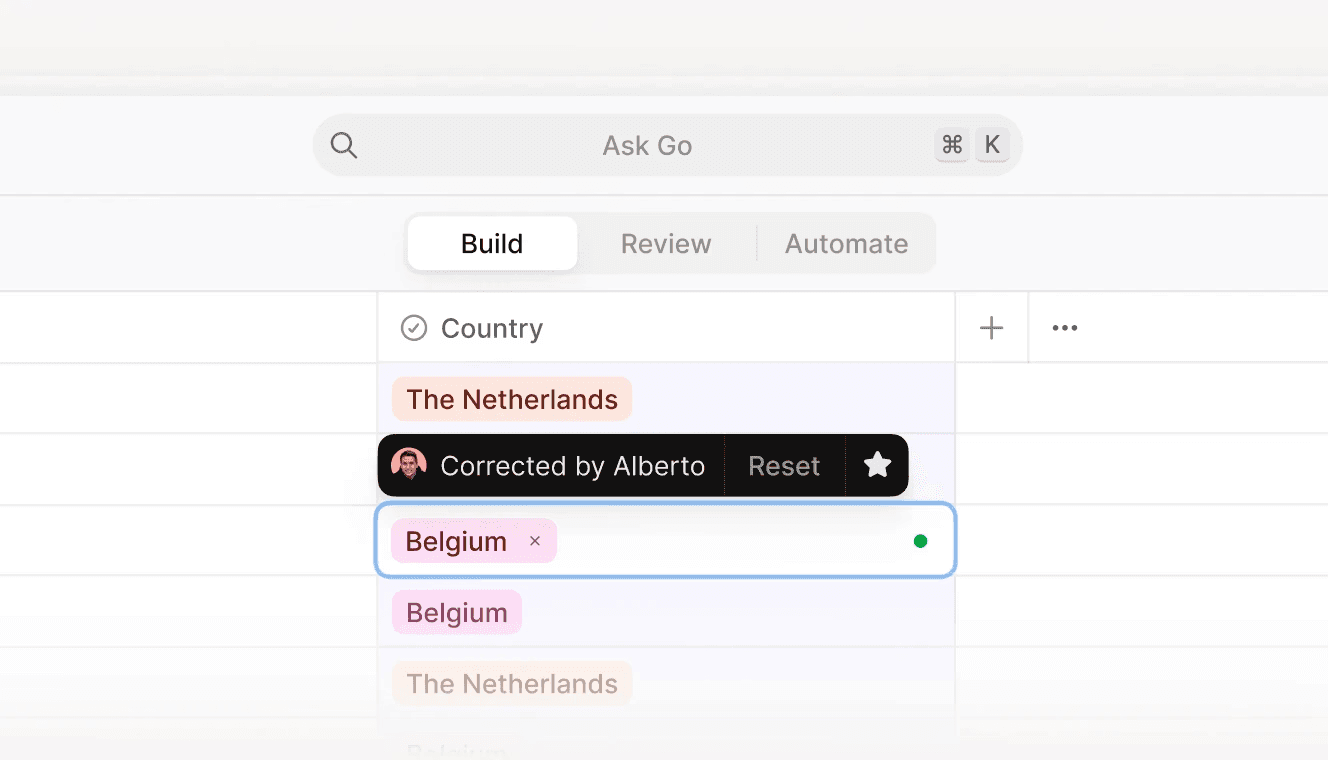

Keep Humans in the Loop

AI should augment, not replace the human expertise in appraisal. Establish a workflow where AI provides recommendations or drafts, and a human reviews and approves or adjusts them when flagged or needed.

A user making a manual correction in V7 Go.

Maintaining this human-in-the-loop approach ensures that professional judgment and local knowledge temper the AI’s output. It also provides a safety net to catch any AI mistakes.

To paraphrase an oft-used quote about the rise of AI,

“AI won’t replace appraisers, but appraisers who use AI effectively will replace those who don’t.”

Encourage appraisers to see AI as their 24/7 assistant, handling repetitive tasks so they can focus on analysis and verification. Celebrate time saved or improved accuracy due to AI to build confidence.

On the client side, if you’re providing AI-enhanced products like an automated review report, explain the benefits to them (faster turnaround, extra layer of review and so on).

What are the best AI tools for real estate?

Part of best practice includes choosing the right vendors to partner with. The best choice will depend on your particular requirements.

Property appraisal documents being analyzed in V7 Go

Some of the notable AI tools for real estate valuation include:

V7 Go: V7 Go is a document intelligence platform that goes far beyond standard document processing, combining advanced technologies like chain-of-thought reasoning and multimodal processing to tackle complex real estate workflows. Flexible integrations connect seamlessly with the rest of an appraisal tech stack, allowing firms to introduce automation without disrupting existing systems.

HouseCanary and ClearCapital: They offer advanced AVMs and analytics platforms for home valuations that many lenders use, blending AI with appraisal data.

Zillow’s Zestimate and Redfin Estimate: These are well-known consumer-facing AVMs. While not used for official appraisals, they show the capabilities of large-scale AI valuation models

Restb.ai and Cape Analytics: These specialize in computer vision for real estate – e.g., analyzing listing photos or aerial images to score property condition and features at scale. They often integrate with valuation workflows to enhance accuracy.

Reggora and other appraisal tech platforms: Some companies combine AI with end-to-end appraisal management. They might auto-assign the best appraiser, use AI QC checks on reports, and incorporate AVMs for audit.

Generic AI like ChatGPT or Bard: These can be useful to real estate professionals for tasks like writing property descriptions, summarizing market trends, or brainstorming investment ideas. They’re not real estate-specific, but many agents and appraisers use them as productivity boosters.

What’s Next for AI in Property Appraisal?

AI in property appraisal will bring even deeper changes to the industry over the coming years. Here are a few ways AI could further shape property valuation in the future:

Deeper Data Integration

Future AI-driven appraisals will tap into an even wider array of data. We can expect models to integrate Internet of Things (IoT) sensor data from smart homes, such as a sensor that monitors building health or energy efficiency could inform value. Building Information Modeling (BIM) data might be used for commercial property valuations, giving precise info on building materials and structural details. City planning databases might feed in information about upcoming developments or zoning changes automatically.

The richer the data portrait of a property and its surroundings, the more nuanced the valuation. AI will be the glue to merge these disparate data streams and extract meaningful value indicators.

Regulatory Evolution and Standard

We will see more formal guidelines for AI in valuation. The RICS global standard taking effect in 2026 is likely the first of many.

In the U.S., the PAVE task force recommendations and the new AVM rule are early steps, but we might eventually have something like a certification or scoring system for AVMs (imagine an “AVM quality seal” that indicates it meets certain accuracy and fairness criteria).

Model governance expectations will harden: lenders might need an “AI audit” function to regularly report on their valuation models’ performance and bias testing to regulators. These evolutions will further legitimize AI in appraisal, but also raise the bar for participants to use it responsibly. In essence, responsible AI will become a norm, not an option.

Global Adoption and Emerging Markets

As countries digitize their land records and sales data, AI-based valuations will spread globally. Emerging markets that historically lacked reliable appraisal processes might leapfrog straight to AI-assisted valuations once they have data in place.

We may also see more cross-border valuation models as global investors seek AI insight on properties anywhere in the world. However, these models will need localization and local market knowledge will still be crucial, so expect partnerships between global tech firms and local real estate experts.

Standardization of data, like international valuation data standards, will facilitate AI’s spread. The end result could be more efficient property markets world-wide, with AI helping to stabilize and bring confidence in valuations even where the human appraiser profession is smaller.

Augmented Appraisers and New Roles

Rather than AI replacing appraisers, the role of the appraiser will likely shift. Appraisers will spend less time on rote form-filling or chasing down comps, and more time on investigative and judgment tasks.

They’ll also serve as a crucial check on fairness and reasonableness, essentially being the conscience and common sense of the process.

The appraisal education might include more data science basics or AI interpretation skills. We already see this trend: forward-thinking appraisers incorporate AI tools into their workflow and market themselves as being more efficient and data-savvy, which gives them an edge.

Speaking of augmented appraisers…

Will AI Replace Appraisers?

This is a question on many minds, and the resounding consensus is no, AI will not outright replace human appraisers or surveyors in the foreseeable future. Instead, we are headed toward a hybrid model where AI handles certain tasks and humans focus on others.

Appraisal duties require a human touch by nature or by law

Many regulatory frameworks require human judgment in the loop. Mortgage lenders and courts often need a credentialed professional’s sign-off on value, not just a number from a model.

Additionally, appraisers don’t just determine value, they also assess physical property aspects like structural soundness, safety issues, and code compliance during an inspection. Current AI and remote technologies cannot fully replicate a trained person walking through a home, feeling the springy floor, smelling mold, or noticing subtle signs of a problem.

Importantly, certain segments like high-end custom properties, complex commercial valuations, or appraisal reviews will likely always demand intensive human expertise. Human creativity and paired with deep market knowledge have an edge in such scenarios.

Appraisers carry professional liability and trust

When a human appraiser signs a report, they are accountable . If they were negligent or biased, there’s a person to answer for it (and they typically have indemnity insurance).

With AI appraisal, who is responsible if it gets a value wrong and someone incurs a loss? That liability question is a big barrier. In practice, lenders and clients still want someone who can explain the valuation, bring their expertise, and own the outcomes.

Transform Your Property Appraisal Workflows With AI

What used to be a slow, manual workflow can now be enhanced and accelerated with data analytics, computer vision, automated document workflows and more. We’ve seen how AI serves as a practical co-pilot for appraisers, reducing turnaround times and improving consistency. At the same time, new rules in the U.S. and UK are creating a strong framework of ethics and accountability.

In other words, AI has earned its place in the appraisal toolkit, provided we wield it with care.

If you’re a real estate appraiser, lender, or investor, now is the time to explore how AI can enhance your property valuation workflows.

Get in touch with us to see how V7’s solutions could accelerate and enhance your appraisal process across the entire workflow, from initial property data capture to final quality check.

Can AI do property appraisals?

AI can perform a large portion of the property appraisal process (data gathering, comparable analysis, preliminary value estimation). However, it cannot yet do a complete appraisal entirely on its own in most cases. Automated Valuation Models can instantly estimate a home’s value using data and machine learning. For example, lenders often use AVMs to get a quick read on value or even waive a traditional appraisal for low-risk loans. However, a formal appraisal, especially for a mortgage, typically requires a licensed human appraiser’s involvement.

+

Is AI more useful for commercial or residential property valuation?

AI is making inroads in both residential and commercial valuation, but its usage and usefulness differ due to data differences. The homogeneous nature of many houses and a high volume of sales data make residential properties ideal for AVMs and image analysis. For Commercial real estate valuations, adoption is slower. There are fewer transactions and each asset tends to be more unique. However, AI is used widely in commercial valuation for things like market forecasting and trend analysis, document processing and comparable searches.

+

Is AI for property valuation accurate?

AI-driven valuations can be very accurate for many properties, but accuracy varies with context and data. In general, the top AVMs have achieved surprisingly low error rates on average. For example, Zillow’s Zestimate is reported to be within about 2% of the sale price for half of on-market homes. However, accuracy isn’t uniform. AI tends to do best on standard homes in areas with lots of sales data.

+

How is AI used in real estate investing?

AI supports investors by analyzing massive amounts of market data to spot trends, identify undervalued properties, and forecast price movements. It can scan property listings, historical sales, demographic changes, and even alternative signals like job growth or infrastructure projects to uncover opportunities that humans might miss.

+

How much faster can AI make the appraisal process?

+

Imogen is an experienced content writer and marketer, specializing in B2B SaaS. She particularly enjoys writing about the impact of technology on sectors like law, finance, and insurance.